A Promissory Note is a financial instrument that holds immense importance both for lenders and borrowers, as it embodies the promise of repayment under agreed terms. Such forms solidify the details of the loan taken, specifying the principal amount, interest rate, repayment schedule, and the consequences of failing to meet the agreed payments. At its core, this document establishes trust between parties, providing a legal framework that can be enforced in courts if necessary. It is adaptable, serving various needs from personal loans between family members to more significant loans required for starting a business. Understanding how to properly fill out and execute a Promissory Note can save individuals from potential future disputes, making it crucial for anyone considering lending or borrowing funds. In essence, these forms play a pivotal role in formalizing loans, ensuring both parties are clear on their obligations, and laying down a foundation for financial transactions to proceed smoothly and transparently.

Generic Promissory Note Template

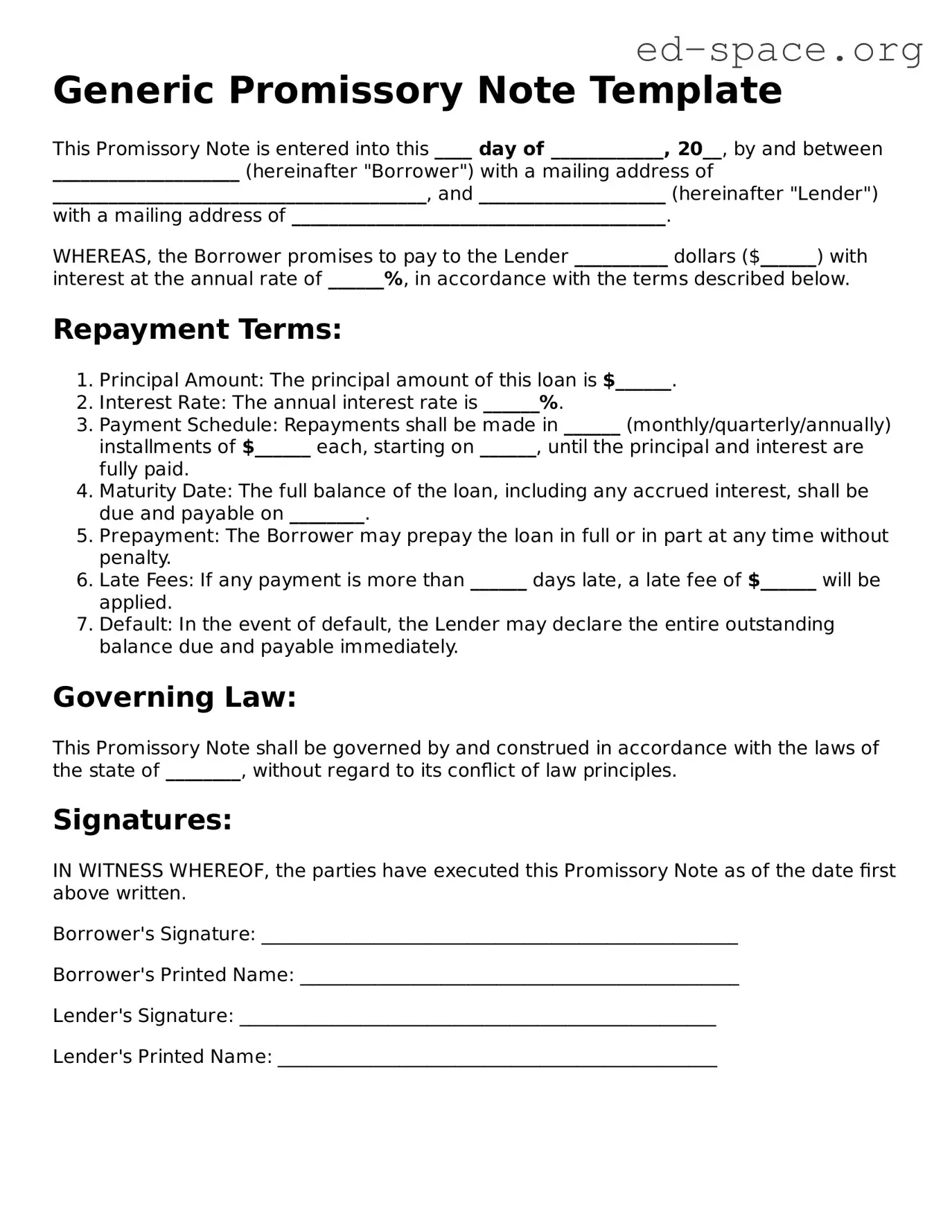

This Promissory Note is entered into this ____ day of ____________, 20__, by and between ____________________ (hereinafter "Borrower") with a mailing address of ________________________________________, and ____________________ (hereinafter "Lender") with a mailing address of ________________________________________.

WHEREAS, the Borrower promises to pay to the Lender __________ dollars ($______) with interest at the annual rate of ______%, in accordance with the terms described below.

Repayment Terms:

Governing Law:

This Promissory Note shall be governed by and construed in accordance with the laws of the state of ________, without regard to its conflict of law principles.

Signatures:

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: ___________________________________________________

Borrower's Printed Name: _______________________________________________

Lender's Signature: ___________________________________________________

Lender's Printed Name: _______________________________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a financial instrument that contains a written promise by one party (the issuer) to pay another party (the payee) a definite sum of money, either on demand or at a specified future date. |

| Legal Enforceability | Promissory notes are legally binding documents. The enforceability of these documents can lead to litigation if the borrower fails to fulfill the terms of the agreement. |

| Components | A standard promissory note typically includes the principal amount, interest rate, maturity date, date and place of issuance, and the signatures of the parties involved. |

| Governing Laws | The laws governing promissory notes can vary by state, but generally fall under the Uniform Commercial Code (UCC) which most states have adopted in some form. |

When preparing to lend money, filling out a promissory note form is a crucial step to ensure the repayment agreement is clearly documented. A promissory note is a binding legal document that outlines the terms under which the loan will be repaid, including the interest rate, repayment schedule, and actions in case of default. By following these steps, you can fill out the promissory note accurately and protect both parties involved in the transaction.

After filling out the promissory note form, it's important to store it in a safe place. This document serves as a legal proof of the loan's terms and conditions and will be crucial if any disputes arise or if enforcement of the agreement is necessary. Both the lender and the borrower should also consider maintaining open communication throughout the duration of the loan term to address any issues that may arise promptly.

What is a Promissory Note?

A Promissory Note is a financial document in which one party (the maker or issuer) promises in writing to pay a determinate sum of money to the other (the payee), either at a fixed or determinable future time or on demand of the payee, under specific terms.

What are the key elements that should be included in a Promissory Note?

Every Promissory Note should include the amount of money being borrowed, the interest rate if applicable, the repayment schedule or due date for the full amount, the signature of the borrower, and any collateral securing the note. It's also wise to include the names and addresses of both the borrower and lender, and the date the note was issued.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document. Once the borrower and the lender have signed the note, both parties are legally obligated to follow its terms. The lender is entitled to be repaid according to the agreed payment schedule, and the borrower is required to make those payments or face potential legal consequences.

Can a Promissory Note be modified?

A Promissory Note can be modified, but any changes must be agreed upon by both the borrower and the lender. The modification should be written and attached as an amendment to the original promissory note to keep the documentation clear and up to date. It's important that both parties sign any amendment, indicating their agreement to the new terms.

When individuals set out to fill a Promissory Note form, it's common to encounter certain pitfalls that can lead to complications down the line. Here we delve into five of the most typical mistakes that can easily be avoided with a bit of foresight and attention to detail.

Not specifying the loan details clearly: The cornerstone of any Promissory Note is the clarity of the loan specifics. Omitting the exact loan amount, interest rate, and repayment schedule can lead to disputes and confusion. It's vital to spell out these details meticulously to ensure both parties have a clear understanding of their obligations.

Failing to include the full legal name of all parties: Using nicknames or incomplete names might seem inconsequential, but in the realm of legal documents, precision is key. Ensure the full legal names of both the lender and borrower are included to avoid any ambiguities about who is bound by the terms of the note.

Overlooking the necessity of witnessing or notarization: Depending on state laws, some Promissory Notes must be either witnessed or notarized to be considered legally binding. Neglecting this step can jeopardize the enforceability of the document, potentially rendering it invalid in a court of law.

Ignoring state-specific legal requirements: Laws governing Promissory Notes can vary significantly from one state to another. It's not uncommon for individuals to overlook the necessity of adhering to their state's unique legal stipulations, such as maximum allowable interest rates (usury laws), which can invalidate the note or lead to legal penalties.

Forgetting to specify the consequences of default: A Promissory Note should always outline the actions that will be taken should the borrower fail to repay the loan as agreed. Without this information, the lender's options in the event of default may be significantly limited, making it more challenging to recover the owed amount.

By being mindful of these common mistakes and approaching the task of completing a Promissory Note with diligence and precision, lenders and borrowers can protect their interests and ensure that the agreement serves its intended purpose without leading to unnecessary legal entanglements.

When engaging in financial transactions that involve lending, a Promissory Note is often the primary document used to outline the terms of the loan. However, this form does not exist in isolation. Several other forms and documents typically accompany it, each serving a critical role in safeguarding the interests of the involved parties and ensuring the clarity and enforceability of the agreement. The following list describes some of these key documents.

Each of these documents plays a pivotal role in ensuring the integrity of the loan transaction. They provide layers of legal protection and clarity, mitigating potential misunderstandings or disputes between the lender and borrower. When used alongside the Promissory Note, these documents create a comprehensive framework for the lending process, ensuring that both parties are well-informed and agree on the specifics of the financial arrangement.

Loan Agreement: Both a promissory note and a loan agreement serve as written promises to pay back borrowed money. However, a loan agreement is typically more comprehensive, detailing the terms of the loan such as the repayment schedule, interest rates, and what happens in case of default. A promissory note might be considered a simpler version that mainly documents the promise to repay the amount.

Mortgage Note: A promissory note is similar to a mortgage note in that both commit the borrower to repay a sum of money. A mortgage note is specifically tied to real estate as collateral, specifying the terms of repayment for a loan used to purchase the property. This ties the borrower’s promise to repay to the legal claim against the property.

IOU (I Owe You): An IOU is a more informal acknowledgment of debt than a promissory note. While an IOU simply states that one party owes another a certain amount of money, a promissory note provides more detailed information, including how and when the debt will be repaid.

Personal Guarantee: A personal guarantee is akin to a promissory note in that it involves a promise to ensure the payment of a debt. In this case, someone else promises to repay the debt if the original borrower does not, providing an additional layer of security for the lender.

Bill of Sale: A bill of sale and a promissory note both serve as written evidence for transactions; however, their purposes diverge. A bill of sale proves the transfer of ownership of an item, whereas a promissory note documents the promise to pay a debt. They can be used together, particularly if the purchase involves deferred payments.

Credit Agreement: This is a formal agreement typically between a borrower and a bank, detailing the loan's terms, including repayment, financial covenants, and rights in the case of default. Like a promissory note, it is a debt instrument, but it often involves larger sums and more complex arrangements.

Debenture: Primarily used by corporations, a debenture is an unsecured loan certificate issued by a company, promising to repay the principal along with interest. Similar to a promissory note, it is a debt instrument, but debentures are often used for raising capital and may offer different protections and rights to investors.

Rental Agreement: Though not a debt instrument, a rental agreement shares similarities with a promissory note because it outlines terms between parties, such as a landlord and tenant, including payments to be made for the use of property. Both documents establish a set of agreed-upon terms that legally bind the parties.

When filling out a Promissory Note form, it's important to approach the process with care to ensure the agreement is clear and legally binding. Here are some key dos and don'ts to consider:

Do:Ensure all parties involved clearly understand the terms before proceeding. This means the borrower, lender, and any co-signers should have a mutual understanding of the repayment schedule, interest rate, and consequences of non-payment.

Use clear and concise language that all parties can understand. Avoid technical legal terms that might confuse those not familiar with legal jargon.

Be precise about the amounts, dates, and parties involved. This includes the full legal names of the borrower and lender, the loan amount, and the due date for the first payment as well as subsequent ones.

Specify the interest rate and how it is calculated, ensuring compliance with state laws regarding maximum rates.

Include clear terms about what happens in the event of a default by the borrower. This can cover options for the lender and any penalties for the borrower.

Sign the note in the presence of a notary or witnesses, depending on state requirements, to add another layer of validity.

Forget to include any key terms or details, as this can lead to disputes and legal complications down the road.

Leave blanks unfilled. If a section does not apply, mark it as "Not Applicable" or "N/A" to ensure clarity and prevent unauthorized alterations.

Fail to check state laws and regulations which might affect your Promissory Note. For instance, the enforceability of your agreement or the legal interest rate can vary from one state to another.

Sign without reviewing. Take the time to read through the entire document to confirm all information is correct and reflects the agreed terms.

Assume verbal agreements will be enforceable. Always include all agreed terms in the Promissory Note to ensure there is a clear, legal record.

Disregard the need for a witness or notary where required. Their endorsement can significantly strengthen the document's enforceability.

When it comes to understanding financial documents, the Promissory Note often comes with its share of misconceptions. These misunderstandings can lead to confusion and can impact the parties involved in significant ways. Here, we aim to clarify some common misconceptions regarding the Promissory Note form.

All Promissory Notes Are the Same: One common misconception is that all Promissory Notes are uniform, with no variance in terms or conditions. In reality, Promissory Notes can be highly customized to fit the agreement specifics between the lender and the borrower. They can include different interest rates, repayment schedules, and consequences of non-payment, reflecting the unique aspects of each loan agreement.

Only Banks Can Issue Them: Another misconception is that only banks or financial institutions can issue Promissory Notes. However, any individual or entity can create a Promissory Note as long as it is to document a loan between a borrower and a lender. This flexibility allows personal loans between family and friends to be formalized legally, ensuring clarity and legality in private lending.

They Are Legally Binding Without Being Witnessed or Notarized: People often think that for a Promissory Note to be legally binding, it needs to be witnessed or notarized. While having a Promissory Note notarized or witnessed can add an extra layer of protection and authentication, the note itself can be a legally binding document as long as it contains all essential elements and is signed by both parties.

No Need for a Written Agreement if Trust Is Involved: Trust between the parties might lead to a belief that a verbal agreement or a handshake is enough, sidelining the need for a written Promissory Note. This approach can lead to disputes and misunderstandings about the loan's terms. A written Promissory Note clearly outlines each party's obligations and expectations, providing a reference point that can prevent conflicts and help in legal enforcement if necessary.

Understanding these misconceptions is crucial for anyone involved in creating or signing a Promissory Note. It ensures that all parties are adequately informed and can proceed with confidence, knowing the legal implications and protections that a properly executed Promissory Note offers.

Filling out and using the Promissory Note form is a critical step for ensuring the terms of a loan are clear and legally binding. Here are four key takeaways to consider:

Accuracy is pivotal when completing a Promissory Note. It's essential to include precise information about the loan amount, interest rate, repayment schedule, and parties involved. Mistakes or omissions can lead to disputes or legal challenges.

Understanding the legal obligations is crucial for both the borrower and the lender. The Promissory Note details the borrower's promise to repay the loan under the agreed conditions. Failure to abide by these terms can result in legal repercussions.

Customizing the Promissory Note to fit specific needs can provide additional protection for the parties involved. Depending on the nature of the loan, incorporating clauses related to late fees, prepayment, or collateral might be advisable.

Securing signatures from both parties on the Promissory Note is necessary for it to be legally enforceable. A witness or notarization can further validate the document, adding an extra layer of authenticity and protection.

When these elements are carefully addressed, the Promissory Note serves as a vital document in defining the relationship between borrower and lender, offering clarity and legal grounding for the transaction.

Dwc-1 Form 2024 - The form helps establish a claim number for the injured employee.

Georgia Parts Replacement Verification Form - The form is a legal document that holds the owner accountable for the information provided.

How to Answer a Civil Summons Without an Attorney - The relief sought from the defendant should be clearly stated.