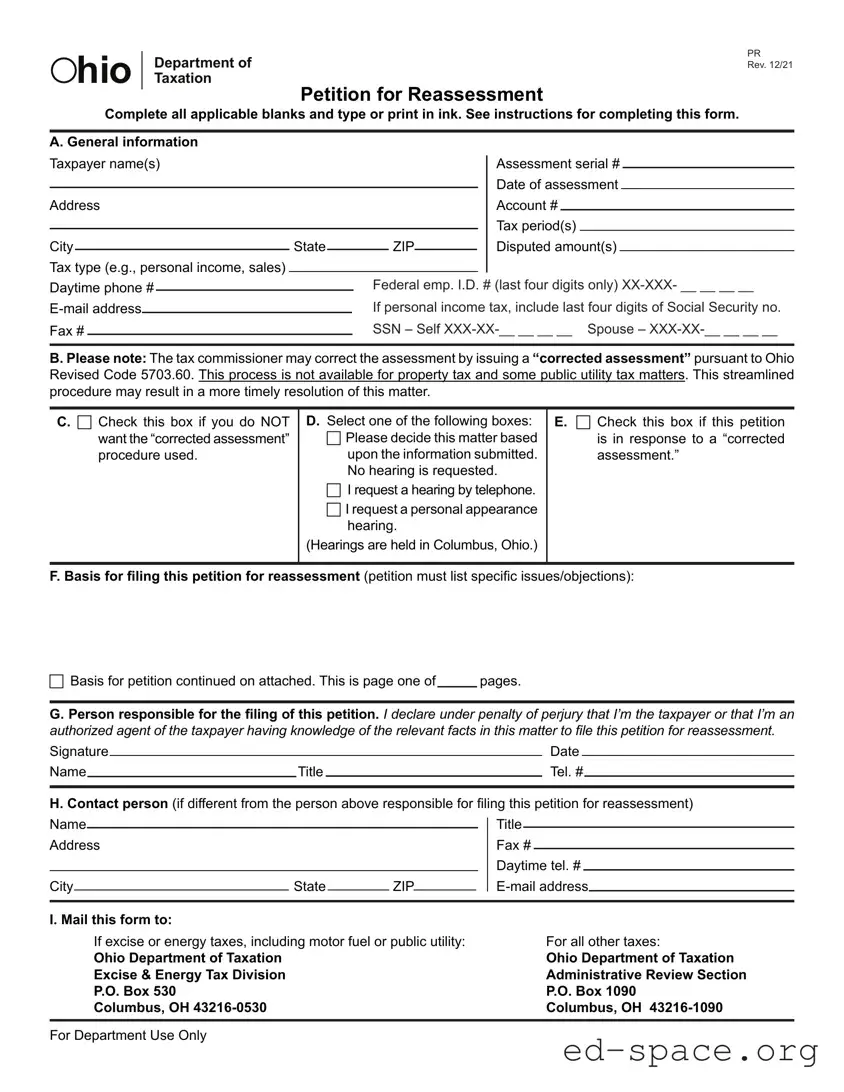

The Ohio Petition For Reassessment form serves as a critical tool for taxpayers seeking to contest a tax assessment issued by the Ohio Department of Taxation. This form requires individuals to provide essential information such as their name, address, and details about the disputed tax assessment, including the type of tax, assessment serial number, and the specific amount being contested. The process allows taxpayers to either request a corrected assessment or opt for a hearing, either by telephone or in person, to present their case. It is important to note that the opportunity for a corrected assessment is not available for property taxes or certain public utility taxes. Taxpayers must also declare their authority to file the petition, either as the taxpayer themselves or as an authorized agent. The form includes sections for the basis of the petition, where individuals can outline their objections to the assessment, and it emphasizes the importance of filing within a specific timeframe—generally within 60 days from the date of the assessment. Clear instructions guide users through the completion process, ensuring that all necessary information is submitted accurately to facilitate a timely resolution of the dispute.

| Fact Name | Details |

|---|---|

| Form Title | Ohio Department of Taxation Petition for Reassessment |

| Form Revision Date | Revised December 2021 |

| Filing Deadline | Must be filed no later than 60 days from the date on the assessment. |

| Governing Law | Ohio Revised Code 5703.60 |

| Corrected Assessment | This process allows the Tax Commissioner to issue a corrected assessment in response to a filed petition. |

| Hearing Options | Taxpayers can request a hearing by telephone or a personal appearance hearing. |

| Disputed Amount | Only the portion of the assessment being protested needs to be listed. |

| Signature Requirement | The person filing the petition must declare under penalty of perjury that they are authorized to do so. |

| Mailing Addresses | Different addresses are designated for excise taxes and all other taxes. |

After completing the Ohio Petition for Reassessment form, the next step is to submit it to the appropriate department. Make sure to follow the instructions carefully to ensure your petition is processed without delay.

What is the Ohio Petition for Reassessment form?

The Ohio Petition for Reassessment form is a document that taxpayers can use to contest an assessment made by the Ohio Department of Taxation. This form allows individuals or businesses to formally request a review of their tax assessment, providing an opportunity to dispute the amount owed based on specific grounds. It is essential for ensuring that taxpayers have a voice in the assessment process.

Who should file a Petition for Reassessment?

Any taxpayer who disagrees with an assessment from the Ohio Department of Taxation should consider filing this petition. This includes individuals and businesses facing assessments on personal income, sales tax, and other tax types. If you believe that the assessment is incorrect, this form is your avenue to seek a correction.

What information do I need to complete the form?

To fill out the Petition for Reassessment, you will need several pieces of information. This includes your name, address, the type of tax being assessed, the assessment serial number, the date of the assessment, the tax period in question, and the disputed amount. You should also provide your contact information, including a daytime phone number and email address, to facilitate communication.

What is a "corrected assessment"?

A corrected assessment is a response issued by the Tax Commissioner after a petition for reassessment has been filed. This streamlined process allows for a quicker resolution of the issue without the need for a lengthy review. However, it’s important to note that only a final determination can be appealed to the Board of Tax Appeals or Ohio courts.

Can I request a hearing when filing this petition?

Yes, you can request a hearing when filing your petition. There are options for a hearing by telephone or a personal appearance hearing in Columbus, Ohio. If you choose to have a hearing, it provides an opportunity for you or your representative to present your case and discuss the issues directly with the tax officials.

What happens if I disagree with the corrected assessment?

If you receive a corrected assessment and disagree with it, you can file a new petition for reassessment. This allows you to contest the adjusted amount. However, be aware that failing to file this new petition after receiving a corrected assessment will nullify your original petition, and the corrected assessment will become final.

How long do I have to file a Petition for Reassessment?

You must file the Petition for Reassessment within 60 days from the date of the assessment notice. This timeline is crucial, as missing this deadline could prevent you from contesting the assessment. Make sure to keep track of the assessment date to ensure timely filing.

Do I need to pay the disputed amount before filing the petition?

In most cases, you do not need to pay the disputed amount before filing the petition. However, there are exceptions, particularly when only penalties or interest are being contested in certain tax types. It’s wise to review your specific situation to understand any payment obligations before proceeding.

Where do I send the completed form?

The completed Petition for Reassessment form must be mailed to the appropriate address based on the type of tax you are contesting. For excise or energy taxes, send it to the Excise & Energy Tax Division. For all other taxes, mail it to the Administrative Review Section. If you're unsure, use the address for “all other taxes.” Hand delivery is also an option at the designated office in Columbus.

Leaving Blanks Unfilled: Many people forget to fill out all applicable sections of the form. Each blank is important for the processing of your petition.

Incorrect Tax Type: Selecting the wrong tax type can lead to delays. Ensure that you accurately identify the type of tax you are disputing, whether it's personal income or sales tax.

Missing Assessment Serial Number: This number is crucial. Failing to include it can result in your petition being rejected or delayed.

Not Providing Contact Information: Without a daytime phone number or email address, the tax department may struggle to reach you for clarifications or updates.

Ignoring the Deadline: Submitting your petition more than 60 days after the assessment date can lead to automatic rejection. Be mindful of the timeline!

Failure to Specify Disputed Amount: Clearly stating the amount you are disputing is essential. Vague statements can weaken your case.

Not Checking the Correct Boxes: Always double-check that you’ve selected the appropriate options for hearings or reassessment procedures. Missteps here can lead to misunderstandings.

Missing Signatures: The petition must be signed by the taxpayer or an authorized agent. An unsigned petition is invalid.

Inadequate Basis for Filing: Providing vague or insufficient reasons for your reassessment request can hinder your chances of success. Be specific!

Incorrect Mailing Address: Ensure that you send the petition to the correct address. Different taxes require different mailing locations, and mistakes can lead to significant delays.

The Ohio Petition for Reassessment form is an important document for taxpayers wishing to challenge an assessment made by the Ohio Department of Taxation. When filing this petition, several other forms and documents may also be required to support the case. Below is a list of commonly used forms and documents that may accompany the petition.

These forms and documents play a vital role in the reassessment process. They help ensure that the taxpayer's case is thoroughly presented and can significantly influence the outcome of the petition. Properly compiling and submitting these materials can facilitate a more efficient review by the Ohio Department of Taxation.

When filling out the Ohio Petition For Reassessment form, it is important to follow specific guidelines to ensure your petition is processed smoothly. Below is a list of things to do and avoid during this process.

By adhering to these guidelines, you can enhance the likelihood of a favorable outcome for your reassessment petition.

This is not entirely accurate. While the form can be used for various taxes, certain taxes like property tax and some public utility taxes have specific restrictions and may not qualify for the reassessment process.

This is misleading. If a corrected assessment is issued, there will be no hearing, even if one was initially requested. The process may be more streamlined, but it does not include a hearing in such cases.

This is not true for all situations. Generally, you do not need to pay the disputed amount before filing, except in specific circumstances like when only penalties or interest are being contested in certain tax types.

This is incorrect. A corrected assessment cannot be appealed. If you disagree with it, you must file a new petition for reassessment, which will then lead to a final determination that can be appealed.

This is a common misunderstanding. You actually have up to 60 days from the date on the assessment to file the petition, allowing for a bit more time to prepare your case.

While you can submit various types of documentation, it’s essential to be specific about your objections. The form allows for additional pages, but clarity and relevance are key to a successful petition.

This is not the case. You can have any authorized representative file the petition on your behalf, not just an attorney or accountant. However, you must complete the necessary authorization form.

This is misleading. Different taxes require you to mail the petition to specific addresses. If you're unsure, it's best to use the address for "all other taxes" to ensure proper handling.

When filling out the Ohio Petition for Reassessment form, consider the following key takeaways:

Following these guidelines will help facilitate a smoother process when filing your petition for reassessment in Ohio.