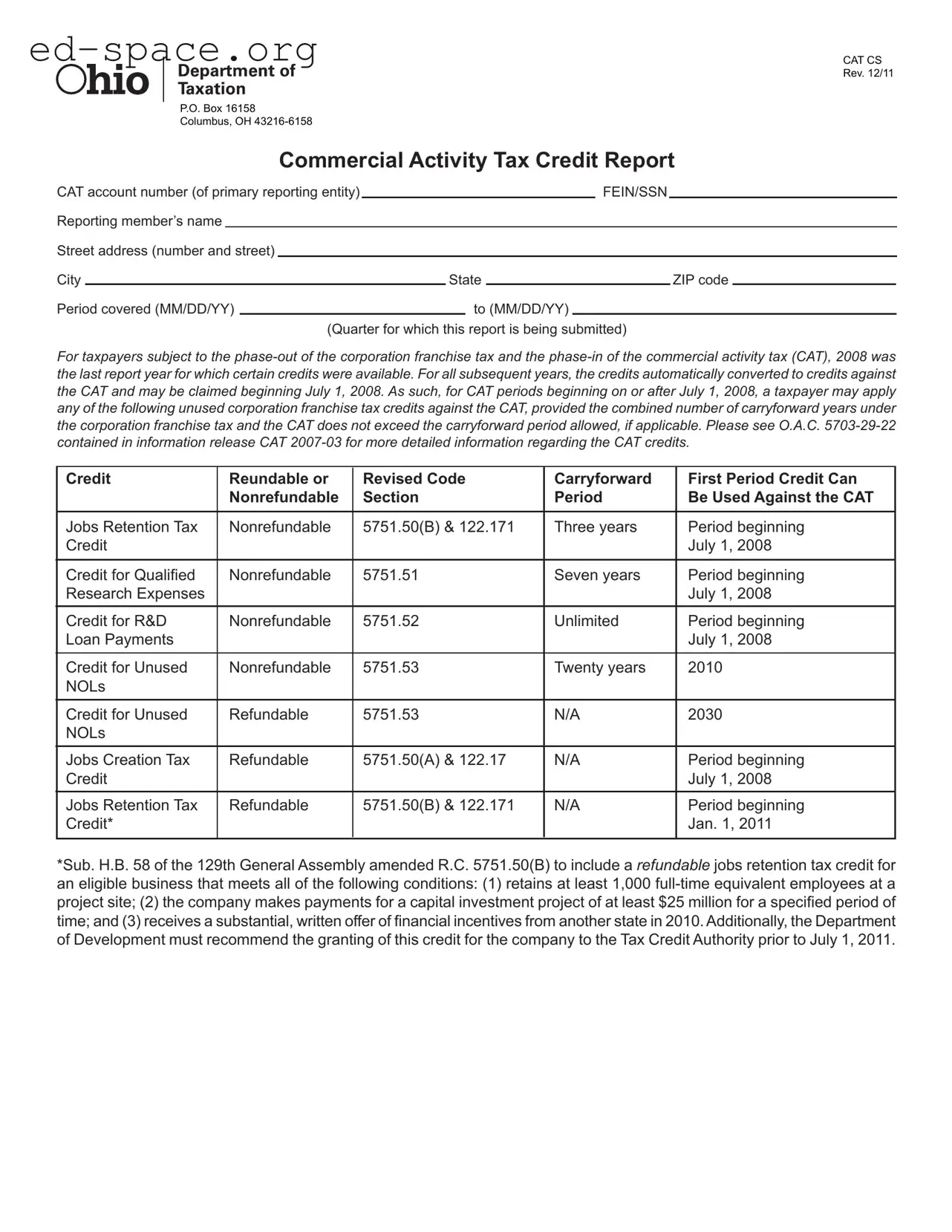

The Ohio Cat Cs form serves as a vital tool for businesses navigating the complexities of the Commercial Activity Tax (CAT) system. This form is specifically designed for taxpayers who are transitioning from the corporation franchise tax to the CAT, particularly those who have unused tax credits from previous years. Since the phase-out of the corporation franchise tax began, businesses have been able to convert certain credits into applicable offsets against their CAT liabilities starting July 1, 2008. The form requires essential information, including the CAT account number, the Federal Employer Identification Number (FEIN) or Social Security Number (SSN), and the reporting member's details, such as name and address. Additionally, it outlines various tax credits available for claims, including the Jobs Retention Tax Credit, the Qualified Research Expenses Credit, and the Research and Development Loan Payments Credit, each with specific eligibility criteria and carryforward provisions. The form also necessitates the declaration of credits claimed during the reporting period, ensuring that businesses maintain accurate records for compliance. Understanding the nuances of the Ohio Cat Cs form is crucial for any business looking to optimize its tax position while adhering to state regulations.

CAT CS

Rev. 12/11

P.O. Box 16158

Columbus, OH

Commercial Activity Tax Credit Report

CAT account number (of primary reporting entity) |

|

|

|

|

|

FEIN/SSN |

|

|

|

||||

Reporting member’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) |

|

|

|

|

|

|

|

|

|

|

|||

City |

|

|

|

State |

|

|

|

ZIP code |

|

||||

Period covered (MM/DD/YY) |

|

|

|

to (MM/DD/YY) |

|

|

|

|

|||||

|

|

|

|

(Quarter for which this report is being submitted) |

|

|

|

||||||

For taxpayers subject to the

Credit |

Reundable or |

Revised Code |

Carryforward |

First Period Credit Can |

|

Nonrefundable |

Section |

Period |

Be Used Against the CAT |

|

|

|

|

|

Jobs Retention Tax |

Nonrefundable |

5751.50(B) & 122.171 |

Three years |

Period beginning |

Credit |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for Qualifi ed |

Nonrefundable |

5751.51 |

Seven years |

Period beginning |

Research Expenses |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for R&D |

Nonrefundable |

5751.52 |

Unlimited |

Period beginning |

Loan Payments |

|

|

|

July 1, 2008 |

|

|

|

|

|

Credit for Unused |

Nonrefundable |

5751.53 |

Twenty years |

2010 |

NOLs |

|

|

|

|

|

|

|

|

|

Credit for Unused |

Refundable |

5751.53 |

N/A |

2030 |

NOLs |

|

|

|

|

|

|

|

|

|

Jobs Creation Tax |

Refundable |

5751.50(A) & 122.17 |

N/A |

Period beginning |

Credit |

|

|

|

July 1, 2008 |

|

|

|

|

|

Jobs Retention Tax |

Refundable |

5751.50(B) & 122.171 |

N/A |

Period beginning |

Credit* |

|

|

|

Jan. 1, 2011 |

|

|

|

|

|

*Sub. H.B. 58 of the 129th General Assembly amended R.C. 5751.50(B) to include a refundable jobs retention tax credit for an eligible business that meets all of the following conditions: (1) retains at least 1,000

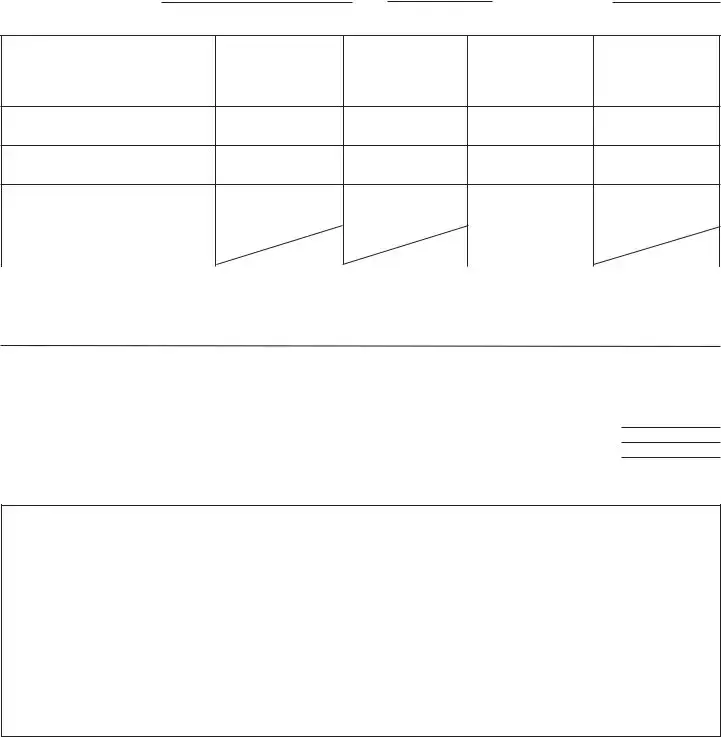

Credit Schedule

(If credits are being claimed by members of a consolidated elected or combined taxpayer group, a separate schedule is required for each entity that is claiming a credit.)

The CAT account number of the entity entitled to the credit may be different than that of the primary reporting entity.

Entity entitled to credit: NameFEINCAT account number

Nonrefundable Credits

A |

B |

C |

D |

|

|

|

|

|

|

Opening Unused |

Credit Earned |

Credits Claimed |

Closing Unused |

|

During Current |

During Current |

|||

Credit Balance |

Credit Balance |

|||

Reporting Period |

Reporting Period |

|||

|

|

1.Jobs retention credit+

2.Qualifi ed research expense credit

3.Research and development loan repayment credit+

4. Total |

|

* |

|

|

|

|

|

|

|

|

|

*Combine with credits being claimed by other entities in group (if any) and carry this forward to line 7 on your CAT return.

+Must attach credit certifi cate received from the Department of Development

Refundable Credits

Must attach credit certifi cate received from the Department of Development

Jobs creation credit |

1. |

Jobs retention credit |

2. |

Total of lines 1 and 2 to be carried forward to line 11 of CAT return |

3. |

Declaration and signature (an offi cer or managing agent of the corporation must sign this declaration)

I declare under penalties of perjury that this report (including any |

use any of its money or property for or in aid of or opposition to |

accompanying schedule or statement) has been examined by |

a political party, a candidate for election or nomination to public |

me and to the best of my knowledge and belief is a true, correct |

office, or a political action committee, legislation campaign fund, |

and complete return and report, and that this corporation has not, |

or organization that supports or opposes any such candidate or |

during the preceding year, except as permitted by Ohio Revised |

in any manner used any of its money for any partisan political |

Code sections 3517.082, 3599.03 and 3599.031, directly or |

purpose whatsoever, or for reimbursement or indemnification of |

indirectly paid, used or offered, consented, or agreed to pay or |

any person for money or property so used. |

|

|

|

|

|

|

||

Date (MM/DD/YY) |

Signature of offi cer or managing agent |

Title |

|||||

|

|||||||

|

|

|

|

|

|

|

|

Contact telephone no. |

|

|

|

|

|||

| Fact Name | Details |

|---|---|

| Form Purpose | The Ohio CAT Cs form is used to report Commercial Activity Tax credits. |

| Governing Laws | The form is governed by Ohio Revised Code sections 5751.50, 5751.51, 5751.52, and 5751.53. |

| Last Reporting Year | 2008 was the last year for which certain credits under the corporation franchise tax were available. |

| Credit Conversion | Credits automatically converted to CAT credits starting July 1, 2008. |

| Carryforward Rules | Unused corporation franchise tax credits can be applied against the CAT, subject to carryforward limitations. |

| Jobs Retention Credit | This nonrefundable credit can be claimed for a period of three years, beginning July 1, 2008. |

| Research Expense Credit | The qualified research expenses credit is nonrefundable and can be claimed for seven years starting July 1, 2008. |

| Loan Payment Credit | The research and development loan payment credit is nonrefundable and has an unlimited carryforward period. |

| Jobs Creation Credit | This refundable credit is available for claims starting July 1, 2008, and has no specified carryforward limit. |

| Declaration Requirement | An officer or managing agent must sign the declaration under penalties of perjury, affirming the accuracy of the report. |

Filling out the Ohio CAT Cs form is a straightforward process, but it’s important to complete each section carefully. Ensure that you have all necessary information at hand before you begin. Once you have filled out the form, you will submit it to the appropriate state department for processing.

