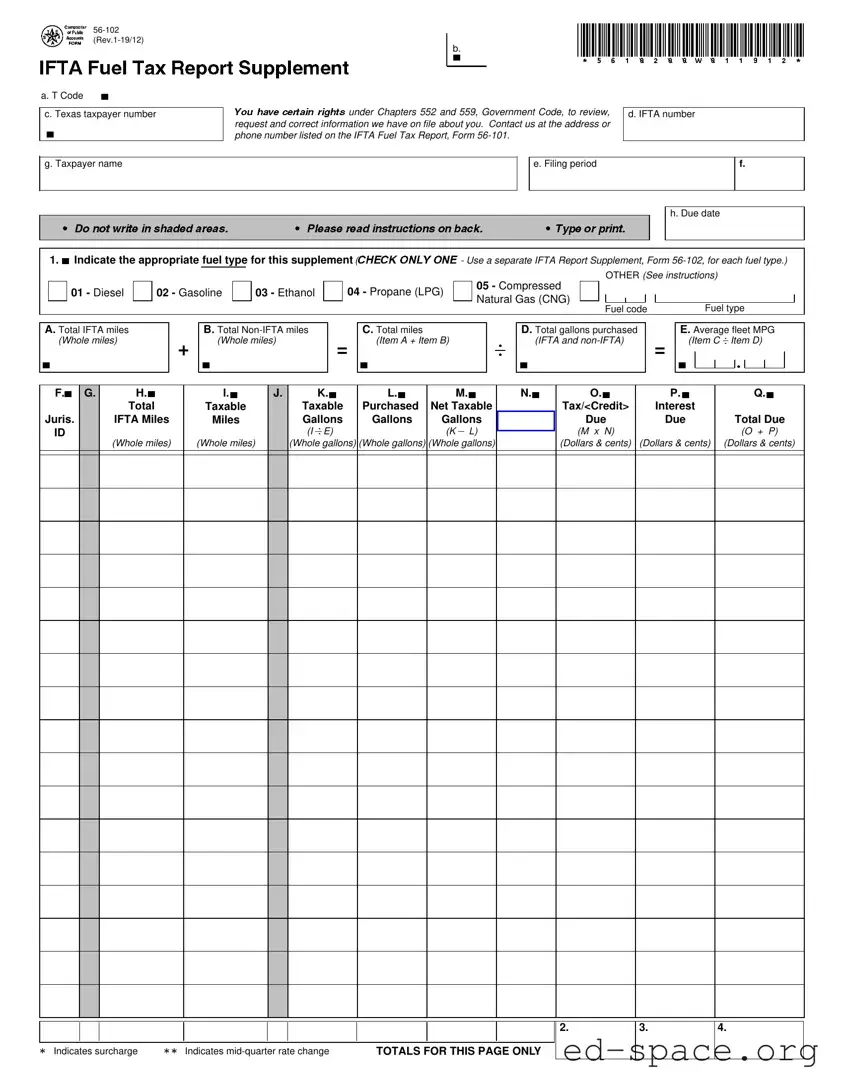

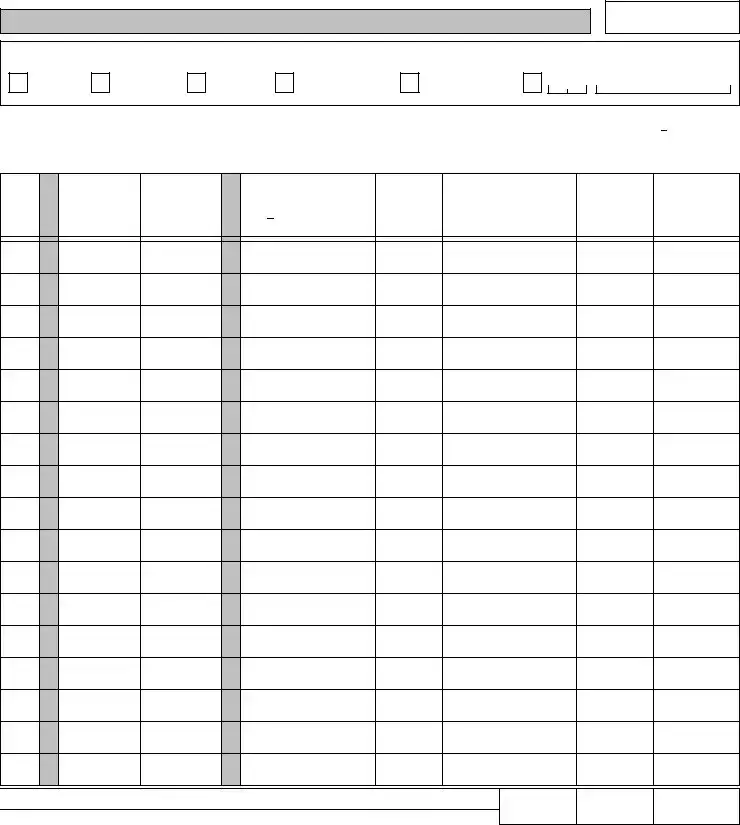

The Texas IFTA Form, specifically Form 56-102, serves as a crucial document for businesses engaged in interstate transportation, particularly those utilizing qualified motor vehicles. This form is designed to facilitate the reporting of fuel usage across jurisdictions, ensuring compliance with the International Fuel Tax Agreement (IFTA). Key components of the form include the identification of fuel types, such as diesel, gasoline, and compressed natural gas, which must be clearly marked for accurate reporting. Additionally, users are required to provide detailed mileage information, differentiating between IFTA miles and non-IFTA miles, as well as total gallons of fuel purchased. The form also necessitates calculations related to average fleet miles per gallon, taxable miles, and the corresponding tax rates for each jurisdiction. It is essential for filers to account for any surcharges applicable in certain jurisdictions and to report any changes in tax rates that may occur within a quarter. The final sections of the form summarize the total tax due or credits applicable, along with any interest accrued from late filings. Accurate completion of Form 56-102 is vital for maintaining regulatory compliance and avoiding potential penalties.

| Fact Name | Description |

|---|---|

| Form Number | The Texas IFTA form is officially designated as Form 56-102. |

| Purpose | This form is used to report fuel tax information for vehicles operating under the International Fuel Tax Agreement. |

| Filing Frequency | Taxpayers must file this report quarterly to remain compliant with state and federal regulations. |

| Due Date | The due date for filing is the last day of the month following the end of each quarter. |

| Fuel Types | Reportable fuel types include Diesel, Gasoline, Ethanol, Propane, and Compressed Natural Gas, among others. |

| Tax Calculation | Tax is calculated based on the taxable gallons consumed and the applicable tax rate for each jurisdiction. |

| Interest on Late Payments | If filed late, interest will accrue on the tax due from the report's due date until payment is made. |

| Governing Laws | This form is governed by Chapters 552 and 559 of the Texas Government Code. |

Filling out the Texas IFTA form requires careful attention to detail. Each section must be completed accurately to ensure compliance with state regulations. Follow these steps to fill out the form correctly.

What is the Texas IFTA Form 56-102 used for?

The Texas IFTA Form 56-102 is used to report fuel consumption and mileage for vehicles operating under the International Fuel Tax Agreement (IFTA). This form helps track fuel usage and ensures that taxes are paid appropriately based on the miles traveled in different jurisdictions. It is essential for maintaining compliance with state and federal tax regulations related to fuel use.

How do I fill out the fuel type section on Form 56-102?

When filling out the fuel type section, you need to indicate the appropriate fuel type by checking the corresponding box. The options include Diesel, Gasoline, Ethanol, Propane, and Compressed Natural Gas. If your fuel type is not listed, check the "OTHER" box and provide the specific fuel code and type. Remember, a separate Form 56-102 is required for each fuel type you use.

What information is required for reporting mileage on the form?

You must report total IFTA miles, total non-IFTA miles, and total miles traveled. Total IFTA miles include all miles traveled in IFTA jurisdictions by qualified vehicles using the indicated fuel type. Total non-IFTA miles cover miles traveled in jurisdictions not part of IFTA. The total miles is simply the sum of both IFTA and non-IFTA miles. Accurate reporting is crucial for tax calculations.

What should I do if I operated in jurisdictions with different tax rates during the quarter?

If you traveled in jurisdictions that changed their tax rates mid-quarter, you will need to report the miles traveled during each rate period separately on the form. This means listing the jurisdiction multiple times on the supplement for each rate change. If you did not travel during a specific rate period, you should enter zeros for that period to ensure accurate reporting.

What happens if I file my IFTA report late?

If you file your IFTA report after the due date, you will incur interest on the tax due for each jurisdiction. The interest is calculated from the due date until the payment is postmarked. To avoid penalties, ensure that your report is postmarked by the last day of the month following the end of the quarter. If this date falls on a weekend or holiday, the deadline extends to the next business day.

Incorrect Fuel Type Selection: One common mistake is failing to accurately indicate the appropriate fuel type. It is crucial to check only one box for the fuel type being reported. Using the wrong fuel type can lead to incorrect calculations and potential penalties.

Missing Jurisdiction Entries: Another frequent error involves leaving out jurisdictions where travel occurred. All jurisdictions where miles were driven must be reported, even if no tax is owed. Failing to include this information can result in discrepancies.

Inaccurate Mileage Reporting: People often miscalculate total miles. It is essential to report both IFTA miles and non-IFTA miles accurately. The total miles must reflect all travel, as errors can lead to tax issues.

Omitting Taxable Gallons: Some individuals forget to calculate and report the taxable gallons consumed in each jurisdiction. This oversight can significantly affect the total tax due and lead to complications with tax authorities.

Failure to Keep Receipts: Not retaining fuel purchase receipts is a common mistake. Receipts are essential for verifying the gallons purchased and must be kept for all claimed purchases to avoid disputes.

Ignoring Rate Changes: Some filers neglect to account for mid-quarter tax rate changes. If a jurisdiction's tax rate changes during the quarter, it is necessary to report the miles traveled under each rate separately.

Late Filing and Interest Calculation: Lastly, individuals often file late without considering the interest due on unpaid taxes. It is important to file on time to avoid additional charges and accurately calculate any interest owed.

When dealing with the Texas IFTA form, several other documents often accompany it to ensure compliance with tax regulations and accurate reporting. Each of these forms serves a specific purpose, aiding in the collection and reporting of fuel taxes for commercial vehicles. Here’s a brief overview of the key documents you might encounter alongside the Texas IFTA form.

Understanding these documents can streamline the filing process and help ensure compliance with IFTA regulations. Keeping organized records not only simplifies your reporting but also protects you in case of an audit. By being proactive and thorough, you can navigate the complexities of fuel tax reporting with confidence.

The Texas IFTA form, specifically Form 56-102, shares similarities with several other important documents related to fuel taxes and vehicle operations. Here’s a breakdown of six such documents:

When filling out the Texas IFTA form, there are important guidelines to follow. Here’s a list of things to do and avoid:

Understanding the Texas IFTA form can be challenging, and several misconceptions often arise. Here are eight common misunderstandings about the Texas IFTA form, along with clarifications:

This is incorrect. The Texas IFTA form is applicable to various fuel types, including gasoline, ethanol, propane, and compressed natural gas. Each fuel type requires a separate report supplement.

Submitting the form without complete information can lead to delays or penalties. It's crucial to ensure all sections are filled out accurately before submission.

All miles traveled, including non-IFTA miles, must be reported on the form. This includes travel in jurisdictions outside of IFTA member states.

This is a misunderstanding. Keeping receipts is essential for verifying fuel purchases claimed on the form. Without them, you may face challenges during audits.

Tax rates vary by jurisdiction. It's important to check the current rates for each area where fuel was purchased and report them accurately.

Filing late incurs interest on the tax due. It's important to calculate this interest and include it in your total amount due on the form.

If there are mid-quarter rate changes, you must report taxable gallons separately for each rate period. This ensures accurate tax calculations.

While the IFTA form is typically filed quarterly, it must be postmarked by the last day of the month following the end of each quarter to avoid penalties.

Ensure accurate completion of the Texas IFTA form by providing your taxpayer name and IFTA number ID. Do not write in shaded areas.

Indicate the fuel type by checking only one box. Use a separate Form 56-102 for each fuel type.

Report all miles traveled in both IFTA and non-IFTA jurisdictions. This includes both taxable and non-taxable miles.

Keep all receipts for fuel purchases. Only gallons removed for use in qualified vehicles can be claimed.

Be aware of fuel tax surcharges that may apply in certain jurisdictions. These surcharges must be calculated and reported on the form.

Submit the form by the due date to avoid penalties. Reports must be postmarked no later than the last day of the month following the end of the quarter.