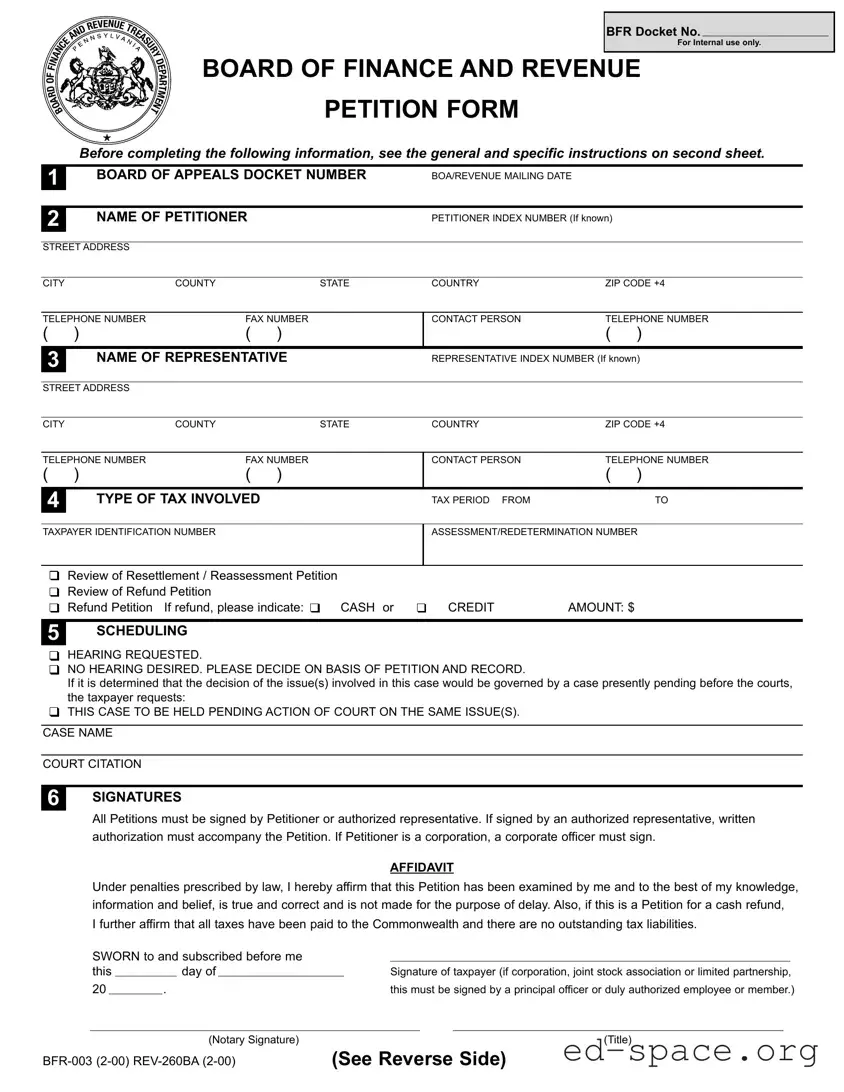

The Pennsylvania BFR 003 form serves as a crucial tool for taxpayers seeking to challenge decisions made by the Board of Appeals or request a refund of taxes they believe were improperly assessed. This form is essential for those navigating the complexities of tax disputes, allowing individuals and businesses to formally present their cases to the Board of Finance and Revenue. Key components of the form include sections for the petitioner’s information, the type of tax involved, and specific details regarding the tax period in question. Additionally, it requires a clear articulation of the relief sought and the arguments supporting the petition. Taxpayers must also provide necessary documentation, such as proof of payment and any relevant notices being appealed. Importantly, the form must be signed by the petitioner or an authorized representative, with notarization required to validate the submission. Understanding the structure and requirements of the BFR 003 form is vital for anyone looking to effectively advocate for their tax rights in Pennsylvania.

| Fact Name | Details |

|---|---|

| Governing Law | The Pennsylvania BFR 003 form is governed by the Pennsylvania Consolidated Statutes, Title 72, which outlines tax appeals and procedures. |

| Purpose | This form is used to petition the Board of Finance and Revenue for a review of decisions made by the Board of Appeals or for a refund of taxes. |

| Filing Deadline | Petitions must be filed within specific time limits set by law, depending on the type of tax involved. The postmark date is used for submissions via U.S. Postal Service. |

| Signature Requirement | All petitions must be signed by the petitioner or an authorized representative. Notarization is also required to affirm the truthfulness of the petition. |

Completing the Pennsylvania BFR 003 form involves several steps to ensure all necessary information is accurately provided. This form is used to petition the Board of Finance and Revenue regarding tax matters. Following the steps outlined below will help in submitting a complete and correct petition.

After submitting the form, you will await further communication from the Board of Finance and Revenue. They may schedule a hearing or make a decision based on the petition and supporting documents provided. It is crucial to keep track of any deadlines and ensure that all necessary materials are submitted on time.

What is the Pennsylvania BFR 003 form?

The Pennsylvania BFR 003 form is a petition form used to appeal decisions made by the Board of Appeals or to request a review of an assessment, redetermination, or resettlement by the Department of Revenue. Taxpayers can also use this form to seek refunds for taxes they believe were improperly paid to the Commonwealth.

Who can file a BFR 003 petition?

Any taxpayer who feels aggrieved by a decision from the Board of Appeals or who wishes to challenge an assessment or seek a refund can file this petition. This includes individuals, corporations, and other entities that have a tax liability in Pennsylvania.

What information is required to complete the form?

The form requires various details, including the petitioner's name, address, and contact information. You will also need to provide the type of tax involved, the tax period, and any relevant identification numbers. If applicable, details about a representative must be included, along with the specific relief requested and arguments supporting the request.

How do I submit the BFR 003 form?

The completed form should be mailed to the Commonwealth of Pennsylvania Board of Finance and Revenue at the specified address: 1101 South Front Street, Suite 400, Harrisburg, PA 17104-2539. It is important to ensure that the form is sent well before any deadlines to avoid complications.

What is the significance of the hearing request on the form?

On the BFR 003 form, you can indicate whether you want a hearing or if you prefer the Board to decide based on the petition and the record. If a hearing is requested, you will receive a notice of the hearing date. If you do not wish to attend, the Board can still make a decision based on the submitted materials.

Are there any deadlines for filing the BFR 003 form?

Yes, all petitions must be filed within specific time limits established by law for the type of tax involved. If you are mailing the petition, it is considered filed based on the postmark date. Therefore, it is crucial to be mindful of these deadlines to ensure your petition is accepted.

What kind of evidence should accompany my petition?

When submitting your petition, include any supporting evidence that bolsters your arguments. This may consist of copies of notices being appealed, proof of tax payment, invoices, or other relevant documents. It is essential to provide this evidence as soon as possible, ideally before five working days of the hearing date.

What happens if my case involves an issue currently pending in court?

If your case relates to an issue that is pending before the courts, you have the option to request that your case be held until the court reaches a decision. Alternatively, you can choose to proceed with the hearing. However, the Board typically does not grant relief while similar issues are being litigated in court, as they consider their position to be valid until the courts decide otherwise.

What are the signature requirements for the BFR 003 form?

All petitions must be signed by the petitioner or an authorized representative. If someone other than the petitioner is signing, a written authorization must accompany the petition. For corporate petitions, a principal officer or duly authorized employee must sign the form. Additionally, the petition must be notarized to confirm its authenticity.

Failing to read the general and specific instructions on the second sheet can lead to incorrect submissions.

Omitting the Board of Appeals Docket Number and mailing date when petitioning for review can result in delays.

Not completing all required information in Block 2 may cause the petition to be rejected.

Neglecting to indicate the type of tax involved can create confusion and hinder processing.

Forgetting to check one of the three blocks regarding the type of petition can lead to misclassification.

Submitting multiple petitions for the same tax year or type without separating them may complicate the review process.

Failing to include the taxpayer identification number and any assessment number can delay the case.

Not requesting a hearing when desired can limit the taxpayer's opportunity to present their case.

Neglecting to sign and notarize the petition can result in immediate rejection.

Submitting evidence after the five working days deadline prior to the hearing date may lead to exclusion from consideration.

When filing a petition using the Pennsylvania BFR 003 form, several other documents may be necessary to support your case. These documents provide additional context and evidence to strengthen your petition. Below is a list of commonly used forms and documents that may accompany the BFR 003 form.

Each of these documents plays a vital role in ensuring that your petition is complete and well-supported. By including all necessary paperwork, you enhance your chances of a favorable outcome. It is always advisable to carefully review each document and ensure that they align with the information provided in your BFR 003 form.

When filling out the Pennsylvania BFR 003 form, consider the following dos and don'ts:

Misconceptions about the Pennsylvania BFR 003 form can lead to confusion and errors in the petition process. Below are some common misconceptions along with clarifications.

Filling out the Pennsylvania BFR 003 form requires careful attention to detail. Here are five key takeaways to consider:

By keeping these points in mind, you can navigate the process more effectively and increase the likelihood of a favorable outcome.