The Texas 01-924 form serves as a vital tool for commercial agricultural producers seeking to claim an exemption from sales and use tax on qualifying agricultural purchases. This form is specifically designed for items that will be used exclusively in the production of agricultural products intended for sale. It is important to note that the form cannot be used for motor vehicle tax exemptions; for such cases, a different certificate must be provided. Certain agricultural items, including livestock and feed, are exempt from requiring this certificate, while others necessitate its completion to validate the exemption. The form outlines essential information, such as the purchaser's details, the retailer's information, and the ag/timber number, which must be included to ensure compliance. Additionally, it emphasizes the need for proper record-keeping to verify eligibility for the claimed exemptions. Misuse of the form can lead to serious legal consequences. Understanding the proper use of the Texas 01-924 form is crucial for agricultural producers to navigate tax regulations effectively and avoid potential pitfalls.

PRINT FORM |

CLEAR FORM |

|

|

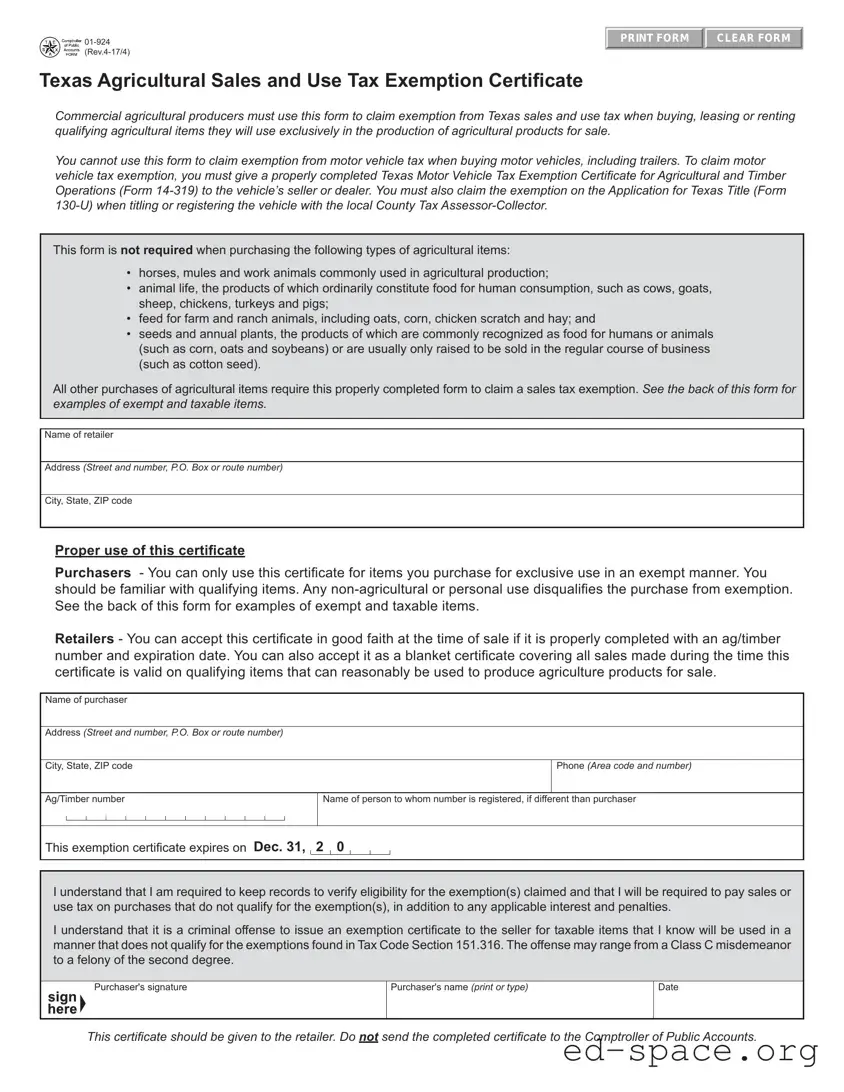

Texas Agricultural Sales and Use Tax Exemption Certificate

Commercial agricultural producers must use this form to claim exemption from Texas sales and use tax when buying, leasing or renting qualifying agricultural items they will use exclusively in the production of agricultural products for sale.

You cannot use this form to claim exemption from motor vehicle tax when buying motor vehicles, including trailers. To claim motor vehicle tax exemption, you must give a properly completed Texas Motor Vehicle Tax Exemption Certificate for Agricultural and Timber Operations (Form

This form is not required when purchasing the following types of agricultural items:

•horses, mules and work animals commonly used in agricultural production;

•animal life, the products of which ordinarily constitute food for human consumption, such as cows, goats, sheep, chickens, turkeys and pigs;

•feed for farm and ranch animals, including oats, corn, chicken scratch and hay; and

•seeds and annual plants, the products of which are commonly recognized as food for humans or animals (such as corn, oats and soybeans) or are usually only raised to be sold in the regular course of business (such as cotton seed).

All other purchases of agricultural items require this properly completed form to claim a sales tax exemption. See the back of this form for examples of exempt and taxable items.

Name of retailer

Address (Street and number, P.O. Box or route number)

City, State, ZIP code

Proper use of this certificate

Purchasers - You can only use this certificate for items you purchase for exclusive use in an exempt manner. You should be familiar with qualifying items. Any

Retailers - You can accept this certificate in good faith at the time of sale if it is properly completed with an ag/timber number and expiration date. You can also accept it as a blanket certificate covering all sales made during the time this certificate is valid on qualifying items that can reasonably be used to produce agriculture products for sale.

Name of purchaser

Address (Street and number, P.O. Box or route number)

City, State, ZIP code

Phone (Area code and number)

Ag/Timber number

Name of person to whom number is registered, if different than purchaser

This exemption certificate expires on Dec. 31, 2 0

I understand that I am required to keep records to verify eligibility for the exemption(s) claimed and that I will be required to pay sales or use tax on purchases that do not qualify for the exemption(s), in addition to any applicable interest and penalties.

I understand that it is a criminal offense to issue an exemption certificate to the seller for taxable items that I know will be used in a manner that does not qualify for the exemptions found in Tax Code Section 151.316. The offense may range from a Class C misdemeanor to a felony of the second degree.

Purchaser's signature

Purchaser's name (print or type)

Date

This certificate should be given to the retailer. Do not send the completed certificate to the Comptroller of Public Accounts.

Form

Always Exempt

These items are always exempt and do not require an exemption certificate or an ag/timber number.

•Horses, mules and work animals commonly used in agricultural production;

•Animal life, the products of which ordinarily constitute food for human consumption, such as cattle, goats, sheep, chickens, turkeys and hogs;

•Feed such as oats, hay, chicken scratch, wild bird seed and deer corn for livestock and wild game (pet food is not exempt); and

•Seeds and annual plants, the products of which are commonly recognized as food for humans or animals, such as corn, oats and soybeans or for fiber, such as cotton seed.

Exempt

Here are examples of items that are exempt from sales tax when used exclusively on a farm or ranch to produce agricultural products for sale and pur- chased by a person with a current ag/timber number.

Air tanks

Augers

Bale transportation equipment

Baler twine

Baler wrap

Balers

Binders

Branding irons

Brush hogs Bulk milk coolers Bulk milk tanks

Calf weaners and feeders

Cattle currying and oiling machines

Cattle feeders

Chain saws used for clearing fence lines or pruning orchards

Choppers

Combines

Conveyors

Corn pickers

Corral panels

Cotton pickers, strippers

Crawlers – tractors

Crushers

Cultipackers

Discs

Drags

Dryers

Dusters

Egg handling equipment

Ensilage cutters

Farm machinery and repair or replacement parts

Farm tractors Farm wagons

Farrowing houses (portable and crates)

Feed carts

Feed grinders

Feeders

Fertilizer

Fertilizer distributors

Floats for water troughs

Foggers

Forage boxes

Forage harvesters

Fruit graters

Fruit harvesters

Grain binders

Grain bins

Grain drills

Grain handling equipment

Greases, lubricants and oils for qualifying farm machinery and equipment

Harrows

Head gates

Hoists

Husking machines

Hydraulic fluid

Irrigation equipment

Manure handling equipment Manure spreaders Milking equipment

Mowers (hay and rotary blade)

Pesticides

Pickers

Planters Poultry feeders

Poultry house equipment

Pruning equipment

Rollbar equipment Rollers

Root vegetable harvesters

Rotary hoes

Salt stands

Seed cleaners

Shellers

Silo unloaders

Soilmovers used to grade farmland

Sorters

Sowers

Sprayers

Spreaders

Squeeze chutes

Stalls

Stanchions

Subsoilers

Telecommunications services used to navigate farm machinery and equipment*

Threshing machines Tillers

Tires for exempt equipment Troughs, feed and water

Vacuum coolers

Vegetable graders

Vegetable washers

Vegetable waxers

* As of Sept. 1, 2015, telecommunications services used to navigate farm machinery and equipment are exempt.

Taxable

These items DO NOT qualify for sales and use tax exemption for agricultural production.

