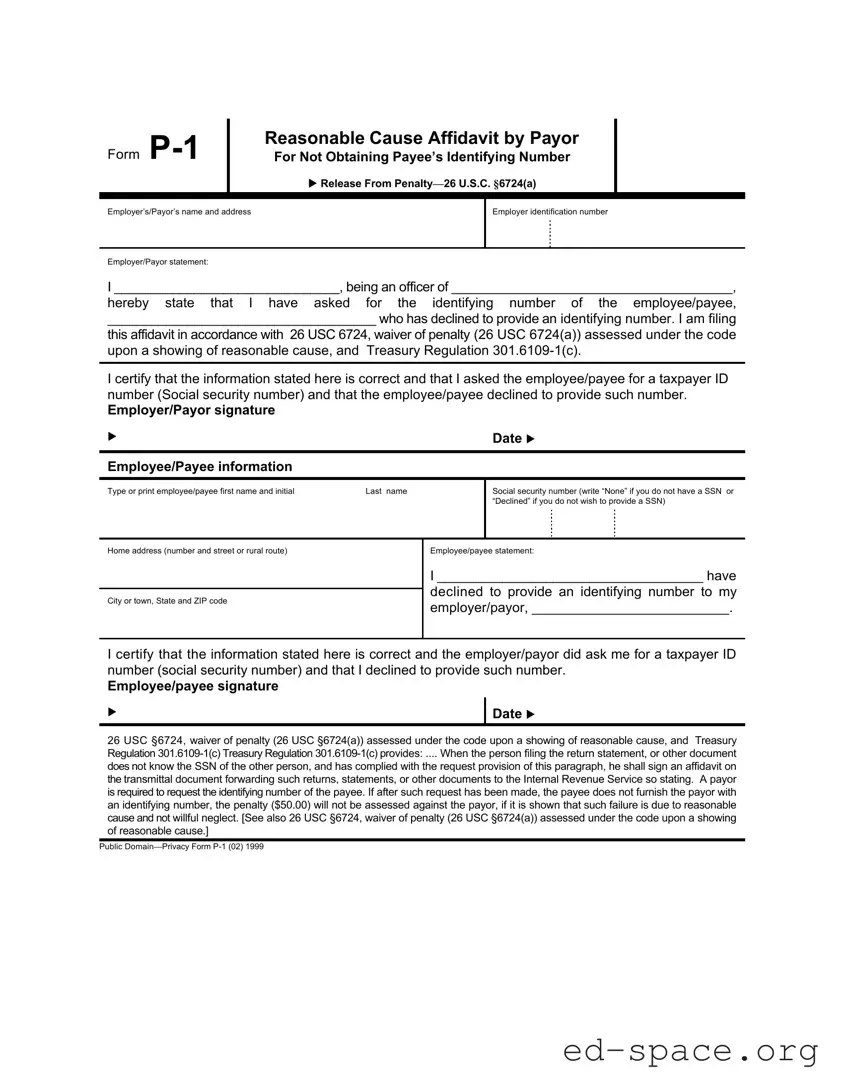

The P 1 form, officially known as the Reasonable Cause Affidavit by Payor for Not Obtaining Payee’s Identifying Number, serves a critical function for employers and payors navigating the complexities of tax compliance. This form allows an employer to declare that they have requested the identifying number of an employee or payee, who has declined to provide it. By filing this affidavit, the employer seeks a waiver of any penalties that may arise from the failure to obtain this information, as outlined in 26 U.S.C. §6724(a). The form requires the employer’s name, address, and identification number, alongside a statement affirming that they have made a reasonable effort to obtain the necessary taxpayer ID number. It also includes sections for the employee or payee to confirm their refusal to provide such information. This process is governed by Treasury Regulation 301.6109-1(c), which stipulates that if a payor has made a proper request for the identifying number and the payee does not comply, the payor can avoid penalties, provided they demonstrate reasonable cause for the omission. Thus, the P 1 form is not just a bureaucratic requirement; it is a safeguard for payors against potential financial penalties while ensuring compliance with federal tax regulations.

| Fact Name | Description |

|---|---|

| Purpose of Form P-1 | This form serves as a Reasonable Cause Affidavit by the payor for not obtaining the payee's identifying number. It is essential for employers to document their efforts to request this information. |

| Governing Law | The form is governed by 26 U.S.C. §6724(a), which outlines the waiver of penalties for payors who demonstrate reasonable cause for not obtaining a payee's identifying number. |

| Employer/Payor Requirements | Employers must request the identifying number from the payee. If the payee declines to provide it, the employer can file this affidavit to avoid penalties. |

| Employee/Payee Statement | The payee must confirm their refusal to provide the identifying number, affirming that the employer did indeed ask for it. |

| Signature Requirement | Both the employer/payor and the employee/payee are required to sign the form to validate the statements made within it. |

| Regulatory Reference | Treasury Regulation 301.6109-1(c) provides additional context, stating that an affidavit must accompany returns if the payor does not know the payee's SSN. |

After completing the P-1 form, it will be submitted to the Internal Revenue Service (IRS) to demonstrate that reasonable cause exists for not obtaining the payee's identifying number. This form serves as a declaration that the payee declined to provide their taxpayer ID number, which is necessary to avoid penalties.

