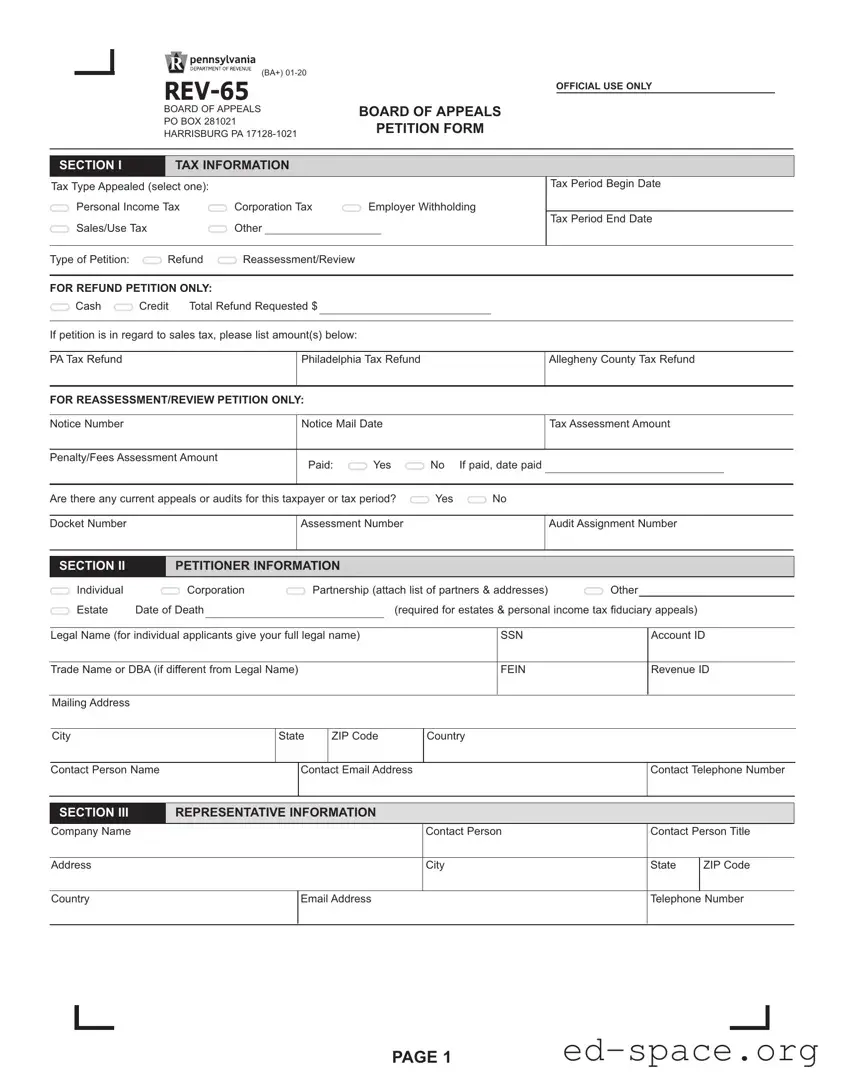

The Pennsylvania form, known as the REV-65 Board of Appeals Petition, serves as a crucial tool for taxpayers seeking to contest various tax-related issues. It allows individuals and businesses to appeal decisions regarding personal income tax, corporation tax, employer withholding, and sales/use tax, among others. The form requires detailed information about the tax period in question, including start and end dates, as well as the specific type of petition being filed—whether for a refund or for reassessment and review. Taxpayers must also provide their legal name, Social Security number, and relevant account identifiers, ensuring that the Board of Appeals can accurately process their requests. Additionally, the form includes sections for listing any current appeals or audits, which can impact the outcome of the petition. A clear outline of the issues involved is essential, as petitioners must articulate their concerns and the reasons for seeking relief. Importantly, all petitions must be signed by the petitioner or an authorized representative, emphasizing the necessity of proper authorization and compliance with legal requirements. Taxpayers are encouraged to submit their petitions online for efficiency, although mail submissions are also accepted. By understanding the intricacies of the REV-65 form, individuals and entities can navigate the appeals process more effectively, ensuring their voices are heard in matters of tax assessment and refunds.

(BA+)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax Type Appealed (select one): |

|

|

|

|

|

|

|

|

|

Tax Period Begin Date |

||||

|

|

|

|

|

|

|

|

|

|

|

||||

Personal Income Tax |

|

Corporation Tax |

Employer Withholding |

|

|

|||||||||

Sales/Use Tax |

|

Other |

|

|

|

|

|

|

Tax Period End Date |

|||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Type of Petition: |

|

Refund |

Reassessment/Review |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash |

Credit |

Total Refund Requested $ |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If petition is in regard to sales tax, please list amount(s) below: |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

PATax Refund |

|

|

|

|

|

Philadelphia Tax Refund |

|

|

|

Allegheny County Tax Refund |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Notice Number |

|

|

|

|

|

Notice Mail Date |

|

|

|

Tax Assessment Amount |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Penalty/Fees Assessment Amount |

|

|

Paid: |

Yes |

No |

If paid, date paid |

||||||||

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Are there any current appeals or audits for this taxpayer or tax period? |

Yes |

|

No |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

Docket Number |

|

|

|

|

|

Assessment Number |

|

|

|

Audit Assignment Number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Individual |

Corporation |

|

|

Partnership (attach list of partners & addresses) |

Other |

|

||||||

Estate |

Date of Death |

|

|

|

|

(required for estates & personal income tax fiduciary appeals) |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal Name (for individual applicants give your full legal name) |

|

|

SSN |

|

|

Account ID |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade Name or DBA (if different from Legal Name) |

|

|

|

|

FEIN |

|

|

Revenue ID |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

|

|

State |

|

ZIP Code |

|

Country |

|

|

|

||

|

|

|

|

|

|

|

|

|

||||

Contact Person Name |

|

Contact Email Address |

|

|

Contact Telephone Number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

V

Company Name

Address

Country

Contact Person |

Contact Person Title |

||

City |

State |

|

ZIP Code |

|

|||

|

|

|

|

Email Address |

Telephone Number |

||

V

Hearing Requested |

No Hearing Requested. Please decide on basis of the petition and record. |

|||

This case to be held pending action on the same issue(s). Case Number |

|

Court Citation Number |

||

|

|

|

|

|

V

If you elect to receive communications via email, you are authorizing the Board ofAppeals to send correspondence, including the final Decision & Order, via email.

Send Correspondence to (select one): |

Petitioner |

Representative |

Send Correspondence via (select one): |

U.S. Mail |

|

Send Decision and Order via (select one): |

U.S. Mail |

V

Itemize the issue(s) involved. What is the subject of appeal? Attach a separate sheet if more space is required.

V

All petitions must be signed by the petitioner or authorized representative. If signed only by an authorized representative, written authorization must accompany the petition. If the petitioner is a corporation, a corporate officer must sign.

Under penalties prescribed by law, I hereby certify this petition has been examined by me, and to the best of my knowledge, information and belief, the facts contained in the petition are true, correct and complete and the petition is not made for the purpose of delay. Also, if this is a petition for refund, I certify that the refund requested has not been granted in an audit report, nor has it been included in any other petition for refund.

Petitioner’s Name |

Petitioner’s Signature |

Petitioner’s Title |

Date |

|

|

|

|

Representative’s Name |

Representative’s Signature |

Representative’s Title |

Date |

|

|

|

|

Please type or print neatly in blue or black ink.Attach acopy of the notice being appealed.

Petitions should be sent directly to the Board of Appeals online or by mail. The preferred method of filing is online because this method provides a confirmation number. Online petitions are filed through the Board of Appeals

website at rdppssttpus .The mailing address for the Board ofAppeals is:

-

Petition is considered filed as of the postmark date. Meter dates or any other mark (except the USPS postmark) is not recognized. Failure to include any required information may result in a dismissal of your appeal.

The Board of Appeals will consider compromises of assessment and refund appeals. If you wish to propose a compromise, please complete and submit a Request for Compromise

SECTION I

Fillintheovalforthetaxtypebeingappealed.Administrative Appeals of Record such as revocation of a lottery license can be identified in Other.

Please clearly identify the tax period being appealed.