•Automotive parts, such as tires, for vehicles licensed for highway use, even if the vehicle has farm plates

•Clothing, including work clothing, safety apparel and shoes

•Computers and computer software used for any purposes other than agricultural production

•Furniture, home furnishings and housewares

•Golf carts, dirt bikes, dune buggies and

•Guns, ammunition, traps and similar items

*See

•Materials used to construct roads or buildings used for shelter, housing, storage or work space (examples include general storage barns, sheds or shelters)

•Motor vehicles and trailers*

•Pet food

•Taxable services such as nonresidential real property repairs or remodeling, security services, and waste removal

Tax Help: www.comptroller.texas.gov/taxes/ = Window on State Government: www.comptroller.texas.gov

Tax Assistance:

Sign up to receive email updates on the Comptroller topics of your choice at www.comptroller.texas.gov/subscribe.

| Fact Name | Details |

|---|---|

| Purpose of Form | This form allows commercial agricultural producers to claim exemption from Texas sales and use tax for qualifying agricultural items used exclusively in production for sale. |

| Exemption Limitations | It cannot be used for motor vehicle tax exemptions. For vehicles, a separate Texas Motor Vehicle Tax Exemption Certificate (Form 14-319) is required. |

| Always Exempt Items | Certain items, such as horses, feed, and seeds, are always exempt from tax and do not require this certificate. |

| Governing Law | The use of this form is governed by Texas Tax Code Section 151.316. |

Filling out the Texas 01-924 form is straightforward, but attention to detail is essential. This form serves as a certificate for agricultural producers to claim a sales tax exemption. After completing the form, submit it to the retailer where you are making your purchase. Keep in mind that this form should not be sent to the Comptroller of Public Accounts.

After completing these steps, hand the form to the retailer at the time of purchase. Remember to keep a copy for your records, as you may need it for future reference or verification of your exemption eligibility.

What is the Texas 01-924 form used for?

The Texas 01-924 form is an Agricultural Sales and Use Tax Exemption Certificate. It allows commercial agricultural producers to claim exemption from Texas sales and use tax when purchasing, leasing, or renting qualifying agricultural items. These items must be used exclusively in the production of agricultural products intended for sale. It is important to note that this form cannot be used for motor vehicle tax exemptions; a different form is required for those transactions.

Who is eligible to use the Texas 01-924 form?

Only commercial agricultural producers can use the Texas 01-924 form. To qualify, the items purchased must be for exclusive agricultural use. If any part of the purchase is for non-agricultural or personal use, the exemption does not apply. It is crucial for purchasers to be familiar with which items qualify for exemption to avoid any issues during transactions.

What items are exempt from sales tax when using this form?

Many agricultural items are exempt from sales tax when purchased with the Texas 01-924 form. Examples include farm machinery, irrigation equipment, and various tools used in agricultural production. However, certain items, such as horses, feed for livestock, and seeds, do not require this form for exemption. It is advisable to refer to the list provided on the back of the form for a comprehensive understanding of exempt and taxable items.

What happens if the exemption is misused?

Misusing the Texas 01-924 form can lead to serious consequences. If a purchaser issues this exemption certificate for items that do not qualify, they may be held liable for unpaid sales or use tax, along with any applicable interest and penalties. In some cases, this misuse may even result in criminal charges, ranging from a Class C misdemeanor to a felony of the second degree. Therefore, it is essential to use the form correctly and keep accurate records to verify eligibility for exemptions claimed.

Not including the Ag/Timber number. This number is essential for claiming the exemption. Without it, the form is incomplete.

Failing to provide a valid expiration date. Each exemption certificate has a specific validity period. Missing this date can lead to complications.

Using the form for non-agricultural purchases. This certificate is strictly for agricultural items. Misuse can result in penalties.

Not signing the certificate. The purchaser's signature confirms the accuracy of the information provided.

Providing an incorrect address. Ensure that all addresses are accurate. This helps in maintaining clear records.

Ignoring the requirement to keep records. It's important to maintain documentation to verify eligibility for the claimed exemptions.

Not understanding the difference between exempt and taxable items. Familiarize yourself with what qualifies for exemption to avoid errors.

Submitting the form to the Comptroller of Public Accounts. The completed form should be given directly to the retailer, not sent to the state.

Not keeping track of changes in tax laws. Tax regulations can change, and staying informed is crucial for compliance.

The Texas 01-924 form is essential for agricultural producers seeking to claim a sales and use tax exemption. To ensure compliance and streamline the exemption process, other forms and documents are often used in conjunction with the 01-924. Here are some of the key documents that may be necessary:

Utilizing these forms and documents effectively can help agricultural producers navigate the complexities of tax exemptions in Texas. Understanding their purpose and proper usage is key to ensuring compliance and maximizing benefits under the law.

The Texas 01-924 form is an important document for agricultural producers looking to claim a sales and use tax exemption. There are several other documents that serve similar purposes in different contexts. Here’s a list of nine such documents:

Each of these documents serves a unique purpose while sharing the common goal of facilitating tax exemptions for specific types of purchases. Understanding these similarities can help individuals and businesses navigate the tax landscape more effectively.

When filling out the Texas 01-924 form, it's important to follow certain guidelines to ensure that the process goes smoothly. Here are nine things you should and shouldn't do:

Misconceptions about the Texas 01-924 form can lead to confusion for both purchasers and retailers. Here are five common misconceptions:

Understanding the Texas 01-924 form is essential for agricultural producers looking to claim tax exemptions. Here are five key takeaways to keep in mind: