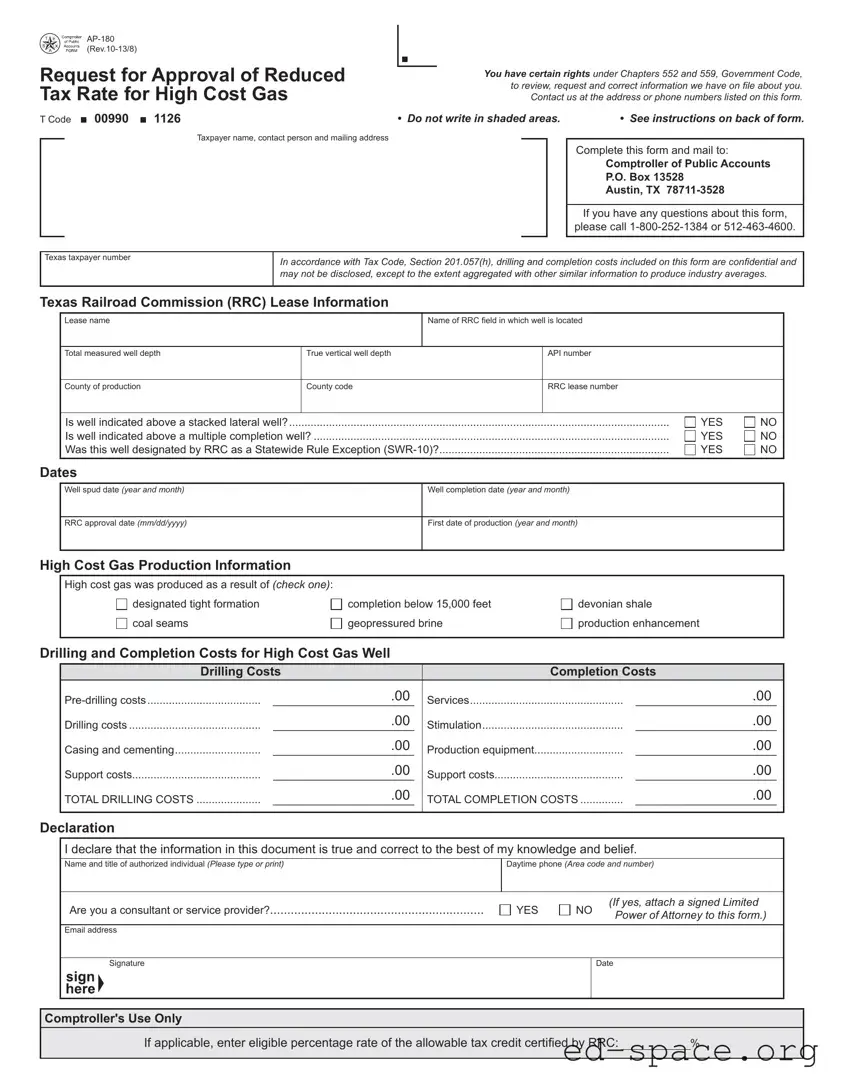

The Texas AP-180 form serves as a critical tool for natural gas producers seeking to obtain a reduced tax rate for high-cost gas wells certified by the Texas Railroad Commission (RRC). This form requires detailed information about the taxpayer, including their name, contact details, and Texas taxpayer number, alongside specific lease information such as the well's depth, API number, and production county. Producers must also disclose drilling and completion costs associated with high-cost gas production, which can include various categories like pre-drilling, drilling, casing, cementing, and completion costs. The form emphasizes the confidentiality of certain drilling and completion costs, aligning with Texas Tax Code regulations. Additionally, it outlines the necessary steps for filing, including the requirement of a certification letter from the RRC and the importance of adhering to specific deadlines to avoid penalties. Producers must ensure that the information provided is accurate and complete, as it plays a pivotal role in determining eligibility for tax credits and exemptions related to high-cost gas production. Understanding the intricacies of the AP-180 form is essential for navigating the complexities of Texas's tax landscape in the natural gas industry.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Texas AP-180 form is used to request approval for a reduced tax rate for high cost gas wells certified by the Texas Railroad Commission (RRC). |

| Filing Requirement | Producers seeking a reduced tax rate must file Form AP-180. This includes submitting a Limited Power of Attorney if a consultant or service provider files on behalf of a taxpayer. |

| Confidentiality Clause | According to Tax Code, Section 201.057(h), drilling and completion costs reported on this form are confidential and cannot be disclosed except in aggregated form. |

| Filing Deadline | Form AP-180 must be filed within 180 days after the first production date or within 45 days after RRC approval to avoid a 10% penalty. |

| Required Documentation | A letter of certification from the Texas Railroad Commission must accompany each completed Form AP-180. |

| Exemption Duration | The exemption for an approved high cost gas well lasts either for 120 months from the first production date or until the cumulative tax savings equal 50% of total drilling and completion costs. |

| Online Resources | Detailed information about the reduced tax rate for high cost gas leases can be found on the Texas Comptroller's website. |

| Contact Information | For questions regarding Form AP-180, individuals can contact the Texas Comptroller's office at 1-800-252-1384 or 512-463-4600. |

Filling out the Texas AP 180 form requires attention to detail and accurate information. After completing the form, you will need to submit it to the Comptroller of Public Accounts along with any necessary supporting documents. Make sure to check for completeness before mailing your application to avoid delays.

What is the purpose of the Texas AP-180 form?

The Texas AP-180 form is used by gas producers to request a reduced tax rate for gas wells that have been certified as high cost gas wells by the Texas Railroad Commission (RRC). This form allows producers to recoup credits for taxes previously paid on these wells, making it an important document for those in the natural gas industry.

Who needs to file the AP-180 form?

Any producer seeking a reduced tax rate for high cost gas wells must file the AP-180 form. If a consultant or service provider is filing on behalf of a taxpayer, a Limited Power of Attorney must accompany the form. This ensures that the appropriate parties are authorized to handle the tax matters related to the high cost gas wells.

What information is required when filing the AP-180 form?

When completing the AP-180 form, you will need to provide detailed information about the gas well, including the lease name, RRC field name, total measured well depth, and various costs associated with drilling and completion. Additionally, a copy of the certification letter from the Texas Railroad Commission must be submitted with the form.

When should the AP-180 form be filed?

The AP-180 form should be filed within specific time frames to avoid penalties. Generally, it must be submitted within 180 days after the first production date or 45 days after RRC approval. If not filed by these deadlines, the tax exemption could be reduced by 10 percent. Additionally, credit-amended reports must be filed within four years from the due date of a production period to recoup previously paid taxes.

What are the consequences of not filing the AP-180 form on time?

Failure to file the AP-180 form within the required deadlines can result in a 10 percent reduction in the tax exemption or deduction for the period after the 180th day from the first day of production. This emphasizes the importance of timely filing to ensure that producers receive the full benefits of the reduced tax rate.

What types of costs can be included on the AP-180 form?

Costs related to drilling and completion can be included on the AP-180 form. This encompasses pre-drilling costs, drilling costs, casing and cementing expenses, and completion costs. However, it is important to note that marketing costs incurred after the outlet of a lease separator are not included. Detailed categories help ensure that only qualifying expenses are reported.

Where can I find more information about the AP-180 form?

For additional details on the AP-180 form and the reduced tax rate for high cost gas leases, you can visit the Texas Comptroller's website. There, you will find comprehensive information and resources, including links to relevant forms and guidelines.

Neglecting to Read Instructions: Many individuals overlook the instructions provided on the back of the AP-180 form. This can lead to incomplete or incorrect submissions. Understanding the requirements is essential for a successful application.

Omitting Required Documentation: A common mistake is failing to include the necessary letter of certification from the Texas Railroad Commission. This document is crucial for the approval process, and without it, the application may be rejected.

Incorrectly Reporting Costs: Some applicants miscalculate or misreport drilling and completion costs. It is vital to ensure that all costs are accurately categorized and totaled to avoid discrepancies that could affect the tax rate approval.

Missing Deadlines: The deadlines for filing the AP-180 form are strict. Failing to submit the form within the specified time frames can result in penalties or loss of tax credits. Keeping track of these dates is essential for compliance.

Improper Signature or Authorization: The declaration section requires a signature from an authorized individual. If this section is not completed correctly, or if a consultant files without a Limited Power of Attorney, the application may be invalidated.

Ignoring Shaded Areas: The form contains shaded areas where no information should be entered. Ignoring this guideline can lead to confusion and potential rejection of the application.

The Texas AP-180 form is essential for producers seeking a reduced tax rate for high-cost gas wells certified by the Texas Railroad Commission. However, this form often accompanies various other documents that provide necessary information or support for the application process. Below is a list of commonly used forms and documents that can enhance or complement the AP-180 filing.

In summary, the Texas AP-180 form is part of a broader set of documents that together ensure compliance and facilitate the process of securing tax reductions for high-cost gas wells. Understanding the role of each document helps producers navigate the complexities of tax filings and regulatory requirements more effectively.

The Texas AP-180 form is a critical document for producers seeking a reduced tax rate for high-cost gas wells. Several other forms share similarities with AP-180, particularly in terms of purpose, required information, and the context in which they are used. Here’s a list of nine documents that are similar to the Texas AP-180 form:

Each of these forms plays a vital role in the regulatory landscape of Texas oil and gas production, ensuring compliance and facilitating the appropriate tax considerations for producers.

When filling out the Texas AP 180 form, there are several important dos and don'ts to keep in mind. Here’s a helpful list to guide you through the process:

By following these guidelines, you can help ensure that your submission is processed smoothly and efficiently. Remember, accuracy and attention to detail are key when dealing with tax forms.

Understanding the Texas AP-180 form is crucial for producers seeking tax reductions on high-cost gas wells. However, several misconceptions can lead to confusion. Here are five common misunderstandings about this form:

Being aware of these misconceptions can help producers navigate the complexities of the Texas AP-180 form more effectively. Understanding the requirements and limitations is essential for maximizing tax benefits in the oil and gas industry.

Here are some key takeaways about filling out and using the Texas AP-180 form:

Following these guidelines will help ensure a smoother process when using the Texas AP-180 form.