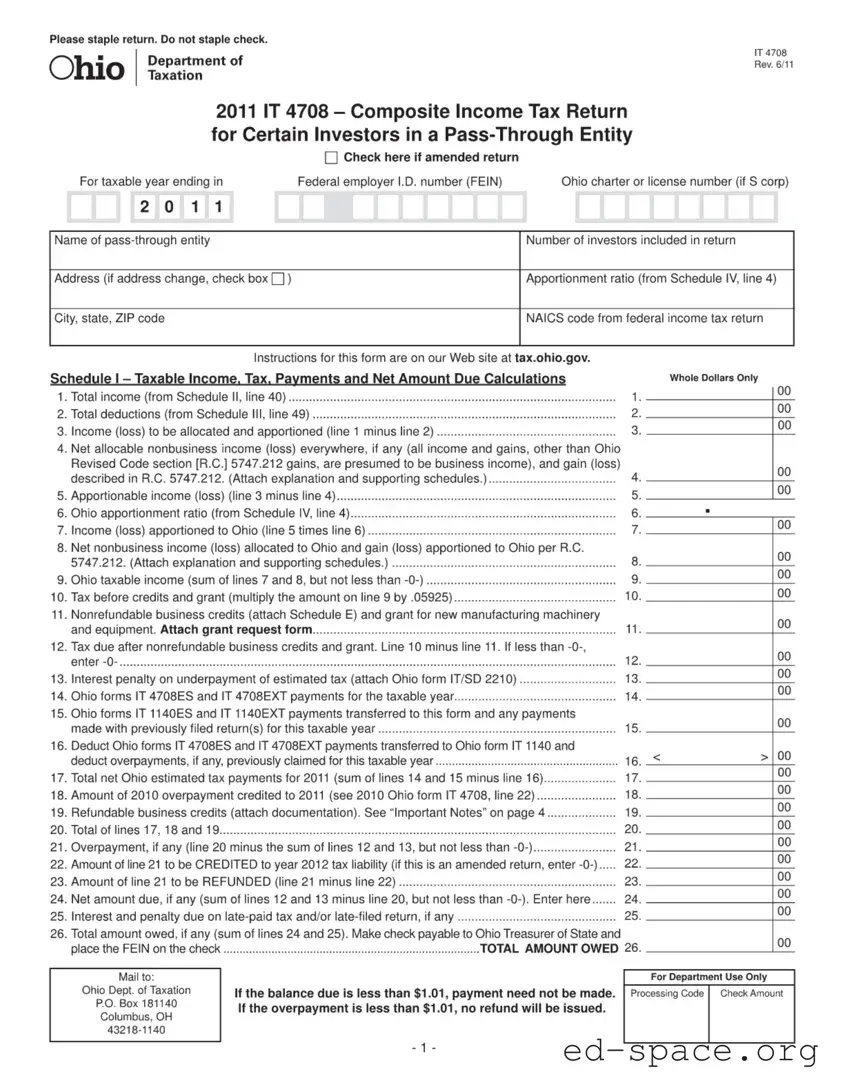

The Ohio IT 4708 form serves as a composite income tax return specifically designed for certain investors involved in a pass-through entity. This form is essential for those who need to report their share of income, deductions, and credits derived from their investments in partnerships or S corporations. It includes key sections such as the identification of the pass-through entity, the total income and deductions, and the calculation of Ohio taxable income. Investors will find that the form requires detailed information, including the apportionment ratio and the NAICS code from the federal income tax return. Additionally, it provides a structured way to report nonbusiness income and calculate any tax due after considering applicable credits. For those filing an amended return, there is a specific checkbox to indicate this change. The form also emphasizes the importance of attaching supporting schedules and documentation, ensuring compliance with Ohio tax regulations. Instructions for completing the form can be accessed online, making it easier for investors to navigate the filing process.

| Fact Name | Details |

|---|---|

| Form Purpose | The IT 4708 form is used for filing a composite income tax return for certain investors in a pass-through entity in Ohio. |

| Governing Law | The form is governed by the Ohio Revised Code, specifically R.C. 5747.212. |

| Tax Year | The IT 4708 form is applicable for the taxable year ending in 2011. |

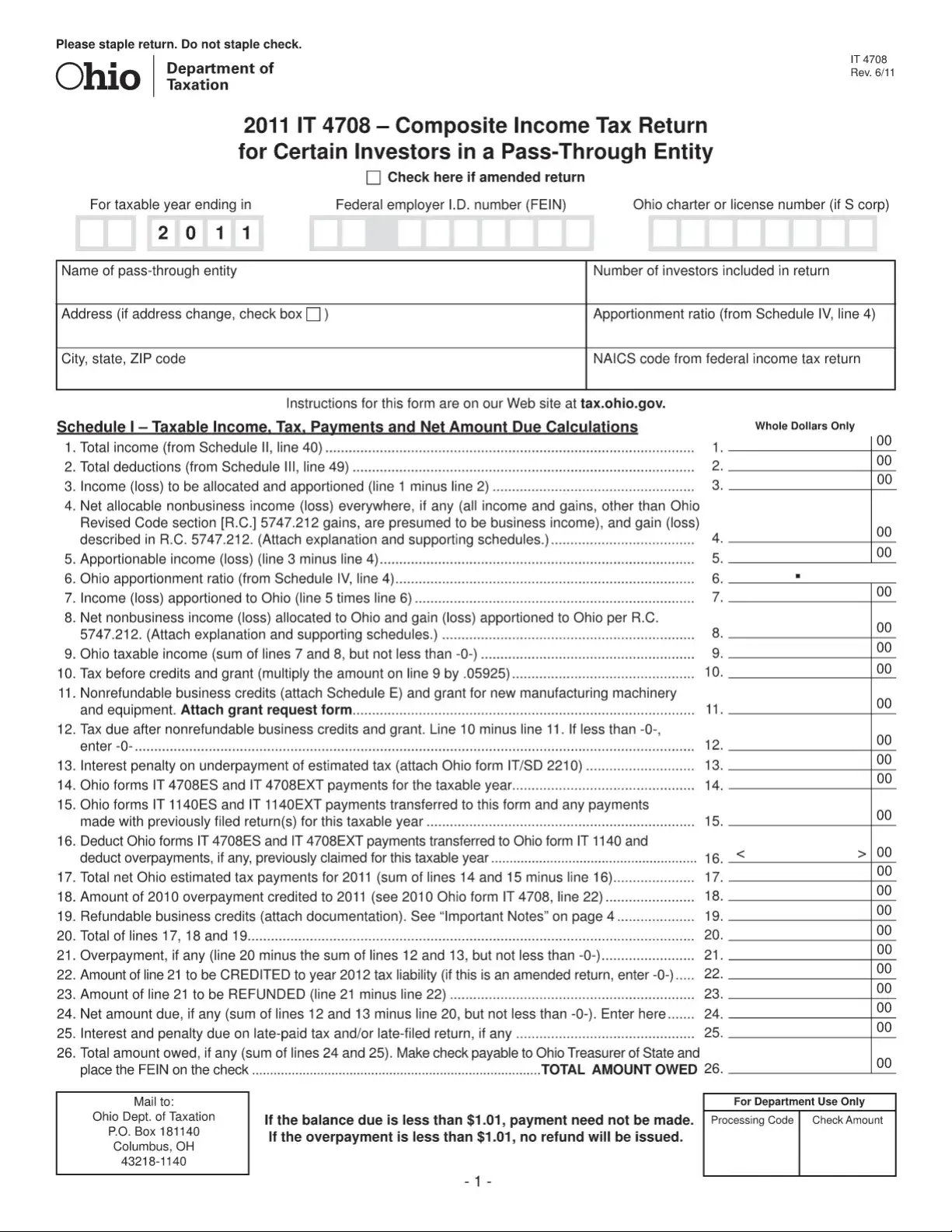

| Filing Requirements | All investors participating in the return must be included, and a copy of IRS forms 1120S or 1065 must be attached. |

| Amended Returns | Check the box provided if the return is an amended return to indicate changes. |

| Payment Instructions | Tax payments should be made payable to the Ohio Treasurer of State, and the FEIN must be included on the check. |

| Nonbusiness Income | Net nonbusiness income allocated to Ohio must be calculated and reported as per R.C. 5747.212. |

| Interest Penalties | Interest penalties may apply for underpayment of estimated tax, requiring the attachment of Ohio form IT/SD 2210. |

| Refunds and Credits | Refundable business credits must be documented, and overpayments can be credited to future tax liabilities. |

Filling out the Ohio IT 4708 form is essential for reporting income from a pass-through entity. This process requires careful attention to detail to ensure accuracy. After completing the form, you will need to submit it along with any necessary attachments and payments, if applicable.

What is the Ohio IT 4708 form?

The Ohio IT 4708 form is a Composite Income Tax Return designed for certain investors in a pass-through entity. This form allows multiple investors to file their taxes collectively, simplifying the process for those who are part of a partnership, S corporation, or limited liability company (LLC). It is specifically for tax years ending in 2011 and is used to report income, deductions, and tax liability.

Who needs to file the IT 4708 form?

What information is required to complete the IT 4708 form?

To fill out the IT 4708 form, you will need details about the pass-through entity, such as its name, address, and federal employer identification number (FEIN). Additionally, you will need information about your income, deductions, and any business credits you may qualify for. It is also important to provide the number of investors included in the return and the apportionment ratio.

How do I calculate my taxable income on the IT 4708 form?

To calculate your taxable income, you start with your total income from the pass-through entity. From there, you subtract total deductions to find your income (or loss) that needs to be allocated and apportioned. This figure is then adjusted for any nonbusiness income or losses to arrive at your Ohio taxable income. Make sure to follow the specific lines on the form for accurate calculations.

What should I do if I need to amend my return?

If you need to amend your return, check the box indicating that this is an amended return on the form. You will also need to provide the corrected information and any necessary explanations. It’s important to ensure that all changes are clearly documented to avoid confusion during processing.

Are there penalties for late filing or underpayment?

Yes, there can be penalties for late filing or underpayment of taxes. If you submit your IT 4708 form after the deadline, you may incur interest and penalties on any tax due. It’s best to file on time and pay any owed taxes to avoid these additional costs.

Where do I send my completed IT 4708 form?

Your completed IT 4708 form should be mailed to the Ohio Department of Taxation at P.O. Box 181140, Columbus, OH 43218-1140. Make sure to staple your return, but do not staple your check if you are making a payment. Always double-check that you have included all necessary documentation and signatures.

Can I claim business credits on the IT 4708 form?

Yes, you can claim nonrefundable business credits on the IT 4708 form. You will need to attach Schedule E, which outlines the credits you are claiming. Be sure to provide any required documentation to support your claims. This can help reduce your overall tax liability.

Incorrect Entity Name: Failing to accurately enter the name of the pass-through entity can lead to processing delays or rejections.

Missing Federal Employer Identification Number: Omitting the FEIN can result in the form being deemed incomplete, causing potential penalties.

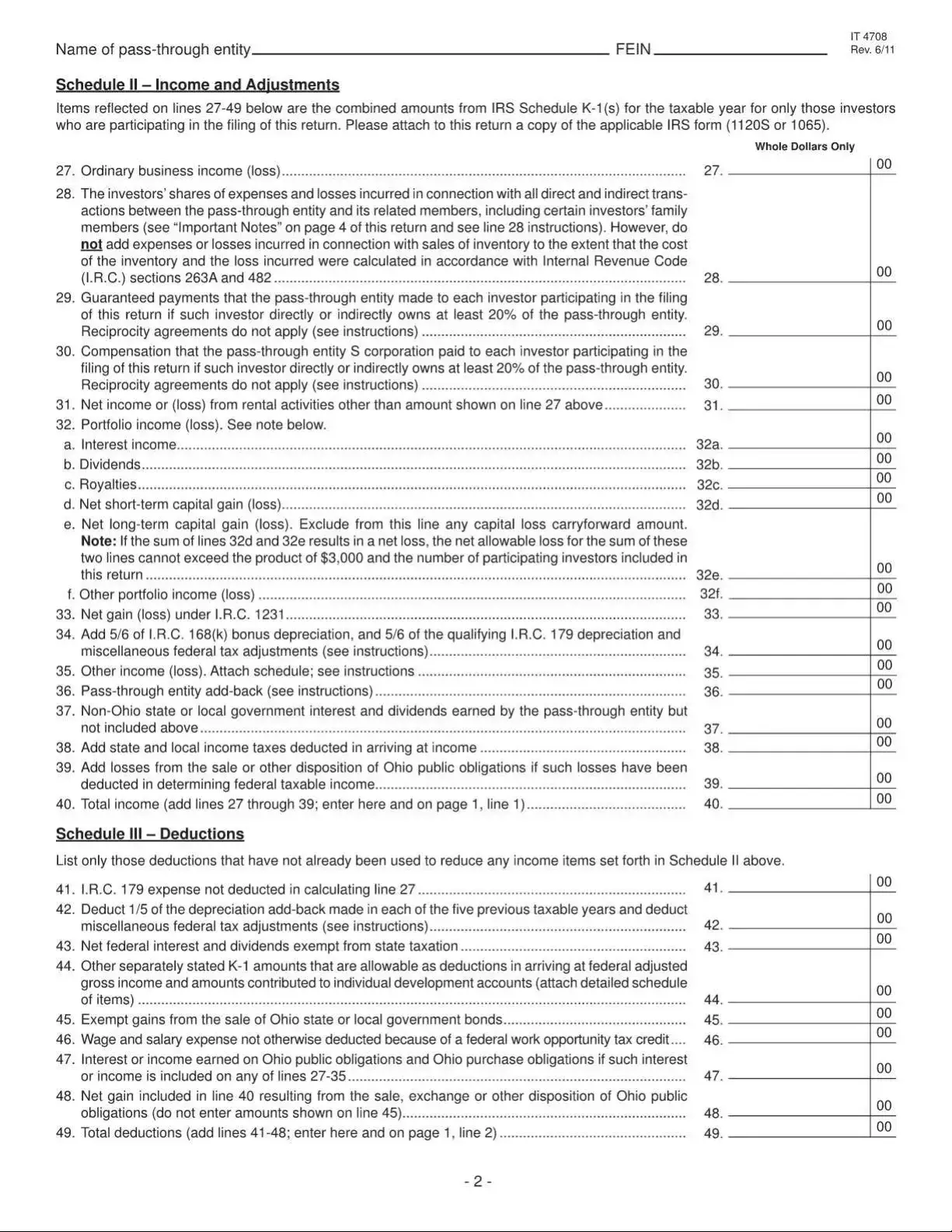

Improper Calculation of Apportionment Ratio: Errors in calculating the apportionment ratio can affect the overall tax liability.

Not Attaching Required Schedules: Failing to include necessary supporting schedules or documentation can result in the return being rejected.

Inaccurate Income Reporting: Misreporting total income or deductions can lead to incorrect tax calculations and potential audits.

Neglecting to Check for Amended Returns: If the return is amended, the appropriate box must be checked to avoid confusion.

Improper Payment Instructions: Not following the payment instructions, such as stapling the check incorrectly, can delay processing.

Failure to Review for Accuracy: Not double-checking all entries for accuracy can lead to simple mistakes that may have significant consequences.

The Ohio IT 4708 form is a composite income tax return for certain investors in a pass-through entity. When filing this form, there are several other documents and forms that may be required. Each of these documents serves a specific purpose in the tax filing process, helping to ensure that all necessary information is submitted accurately and completely. Below is a list of common forms and documents often used alongside the IT 4708.

Understanding these forms and documents can simplify the filing process and help ensure compliance with Ohio tax laws. By preparing all necessary documentation, investors can avoid delays and potential penalties related to their tax returns.

The Ohio IT 4708 form is a composite income tax return specifically designed for certain investors in a pass-through entity. Several other tax documents serve similar purposes, each catering to different aspects of income reporting and tax obligations. Below are five documents that share similarities with the Ohio IT 4708 form:

Understanding these documents can help clarify the responsibilities and reporting requirements for individuals involved with pass-through entities. Each form plays a critical role in ensuring compliance with tax obligations while providing necessary information for accurate income reporting.

When filling out the Ohio IT 4708 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are seven key do's and don'ts to keep in mind:

By adhering to these guidelines, you can help ensure that your submission is processed smoothly and efficiently.

Understanding the Ohio IT 4708 form is crucial for investors involved in pass-through entities. However, several misconceptions can lead to confusion. Here are six common misconceptions:

This form is specifically designed for certain investors in pass-through entities, which can include small businesses and partnerships, not just large corporations.

Filing is required only if there is income to report. If there is no income or loss, you may not need to file the form.

This form serves a specific purpose for pass-through entities and is different from standard individual income tax returns.

It is important to note that the form should be stapled, but the check must not be stapled to it. This helps ensure proper processing.

Supporting documents, such as copies of IRS Schedule K-1 forms, are necessary to complete the filing process accurately.

Amended returns can be filed using the IT 4708 form if corrections are needed. Check the appropriate box to indicate that it is an amended return.

Filling out the Ohio IT 4708 form can be a straightforward process if you keep a few key points in mind. This form is specifically designed for certain investors in a pass-through entity and is essential for reporting income and calculating tax obligations. Here are some important takeaways to consider:

By following these guidelines, you can navigate the Ohio IT 4708 form with greater confidence and accuracy, ensuring compliance with state tax requirements.