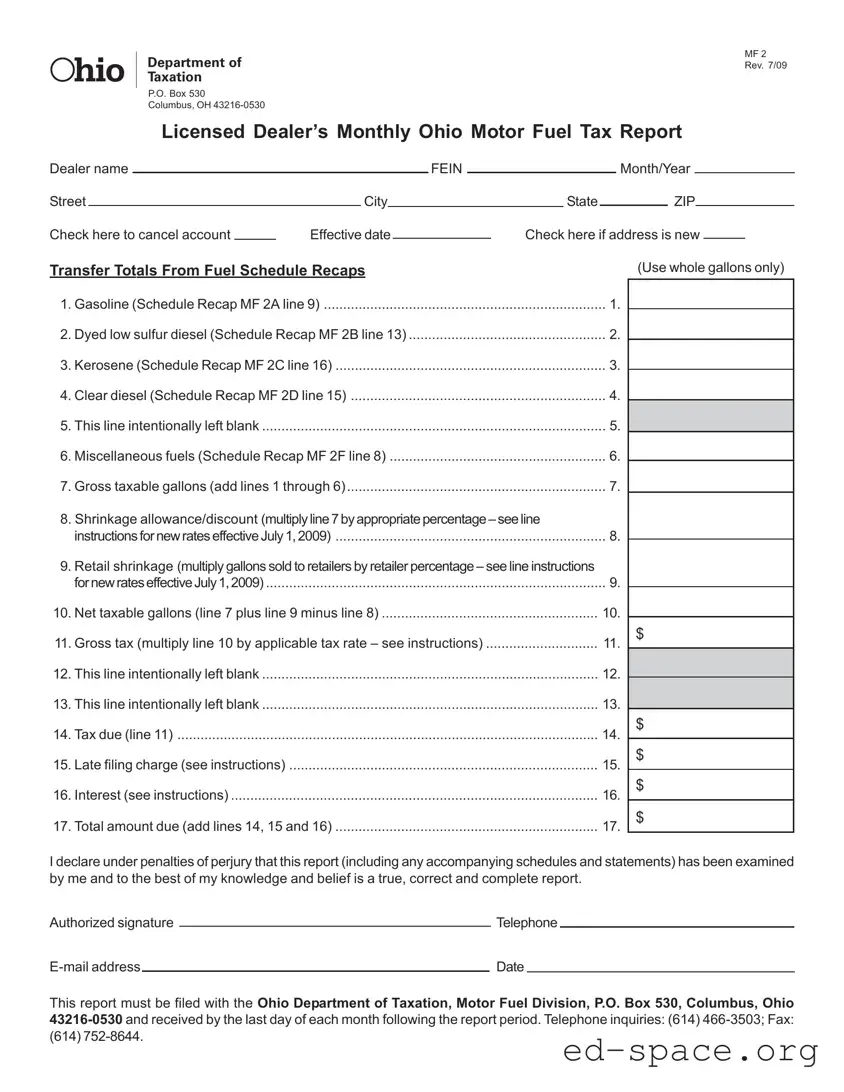

The Ohio MF 2 form is an essential document for licensed dealers involved in the sale of motor fuels within the state. This monthly report serves as a comprehensive record of the dealer's fuel sales, detailing various types of fuels including gasoline, dyed low sulfur diesel, kerosene, clear diesel, and miscellaneous fuels. Each dealer must accurately report their gross taxable gallons, accounting for allowances such as shrinkage and retail shrinkage, which are calculated based on specific percentages that vary by reporting period. The form also requires dealers to calculate the total tax due, which is based on the net taxable gallons multiplied by the applicable tax rate. Timely submission is crucial; the form must reach the Ohio Department of Taxation by the last day of each month following the reporting period. Failure to comply can result in late fees and interest charges, emphasizing the importance of understanding the nuances of the form. Additionally, the MF 2 form includes sections for authorized signatures and contact information, ensuring accountability and transparency in the reporting process.

| Fact Name | Details |

|---|---|

| Form Purpose | The Ohio MF 2 form is used for reporting the monthly motor fuel tax by licensed dealers. |

| Filing Requirement | Dealers must file the form by the last day of each month following the reporting period. |

| Governing Law | The form is governed by Ohio Revised Code Section 5735.06(C). |

| Tax Calculation | Tax due is calculated by multiplying net taxable gallons by the applicable tax rate. |

| Shrinkage Allowance | Shrinkage allowance is based on taxable gallons and varies by reporting period. |

| Retail Shrinkage | Retail shrinkage must be added back for gallons sold to retail dealers, excluding those under the same FEIN. |

| Late Filing Charge | A late filing charge applies if the form is not submitted by the due date, calculated as 10% of the liability or $50, whichever is greater. |

| Interest Accrual | Interest is charged from the due date until payment is received, with rates determined annually. |

| Contact Information | Inquiries can be directed to the Ohio Department of Taxation at (614) 466-3503. |

| Form Revision Date | The current version of the form was revised in July 2009. |

Filling out the Ohio MF 2 form is essential for licensed dealers to report their monthly motor fuel tax. Once completed, this form must be submitted to the Ohio Department of Taxation by the end of each month following the reporting period.

What is the Ohio MF 2 form?

The Ohio MF 2 form is a monthly report that licensed dealers must file to report their motor fuel tax obligations. It includes details about the types and amounts of fuel sold, as well as the taxes owed. This form is essential for compliance with state tax regulations regarding motor fuel sales in Ohio.

Who needs to file the Ohio MF 2 form?

Any licensed dealer who sells motor fuel in Ohio is required to file the MF 2 form. This includes businesses that sell gasoline, diesel, kerosene, and other fuels. If you are a dealer operating under a Federal Employer Identification Number (FEIN), you must submit this report monthly to the Ohio Department of Taxation.

When is the Ohio MF 2 form due?

The Ohio MF 2 form must be filed by the last day of each month following the reporting period. For example, the report for January is due by the end of February. Timely filing is crucial to avoid penalties and interest on unpaid taxes.

What happens if I miss the filing deadline?

If the Ohio MF 2 form is not filed by the due date, a late filing charge will be applied. This charge is either 10% of the tax liability or a flat fee of $50, whichever is greater. Additionally, interest will accrue on the unpaid tax amount from the due date until payment is received.

What is the shrinkage allowance mentioned in the form?

The shrinkage allowance accounts for the loss of fuel due to evaporation, spillage, or other factors during storage and distribution. If the report is filed on time, dealers can claim a percentage of the taxable gallons sold as a shrinkage allowance. The percentage varies depending on the reporting period, so it’s important to check the current rates.

Can I change my address or cancel my account using the Ohio MF 2 form?

Yes, the Ohio MF 2 form provides options to indicate a change of address or to cancel your account. Simply check the appropriate box on the form and provide the effective date for the change. This ensures that the Ohio Department of Taxation has your correct information for future correspondence.

How is the tax calculated on the Ohio MF 2 form?

The tax is calculated by multiplying the net taxable gallons (calculated on the form) by the applicable tax rate. The tax rate can change, so it’s essential to refer to the latest instructions for the correct rate based on the reporting period. Once calculated, this amount is reported on line 11 of the form.

Where do I send the completed Ohio MF 2 form?

After completing the Ohio MF 2 form, it should be sent to the Ohio Department of Taxation, Motor Fuel Division, at P.O. Box 530, Columbus, Ohio 43216-0530. Ensure it is mailed in time to meet the filing deadline to avoid penalties.

Incorrect or Missing Information: Failing to provide complete details such as the dealer name, FEIN, or address can lead to delays. Ensure all sections are filled out accurately.

Improper Calculation of Taxable Gallons: Mistakes in adding the gallons from the various schedules can result in incorrect totals. Double-check calculations to avoid errors.

Not Using the Correct Shrinkage Percentage: Each reporting period has a specific shrinkage percentage. Using the wrong percentage can affect the tax due. Be sure to reference the correct rates for your reporting period.

Late Submission: Failing to file the form by the deadline may incur late fees and interest. Submit the form on time to avoid these additional charges.

The Ohio MF 2 form is an essential document for licensed dealers reporting their monthly motor fuel tax. To ensure compliance and accurate reporting, several other forms and documents may be needed alongside the MF 2. Below is a list of these documents, along with brief descriptions of each.

Having these forms and documents ready can streamline the reporting process and help avoid potential issues with the Ohio Department of Taxation. Proper preparation ensures compliance and can save time and resources in the long run.

The Ohio MF 2 form is a key document for licensed dealers reporting motor fuel tax. Several other forms share similarities with it, primarily in their purpose and structure. Here’s a list of seven documents that are comparable to the Ohio MF 2 form:

When completing the Ohio MF 2 form, it is important to ensure accuracy and compliance. Here are six key do's and don'ts to guide you through the process.

Following these guidelines will help ensure a smooth filing process. Take the time to review your submission carefully before sending it to the Ohio Department of Taxation.

Understanding the Ohio MF 2 form is essential for licensed dealers in the state. However, several misconceptions can lead to confusion. Here are eight common misunderstandings about this important tax report:

In reality, this form covers multiple fuel types, including dyed low sulfur diesel, kerosene, clear diesel, and miscellaneous fuels. Dealers must report all applicable fuel sales to ensure compliance.

The shrinkage allowance is only available if the report is filed and paid on time. Late submissions disqualify dealers from this benefit, emphasizing the importance of timely compliance.

Dealers must use specific percentages based on the reporting period. These percentages change over time, and it’s crucial to refer to the correct rates for accurate calculations.

Retail shrinkage must be reported and calculated based on gallons sold to retail dealers. This ensures that all fuel sales are accurately accounted for in the tax report.

The tax rate for motor fuel changes periodically. Dealers should verify the current rate for the applicable reporting period to avoid errors in their calculations.

Late filing can lead to significant penalties, including a charge of 10% of the liability or a minimum of $50. Ignoring these charges can result in increased financial burdens.

The interest rate for late payments can vary from year to year. Dealers should check the Ohio Department of Taxation's website for the most current rates to ensure accurate calculations.

The Ohio MF 2 form must be filed by the last day of each month following the report period. Late submissions can incur penalties and affect the dealer's standing with the tax authorities.

By clearing up these misconceptions, licensed dealers can better navigate the requirements of the Ohio MF 2 form and ensure compliance with state regulations.