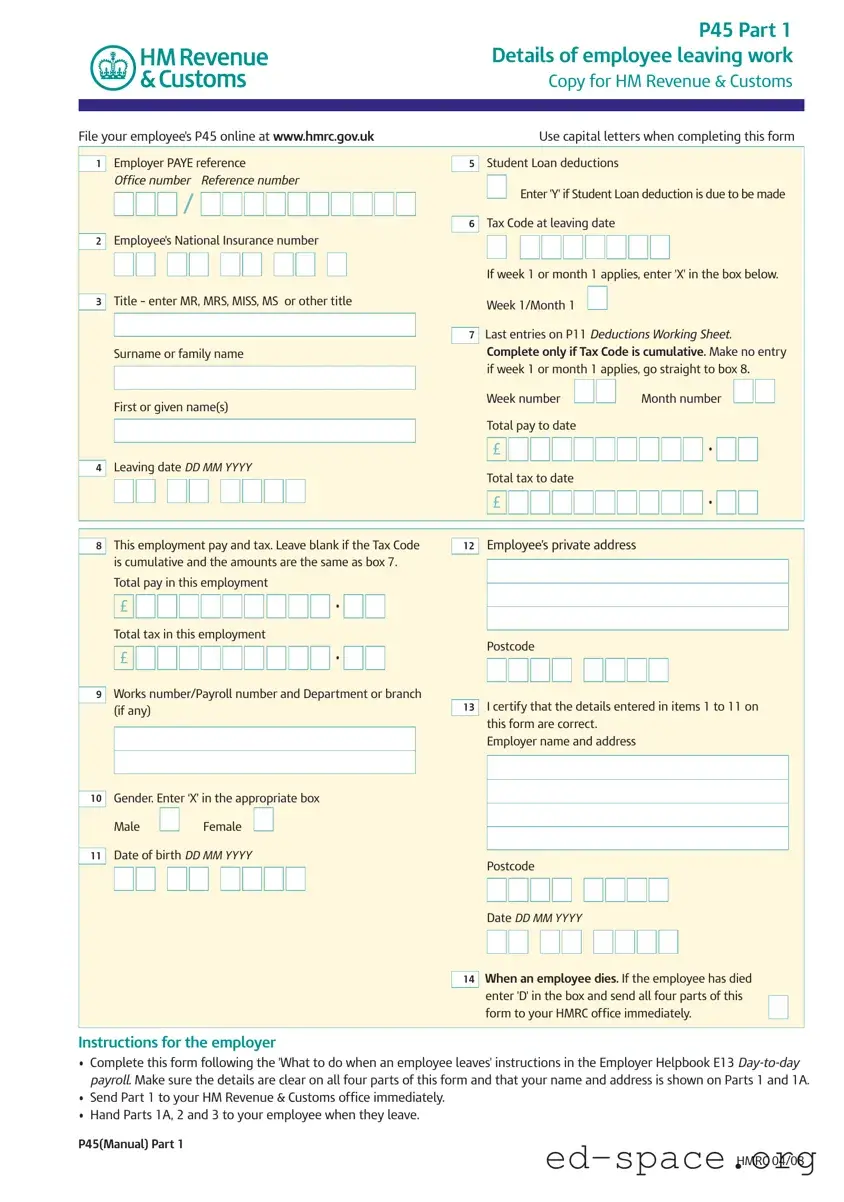

The P45 form is an essential document for both employers and employees in the United Kingdom, particularly during the transition between jobs. It serves multiple purposes, providing crucial information about an employee's tax status and earnings at the time of leaving a job. The form is divided into three parts, with each part designated for different stakeholders: HM Revenue & Customs (HMRC), the departing employee, and the new employer. When an employee leaves a job, the employer must complete the P45, detailing the employee's total pay and tax deductions to date, along with their National Insurance number and leaving date. Employers are responsible for sending the first part of the form to HMRC promptly, while the remaining parts are handed to the employee. This documentation is vital for the employee, as it helps ensure that they are taxed correctly in their new role or when claiming benefits. The P45 also includes specific instructions for handling situations such as student loan deductions and what to do if the employee has passed away. Understanding the P45 form is important for maintaining accurate tax records and ensuring a smooth transition in employment.