What is the Ohio CAT Cs form?

The Ohio CAT Cs form, or Commercial Activity Tax Credit Report, is a document that businesses in Ohio use to report and claim various tax credits associated with the Commercial Activity Tax (CAT). This form is particularly important for businesses that have transitioned from the corporation franchise tax to the CAT, as it allows them to carry forward unused credits from the previous tax system. The form includes sections for listing credits, providing business information, and declaring the accuracy of the report.

Who needs to file the Ohio CAT Cs form?

What types of credits can be claimed using the Ohio CAT Cs form?

What should I do if I need assistance with the Ohio CAT Cs form?

Failing to include the CAT account number of the primary reporting entity. This number is essential for proper identification.

Not providing the correct FEIN or SSN. Ensure that the number matches the entity's tax records.

Omitting the reporting member’s name. This must be clearly stated to avoid confusion.

Incorrectly filling out the address fields. Double-check the street address, city, state, and ZIP code for accuracy.

Neglecting to specify the period covered by the report. This should be clearly stated in MM/DD/YY format.

Claiming credits without attaching the credit certificate received from the Department of Development. This is mandatory for certain credits.

Misunderstanding the carryforward rules for credits. Make sure you are aware of the limits for each credit type.

Failing to sign the declaration section. An officer or managing agent must sign for the report to be valid.

Not providing a contact telephone number or email. This information is vital for any follow-up or clarification.

Submitting the form without reviewing it for errors or omissions. A thorough review can prevent delays or rejections.

The Ohio Cat Cs form is a crucial document for businesses reporting their Commercial Activity Tax credits. Along with this form, several other documents are commonly used to ensure compliance and accurate reporting. Below is a list of these forms and documents, each serving a specific purpose in the tax reporting process.

Each of these documents plays a significant role in the tax reporting process for Ohio businesses. Properly completing and submitting these forms helps ensure compliance with state tax regulations and maximizes available tax credits.

The Ohio CAT Cs form is an important document for businesses that need to report their Commercial Activity Tax (CAT) credits. Several other documents share similarities with the CAT Cs form, primarily in their purpose of reporting tax credits or financial information. Here are six documents that resemble the Ohio CAT Cs form:

Understanding these similarities can help businesses navigate their tax reporting obligations more effectively. Each of these forms plays a crucial role in ensuring that taxpayers can accurately report their financial activities and take advantage of available credits.

When filling out the Ohio Cat Cs form, it’s important to approach the task with care. Here’s a helpful list of things you should and shouldn’t do to ensure a smooth process.

By following these guidelines, you can navigate the Ohio Cat Cs form with confidence. Taking the time to prepare properly will help you avoid common pitfalls and ensure your submission is processed smoothly.

This form is applicable to all businesses subject to the Commercial Activity Tax (CAT), regardless of size. Small businesses can also benefit from the available credits.

Taxpayers must actively claim the credits by completing the CAT Cs form. Failure to do so may result in the loss of potential benefits.

The CAT Cs form must be submitted quarterly, as it covers specific periods. Missing a quarterly submission could lead to penalties or loss of credits.

Unused credits can be carried forward to offset the CAT, as long as the combined carryforward period does not exceed the allowed limits.

Refundable credits are available, but specific eligibility criteria must be met. Businesses should review these criteria to determine their eligibility.

Multiple credits can be claimed simultaneously, provided that each is properly documented and meets the necessary requirements.

Supporting documentation, such as credit certificates, is essential for claiming credits. Failure to include these documents may result in denial of the credits.

Deadlines for submission are strict and must be adhered to. Late submissions can lead to penalties or loss of credits, making timely filing crucial.

When filling out and using the Ohio CAT Cs form, it is essential to understand several key aspects to ensure compliance and maximize potential benefits. Here are some important takeaways:

By following these guidelines, taxpayers can navigate the Ohio CAT Cs form more effectively and ensure they are taking full advantage of available credits.