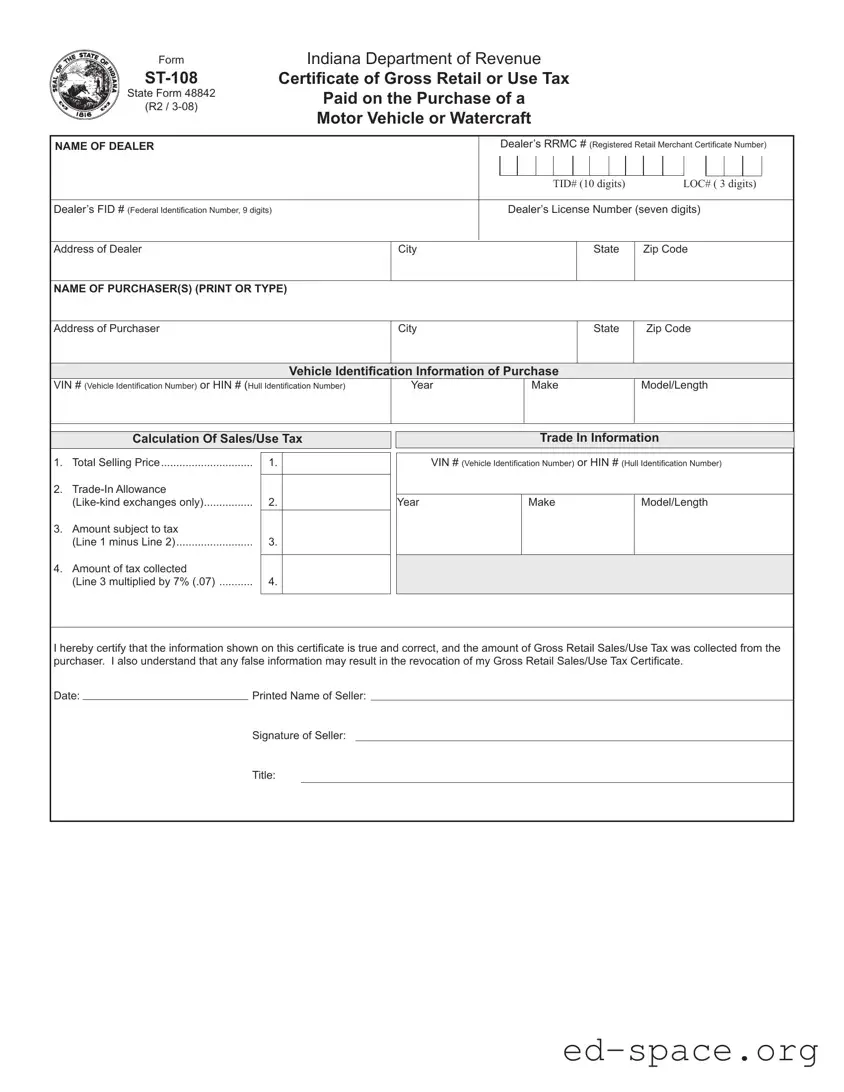

The ST-108 form is an essential document for anyone involved in the purchase of a motor vehicle or watercraft in Indiana. This form, officially titled the Certificate of Gross Retail or Use Tax Paid, serves as proof that the applicable sales or use tax has been collected by the dealer from the purchaser. Key details required on the form include the dealer's information, such as their Registered Retail Merchant Certificate number and Federal Identification Number, as well as the purchaser's name and address. Vehicle identification details, including the Vehicle Identification Number (VIN) or Hull Identification Number (HIN), year, make, and model or length of the watercraft must also be provided. The form outlines a straightforward calculation for determining the sales/use tax, which involves the total selling price, any trade-in allowances, and the final amount subject to tax. Notably, the seller must certify the accuracy of the information provided and sign the form, ensuring compliance with Indiana tax regulations. If an exemption is claimed, an additional form, ST-108E, must be completed. This introductory overview highlights the importance of the ST-108 form in facilitating the legal transfer of ownership while ensuring that tax obligations are met.

