The SF 16 Georgia form plays a crucial role in the Georgia Dream Homeownership Program, specifically designed for individuals seeking to acquire a home through the Georgia Dream First Mortgage Program. This form is not merely a document; it serves as a comprehensive certification of the acquisition costs associated with purchasing a property. Within its pages, borrowers must detail various financial aspects, including the total amount paid to the property seller, costs related to the land and dwelling, and any additional expenses incurred during the home-buying process. The form requires borrowers to calculate both additions, such as the sales price and construction-related costs, and subtractions, which include personal property purchases and services rendered by family members. By meticulously outlining these figures, the SF 16 ensures that the total acquisition cost reflects a true and accurate financial picture, thereby aiding in the assessment of eligibility for the program. Furthermore, the document emphasizes the importance of compliance, as borrowers must affirm the truthfulness of their declarations under penalty of perjury, reinforcing the integrity of the application process. Understanding the nuances of the SF 16 form is essential for prospective homeowners, as it lays the groundwork for their journey toward homeownership in Georgia.

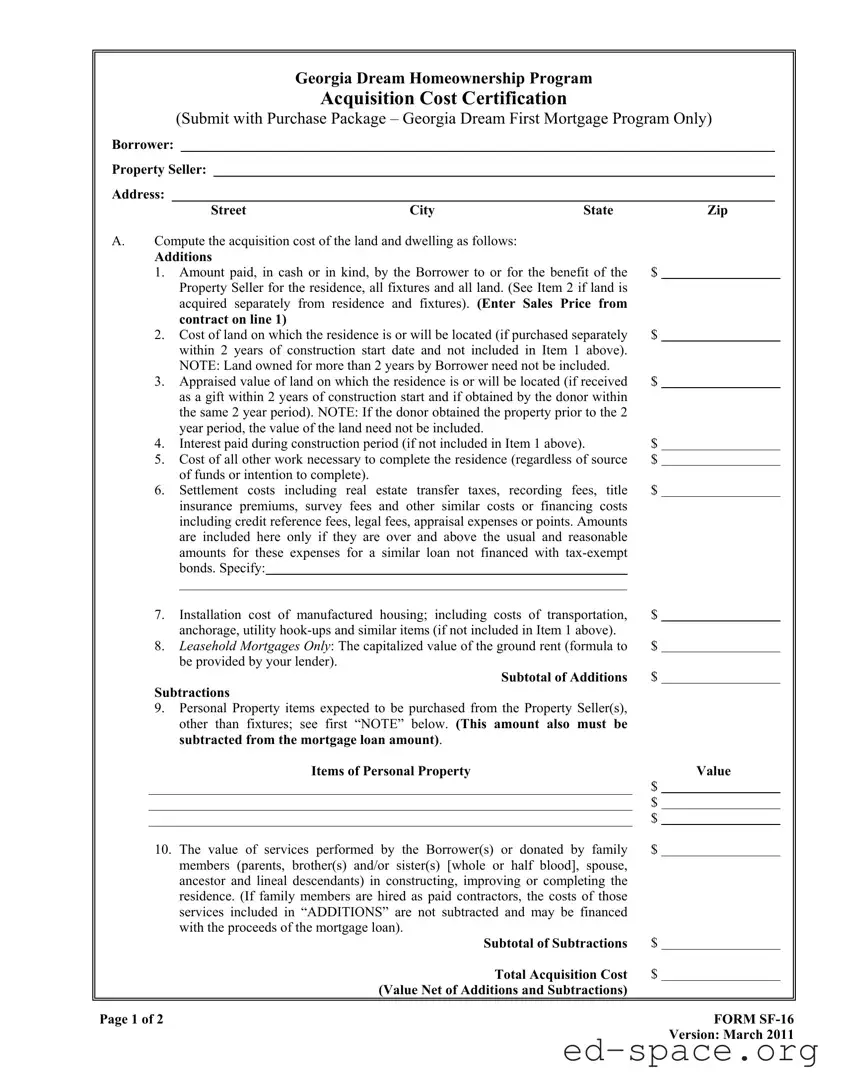

Georgia Dream Homeownership Program

Acquisition Cost Certification

(Submit with Purchase Package – Georgia Dream First Mortgage Program Only)

Borrower:

Property Seller:

Address:

Street |

City |

State |

Zip |

A.Compute the acquisition cost of the land and dwelling as follows:

Additions |

|

|

1. |

Amount paid, in cash or in kind, by the Borrower to or for the benefit of the |

$ |

|

Property Seller for the residence, all fixtures and all land. (See Item 2 if land is |

|

|

acquired separately from residence and fixtures). (Enter Sales Price from |

|

|

contract on line 1) |

|

2. |

Cost of land on which the residence is or will be located (if purchased separately |

$ |

|

within 2 years of construction start date and not included in Item 1 above). |

|

|

NOTE: Land owned for more than 2 years by Borrower need not be included. |

|

3. |

Appraised value of land on which the residence is or will be located (if received |

$ |

|

as a gift within 2 years of construction start and if obtained by the donor within |

|

|

the same 2 year period). NOTE: If the donor obtained the property prior to the 2 |

|

|

year period, the value of the land need not be included. |

|

4. |

Interest paid during construction period (if not included in Item 1 above). |

$ |

5. |

Cost of all other work necessary to complete the residence (regardless of source |

$ |

|

of funds or intention to complete). |

|

6. |

Settlement costs including real estate transfer taxes, recording fees, title |

$ |

|

insurance premiums, survey fees and other similar costs or financing costs |

|

including credit reference fees, legal fees, appraisal expenses or points. Amounts are included here only if they are over and above the usual and reasonable amounts for these expenses for a similar loan not financed with

7. |

Installation cost of manufactured housing; including costs of transportation, |

$ |

|

anchorage, utility |

|

8. |

Leasehold Mortgages Only: The capitalized value of the ground rent (formula to |

$ |

|

be provided by your lender). |

|

|

Subtotal of Additions |

$ |

Subtractions

9.Personal Property items expected to be purchased from the Property Seller(s), other than fixtures; see first “NOTE” below. (This amount also must be subtracted from the mortgage loan amount).

Items of Personal Property

$

$

$

Value

|

10. The value of services performed by the Borrower(s) or donated by family |

$ |

|

|

|

|

members (parents, brother(s) and/or sister(s) [whole or half blood], spouse, |

|

|

|

|

|

ancestor and lineal descendants) in constructing, improving or completing the |

|

|

|

|

|

residence. (If family members are hired as paid contractors, the costs of those |

|

|

|

|

|

services included in “ADDITIONS” are not subtracted and may be financed |

|

|

|

|

|

with the proceeds of the mortgage loan). |

|

|

|

|

|

Subtotal of Subtractions |

$ |

|

|

|

|

Total Acquisition Cost |

$ |

|

|

|

|

(Value Net of Additions and Subtractions) |

|

|

|

|

|

|

|

|

||

|

Page 1 of 2 |

|

FORM |

||

|

|

|

Version: March 2011 |

||

NOTE: A “fixture” is property that is affixed to real estate, which the Borrower(s) intend(s) (i): to keep so affixed during its useful life, and (ii) to be part of the real estate. Refrigerators,

NOTE: The acquisition cost of a Single Family Dwelling does not include:

(1)Usual and reasonable settlement and financing costs; “Settlement Costs” include titling and transfer costs, title insurance, survey fees and other similar costs; and “Financing Costs” include credit reference fees, legal fees, appraisal expenses, points which are paid by the Borrower, or other costs of financing the residence. Such amounts must not exceed the usual and reasonable costs which otherwise would be paid for in a similar loan,

(2)The imputed value of services performed by the Borrower or members of his family (which include only the Borrower’s parents, brother(s) and/or sister(s) [whether by whole or half blood], spouse, ancestors and lineal descendant(s) in constructing or completing the residence, or

(3)The cost of land which has been owned by the Borrower for at least 2 years before the date on which the construction of the structure comprising the Single Family Residence begins.

B.To the best of our knowledge, all of the land sold with this residence reasonably maintains the basic livability of the residence.

I fully understand the information set forth above is material to the Georgia Department of Community Affairs and declare under penalty of perjury, which is a felony offense in the State of Georgia that the above information is true and correct.

Subject Property Address: ________________________________________________________________

__________________________________________________________________ , Georgia

Borrower’s Signature |

|

Date |

|

|

|

|

Date |

|

|

|

|

Property Seller’s Signature |

|

Date |

|

|

|

Property Seller’s Signature |

|

Date |

I further certify that the real estate on which the home is located does not provide a source of income to the borrower.

______________________________________________________ |

________________________________ |

Borrower’s Signature |

Date |

______________________________________________________ |

________________________________ |

Co Borrower’s Signature |

Date |

Page 2 of 2 |

FORM |

|

Version: March 2011 |

| Fact Name | Details |

|---|---|

| Form Purpose | The SF 16 Georgia form is used for the Georgia Dream Homeownership Program to certify acquisition costs when applying for a mortgage. |

| Governing Law | This form is governed by the laws of the State of Georgia, specifically under the Georgia Department of Community Affairs regulations. |

| Borrower Information | The form requires the borrower's name and signature, ensuring they acknowledge the accuracy of the information provided. |

| Property Seller Details | Information about the property seller must also be included, including their signature, to confirm the sale. |

| Acquisition Cost Calculation | The form outlines specific components to include when calculating the total acquisition cost, such as purchase price and construction costs. |

| Exclusions from Costs | Certain costs are excluded from the acquisition cost, including usual settlement costs and the value of services provided by family members. |

| Fixtures Definition | A "fixture" is defined within the form, indicating what items are considered part of the real estate versus personal property. |

| Certification Requirement | Borrowers must certify that the information is true and correct, with penalties for false statements, emphasizing the seriousness of the declaration. |

| Submission Requirement | The completed form must be submitted with the purchase package for the Georgia Dream First Mortgage Program. |

Filling out the SF 16 Georgia form is a straightforward process that requires careful attention to detail. This form is essential for certifying the acquisition costs associated with the Georgia Dream Homeownership Program. Follow these steps to ensure accurate completion.

Once you have completed the form, review it carefully to ensure all information is accurate. This form should be submitted with your purchase package as part of the Georgia Dream First Mortgage Program. Ensure all signatures are in place before submission to avoid delays in processing.

What is the SF 16 Georgia form used for?

The SF 16 form is part of the Georgia Dream Homeownership Program. It is specifically used for the Acquisition Cost Certification. Borrowers must submit this form along with their purchase package when applying for the Georgia Dream First Mortgage Program. The form helps determine the total acquisition cost of the property, which includes the price of the land and dwelling, as well as any additional costs incurred during the purchase process.

What information do I need to provide on the SF 16 form?

When filling out the SF 16 form, you will need to provide details about the property, including the borrower's and seller's names, and the property's address. You will also need to calculate the acquisition cost by listing various expenses, such as the sales price, cost of land, interest paid during construction, and settlement costs. Additionally, you must account for any personal property items being purchased from the seller and the value of services performed by family members.

Are there any items that should not be included in the acquisition cost?

Yes, certain costs should not be included in the acquisition cost. These include usual and reasonable settlement and financing costs, the imputed value of services performed by the borrower or their family, and the cost of land owned by the borrower for at least two years before construction begins. It's important to ensure that only applicable costs are included to avoid complications with your application.

What happens if the information provided is found to be incorrect?

Providing false information on the SF 16 form is a serious matter. The form includes a declaration that the information is true and correct, and signing it under penalty of perjury can lead to felony charges in Georgia. Therefore, it is crucial to double-check all entries and ensure accuracy before submission.

Can I include the value of personal property items in the acquisition cost?

No, personal property items expected to be purchased from the seller must be subtracted from the total acquisition cost. This includes items that are not considered fixtures, such as refrigerators or free-standing stoves. Only the value of fixtures that are permanently affixed to the property should be included in the acquisition cost.

What is considered a "fixture" in the context of the SF 16 form?

A fixture is defined as property that is permanently affixed to real estate. It should be intended to remain affixed during its useful life and be considered part of the real estate. Examples of fixtures include built-in appliances and lighting fixtures. However, items like refrigerators and free-standing stoves are not considered fixtures unless they are built into the residence.

Inaccurate Calculation of Acquisition Costs: Many individuals miscalculate the total acquisition costs by failing to include all necessary components. This includes the purchase price, land costs, and additional expenses such as settlement costs. Each item must be accurately accounted for to avoid discrepancies.

Neglecting to Subtract Personal Property: Some borrowers forget to subtract the value of personal property items that are not fixtures. This can lead to an inflated total acquisition cost, which may affect eligibility for the program.

Omitting Important Documentation: It's essential to provide all required documentation when submitting the form. Missing documents can delay the process or result in denial of the application. Ensure that all necessary paperwork accompanies the form.

Misunderstanding the Definition of Fixtures: A common mistake is confusing personal property with fixtures. Understanding what qualifies as a fixture versus personal property is crucial. Items like refrigerators and free-standing stoves are not considered fixtures unless they are built into the home.

Failure to Review for Accuracy: Before submission, it is vital to review the entire form for accuracy. Simple errors, such as typos or incorrect figures, can have significant consequences. A thorough review can help catch mistakes that could affect the application.

The SF 16 form is a crucial document for participants in the Georgia Dream Homeownership Program. Alongside this form, several other documents are commonly required to ensure a complete application and compliance with program guidelines. Below is a list of these accompanying forms and documents, each serving a specific purpose in the home buying process.

Each of these documents plays a vital role in facilitating the home buying process and ensuring compliance with the Georgia Dream Homeownership Program. Proper preparation and submission of these forms can significantly enhance the likelihood of a smooth transaction.

Form 1003 (Uniform Residential Loan Application): Similar to the SF 16, this form collects essential information about the borrower and the property. Both documents require details about the acquisition costs and the financial background of the borrower.

Form 4506-T (Request for Transcript of Tax Return): This form is used to verify a borrower's income. Like the SF 16, it helps lenders assess the financial situation of the borrower to determine eligibility for financing.

Form 8821 (Tax Information Authorization): This document allows lenders to obtain tax information from the IRS. It serves a similar purpose as the SF 16 by ensuring that the lender has accurate financial data to evaluate the borrower's application.

Form 1065 (U.S. Return of Partnership Income): For borrowers who are business partners, this form provides insight into the financial health of the partnership. It complements the SF 16 by offering additional information about income sources.

Form 1099 (Miscellaneous Income): This form reports various types of income received by the borrower. It is similar to the SF 16 in that it helps lenders understand all income streams when assessing loan eligibility.

Form W-2 (Wage and Tax Statement): This document shows an employee's annual wages and the taxes withheld. Like the SF 16, it is used to verify income, which is crucial for determining the borrower's ability to repay the loan.

Form 4506 (Request for Copy of Tax Return): This form allows borrowers to request copies of their tax returns. It is similar to the SF 16 as it aids lenders in verifying the financial information provided by the borrower.

Form 1040 (U.S. Individual Income Tax Return): This is the standard tax return form for individuals. It provides a comprehensive view of a borrower’s financial situation, similar to the SF 16, which focuses on acquisition costs.

Form 1004 (Uniform Residential Appraisal Report): This form is used to assess the value of the property being purchased. It relates to the SF 16 as both documents address the financial aspects of acquiring a home.

When filling out the SF 16 Georgia form, it's essential to approach the process with care. Here’s a list of things you should and shouldn't do to ensure a smooth completion.

Pay attention to these guidelines. They can make a significant difference in the efficiency of your application process.

Understanding the SF 16 form for the Georgia Dream Homeownership Program is crucial for prospective homeowners. However, several misconceptions may lead to confusion. Here are four common misconceptions:

This form can be used by any eligible borrower participating in the Georgia Dream Homeownership Program, not just first-time buyers. It is designed to assess acquisition costs, regardless of previous homeownership experience.

Not all costs are included. Certain costs, such as usual settlement and financing costs, are excluded from the acquisition cost calculation. Only specific expenses outlined in the form should be considered.

Personal property items, like appliances that are not affixed to the home, must be subtracted from the acquisition cost. Only fixtures that are part of the real estate can be included.

The SF 16 form can be used for both new construction and existing homes. It assesses the acquisition costs of any eligible property under the program.

When filling out the SF 16 Georgia form for the Georgia Dream Homeownership Program, there are several important points to keep in mind:

By following these guidelines, you can help ensure a smooth application process for the Georgia Dream Homeownership Program.