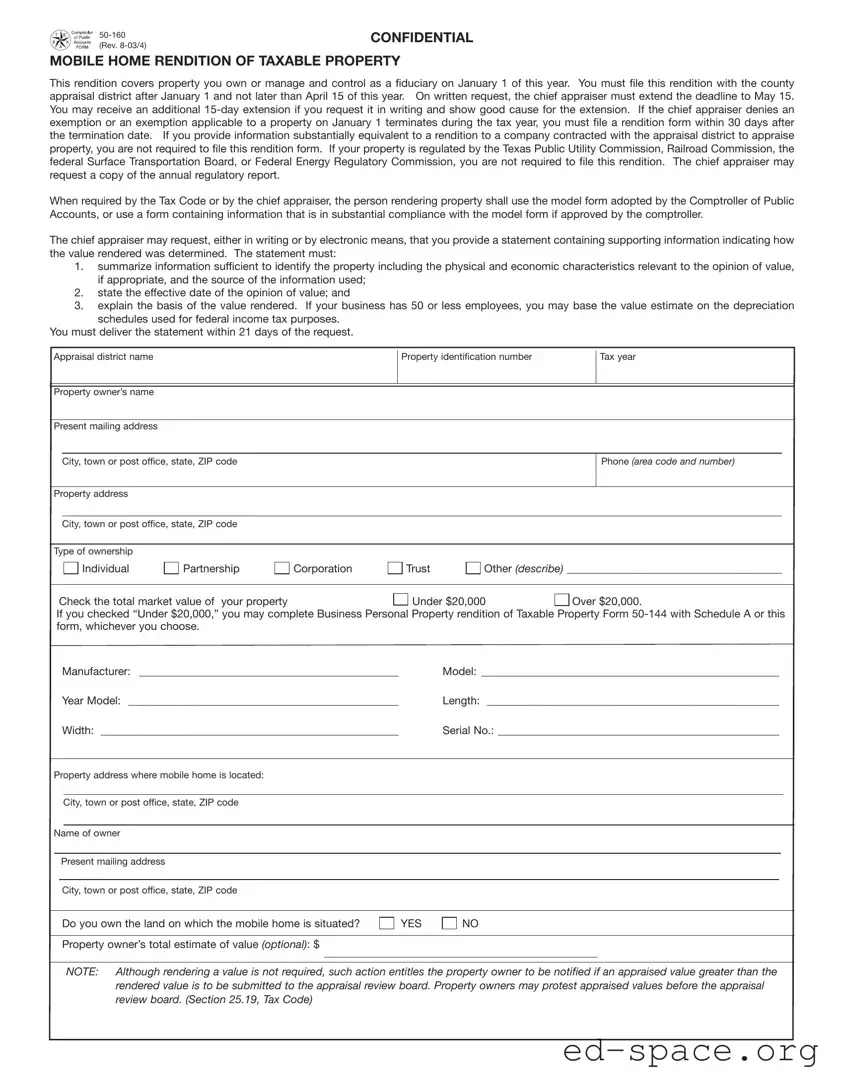

The Texas 50-160 form, also known as the Confidential Mobile Home Rendition of Taxable Property, serves as an essential document for property owners and fiduciaries managing mobile homes. This form must be submitted to the county appraisal district between January 1 and April 15 of the tax year, ensuring that property values are accurately reported for taxation purposes. In certain circumstances, such as when an exemption is denied or terminates, property owners are required to file this form within 30 days of the change. The form collects vital information, including property identification details, ownership type, and market value estimates. For businesses with 50 or fewer employees, the form allows the use of federal depreciation schedules to estimate property value. It is important to note that if a property owner provides information that is equivalent to a rendition to a contracted appraisal company, filing the 50-160 may not be necessary. Additionally, if the property falls under specific regulatory commissions, the requirement to file is waived. The chief appraiser may request further supporting documentation to clarify how the value was determined, reinforcing the need for accuracy and transparency in property reporting. Completing this form correctly can help property owners stay informed about appraised values and exercise their rights to protest if needed.

| Fact Name | Description |

|---|---|

| Filing Deadline | The Texas 50-160 form must be filed with the county appraisal district after January 1 and no later than April 15 of the current year. An extension to May 15 may be granted upon written request to the chief appraiser. |

| Extension Policy | If a property owner shows good cause, they may receive an additional 15-day extension. This request must also be submitted in writing. |

| Exemption Reporting | Property owners must file a rendition within 30 days if an exemption is denied or if an exemption applicable to the property terminates during the tax year. |

| Regulatory Exceptions | Owners of properties regulated by specific agencies, such as the Texas Public Utility Commission, are not required to file the rendition form. |

| Legal Authority | This form is governed by the Texas Tax Code, specifically Section 25.19, which outlines the requirements and penalties associated with filing a rendition. |

Completing the Texas 50-160 form requires accurate information about the mobile home you own or manage. After filling out the form, submit it to the county appraisal district by the specified deadline. Be mindful of possible extensions if needed.

What is the Texas 50 160 form?

The Texas 50 160 form is a confidential mobile home rendition of taxable property. It is used to report property that you own, manage, or control as a fiduciary as of January 1 of the current year. This form must be filed with the county appraisal district between January 1 and April 15. Extensions may be requested under certain conditions.

Who needs to file the Texas 50 160 form?

What are the deadlines for filing the Texas 50 160 form?

The form must be filed between January 1 and April 15 of the tax year. If you need more time, you can request an extension from the chief appraiser, which can extend the deadline to May 15. A further 15-day extension may be granted if you show good cause in writing.

What happens if I miss the filing deadline?

If you fail to file the Texas 50 160 form by the deadline, the chief appraiser will impose a penalty. This penalty is equal to 10 percent of the total taxes due on the property for the current year. Additional penalties may apply if fraudulent information is submitted.

Can I base my property value estimate on my federal tax depreciation schedules?

If your business has 50 or fewer employees, you may use the depreciation schedules from your federal income tax returns to estimate the value of your mobile home. This can simplify the process and ensure compliance with the reporting requirements.

What information do I need to provide on the Texas 50 160 form?

The form requires various details, including your name, mailing address, property identification number, and the market value of your property. You must also provide specifics about the mobile home, such as its model, year, length, width, and serial number. Additionally, you may need to explain how you determined the value if requested by the chief appraiser.

What are the consequences of providing false information on the Texas 50 160 form?

Providing false information can lead to severe penalties, including being charged with a Class A misdemeanor or a state jail felony. If the chief appraiser finds that you filed a false rendition with intent to commit fraud, the penalties can escalate significantly, potentially reaching 50 percent of the total taxes due for the year.

Missing Deadline: Many individuals fail to submit the Texas 50-160 form by the April 15 deadline. While extensions are available, it is crucial to request them in writing and demonstrate good cause.

Incorrect Property Identification: Providing inaccurate or incomplete property identification information can lead to delays or issues with the appraisal process. Ensure that the property identification number and address are correct.

Neglecting to Sign: A common oversight is forgetting to sign and date the form. This step is essential, as the form is not valid without a signature attesting to the truthfulness of the information provided.

Failure to Provide Supporting Information: If requested by the chief appraiser, individuals must submit a statement detailing how the property value was determined. Not providing this information within the specified timeframe can lead to complications.

The Texas 50-160 form is essential for reporting mobile home property for tax purposes. However, there are several other forms and documents that often accompany this submission. Each of these documents plays a crucial role in ensuring compliance with state tax regulations and providing necessary information to the appraisal district. Below is a list of commonly used forms alongside the Texas 50-160.

Understanding these additional forms can help property owners navigate the tax reporting process more effectively. Each document serves a specific purpose and contributes to a comprehensive approach to property taxation in Texas.

The Texas 50-160 form, which is a rendition of taxable property for mobile homes, shares similarities with several other important documents used in property management and taxation. Below are five documents that are comparable to the Texas 50-160 form, along with an explanation of how they relate.

Filling out the Texas 50-160 form can seem daunting, but with a little guidance, you can navigate it smoothly. Here’s a list of what you should and shouldn’t do to ensure your submission is accurate and timely.

By following these guidelines, you can complete the Texas 50-160 form with confidence. Remember, accuracy is key, and timely submission is crucial to avoid penalties. Happy filing!

This form is specifically designed for reporting mobile homes, but it also applies to fiduciaries managing or controlling properties. Thus, various property types may require this form.

Filing the Texas 50-160 form is mandatory for those who own or manage mobile homes as of January 1. Failure to file can result in penalties.

While the standard deadline is April 15, property owners can request an extension to May 15. Additionally, a further 15-day extension may be granted with a valid reason.

If the property is regulated by certain commissions, such as the Texas Public Utility Commission, a valuation statement may not be necessary. However, the chief appraiser can still request supporting information.

Even businesses with 50 or fewer employees must file the form if they own mobile homes. They can base their value estimates on federal depreciation schedules.

No notarization is necessary when signing the Texas 50-160 form. The property owner or designated representative simply needs to attest to the truthfulness of the information provided.

Late filings incur a penalty of 10 percent of the total taxes due. If fraudulent intent is determined, the penalty can increase significantly.

The form must be filed after January 1 and before the April 15 deadline, or within 30 days if an exemption is denied or terminated during the tax year.

When filling out and using the Texas 50-160 form, there are several important points to keep in mind. Here are some key takeaways:

Understanding these aspects can help ensure that you complete the Texas 50-160 form correctly and on time, avoiding potential penalties and complications.