Form

State Form 48842

(R2 /

Indiana Department of Revenue

Certificate of Gross Retail or Use Tax

Paid on the Purchase of a

Motor Vehicle or Watercraft

NAME OF DEALER |

|

|

Dealer’s RRMC # (Registered Retail Merchant Certificate Number) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TID# (10 digits) |

|

|

LOC# ( 3 digits) |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Dealer’s FID # (Federal Identification Number, 9 digits) |

|

|

Dealer’s License Number (seven digits) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Dealer |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Purchaser(s) (pRINT OR tYPE) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Purchaser |

City |

|

|

|

|

|

|

|

State |

|

Zip Code |

||||||||

Vehicle Identification Information of Purchase

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number) |

Year |

Make |

Model/Length |

|

|

|

|

Calculation Of Sales/Use Tax

1. |

Total Selling Price |

1. |

|

2. |

|

|

|

|

2. |

|

|

3. |

Amount subject to tax |

|

|

|

(Line 1 minus Line 2) |

3. |

|

4. |

Amount of tax collected |

|

|

|

|

||

|

(Line 3 multiplied by 7% (.07) |

4. |

|

|

|

|

|

Trade In Information

VIN # (Vehicle Identification Number) or HIN # (Hull Identification Number)

Year |

Make |

Model/Length |

|

|

|

|

|

|

I hereby certify that the information shown on this certificate is true and correct, and the amount of Gross Retail Sales/Use Tax was collected from the purchaser. I also understand that any false information may result in the revocation of my Gross Retail Sales/Use Tax Certificate.

Date: |

|

Printed Name of Seller: |

|

|

|

Signature of Seller: |

|

|

|

Title: |

|

Instructions for completing Form

or Use Tax on the Purchase of a Motor Vehicle or Watercraft.

INDIANA CODE

The

If an exemption from the tax is claimed, the purchaser and the dealer must complete Form

Seller Information

NAME OF DEALER: Indicate the name of the dealer as it appears on the Registered Retail Merchant Certificate (RRMC).

FID # (Federal Identification Number): Indicate the Federal Identification Number of the dealer, if applicable.

Dealer’s License #: Indicate the Dealer’s License Number(seven digits) as it appears on the Dealer’s License Certificate.

RRMC # (same as TID # - 10 Digits + LOC # - 3 Digits): Indicate the Indiana Taxpayer Identification Number and Location Number as it appears on the Registered Retail Merchant Certificate. This number must be in the following format:

Address of Dealer: Indicate the address of the dealer as it appears on the Registered Retail Merchant Certifi- cate.

Vehicle Identification Information

VIN or HIN ID #: Enter the Vehicle ID # (VIN) or the Hull ID # (HIN).

YEAR: Indicate the year the motor vehicle or watercraft was manufactured.

MODEL # OR WATERCRAFT LENGTH: If a motor vehicle is being sold indicate the model name for the vehicle. If a watercraft is being sold indicate the length of the craft.

Calculation of Sales/Use Tax

TOTAL SELLING PRICE: When determining the total selling price include all delivery, make ready, repair, or other costs incurred prior to transfer to the buyer. Federal excise tax is NOT included.

You must also indicate the make, model, year, and ID # of the

AMOUNT SUBJECT TO TAX: Line 1 minus Line 2 results in the amount on which the sales/use tax will be calcu- lated.

AMOUNT OF TAX COLLECTED: Line 3 multiplied by 7% or .07 equals the amount to be collected by the seller.

Signature Section: The Seller must sign the

| Fact Name | Description |

|---|---|

| Form Title | ST-108 is the Certificate of Gross Retail or Use Tax Paid on the Purchase of a Motor Vehicle or Watercraft. |

| Governing Law | Indiana Code 6-2.5-9-6 mandates the use of this form when titling a vehicle or watercraft. |

| Dealer Information | Dealers must provide their Registered Retail Merchant Certificate Number and Federal Identification Number. |

| Tax Rate | The sales/use tax collected is calculated at a rate of 7% of the taxable amount. |

| Trade-In Allowance | Only like-kind exchanges qualify for a trade-in allowance to reduce the taxable selling price. |

| Signature Requirement | The seller must sign the form to certify that the tax has been collected; otherwise, the form will be rejected. |

| Tax Submission | Dealers are required to submit the collected sales/use tax to the Indiana Department of Revenue. |

| Exemption Procedure | If claiming an exemption, both purchaser and dealer must complete Form ST-108E. |

| Information Accuracy | All information on the form must be true and correct to avoid penalties or revocation of the tax certificate. |

| Form Rejection | Failure to provide the correct format for the RRMC will result in rejection of the ST-108 by the license branch. |

Filling out the ST-108 form is a necessary step when titling a vehicle or watercraft in Indiana. This form certifies that the appropriate sales or use tax has been collected by the dealer. Following these steps will help ensure that the form is completed accurately and can be processed without delay.

Once the form is completed, it should be submitted along with any necessary documentation to the appropriate licensing branch. Ensure that all information is accurate to avoid any processing delays.

What is the purpose of Form ST-108?

Form ST-108 serves as a Certificate of Gross Retail or Use Tax Paid on the purchase of a motor vehicle or watercraft in Indiana. It is required by law to demonstrate that the appropriate sales tax has been collected by the dealer at the time of sale. This form must be presented when titling the vehicle or watercraft to avoid direct tax payment to the Bureau of Motor Vehicles license branch.

Who needs to complete Form ST-108?

The dealer selling the motor vehicle or watercraft is responsible for completing Form ST-108. Additionally, the purchaser's information must be included. Both parties must ensure that the details are accurate, as any discrepancies could lead to issues during the titling process.

What information is required on Form ST-108?

Form ST-108 requires several key pieces of information. This includes the dealer’s name, Registered Retail Merchant Certificate number, Federal Identification Number, and license number. It also requires the purchaser’s name and address, along with vehicle identification details such as the Vehicle Identification Number (VIN) or Hull Identification Number (HIN), year, make, and model or length of the watercraft. Lastly, the form includes calculations for total selling price, trade-in allowance, and the amount of sales tax collected.

How is the sales/use tax calculated on Form ST-108?

The sales/use tax is calculated based on the total selling price of the vehicle or watercraft, minus any trade-in allowance for like-kind exchanges. Specifically, the formula is as follows: take the total selling price, subtract the trade-in allowance, and then multiply the resulting amount by 7% (0.07) to determine the sales tax to be collected. It’s important to include all applicable costs in the total selling price, excluding federal excise tax.

What happens if the information on Form ST-108 is incorrect?

If any information on Form ST-108 is incorrect, the license branch may reject the form. This could necessitate the purchaser returning to the dealer to obtain a corrected form. It is crucial for both the dealer and purchaser to double-check all entries to ensure compliance with state requirements and to avoid delays in the titling process.

Is there an exemption available for sales/use tax when using Form ST-108?

Yes, there is a provision for exemptions. If a purchaser believes they qualify for an exemption from the sales/use tax, both the dealer and the purchaser must complete Form ST-108E. This form acts as an affidavit of exemption and must be submitted at the time of licensing. It outlines the exemptions available and ensures that the appropriate documentation is in place to avoid unnecessary tax payments.

Incorrect Dealer Information: Ensure the dealer's name, RRMC number, and address match exactly as they appear on the Registered Retail Merchant Certificate. Any discrepancies can lead to rejection.

Missing or Incorrect TID Number: The Taxpayer Identification Number must be formatted correctly (10 digits + 3 digits). An incorrect format will cause the form to be rejected.

Omitting the Vehicle Identification Number (VIN): Always include the VIN or HIN. This information is crucial for identifying the vehicle or watercraft being purchased.

Improper Calculation of Sales/Use Tax: Ensure that the total selling price includes all relevant costs. Missing costs can result in incorrect tax calculations.

Not Including Trade-In Information: If a trade-in is involved, provide details such as the make, model, year, and ID number of the traded vehicle or watercraft. Failing to do so can affect tax calculations.

Failure to Sign the Form: The seller must sign the ST-108. A missing signature will lead to the form being rejected, requiring the purchaser to return to the seller for completion.

Incorrect Amount Subject to Tax: Double-check the calculation of the amount subject to tax. This should be the total selling price minus any trade-in allowances.

Neglecting to Include All Costs: Remember to include delivery and other costs in the total selling price. Omitting these can lead to tax discrepancies.

Not Understanding Exemptions: If claiming an exemption, make sure to complete Form ST-108E. Not doing so can complicate the licensing process.

When dealing with the ST-108 form in Indiana, several other documents may come into play. Each of these forms serves a specific purpose in the process of buying or selling a motor vehicle or watercraft. Understanding these documents can help ensure a smoother transaction.

Familiarizing yourself with these forms can help streamline the process of buying or selling a vehicle or watercraft in Indiana. Being prepared with the right documentation ensures compliance with state regulations and protects your interests in the transaction.

The ST-108 form has similarities with several other documents related to tax and vehicle transactions. Here are four documents that share characteristics with the ST-108:

When filling out the ST-108 form, it is essential to adhere to specific guidelines to ensure accuracy and compliance. Below is a list of actions to take and avoid during this process.

Here are five common misconceptions about the ST-108 form, along with clarifications for each:

When filling out and using the ST-108 form, it’s essential to follow specific guidelines to ensure compliance and smooth processing. Here are some key takeaways: