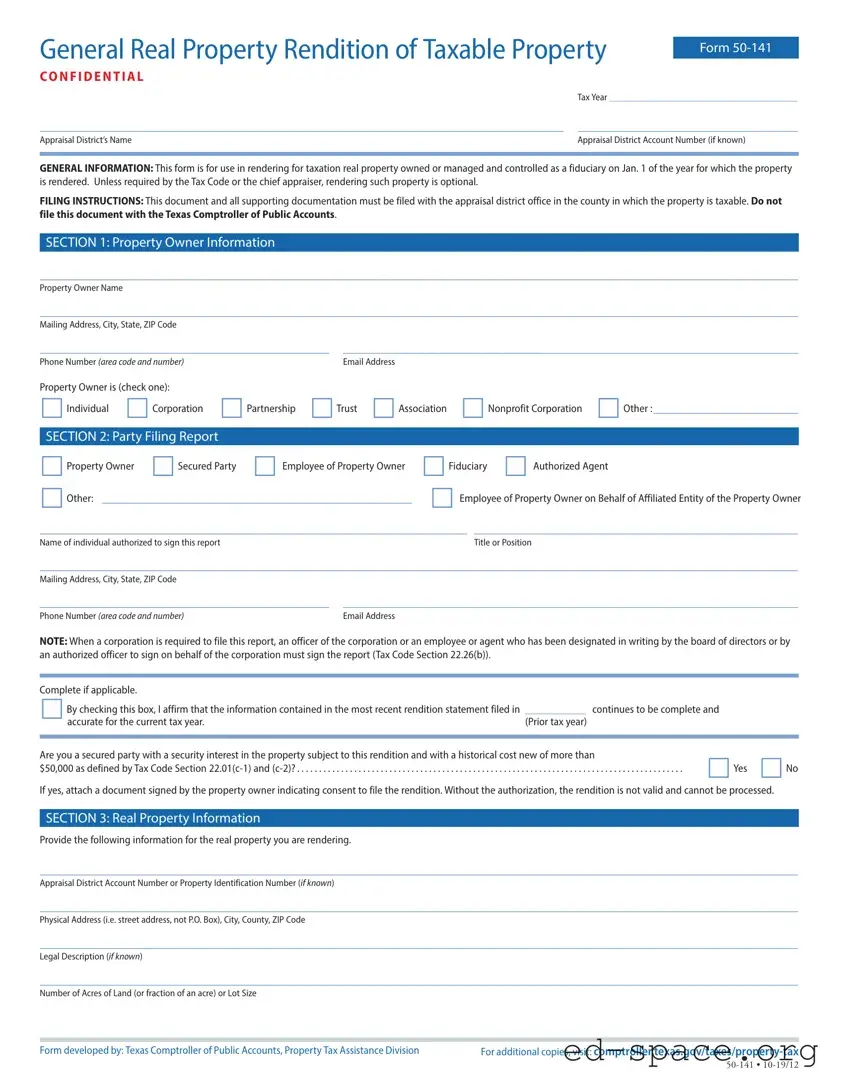

The Texas 50-141 form, officially known as the General Real Property Rendition of Taxable Property, plays a crucial role in the taxation process for real property owned or managed as a fiduciary. This form is designed for use by property owners, including individuals, corporations, and trusts, to report their real property holdings as of January 1 of the tax year. While filing this form is generally optional, it is essential for those who wish to ensure their property is accurately assessed for taxation. The form requires detailed information, including the property owner's name, contact details, and a description of the property being rendered. It also allows for the estimation of the property's market value, which can be beneficial for property owners to receive notifications if the appraised value exceeds their reported value. The completed form must be submitted to the local appraisal district office and not to the Texas Comptroller of Public Accounts. Additionally, the form emphasizes the importance of accuracy, as providing false information can lead to serious legal consequences. Understanding the filing instructions and deadlines is vital for compliance, as these can vary based on property type and regulatory requirements.

| Fact Name | Fact Description |

|---|---|

| Purpose | The Texas 50-141 form is used to render real property for taxation purposes, specifically for properties owned or managed as a fiduciary as of January 1 of the tax year. |

| Governing Law | This form is governed by the Texas Tax Code, particularly Sections 22.01, 22.26, and 25.19. |

| Confidentiality | The information provided on this form is confidential and not open to public inspection, as per Tax Code Section 22.27. |

| Filing Instructions | Submit the completed form and supporting documents to the appraisal district office in the county where the property is taxable. Do not send it to the Texas Comptroller of Public Accounts. |

| Optional Rendering | Rendering property for taxation is generally optional unless mandated by the Tax Code or the chief appraiser. |

| Deadline | The form must be filed by May 15, with an extension of 15 days available upon written request for good cause shown. |

| Signature Requirement | The form must be signed by an authorized individual, and if this individual is not the property owner, notarization is required. |

| Market Value Estimate | Property owners may provide an estimate of the total market value of the property, although this is optional. |

| Secured Party Notification | If a secured party has a security interest in the property, they must obtain the property owner's consent to file the rendition. |

| Contact Information | Contact details for appraisal district offices can be found on the Texas Comptroller’s website for assistance with filing. |

Filling out the Texas 50-141 form is a straightforward process. This form is used to report real property for taxation purposes, and it requires specific information about the property and the owner. After completing the form, it must be submitted to the appropriate appraisal district office in your county.

What is the Texas Form 50-141?

The Texas Form 50-141, also known as the General Real Property Rendition of Taxable Property, is a document used to report real property owned or managed as a fiduciary for tax purposes. This form is specifically for properties that are under fiduciary control as of January 1 of the tax year. While filing this form is generally optional, it can be required by the Tax Code or the chief appraiser.

Who needs to file the Form 50-141?

Any individual or entity that owns or manages real property as a fiduciary may need to file this form. This includes individuals, corporations, partnerships, trusts, associations, and nonprofit corporations. If you are managing property on behalf of someone else, you may also be required to file this form.

Where do I file the Form 50-141?

You must file the Form 50-141 with the appraisal district office in the county where the property is located. It is important to note that this form should not be submitted to the Texas Comptroller of Public Accounts. For accurate filing, check the appraisal district's contact information on the Comptroller’s website.

What is the deadline for filing the Form 50-141?

The deadline for submitting the Form 50-141 depends on the type of property being reported. Generally, the form must be filed after January 1 and no later than April 15. However, there are extensions available under certain conditions, such as an additional 15 days upon written request. Specific deadlines may vary for properties regulated by certain commissions, so it’s best to verify based on your property type.

What information is required on the Form 50-141?

The form requires various pieces of information, including the property owner's name, mailing address, and contact details. You must also provide details about the property itself, such as its physical address, legal description, and an estimate of its total market value. Accurate and complete information is crucial for processing your rendition.

What happens if I don’t file the Form 50-141?

If you fail to file the Form 50-141, you may miss out on important notifications regarding the appraised value of your property. Additionally, non-filing could lead to penalties or issues with property tax assessments. It is advisable to file the form to ensure compliance and protect your interests.

Can I amend my Form 50-141 after filing?

Yes, you can amend your Form 50-141 if you discover errors or need to update information. It is essential to contact the appraisal district where you filed the original form to understand their specific procedures for submitting an amendment. Timeliness is key, so act quickly to correct any inaccuracies.

Is the information on Form 50-141 public?

The information provided on the Form 50-141 is confidential and not open to public inspection. Disclosure is only permitted under specific terms outlined in the Tax Code. This confidentiality helps protect sensitive information regarding property ownership and values.

What are the consequences of providing false information on the Form 50-141?

Providing false information on the Form 50-141 can lead to serious legal consequences. Under Texas law, making a false statement on this form may result in being charged with a Class A misdemeanor or a state jail felony. It is crucial to ensure that all information submitted is accurate and truthful.

What if I need assistance with the Form 50-141?

If you need help with the Form 50-141, consider reaching out to a tax professional or an attorney who specializes in property tax law. They can provide guidance on completing the form correctly and ensuring compliance with all relevant regulations. Additionally, the appraisal district may offer resources or assistance for filing the form.

Omitting Required Information: One common mistake is failing to provide all necessary details, such as the property owner’s name or the appraisal district account number. This omission can lead to processing delays.

Incorrect Mailing Address: Providing an inaccurate mailing address can result in important documents not reaching the property owner. It is crucial to double-check the address for accuracy.

Choosing the Wrong Filing Party: Selecting an incorrect option for the party filing the report can invalidate the submission. Ensure the correct category, such as “Property Owner” or “Authorized Agent,” is checked.

Failure to Sign: Not signing the form is a frequent error. The report must be signed by an authorized individual, or it may not be accepted.

Not Notarizing When Required: If the filer is not the property owner or an authorized employee, the signature must be notarized. Skipping this step can lead to rejection of the form.

Ignoring Deadlines: Missing the submission deadline can have serious consequences. It is essential to be aware of the specific deadlines for filing the form to avoid penalties.

Neglecting Supporting Documentation: Failing to attach required documents, such as consent from the property owner when applicable, can render the form invalid. Always include all necessary attachments.

When dealing with the Texas 50-141 form, several other documents may be necessary to ensure proper filing and compliance with tax regulations. Each document plays a specific role in the property tax process, helping property owners and fiduciaries accurately report and manage their real property. Below is a list of related forms and documents commonly used alongside the Texas 50-141 form.

Understanding these forms and documents can simplify the process of managing property taxes in Texas. Each plays a vital role in ensuring compliance and protecting the rights of property owners. Always consult with a tax professional or legal expert if there are questions about specific forms or filing requirements.

The Texas 50-141 form is used for rendering real property for taxation purposes. It has similarities with several other documents that serve related functions in property management and taxation. Below are four documents that share characteristics with the Texas 50-141 form:

When filling out the Texas 50-141 form, it is essential to approach the process with care. Below are five important dos and don'ts to consider.

Misconception 1: The Texas 50-141 form must be filed every year.

Many people believe that filing the Texas 50-141 form is mandatory each year. However, it is optional unless specifically required by the Tax Code or the chief appraiser. This means that if you are not obligated to file, you can choose not to do so.

Misconception 2: The form should be submitted to the Texas Comptroller of Public Accounts.

It is a common misunderstanding that the Texas 50-141 form should be sent to the Texas Comptroller. In reality, this form must be filed with the appraisal district office in the county where the property is located. Filing with the Comptroller is incorrect and could delay your submission.

Misconception 3: Anyone can sign the form on behalf of the property owner.

Some individuals think that any person can sign the Texas 50-141 form for the property owner. This is not true. Only specific individuals, such as an officer of the corporation or an authorized agent, can sign the form. If the signer is not one of these individuals, their signature must be notarized.

Misconception 4: Providing a property value on the form is required.

There is a belief that property owners must provide an estimate of the property's market value on the Texas 50-141 form. This is incorrect. While you can provide an estimate, it is optional. However, if you do render a value, you will receive notifications if the appraised value exceeds your rendered value.

Filling out the Texas 50-141 form correctly is essential for property owners and fiduciaries. Here are some key takeaways to keep in mind:

By following these guidelines, property owners can navigate the process smoothly and ensure compliance with Texas tax regulations.