The Notice of Right to Cure Auto Loan Letter is an important document for borrowers who have fallen behind on their auto loan payments. This letter serves as a formal notification that the borrower has been in default for at least ten days. It outlines the specifics of the loan in question, including the payment amount needed to remedy the default. Borrowers are informed that they have a right to cure the default within twenty days from the date of the notice. To do so, they must make the specified payment to the lender at the provided address. Additionally, the letter warns that failing to cure the default may lead to the cancellation of any credit insurance linked to the loan. If the borrower defaults again, the lender may not be required to send another notice. For any questions or clarifications, the letter encourages borrowers to reach out promptly. This form is approved by the Nebraska Department of Banking and Finance, ensuring it meets state regulations.

Notice of Right to Cure Loan Default

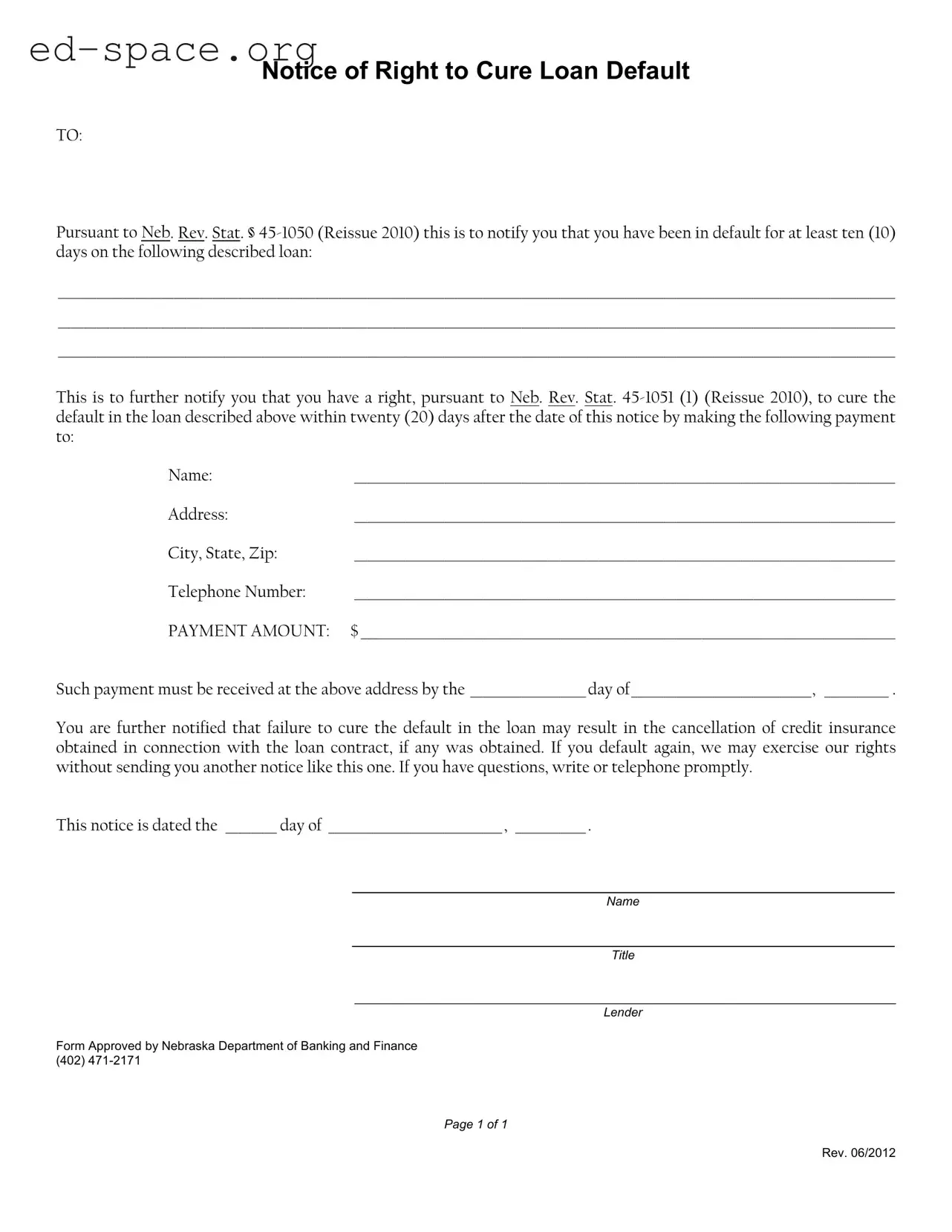

TO:

Pursuant to Neb. Rev. Stat. §

__________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________________

This is to further notify you that you have a right, pursuant to Neb. Rev. Stat.

Name: |

____________________________________________________________________________________ |

Address: |

____________________________________________________________________________________ |

City, State, Zip: |

____________________________________________________________________________________ |

Telephone Number: |

____________________________________________________________________________________ |

PAYMENT AMOUNT: |

$ ___________________________________________________________________________________ |

Such payment must be received at the above address by the __________________ day of____________________________, __________ .

You are further notified that failure to cure the default in the loan may result in the cancellation of credit insurance obtained in connection with the loan contract, if any was obtained. If you default again, we may exercise our rights without sending you another notice like this one. If you have questions, write or telephone promptly.

This notice is dated the ________ day of ___________________________, ___________ .

_________________________________________________________

Name

_________________________________________________________

Title

__________________________________________________________

Lender

Form Approved by Nebraska Department of Banking and Finance (402)

Page 1 of 1

Rev. 06/2012

| Fact Name | Details |

|---|---|

| Purpose | This letter notifies borrowers of their default status on an auto loan. |

| Governing Law | Based on Neb. Rev. Stat. § 45-1050 and § 45-1051 (Reissue 2010). |

| Default Period | A borrower must be in default for at least ten (10) days to receive this notice. |

| Cure Period | Borrowers have twenty (20) days to cure the default after receiving the notice. |

| Payment Requirement | Borrowers must make a specified payment to cure the default. |

| Consequences of Non-Cure | Failure to cure the default may lead to cancellation of credit insurance. |

| Subsequent Defaults | If a borrower defaults again, no further notice is required before action. |

| Contact Information | Borrowers are encouraged to contact the lender with any questions. |

After you have gathered all necessary information, filling out the Notice of Right to Cure Auto Loan Letter form is straightforward. This form serves as a formal notification regarding your auto loan status and your rights related to curing any defaults. Follow the steps below to complete the form correctly.

Once the form is filled out, it should be sent to the borrower. Make sure to keep a copy for your records. This ensures that both parties have documentation of the communication regarding the loan default.

What is the Notice of Right to Cure Auto Loan Letter?

The Notice of Right to Cure Auto Loan Letter is a formal notification sent to borrowers who have defaulted on their auto loan payments. It informs them of their right to remedy the default by making a specified payment within a certain timeframe.

How long do I have to cure the default?

You have twenty (20) days from the date of the notice to cure the default. This means you must make the required payment by the specified deadline to avoid further action.

What happens if I do not cure the default?

If you fail to cure the default within the given timeframe, the lender may take further action, which could include cancellation of any credit insurance associated with the loan. Additionally, the lender may pursue other remedies without sending another notice.

What information is included in the notice?

The notice includes details about the loan, such as the loan amount, the payment required to cure the default, and the deadline for making that payment. It also provides contact information for the lender.

What should I do if I receive this notice?

If you receive this notice, review it carefully. If you can make the payment to cure the default, do so by the deadline. If you have questions or need assistance, contact the lender using the information provided in the notice.

Can I cure the default after the deadline?

What if I have questions about the notice?

If you have questions about the notice or the loan, it is best to contact the lender directly. You can write or call using the contact information provided in the notice.

Is this notice required by law?

Yes, this notice is required under Nebraska law, specifically Neb. Rev. Stat. § 45-1050 and § 45-1051. It ensures that borrowers are informed of their rights and options when they are in default.

What is the significance of the payment amount listed in the notice?

The payment amount listed is the specific amount you need to pay to cure the default. It is crucial to make this payment in full and on time to restore your loan status and avoid further penalties.

Failing to include the loan details: It is crucial to provide accurate information about the loan, including the loan number and any relevant identifiers. Omitting this information can lead to confusion and delays.

Neglecting to specify the payment amount: The payment amount required to cure the default must be clearly stated. Without this, the recipient may not know how much to pay to rectify the situation.

Missing the deadline for payment: The form requires a specific date by which the payment must be received. Failing to highlight this date can result in the loss of the right to cure the default.

Incorrectly filling out the contact information: Providing inaccurate or incomplete contact details can hinder communication. Ensure that the name, address, and telephone number are correct and legible.

Overlooking the signature requirement: The notice must be signed by an authorized individual. An unsigned form may be deemed invalid, leading to further complications.

Failing to keep a copy of the notice: It is essential to retain a copy of the completed form for personal records. This serves as proof of the notice and the actions taken.

Ignoring the importance of timely communication: If there are questions or concerns, it is vital to reach out promptly. Delayed communication can exacerbate the situation and limit options.

The Notice of Right to Cure Auto Loan Letter is an important document that informs borrowers about their default status and their rights to remedy the situation. However, it is often accompanied by other forms and documents that help clarify the process and protect both the lender's and borrower's interests. Below is a list of additional documents that may be relevant in conjunction with this notice.

Understanding these documents can empower borrowers to navigate their financial challenges more effectively. Each piece plays a role in the overall process of managing a loan and addressing defaults. It’s essential to keep all communication clear and to seek assistance when needed.

The Notice of Right to Cure Auto Loan Letter form serves a specific purpose in notifying borrowers about their default status and their rights. Similar documents include:

When filling out the Notice Of Right To Cure Auto Loan Letter form, it’s important to follow some guidelines to ensure everything is completed correctly. Here’s a list of things you should and shouldn’t do:

By following these tips, you can help ensure that your form is completed properly and that you understand your rights regarding the loan default.

Misconceptions about the Notice of Right to Cure Auto Loan Letter can lead to confusion for borrowers. Here are six common misunderstandings:

Understanding these misconceptions can help borrowers navigate their options more effectively and take the necessary steps to address their loan situation.

When dealing with the Notice of Right to Cure Auto Loan Letter, it's important to understand its implications and your options. Here are some key takeaways to keep in mind: