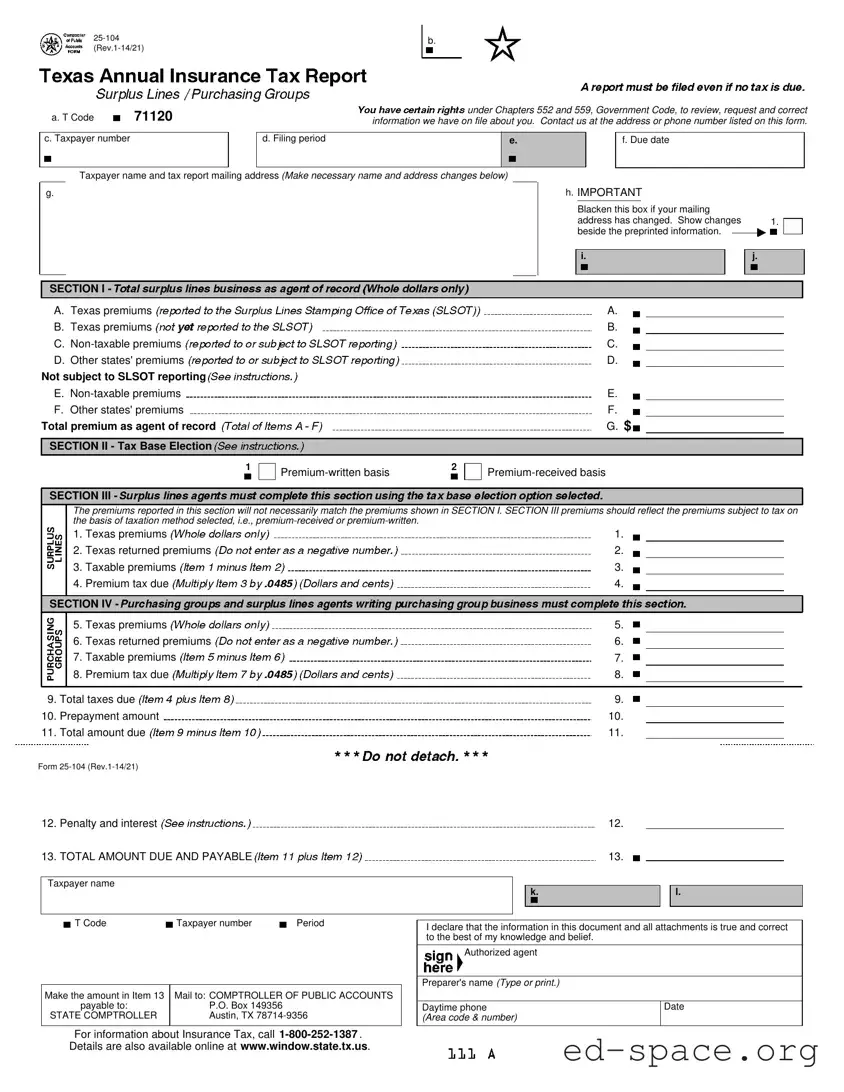

The Texas 25-104 form plays a crucial role in the annual reporting of insurance premiums for surplus lines agents and purchasing groups registered in Texas. This form is essential for ensuring compliance with state tax regulations and must be submitted even if no tax is due. It covers various aspects of premium reporting, including Texas premiums, non-taxable premiums, and premiums from other states. The form requires agents to specify the tax base they are using—either a premium-written or premium-received basis—allowing flexibility in how taxes are calculated. Additionally, the 25-104 form includes sections for reporting returned premiums and calculating any penalties or interest for late payments. It is important to note that specific instructions are provided to guide users through the completion process, ensuring accurate reporting and compliance with Texas laws. Overall, understanding the Texas 25-104 form is vital for agents and groups to navigate their tax obligations effectively.

a. T Code |

71120 |

c. Taxpayer number

b.

under Chapters 552 and 559, Government Code, to review, request and correct inf rmati n we have on file about you. Contact us at the address or phone number listed on this form.

d. Fili peri d |

e. |

|

f. Due date |

|

|

|

|

Taxpayer name and tax |

mailing addr (Make neces ary name and address chang s b low) |

g.

h. IMPORTANT

Blacken this ox if your mailing |

|

|

address has changed. Show changes |

1. |

|

esi e the preprinted information. |

|

|

|

|

|

i.

j.

SECTION I -

A. Texas premiums |

A. |

|

|

B. Texas premiums |

B. |

|

|

C. |

C. |

|

|

D. Other states' premiums |

D. |

||

Not subject to LSOT repor ing |

|

|

|

E. |

E. |

|

|

F. Other states' premiums |

F. |

|

|

Total premium as ag nt of record |

G. $ |

||

|

|

|

|

SECTION II - Tax Ba Elect on |

|

|

|

|

|

|

|

Pr |

2 |

|

SECTION III - |

|

|

|

|

|

|

||

|

The premiums eported |

his se |

will |

ot nece rily m ch the premiums shown SECTION I. SECTION III premiums should refl the premiums subject to tax on |

||||

|

the basis of taxation method |

d, .e., |

||||||

|

1. |

Texas premiu |

s |

|

|

1. |

|

|

|

2. |

Texas return |

d pr |

m s |

|

2. |

|

|

|

3. |

Taxable p emiums |

|

|

3. |

|

|

|

|

4. |

Premium tax due |

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

SECTION IV - |

|

|

|

|

|

|

||

|

5. |

Texas premiu |

s |

|

|

5. |

|

|

|

6. |

Texas return |

d pr |

|

|

6. |

|

|

|

7. |

Taxable premiums |

|

|

7. |

|

|

|

|

8. |

Premium tax due |

|

|

8. |

|

|

|

|

|

|

|

|

|

|

|

|

9. Total taxes due |

|

|

|

9. |

|

|

||

10. Prepayment amount |

|

|

10. |

|

|

|||

11. Total amount due |

|

|

|

11. |

|

|

||

Form

12.Penalty and interest

13.TOTAL AMOUNT DUE AND PAYABLE

Taxpayer name

12.

13.

k.

l.

T Code |

Taxpayer number |

Period |

Make the amount in Item 13 |

Mail to: COMPTROLLER OF PUBLIC ACCOUNTS |

payable to: |

P.O. Box 149356 |

STATE COMPTROLLER |

Austin, TX |

|

|

I declare that the information in this document and all attachments is true and correct to the best of my knowledge and belief.

Authorized agent

Preparer's name (Type or print.)

Daytime phone |

Date |

(Area code & number) |

|

|

|

For information about Insurance Tax, call

Form

Inst uctio |

f r Completing the Texas Annual Insurance T x Report |

Who Must File |

|

All surpl lines ag ts licen ed Texas and a |

purchasi gr ups registered in Texas must file this report, even if no tax is due. |

When to File

he report and payment are d on March 1 of the year following the tax year.

Section I

he

Item A - Texas Pr miums - Enter the total Texas premiums for policies that were effective prior to July 21, 2011 (net of return premiums) that were reported to the SLSOT during the tax year. Enter the total amount of premiums for policies that were effective on or after July 21, 2011 (net of return premiums) that have been reported to the SLSOT where Texas is the home tate of the insured.

Item - Texas Pr miums - Enter the total Texas premiums for policies that were effective prior to July 21, 2011 (net of return premiums) that have NOT YET been reported to the SLSOT during the tax year. Ent r he total amount of premiums for policies that were effective on or after July 21, 2011 (net of return premiums) that have NOT YET been reported to the SLSOT where Texas is the home state of the insured.

Item C -

entirely Texas and the

the premiums are exem t from taxation or are preempted from taxation.

Item D - Oth r States' Premi ms - Enter the total premiums for policies that were effective prior to July 21, 2011 (net of return premiums) allocated to all other states from a

100% of the policy premium, but also allows the monitoring of the amount of

enter the premiums (net of return premium ) that are 100% exempt or

Item F - Oth r States' Premi ms - This category does not apply to policies that are effective on or after July 21, 2011. For policies that are effective prior to July 21, 2011, enter the to al taxable premiums (net of return premiums) allocated to other states for policies that exclusively cover states other than Texas.

Section II

lines agents who received a license during the reporting year must elect one of the tax base options shown.

Rle 34 TAC, Sec. 3.822, provides specific information on the requirements for reporting surplus lines tax. Agents have the option of reporting tax using a

Section III

These premiums will not necessarily match the premiums shown in Section I, because they are based on the reporting method chosen. The term "premium" includes all

premiums, premi m deposits, membership fees, registration fees, assessments, dues and any other consideration for surplus lines insurance. Texas premiums include: premiums written or received for policies that are effective prior to July 21, 2011 that cover risks in this state;

premiums written or received for new or renewal Texas or

Exempt premiums are premiums for a surplus lines policy that covers risks or exposures that are properly allocated to federal waters, international waters, or risks or exposures that are under the jurisdiction of a foreign government. Effective Jan. 1, 2014, premiums on risks or exposures under ocean marine insurance coverage of sto ed or

Feder l preemptions to state taxation for surplus lines insurance include premiums for policies that are issued to the following entities:

the Federal Deposit Insurance Corporation (FDIC), when it acts as the receiver of a failed financial institution that holds the property being insured; the National Credit Union Administration;

a federally chartered credit union; and

Indian Tribal Nations (see Publication

Texas returned premiums - Report the unearned portion of the premium that is credited or refunded to a policyholder as a result of cancellation or premium adjustment prior to the policy expiration. An age t reporting on the premium received basis will not have returned premiums.

Endorsements and audits on surplus lines insurance policies must be reported based on the date of the endorsement or audit, not the date of the original policy. The tax for endorsements and audits that generate return premiums due a policyholder must be calculated using the tax rate that was originally charged.

Section IV

Purchasing groups obtaining coverage from insurers licensed in Texas or surplus lines agents licensed in Texas do NOT owe tax on this report, but must a zero report. Purchasing groups obtaining coverage independently through negotiations and procurement occurring outside Texas are subject to tax on the premiums paid for coverage of their members located in Texas.

Check this box if insurance was obtained from a licensed insurance company or a licensed or registered risk retention group.

Check this box if insurance was obtained from a surplus lines agent licensed in Texas.

Specific Instructions

Item 12 - Penalty and interest

If tax is paid

If tax is paid

If tax is paid over 60 days late: Enter penalty of 10% (.10) of Item 11 plus interest. Calculate interest at the rate published online at www.window.state.tx.us or call the Comptroller at

Electronic reporting nd payment options are available 24 hours day, 7 days a week. Have this form available when you log on.

| Fact Name | Description |

|---|---|

| Governing Laws | The Texas 25-104 form is governed by Chapters 552 and 559 of the Texas Government Code. |

| Who Must File | All surplus lines agents licensed in Texas and purchasing groups registered in Texas must file this report, even if no tax is due. |

| Filing Deadline | The report and payment are due on March 1 of the year following the tax year. |

| Tax Reporting Method | Agents can choose to report tax on a premium-written or premium-received basis, with the option to change every four years. |

Filling out the Texas 25-104 form is an important step for surplus lines agents and purchasing groups registered in Texas. This report must be completed accurately to ensure compliance with state tax regulations. Below are the steps to guide you through the process of filling out the form.

After completing the form, ensure all information is accurate before mailing it to the Comptroller of Public Accounts at the address provided on the form. Timely submission is crucial to avoid penalties.

What is the Texas 25-104 form?

The Texas 25-104 form is an annual insurance tax report required for surplus lines agents and purchasing groups registered in Texas. It provides a detailed account of premiums written, received, and any tax liabilities. This form ensures compliance with Texas tax laws and helps maintain accurate records of insurance transactions within the state.

Who is required to file the Texas 25-104 form?

All surplus lines agents licensed in Texas must file the Texas 25-104 form, even if no tax is due. Additionally, purchasing groups that are registered in Texas are also required to submit this report. This requirement applies regardless of whether the agent or group has any taxable premiums for the year.

When is the Texas 25-104 form due?

The Texas 25-104 form and any associated payments are due on March 1 of the year following the tax year. For example, for tax year 2022, the form must be submitted by March 1, 2023. Timely submission is crucial to avoid penalties and interest on late payments.

What information is needed to complete the form?

To complete the Texas 25-104 form, you will need to provide details such as your taxpayer name, taxpayer number, and mailing address. Additionally, you must report various categories of premiums, including Texas premiums, non-taxable premiums, and premiums from other states. Accurate figures are essential for proper tax calculation.

What happens if I do not file the Texas 25-104 form?

Failure to file the Texas 25-104 form can lead to penalties and interest on any taxes owed. The state may impose a penalty of 5% for late payments within the first 30 days, increasing to 10% for payments made 31-60 days late. If the payment is over 60 days late, additional interest will also apply.

How do I report non-taxable premiums on the form?

Non-taxable premiums must be reported in Section I of the form. You should enter the total non-taxable premiums for policies effective before and after July 21, 2011. Ensure that these premiums cover risks entirely located in Texas or fall under specific exemptions to qualify as non-taxable.

Can I change my reporting method for premiums?

Yes, agents can choose between a premium-written or premium-received basis for reporting. However, once you make a change, you must stick with that method for four years. If you switch from a premium-received to a premium-written basis, you will owe taxes on all outstanding receivables as of January 1 of the year of the change.

What should I do if my mailing address has changed?

If your mailing address has changed, you must blacken the box provided on the form and show the new address. This ensures that the Texas Comptroller's office has your current contact information for any correspondence regarding your tax filings.

Where can I find more information about the Texas 25-104 form?

For additional information, you can call the Texas Comptroller's office at 1-800-252-1387. Detailed guidance is also available online at the Texas Comptroller's website, where you can find resources related to insurance tax and the completion of the Texas 25-104 form.

Failing to update the mailing address if it has changed. This can lead to important documents not reaching the taxpayer.

Not reporting all premiums accurately. Ensure that all Texas premiums, including those effective before and after July 21, 2011, are included.

Ignoring the tax base election option. New agents must choose between a premium-written or premium-received basis.

Misunderstanding the non-taxable premiums. It’s crucial to correctly identify which premiums are exempt from taxation.

Overlooking the penalty and interest section. Late payments incur penalties that must be calculated and reported correctly.

Not providing a complete taxpayer name. Ensure the name matches the official records to avoid processing delays.

Forgetting to sign and date the form. An unsigned form may be considered incomplete and could be rejected.

Failing to include all required attachments. Ensure all necessary documents are submitted along with the form.

Using incorrect taxpayer numbers. Verify that the taxpayer number provided is accurate to prevent issues with processing.

Not keeping records of prior submissions. Retaining copies of previous forms helps in accurate reporting and future reference.

The Texas 25-104 form is essential for surplus lines agents and purchasing groups in Texas to report their insurance premiums and taxes. Alongside this form, several other documents are commonly used in the process of insurance tax reporting and compliance. Below is a list of five important forms and documents that complement the Texas 25-104.

These forms work in conjunction with the Texas 25-104 to ensure comprehensive reporting and compliance with state tax laws. It is vital for agents and purchasing groups to be familiar with these documents to avoid penalties and ensure accurate tax reporting.

Filling out the Texas 25-104 form can seem daunting, but following some simple guidelines can make the process much smoother. Here’s a list of things you should and shouldn’t do when completing this form.

By adhering to these guidelines, you can ensure that your Texas 25-104 form is filled out correctly and submitted on time. This will help you avoid unnecessary complications and keep your records in good standing.

Understanding the Texas 25-104 form can be challenging, and several misconceptions can lead to confusion. Here are seven common misconceptions about this form, along with clarifications to help you navigate the process more easily.

All surplus lines agents licensed in Texas must file this report, regardless of whether any tax is due. This includes those who have no taxable premiums to report.

The report and payment are due on March 1 of the year following the tax year. Timeliness is essential to avoid penalties.

Not all premiums are taxable. The form includes sections for non-taxable premiums and other states' premiums, which must be reported correctly.

While the form focuses on Texas premiums, it also requires reporting of premiums from policies that cover risks in other states, especially in multi-state situations.

If you discover an error after filing, you can correct it by submitting an amended report. It's crucial to ensure the accuracy of your information.

The penalties vary based on how late the payment is. For example, if the tax is paid 1-30 days late, the penalty is 5%, while it increases to 10% if paid 31-60 days late.

Electronic reporting and payment options are available 24/7. This can simplify the process and help ensure timely submission.

Key Takeaways for Filling Out and Using the Texas 25-104 Form

Be diligent in completing this form to avoid unnecessary penalties and ensure compliance with Texas tax laws.