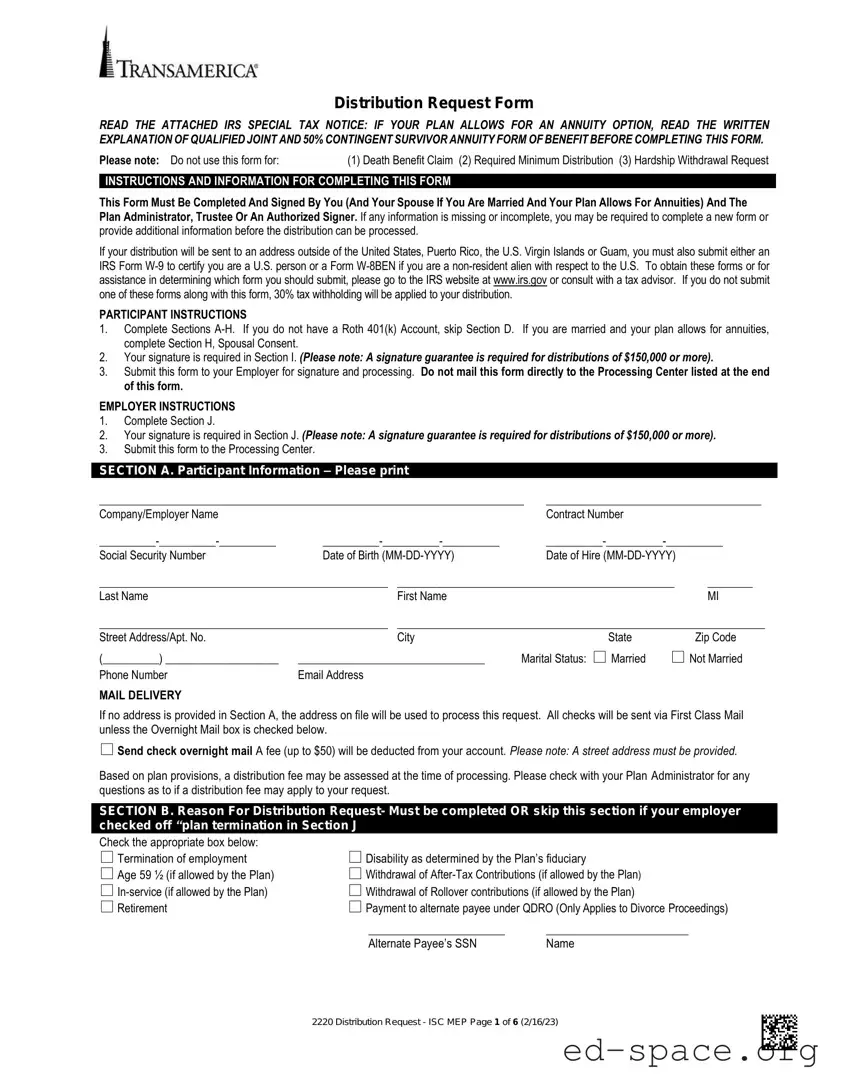

The Transamerica 401K Withdrawal form is an essential document for individuals seeking to access their retirement funds. It requires careful completion and submission to ensure a smooth withdrawal process. Before filling out the form, participants must read the attached IRS Special Tax Notice, which provides important tax information related to their distributions. The form is not intended for certain requests, such as death benefit claims or hardship withdrawals. Participants must complete several sections, including personal information, the reason for withdrawal, and the desired form of payment. If married, spousal consent may also be necessary. Missing or incomplete information could delay the processing of the request, so attention to detail is crucial. Once completed, the form must be submitted to the employer for processing, rather than mailed directly to the processing center. Understanding the various options for distribution, including rollovers and cash payments, is vital for making informed decisions about retirement savings. Additionally, participants should be aware of potential tax implications and fees associated with their withdrawals.

| Fact Name | Description |

|---|---|

| Eligibility Requirements | Participants must complete and sign the form, and if married, their spouse must also sign if the plan allows for annuities. |

| Distribution Options | Participants can choose from several distribution methods, including direct rollovers, cash distributions, or combinations of both. |

| Tax Implications | Federal income tax withholding may apply, especially if the distribution is not rolled over. A 20% withholding applies to certain distributions. |

| State-Specific Considerations | State income tax rules vary. Participants should consult state laws regarding withholding requirements, as some states mandate withholding while others allow for independent elections. |

Completing the Transamerica 401K Withdrawal form is an important step in accessing your retirement funds. It is essential to follow the instructions carefully to ensure that your request is processed without delays. After you submit the completed form to your employer, it will need to be signed and processed by them before it can be sent to the processing center.

What is the purpose of the Transamerica 401K Withdrawal form?

The Transamerica 401K Withdrawal form is used to request a distribution from your 401(k) retirement plan. This form allows you to specify how you want to receive your funds, whether through a direct rollover to another retirement account, a combination of cash and rollover, or a cash distribution. It is essential to complete this form accurately to ensure your withdrawal is processed without delays.

Who needs to sign the Transamerica 401K Withdrawal form?

The form must be completed and signed by you, the participant. If you are married and your plan allows for annuities, your spouse must also sign the form to provide spousal consent. Additionally, the Plan Administrator, Trustee, or an authorized signer must sign the form to validate the request. Missing signatures can lead to processing delays or require a new form submission.

What should I do if I have missing information on the form?

If any information is incomplete or missing, you may be required to fill out a new form or provide additional information before your distribution can be processed. It is crucial to double-check all sections of the form, including your personal information and distribution preferences, to avoid any issues.

Are there any fees associated with the withdrawal?

There may be fees associated with processing your distribution request, depending on your plan provisions. It is advisable to check with your Plan Administrator for details about any potential distribution fees that may apply. Additionally, if you choose to receive your distribution via overnight mail, there will be an express charge of $25 deducted from your check.

What happens if I do not complete the required minimum distribution (RMD)?

If you are required to take a minimum distribution for the current year and have not satisfied this requirement, your RMD must be completed and made payable to you before your direct rollover request can be processed. Failing to take your RMD can lead to tax penalties, so it is important to address this requirement promptly.

Incomplete Sections: Failing to complete all required sections (A-H) can lead to delays. Ensure that each section relevant to your situation is fully filled out.

Missing Signatures: Neglecting to sign the form in Section I is a common oversight. Your signature, and your spouse's if applicable, is essential for processing.

Incorrect Payment Option: Selecting the wrong payment option in Sections C or D can cause issues. Review your choices carefully to ensure they align with your needs.

Skipping Spousal Consent: If you are married and your plan requires spousal consent, failing to complete Section H can halt your request. Always check if this is necessary.

Improper Submission: Submitting the form directly to the Processing Center instead of your employer can lead to rejection. Always follow the submission guidelines outlined in the instructions.

Ignoring Tax Implications: Overlooking the tax withholding requirements can result in unexpected tax liabilities. Familiarize yourself with the tax implications of your distribution.

Missing Contact Information: Not providing a current mailing address in Section A means your distribution may be sent to an outdated address. Always double-check this information.

Failure to Attach Necessary Documentation: If you have an outstanding loan, not including payment details or relevant documentation can delay processing. Make sure to include everything required.

When considering a withdrawal from your Transamerica 401(k), several other forms and documents may be necessary to complete the process. Each of these documents serves a specific purpose and helps ensure that your request is handled correctly. Below is a list of commonly used forms alongside the Transamerica 401(k) Withdrawal form.

Understanding these forms and documents can help streamline the withdrawal process from your Transamerica 401(k). Always ensure that you have all necessary paperwork completed and submitted to avoid delays in receiving your funds.

The Transamerica 401K Withdrawal form shares similarities with several other financial and legal documents. Below is a list of documents that resemble it in terms of purpose, structure, or required information.

Things to Do:

Things Not to Do:

Understanding the Transamerica 401K Withdrawal form is essential for making informed decisions about your retirement savings. However, there are several misconceptions that can lead to confusion. Here are six common misconceptions:

By clarifying these misconceptions, you can navigate the Transamerica 401K Withdrawal form with greater confidence and understanding.

Understanding the Transamerica 401K Withdrawal form is essential for making informed decisions about your retirement funds. Here are some key takeaways to consider:

By keeping these points in mind, you can navigate the withdrawal process more smoothly and make the most of your retirement savings.