Fillinonlyoneovalforthetypeofpetition.Donotmarkboth.

INSTRUCTIONS FOR

Board of Appeals Petition Form

If there are any current appeals or audit for this taxpayer or tax period, provide docket number, assessment number and/or audit assignment number. This section is applicable topetitionsforrefundandpetitionsforreassessment/review.

SECTION II

Social Security number is required for Individual, Estate and Partnership appeals. Include Social Security number for each partner when providing list of partner names and addresses.

The department is authorized under federal law, 42 U.S.C. § 405 (c), to use your Social Security number in administering state tax law.The department uses your Social Security number to establish your identity and to process your appeal.

Account ID Number is the number used to identify the tax account being appealed. Examples include the Sales Tax License Number, the Corporate Box Number, Estate File Number or Control Number.

FederalEmployerIdentificationNumberisissuedbytheIRS to business entities. Complete this number if one has been assigned to you.

Departmental issued number assigned to each business entity with a filing requirement in PA.

SECTION III

V

Representation by an attorney, CPA or other person is not required. Complete representative information only if Petitioner is represented by another person.

|

SECTION IV |

|

|

Provide refund form and amount requested. If the refund |

|

|

|

|

|

||

requested is for sales tax, provide requested amounts for |

Hearings,ifrequested,areheldinHarrisburg.Petitionermay |

||

PA tax refund. If applicable, provide amounts for |

|||

Philadelphia tax refund orAllegheny County tax refund. |

request a phone conference in lieu of a hearing. It is at the |

||

Board’s discretion whether to grant this request. |

|||

|

|||

Provide notice number, notice mail date, tax assessment |

SECTION V |

|

|

amount, and penalty/fees assessment amount. If the tax |

|

|

|

|

|

|

|

assessment amount and penalty/fees assessment amount |

|

|

|

have been paid in full, provide date paid. |

Please select desired method of correspondence. |

|

|

|

|

|

|

rvupv |

- |

1 |

|

Communication, including the board’s final decision and order, may be transmitted to you or your representative via email, should you elect the email option. If you elect to receive communications via email, you and your representatives assume the responsibility for the confidentiality of the information contained in emails sent to and from the Board ofAppeals. The commonwealth will not be held liable for the disclosure of any confidential information sent via email.

SECTION VI

Briefly state the issue(s) involved and explain in detail why relief should be granted.Additional pages may be attached, if necessary.

Any required appeal schedule should be submitted with the petition or within 30 days of the date that the petition is filed. Any evidence in support of the petition may be submitted with the petition but no later than 60 days from the date that the petition is filed.

SECTION VII

All petitions must be signed by the Petitioner and/or Authorized Representative. A Power of Attorney

2 - |

rvupv |

| Fact Name | Description |

|---|---|

| Governing Law | The Pennsylvania Board of Appeals operates under the Pennsylvania Consolidated Statutes, Title 72, Taxation. |

| Filing Method | Petitions can be filed online or by mail. Online filing is preferred due to confirmation number issuance. |

| Required Information | Petitions must include the petitioner's legal name, tax identification numbers, and the specific tax type being appealed. |

| Signature Requirement | All petitions must be signed by the petitioner or an authorized representative, accompanied by written authorization if applicable. |

Filling out the Pennsylvania form requires careful attention to detail. It is important to ensure all necessary information is provided accurately to avoid delays or complications with your appeal.

What is the purpose of the Pennsylvania form REV-65?

The Pennsylvania form REV-65 is used to file a petition with the Board of Appeals regarding various tax matters. Taxpayers can appeal decisions related to personal income tax, corporation tax, employer withholding, sales/use tax, or other tax types. This form allows individuals or entities to request a refund, reassessment, or review of their tax situation. It is essential for taxpayers who believe they have been incorrectly assessed or wish to contest a tax decision made by the Pennsylvania Department of Revenue.

How do I complete the form REV-65?

To complete the REV-65 form, start by selecting the tax type you are appealing and specifying the tax period involved. You will need to provide detailed information, including your legal name, mailing address, and relevant identification numbers, such as your Social Security Number or Federal Employer Identification Number. Be sure to clearly state the issues involved in your appeal and provide any necessary documentation, such as the notice you are appealing. Remember to sign the petition, as it must be signed by either the petitioner or an authorized representative.

What happens after I submit the REV-65 form?

Once you submit the REV-65 form, the Board of Appeals will review your petition. If you have requested a hearing, it may be scheduled in Harrisburg, or you can request a phone conference instead. The Board will consider your appeal based on the information provided. If additional evidence is required, you may need to submit it within 60 days of filing the petition. The Board will communicate its decision to you through the method you selected, either by U.S. mail or email.

Can I represent myself, or do I need an attorney to file the REV-65?

You do not need an attorney to file the REV-65 form. Taxpayers can represent themselves when submitting an appeal. However, if you choose to have someone else, such as an attorney or CPA, represent you, you must provide their information on the form. If the petition is signed only by the authorized representative, a Power of Attorney form (REV-677) must accompany the petition to validate their authority to act on your behalf.

What if I want to propose a compromise regarding my tax assessment?

If you wish to propose a compromise on your assessment or refund appeal, you must complete a Request for Compromise (DBA-10) form. This request should be submitted alongside your REV-65 petition or within 30 days from the date you file your petition. The Board of Appeals will consider your proposal as part of the review process, and it is important to clearly outline your reasons for seeking a compromise in your submission.

Incomplete Information: Many individuals fail to provide all required details, such as the tax period or the type of petition. Omitting this information can lead to delays or dismissals.

Incorrect Tax Type Selection: Selecting the wrong tax type can complicate the appeal process. It is crucial to carefully choose the correct category, whether it be Personal Income Tax, Corporation Tax, or others.

Missing Signatures: All petitions must be signed by the petitioner or an authorized representative. Neglecting to include a signature can result in the petition being considered invalid.

Failure to Attach Required Documents: Not attaching the notice being appealed is a common mistake. This document is essential for the Board of Appeals to process the petition effectively.

Ignoring Deadlines: Each petition has specific deadlines for submission and additional documentation. Missing these deadlines can jeopardize the appeal.

Inadequate Explanation of Issues: Providing a vague or incomplete description of the issues involved can hinder the Board's understanding of the appeal. A detailed explanation is vital for a fair review.

When filing a petition with the Pennsylvania Board of Appeals, there are several forms and documents that may be necessary to support your case. Understanding these documents can help ensure that your appeal process goes smoothly and effectively.

Being aware of these additional forms and documents can significantly improve your chances of a successful appeal. Make sure to prepare all necessary materials ahead of time to avoid delays in the process.

The Pennsylvania form (REV-65) for Board of Appeals petitions shares similarities with several other legal documents commonly used in tax-related appeals. Each of these documents serves specific purposes but often follows a similar structure and process. Here are six documents that resemble the Pennsylvania form:

Understanding these similarities can help taxpayers navigate the often complex landscape of tax appeals. Each form, while unique to its jurisdiction, shares a common purpose: to ensure taxpayers have a fair opportunity to contest tax assessments they believe are incorrect.

When filling out the Pennsylvania form, there are specific actions to take and avoid to ensure the process runs smoothly. Below is a list of guidelines to follow.

Misconceptions about the Pennsylvania form for tax appeals can lead to confusion and potential issues in the appeal process. Here are four common misconceptions:

In reality, all petitions must include supporting documents, such as the notice being appealed. This is crucial for the Board of Appeals to understand the context of the appeal.

Every appeal must adhere to strict deadlines. Petitions are considered filed based on the postmark date. Missing the deadline can result in dismissal of the appeal.

This is not true. Representation by an attorney, CPA, or other person is optional. Petitioner can represent themselves if they choose to do so.

Not all petitions will result in a hearing. Petitioners can request a hearing, but it is at the Board's discretion whether to grant this request based on the specifics of the case.

When filling out and using the Pennsylvania Board of Appeals form (REV-65), there are several important points to keep in mind. Understanding these key takeaways can help ensure a smoother process for your tax appeal.

By following these guidelines, you can navigate the appeals process with greater confidence and clarity. Remember, the goal is to present your case as clearly and thoroughly as possible to achieve a favorable outcome.