What is the purpose of the P-1 form?

The P-1 form serves as a Reasonable Cause Affidavit by a payor who has not been able to obtain the identifying number of a payee. This form is particularly important for employers who have requested their employees' taxpayer identification numbers but have been declined. By filing this form, the payor can demonstrate reasonable cause to avoid penalties for failing to provide the required information to the IRS.

Who needs to fill out the P-1 form?

The P-1 form is intended for employers or payors who have requested an identifying number from a payee, such as an employee, but have not received it. If the payee has declined to provide their Social Security Number (SSN) or other taxpayer identification number, the payor must complete this form to document the request and the payee's refusal.

What information is required on the P-1 form?

To complete the P-1 form, the payor must provide their name, address, and employer identification number. Additionally, the form requires the payee's name, address, and the status of their SSN—either "None" if they do not have one or "Declined" if they choose not to provide it. Both the payor and payee must sign the form to certify the accuracy of the information provided.

What happens if the payee does not provide their identifying number?

If the payee refuses to provide their identifying number after the payor has made a formal request, the payor can file the P-1 form. This filing can help the payor avoid a $50 penalty imposed by the IRS for not having the payee's identifying number, provided that the failure to obtain the number is shown to be due to reasonable cause and not willful neglect.

What is considered 'reasonable cause' under the P-1 form?

Reasonable cause refers to circumstances that prevent the payor from obtaining the payee's identifying number despite making a good faith effort. This includes situations where the payee has explicitly declined to provide their number. The IRS recognizes that not all failures to obtain an identifying number are due to negligence, and the P-1 form helps to substantiate this claim.

How does the P-1 form relate to IRS regulations?

The P-1 form is aligned with IRS regulations, specifically 26 U.S.C. §6724 and Treasury Regulation 301.6109-1(c). These regulations outline the requirements for obtaining taxpayer identification numbers and the process for filing an affidavit when such numbers are unavailable. By following these guidelines, payors can ensure compliance with IRS rules.

Is there a deadline for submitting the P-1 form?

While there is no specific deadline for submitting the P-1 form, it is advisable to file it as soon as the payee declines to provide their identifying number. Timely submission helps demonstrate that the payor acted promptly in seeking the necessary information and strengthens their case for reasonable cause when dealing with potential penalties.

Can the P-1 form be used for multiple payees?

The P-1 form is typically completed for each individual payee who has declined to provide their identifying number. Each payor should file a separate P-1 form for each payee to ensure accurate documentation and compliance with IRS requirements. This practice helps maintain clear records for each case.

Where should the completed P-1 form be submitted?

The completed P-1 form should be included with the transmittal documents sent to the Internal Revenue Service (IRS). It is essential to ensure that the form is properly signed and dated by both the payor and the payee to validate the information contained within. Keeping a copy for your records is also recommended.

Failing to include the employer identification number. This is crucial for identifying the payor.

Not providing the employee/payee's full name. Ensure both first name and last name are clearly stated.

Writing “None” or “Declined” in the social security number field without proper context. Specify if the payee declined to provide the number.

Omitting the home address of the employee/payee. This information is necessary for accurate record-keeping.

Neglecting to sign and date the form. Both the employer/payor and employee/payee must provide their signatures.

Using an incorrect format for the address. Ensure it includes the street number, city, state, and ZIP code.

Not stating the reason for the affidavit clearly. The purpose of the form must be evident to avoid confusion.

Failing to keep a copy of the completed form. Retaining a record is important for future reference.

Ignoring the specific instructions provided in the form. Each section has guidelines that must be followed.

Submitting the form without reviewing it for errors or omissions. Double-checking can prevent unnecessary delays.

When dealing with the P-1 form, several other documents may also be necessary to ensure compliance and proper record-keeping. Each of these forms serves a specific purpose and can help clarify the situation surrounding the request for an identifying number. Here’s a brief overview of these related documents.

Understanding these forms can simplify the process of handling tax-related matters. Each document plays a role in ensuring compliance and protecting both the payor and payee from potential penalties. Keeping them organized and accessible can help facilitate smoother transactions and reporting.

The P-1 form serves a specific purpose in the realm of tax compliance, particularly concerning the identification of payees. Several other documents share similarities with the P-1 form, each serving its own unique function while addressing similar issues of identification and compliance. Here’s a list of those documents:

Each of these forms plays a crucial role in the tax compliance process, ensuring that accurate information is exchanged between payors and payees. Understanding their similarities can help clarify the importance of proper identification in various tax-related situations.

When filling out the P-1 form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here are some dos and don’ts:

Understanding the P-1 form is crucial for both payors and payees. However, several misconceptions can lead to confusion. Here are nine common misunderstandings about the P-1 form:

Being aware of these misconceptions can help ensure that both payors and payees navigate the process with clarity and understanding.

Here are key takeaways about filling out and using the P 1 form: