In the realm of real estate transactions, an innovative approach that garners substantial interest is the Owner Financing Contract. This method of financing opens doors for buyers who might otherwise find the traditional mortgage landscape daunting or inaccessible, and provides sellers with an alternative sales strategy that can expedite the transaction process. At its core, the contract serves as a bridge between parties, enabling a purchase through direct financing from the seller to the buyer, circumventing conventional bank lending. Key components include outlining the payment schedule, interest rates, and terms of the agreement, each meticulously crafted to safeguard both the seller's investment and the buyer's rights to eventual ownership. Moreover, it introduces unique considerations such as the handling of default scenarios, property maintenance responsibilities, and the transfer of title, requiring a careful balance between flexibility and security. Navigating through this method demands a clear understanding of its complexities, potential risks, and benefits to ensure a successful, mutually beneficial arrangement.

Owner Financing Contract Template

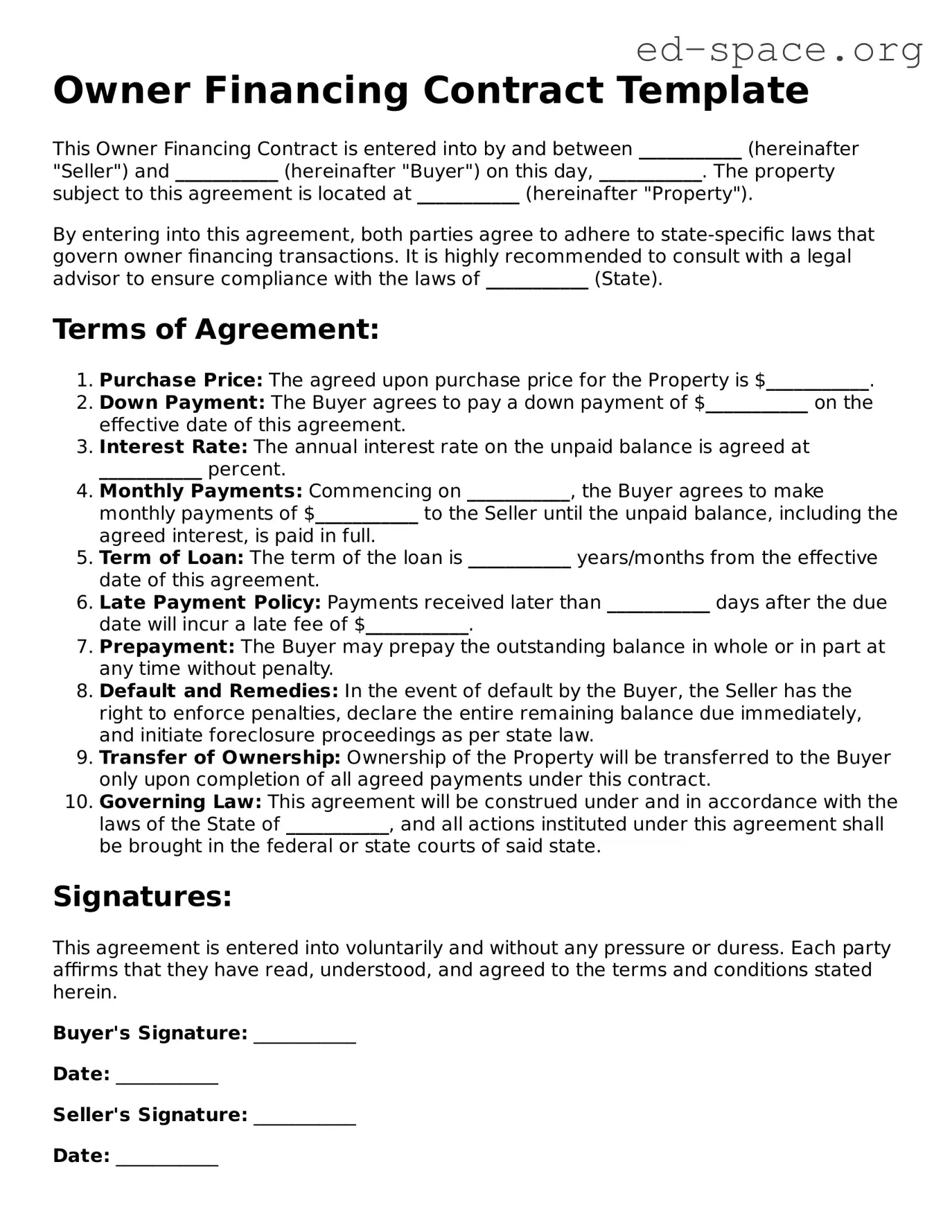

This Owner Financing Contract is entered into by and between ___________ (hereinafter "Seller") and ___________ (hereinafter "Buyer") on this day, ___________. The property subject to this agreement is located at ___________ (hereinafter "Property").

By entering into this agreement, both parties agree to adhere to state-specific laws that govern owner financing transactions. It is highly recommended to consult with a legal advisor to ensure compliance with the laws of ___________ (State).

Terms of Agreement:

Signatures:

This agreement is entered into voluntarily and without any pressure or duress. Each party affirms that they have read, understood, and agreed to the terms and conditions stated herein.

Buyer's Signature: ___________

Date: ___________

Seller's Signature: ___________

Date: ___________

| Fact | Description |

|---|---|

| Definition | An Owner Financing Contract is a legal document that outlines the terms under which the seller of a property provides financing to the buyer, allowing the buyer to purchase the property without obtaining a mortgage from a bank. |

| Key Components | The contract typically includes details such as the purchase price, interest rate, repayment schedule, consequences of default, and any balloon payments required. |

| Advantages for Buyers | Buyers may find these contracts appealing as they often require less stringent credit checks and potentially lower closing costs. |

| Advantages for Sellers | Sellers may benefit from owner financing by selling their property faster and possibly at a higher price, while also earning interest on the loan provided to the buyer. |

| Governing Laws | The terms and enforceability of Owner Financing Contracts are subject to state-specific real estate laws and financing regulations. |

| Risks for Buyers | Buyers should be cautious of high interest rates, unfavorable terms due to less regulation, and the possibility of losing their investment if they default on the contract. |

| Risks for Sellers | Sellers take on the risk that the buyer may default, leaving them to deal with foreclosure proceedings or the hassle of reselling the property. |

| Necessity of Legal Advice | Both parties are strongly advised to seek legal advice before entering into an Owner Financing Contract to ensure the agreement is fair and complies with all applicable laws. |

Once you've decided to take the path of owner financing for the sale or purchase of property, the Owner Financing Contract becomes a pivotal document in the process. This form outlines the agreement between the buyer and the seller where the seller provides the financing for the purchase of the property. Completing this form accurately is crucial as it details the loan terms, payment schedules, and rights and responsibilities of both parties. Below are the steps you'll need to follow to ensure the form is filled out thoroughly and correctly.

With all the necessary information in place and the form duly filled out and signed, the completed Owner Financing Contract solidifies the agreement, providing a legal framework that protects both parties' interests throughout the financing period. It's advisable for both the buyer and the seller to keep a copy of the contract for their records and to refer back to it as needed during the duration of the loan term.

What is an Owner Financing Contract?

An Owner Financing Contract is a legally binding agreement where the seller of a property provides the financing to the buyer for the purchase. This type of contract eliminates the need for the buyer to obtain financing through a traditional lender, such as a bank. Instead, the buyer makes payments directly to the seller under the terms agreed upon in the contract.

How does owner financing benefit the buyer?

Owner financing can offer several benefits to the buyer, including easier qualification for financing, potentially lower closing costs, and the ability to negotiate the down payment, interest rate, and repayment schedule directly with the seller. This can be particularly beneficial for buyers who may not qualify for traditional financing due to credit issues or self-employment.

What are the advantages for sellers offering owner financing?

Sellers offering owner financing can benefit from a wider pool of potential buyers, potentially quicker sale of the property, and the ability to earn interest on the financed amount. It also allows sellers to spread out the tax liability on any capital gains from the sale over the term of the loan.

What should be included in an Owner Financing Contract?

An Owner Financing Contract should clearly spell out the terms of the sale, including the purchase price, down payment, interest rate, repayment schedule, and any other conditions related to the financing. It should also include details of the property being sold, information about both the buyer and seller, and any default remedies available to the seller if the buyer fails to make payments.

Are there any risks associated with owner financing?

Yes, there are risks for both the buyer and the seller. Buyers risk losing their investment if they default on the loan and the property goes into foreclosure. Sellers face the risk of the buyer defaulting on the loan, which could result in the need to initiate foreclosure proceedings to regain possession of the property. Sellers may also have to deal with the hassle and expense of managing the loan.

Can interest rates for an Owner Financing Contract be negotiated?

Yes, one of the key benefits of owner financing is that the interest rate can be negotiated directly between the buyer and seller. This provides flexibility and can be adjusted based on the agreed terms, such as the down payment amount and the duration of the loan.

How is an Owner Financing Contract enforced?

Like any contract, an Owner Financing Contract is enforced through the legal system. If either party fails to meet their obligations under the contract, the other party may pursue legal remedies. For instance, if the buyer fails to make payments, the seller may seek foreclosure on the property to recover their investment.

Can either party change the terms of the Owner Financing Contract after it's signed?

Once an Owner Financing Contract is signed, the terms of the contract are typically binding on both parties. However, the contract terms can be modified if both the buyer and seller agree to the changes in writing.

What happens if the buyer wants to sell the property before paying off the Owner Financing Contract?

If the buyer wants to sell the property before the loan is paid in full, they generally need to pay off the remaining balance of the owner-financed loan at the time of sale. This can be accomplished through obtaining financing from another lender or through the sale proceeds. The specific rights and obligations would be outlined in the original Owner Financing Contract.

Is a down payment required in an Owner Financing Contract?

While it's common for a down payment to be required in an Owner Financing Contract, it's not always necessary. The amount of the down payment, if any, is one of the negotiable terms between the buyer and seller. Requiring a down payment can provide the seller with immediate cash and reduce the risk of default, but flexibility in this area can make the property more accessible to potential buyers.

When entering into an owner financing agreement, it's crucial to approach the process with caution and thoroughness. A well-drafted Owner Financing Contract can pave the way for a smooth and successful real estate transaction, benefiting both buyer and seller. However, individuals often encounter pitfalls that can lead to complications down the line. Here are five common mistakes made when filling out an Owner Financing Contract form:

Overlooking the Importance of a Legal Description of the Property: Many people simply use the street address or a brief description of the property. However, the legal description is a detailed way of identifying the land that must appear in the contract. It usually includes lot numbers, block numbers, and subdivision name, exactly as it appears in official records. The absence of a precise legal description can lead to misunderstandings and disputes about what land is actually being sold.

Not Specifying Repayment Terms Clearly: Repayment terms should be outlined in detail, including the amount, interest rate, term of the loan (how many years), and the payment schedule. Vague terms can result in disagreements and legal challenges. Explicitly stating whether the interest rate is fixed or adjustable, and under what circumstances the rate may change, is essential for preventing future conflicts.

Failing to Include Contingency Clauses: Contingency clauses offer protection to both parties, allowing them to back out under certain conditions without penalty. For instance, the buyer may want an inspection contingency that lets them terminate the contract if significant defects are found during the home inspection. Not including these clauses or failing to clearly define them may trap a party in an unfavorable situation.

Ignoring Local and State Laws: Each state has unique laws regarding real estate transactions, including owner financing. Not considering these laws when drafting your contract can lead to unenforceable terms and legal problems. It's paramount that the contract adheres to local regulations to ensure it's legally valid and binding.

Omitting Details about Default and Foreclosure Procedures: The contract must spell out what constitutes a default, the remedies available to the seller, and the foreclosure process if the buyer fails to meet their obligations. This section should be comprehensive, detailing any grace period before declaring a default and the steps that will be taken to foreclose. Neglecting to thoroughly define these terms can make the foreclosure process more complicated and prolonged than necessary.

Correctly filling out an Owner Financing Contract form requires close attention to detail and an understanding of the legal requirements. These mistakes can be avoided with careful planning, research, and, when necessary, consultation with a legal professional. This ensures that all parties' interests are protected and helps facilitate a smoother property transfer process.

When navigating the realm of owner financing, individuals find themselves engaging with a variety of documents beyond the Owner Financing Contract itself. Each document plays a crucial role in ensuring a transparent, legally sound, and smooth process for both the buyer and seller. The selection of documents provided below serves to guide, protect, and clarify the terms and expectations of all parties involved in the transaction.

Collectively, these documents solidify the foundation of an owner financing agreement. They ensure clarity, legality, and mutual understanding, paving the way for successful real estate transactions. Each document, with its specific function, works in concert with the Owner Financing Contract to protect the interests and rights of all parties involved. By familiarizing themselves with these key documents, buyers and sellers can navigate the owner financing process with confidence and security.

Promissory Note: This document is akin to the Owner Financing Contract in that it outlines the borrower's promise to repay a sum of money borrowed. In both cases, specific terms including interest rate, repayment schedule, and consequences of default are clearly defined, making the promissory note an integral part of seller-financed deals.

Mortgage Agreement: Similar to the Owner Financing Contract, a Mortgage Agreement secures the loan with the property being purchased. It grants the lender (in this case, the seller) a lien on the property as security for the repayment of the loan, allowing for foreclosure in the event of non-payment.

Land Contract: Also known as a Contract for Deed, this document shares similarities with owner financing contracts by allowing the buyer to pay the seller over time for the property, with the deed transferring upon fulfillment of the contract. Both setups bypass traditional lenders but differ in title possession timing.

Deed of Trust: In certain states, a Deed of Trust is used instead of a Mortgage Agreement but serves a comparable purpose to the Owner Financing Contract. It involves a trustee, who holds the property's title until the loan is repaid, offering a layer of security to the transaction similar to a mortgage lien.

Installment Sale Agreement: This agreement is characterized by the payment of the purchase price over time in installments, which is a principal feature of owner-financed transactions. These agreements detail payment schedules, interest rates, and the consequences of default, aligning closely with Owner Financing Contracts.

Real Estate Purchase Agreement: While this document is broader, encompassing all terms of a real estate sale (not just financing), aspects of owner financing can be incorporated into it. It becomes similar to an Owner Financing Contract when it includes terms for seller-financing, effectively making it a comprehensive agreement covering sale and financing terms.

When dealing with an Owner Financing Contract form, paying attention to detail is crucial. These contracts can pave the path to homeownership without traditional lending, but they come with their own set of rules to follow. Here are some essential dos and don'ts to ensure the process is handled correctly and efficiently.

When it comes to owner financing in the purchase of real estate, there are several misconceptions that both buyers and sellers may have. Understanding these can help in making informed decisions about engaging in such agreements.

This is not accurate. While it's true that owner financing can be a viable option for buyers who may not qualify for traditional bank loans, it is also a strategic choice for individuals who want to avoid the complexities and delays of bank financing.

Both parties can benefit from owner financing, and the contract's terms can be negotiated to ensure a fair deal. It's essential that both the buyer and the seller review the agreement with a legal professional before finalizing.

Having a legal professional involved is crucial. They can ensure that the contract is comprehensive, meets all legal requirements, and protects both parties' interests.

Foreclosure laws apply to owner-financed sales just as they do to traditional sales. The seller must follow legal procedures for repossession, which vary from state to state.

Interest rates in owner financing agreements are entirely negotiable and can be higher than those offered by banks, as they also reflect the seller's risk.

Owner financing can be used for the sale of various types of real estate, not just residential homes but also commercial properties and land.

Both buyers and sellers can enjoy tax benefits from owner financing. Sellers may spread their capital gains tax over the period of the loan, while buyers can deduct mortgage interest in some scenarios.

While potentially less complex, these contracts still involve significant legal and financial considerations. Understanding the terms and obligations is necessary to avoid future disputes.

Down payments are often part of owner financing agreements to protect the seller's interests and to give the buyer a stake in the property.

The term of an owner financing contract can vary widely, from a few years to several decades, depending on what both parties agree upon.

When engaging with an Owner Financing Contract form, there are several key considerations that both buyers and sellers should bear in mind. This arrangement, where the seller finances the purchase directly with the buyer, offers unique opportunities and challenges that require careful navigation. Below are key takeaways to ensure that all parties involved can approach these contracts with informed caution and understanding.

By paying close attention to these considerations, individuals who are either offering or accepting owner financing can better protect their interests, ensuring a more secure and equitable arrangement for both parties. As always, consultation with a legal expert is recommended to navigate the complexities of these contracts.

Terminate Real Estate Agent Contract Letter - Provides a clear, legal resolution for ending a property sale, preventing misunderstandings.