The Profit and Loss form is an essential financial document that provides a clear picture of a business's revenues and expenses over a specific period. By summarizing income generated from sales and services, it allows business owners to assess their overall profitability. Key components of the form include total revenue, cost of goods sold, gross profit, operating expenses, and net profit or loss. Each section plays a crucial role in understanding how well a business is performing financially. Additionally, the Profit and Loss form can highlight trends in revenue and expenses, enabling owners to make informed decisions about budgeting, investments, and operational adjustments. This form serves not only as a tool for internal management but also as a valuable resource for external stakeholders, such as investors and lenders, who are interested in the financial health of the business.

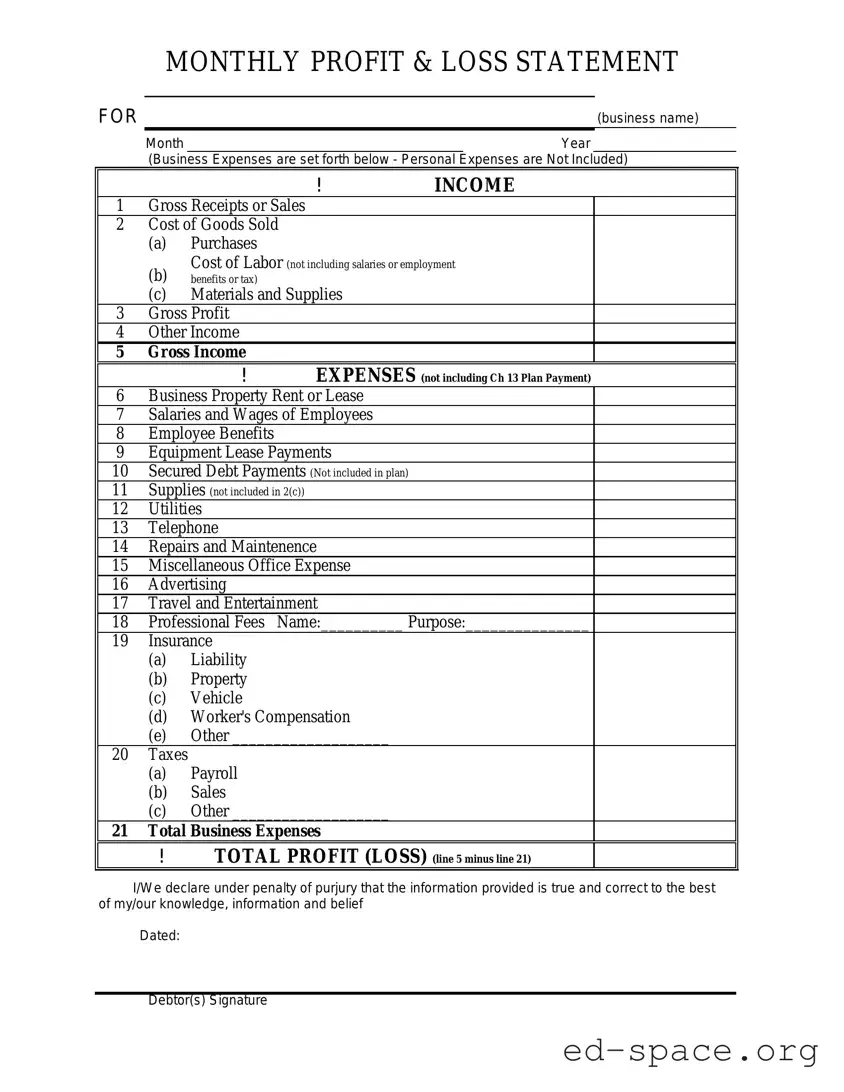

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form is used to summarize revenues, costs, and expenses over a specific period, providing a clear picture of a business's financial performance. |

| Components | This form typically includes sections for income, cost of goods sold, gross profit, operating expenses, and net income. |

| Frequency | Businesses often prepare Profit and Loss statements monthly, quarterly, or annually to track financial health and inform decision-making. |

| State-Specific Forms | Some states require specific formats for Profit and Loss statements, which may vary based on local regulations. |

| Governing Law (California) | In California, the Profit and Loss form must comply with the California Corporations Code, which outlines financial reporting requirements for businesses. |

| Governing Law (New York) | New York businesses must adhere to the New York Business Corporation Law, which specifies the necessary disclosures in financial statements. |

| Importance for Taxation | The Profit and Loss form is crucial for tax purposes, as it provides necessary information for calculating taxable income and fulfilling IRS requirements. |

Filling out the Profit and Loss form is an important step in tracking your business's financial performance. Once you have gathered all necessary financial information, you can begin the process. Follow these steps to complete the form accurately.

Once you have completed these steps, your Profit and Loss form will be ready for submission or further analysis. Make sure to keep a copy for your records.

What is a Profit and Loss form?

A Profit and Loss form, often referred to as a P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period. It provides a clear picture of a business's financial performance, showing whether it made a profit or a loss over that time frame. This form is essential for business owners, investors, and stakeholders to understand the company's financial health.

Why is the Profit and Loss form important?

The Profit and Loss form is crucial for several reasons. First, it helps business owners track their income and expenses, allowing them to make informed decisions. Second, it is often required for tax purposes, as it provides the necessary information to report earnings. Additionally, investors and lenders use this document to assess the viability of a business before making financial commitments.

How often should a Profit and Loss form be completed?

The frequency of completing a Profit and Loss form can vary based on the business's needs. Many businesses prepare this statement monthly or quarterly to keep a close eye on financial performance. Others may opt for an annual report, especially for tax purposes. Regular updates can help identify trends and make timely adjustments to improve profitability.

What are the main components of a Profit and Loss form?

A typical Profit and Loss form includes several key components: revenues (or sales), cost of goods sold (COGS), gross profit, operating expenses, and net profit. Revenues reflect the total income generated, while COGS accounts for the direct costs of producing goods or services. Gross profit is calculated by subtracting COGS from revenues. Operating expenses cover all other costs, and net profit is what remains after all expenses are deducted from total revenues.

How can I use the Profit and Loss form to improve my business?

Using the Profit and Loss form can provide valuable insights into your business's financial performance. By analyzing the data, you can identify areas where expenses can be reduced or revenues increased. For instance, if certain expenses are consistently high, it may be time to reevaluate those costs. Additionally, tracking trends over time can help you make strategic decisions, such as adjusting pricing or exploring new markets.

Can I create a Profit and Loss form myself?

Yes, you can create a Profit and Loss form on your own. Many templates are available online, making it easy to get started. You can also use accounting software that often includes built-in features for generating P&L statements. Just ensure that you accurately record all income and expenses to reflect your business's true financial position.

Not including all sources of income. It's essential to capture every revenue stream, no matter how small.

Failing to categorize expenses correctly. Misclassifying expenses can lead to inaccurate profit calculations.

Overlooking one-time expenses. These costs can significantly affect the overall profit and loss picture.

Forgetting to update the form regularly. Infrequent updates can result in outdated financial information.

Neglecting to include non-cash expenses, such as depreciation. These are important for a complete financial view.

Rounding figures improperly. Small rounding errors can accumulate and distort the final results.

Not reconciling with bank statements. Discrepancies can indicate errors that need correction.

Using estimates instead of actual figures. Estimates can lead to inaccuracies in the profit and loss statement.

Ignoring seasonal fluctuations in income and expenses. This can provide a misleading view of financial health.

Not seeking help when needed. Consulting with a financial professional can prevent many common mistakes.

The Profit and Loss form is a crucial document for understanding a business's financial performance over a specific period. However, it often works best when used alongside other important forms and documents that provide a fuller picture of a company's financial health. Here’s a list of related documents that can complement the Profit and Loss form.

Using these documents in conjunction with the Profit and Loss form can give you a comprehensive view of your business's financial landscape. Together, they help in making informed decisions and planning for the future.

The Profit and Loss form, often referred to as the income statement, serves a critical role in financial reporting. It provides an overview of a company's revenues, expenses, and profits over a specific period. Several other documents share similarities with the Profit and Loss form in their purpose and structure. Below are six such documents:

When filling out the Profit and Loss form, attention to detail is crucial. Here are ten important do's and don'ts to guide you through the process.

By following these guidelines, you can ensure that your Profit and Loss form is accurate and reliable.

The Profit and Loss (P&L) form is an essential financial statement for businesses, yet several misconceptions surround its purpose and function. Here are seven common misunderstandings:

Understanding these misconceptions can help individuals and businesses utilize the Profit and Loss form more effectively, leading to better financial management and decision-making.

Understanding how to effectively fill out and use the Profit and Loss form is crucial for managing finances. Here are some key takeaways to keep in mind: