When entering into a business agreement, understanding the Personal Guarantee form is crucial for both lenders and borrowers. This document serves as a promise from an individual, often a business owner or an executive, to take personal responsibility for the debts of a business. By signing this form, the individual guarantees that if the business defaults on its obligations, they will personally cover the outstanding debts. This adds a layer of security for lenders, as it mitigates their risk. The Personal Guarantee form typically includes essential details such as the names of the parties involved, the specific obligations being guaranteed, and any terms or conditions that apply. It is important to note that this form can take various forms, including limited and unlimited guarantees, which can significantly impact the extent of personal liability. Understanding these nuances is vital for anyone considering signing a Personal Guarantee, as it can have lasting financial implications. With the stakes high, being informed about the responsibilities and potential risks associated with this form is essential for making sound business decisions.

Personal Guarantee Template

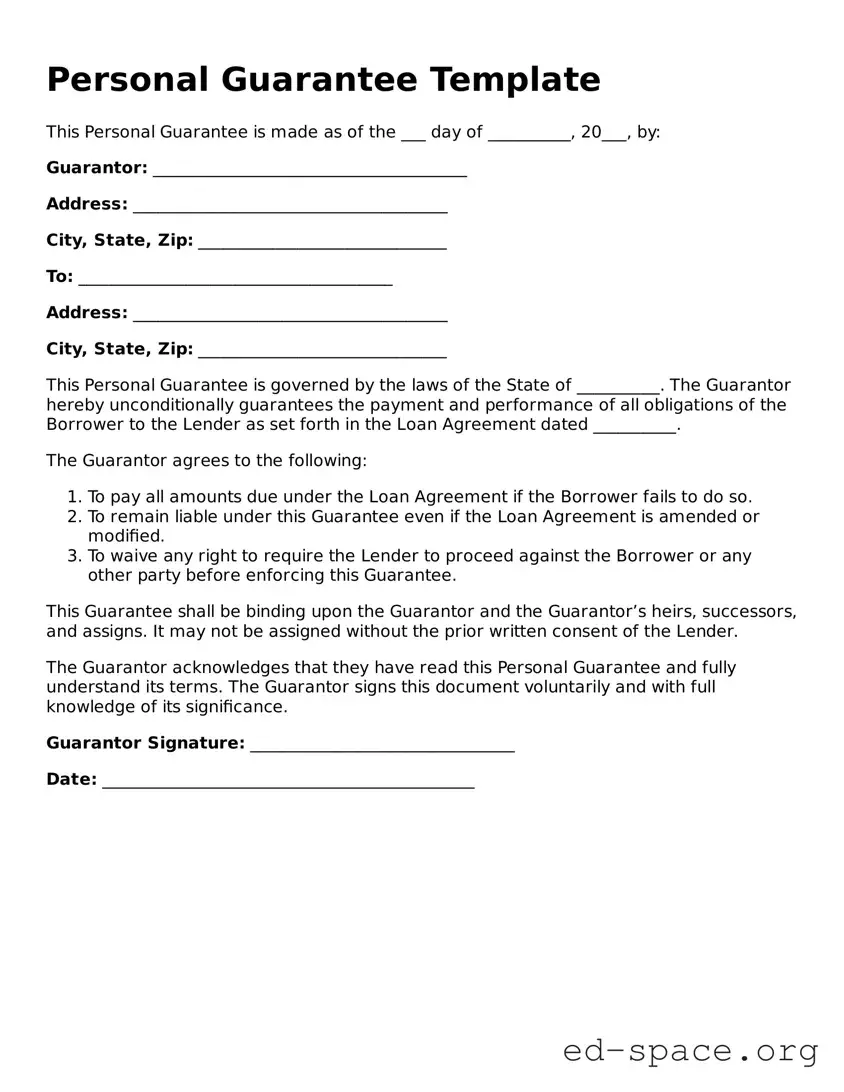

This Personal Guarantee is made as of the ___ day of __________, 20___, by:

Guarantor: ______________________________________

Address: ______________________________________

City, State, Zip: ______________________________

To: ______________________________________

Address: ______________________________________

City, State, Zip: ______________________________

This Personal Guarantee is governed by the laws of the State of __________. The Guarantor hereby unconditionally guarantees the payment and performance of all obligations of the Borrower to the Lender as set forth in the Loan Agreement dated __________.

The Guarantor agrees to the following:

This Guarantee shall be binding upon the Guarantor and the Guarantor’s heirs, successors, and assigns. It may not be assigned without the prior written consent of the Lender.

The Guarantor acknowledges that they have read this Personal Guarantee and fully understand its terms. The Guarantor signs this document voluntarily and with full knowledge of its significance.

Guarantor Signature: ________________________________

Date: _____________________________________________

| Fact Name | Description |

|---|---|

| Definition | A personal guarantee is a promise made by an individual to repay a debt or fulfill an obligation if the primary borrower defaults. |

| Purpose | This form is often used by lenders to secure loans by requiring a personal guarantee from individuals associated with a business. |

| Parties Involved | The form typically involves the lender and the individual providing the guarantee, often a business owner or executive. |

| State-Specific Forms | Each state may have its own version of the personal guarantee form, reflecting local laws and regulations. |

| Governing Law | The governing law for personal guarantees can vary by state, impacting enforcement and interpretation. |

| Liability | By signing the form, the individual accepts personal liability, which means their personal assets may be at risk if the debt is not repaid. |

| Duration | The guarantee may remain in effect until the debt is fully paid off or the lender releases the individual from their obligation. |

| Revocation | In some cases, a personal guarantee can be revoked, but this typically requires the lender's consent and may not be straightforward. |

| Legal Advice | It is advisable to seek legal counsel before signing a personal guarantee to understand the implications fully. |

After receiving the Personal Guarantee form, it is important to complete it accurately. This ensures that all necessary information is provided for processing. Follow the steps outlined below to fill out the form correctly.

Once the form is completed, it should be submitted according to the provided instructions. This may involve sending it via mail or delivering it in person. Ensure that all information is double-checked for accuracy before submission.

What is a Personal Guarantee form?

A Personal Guarantee form is a legal document in which an individual agrees to be personally responsible for the debts or obligations of a business. This means that if the business fails to pay its debts, the individual’s personal assets may be at risk. It is commonly used in business loans and credit agreements to provide lenders with additional security.

Who should consider signing a Personal Guarantee?

Individuals who are starting a business or seeking financing for an existing one should consider signing a Personal Guarantee. This includes business owners, partners, or anyone with a significant stake in the company. If the business lacks established credit or financial history, lenders may require a Personal Guarantee to mitigate their risk.

What are the risks associated with signing a Personal Guarantee?

Signing a Personal Guarantee carries significant risks. If the business cannot meet its financial obligations, the individual may be held liable for the debts. This could lead to personal bankruptcy or loss of personal assets, such as savings accounts, real estate, or other valuables. It’s crucial to fully understand these risks before signing.

Can a Personal Guarantee be revoked?

Generally, a Personal Guarantee cannot be revoked unilaterally once it has been signed. However, it may be possible to negotiate a release from the guarantee with the lender, especially if the business improves its financial standing or if other collateral is provided. Always consult with a legal professional before attempting to revoke a guarantee.

Are there different types of Personal Guarantees?

Yes, there are two main types of Personal Guarantees: unlimited and limited. An unlimited Personal Guarantee holds the individual responsible for the entire debt of the business without any cap. A limited Personal Guarantee, on the other hand, specifies a maximum amount that the individual will be liable for, providing some protection for personal assets.

What should I consider before signing a Personal Guarantee?

Before signing a Personal Guarantee, consider your financial situation and the potential risks involved. Evaluate the business's financial health, its ability to repay debts, and the likelihood of needing to fulfill the guarantee. Consulting with a financial advisor or attorney can provide valuable insights tailored to your specific circumstances.

How does a Personal Guarantee affect my credit score?

Signing a Personal Guarantee can impact your credit score, especially if the business defaults on its debts. If the lender reports the default to credit bureaus, it may affect your personal credit history. This could make it more challenging to secure personal loans or credit in the future.

What happens if the business defaults on its debts?

If the business defaults, the lender can pursue the individual who signed the Personal Guarantee for repayment. This could involve legal action to recover the owed amount. The lender may seek to collect from personal assets, which can lead to significant financial hardship for the guarantor.

Is legal advice necessary when signing a Personal Guarantee?

Yes, obtaining legal advice is highly recommended before signing a Personal Guarantee. A qualified attorney can help you understand the implications of the document, assess your financial risks, and ensure that you are making an informed decision. This step can save you from potential pitfalls down the line.

Inaccurate Personal Information: One common mistake is providing incorrect personal details. This includes misspelling names, entering wrong addresses, or using outdated contact information. Such errors can lead to complications in the enforcement of the guarantee.

Failure to Understand Obligations: Many individuals do not fully grasp what they are committing to when signing a personal guarantee. It’s crucial to understand that this document holds personal assets liable if the business fails to meet its obligations. Without this understanding, individuals may inadvertently expose themselves to significant financial risk.

Not Reviewing the Terms: Skipping the review of the terms and conditions is another frequent error. Individuals often rush through the form without carefully examining the specific obligations they are agreeing to. This oversight can result in unexpected liabilities.

Neglecting to Seek Legal Advice: Many people fill out the form without consulting a legal professional. This can be a costly mistake, as a lawyer can provide valuable insights and help clarify any ambiguous terms. Legal advice can be essential in protecting personal interests.

A Personal Guarantee form is often used in various business transactions to provide assurance for repayment or performance. Alongside this form, several other documents may be required to ensure a comprehensive understanding of the obligations and rights involved. Below is a list of commonly associated forms and documents.

Understanding these associated documents is crucial for ensuring all parties are aware of their responsibilities and protections. Each form plays a distinct role in the overall transaction, providing clarity and security for both the lender and the guarantor.

When filling out a Personal Guarantee form, attention to detail is crucial. Here are six important dos and don'ts to keep in mind:

Understanding the Personal Guarantee form can be challenging, and several misconceptions often arise. Here’s a list of ten common misunderstandings, along with clarifications to help demystify this important document.

This is not true. While many business owners use personal guarantees, individuals seeking loans or credit may also be required to sign one. Lenders often request a personal guarantee from anyone who is personally liable for the debt.

Not necessarily. A personal guarantee typically makes you responsible for the debt if the primary borrower defaults. However, the specifics can vary based on the agreement's terms.

This misconception can lead to surprises. Personal guarantees can be required for loans of any size, depending on the lender's policies and the borrower's creditworthiness.

While signing a personal guarantee creates a binding agreement, there may be options to renegotiate or release the guarantee under certain conditions. Always discuss this with your lender.

This is misleading. While it does provide security for the lender, it can also help the borrower secure financing. By offering a personal guarantee, you may access better loan terms or interest rates.

In reality, personal guarantees can also apply to leases, contracts, and other financial agreements. They serve as a promise to fulfill obligations if the primary party fails to do so.

This is not automatically the case. A personal guarantee itself does not impact your credit score. However, if the borrower defaults and you are unable to pay, your credit may be affected.

This is not universally true. Some lenders may offer loans without requiring personal guarantees, especially for well-established businesses with strong credit histories.

This is a common misconception. Unless your spouse or partner has signed the personal guarantee, they are not automatically liable for the debt. Each person’s financial obligations are typically separate.

This is incorrect. Personal guarantees can vary widely in terms of their conditions, limitations, and the extent of liability. It’s essential to read and understand the specific terms of any guarantee you are considering.

By addressing these misconceptions, individuals can make more informed decisions when it comes to signing a Personal Guarantee. Always consult with a financial advisor or legal professional if you have questions about your obligations and rights.

Filling out and using a Personal Guarantee form is a critical step in many business transactions. Here are some key takeaways to consider:

Being informed and proactive can help mitigate risks associated with a Personal Guarantee. Take the time to understand your responsibilities fully.