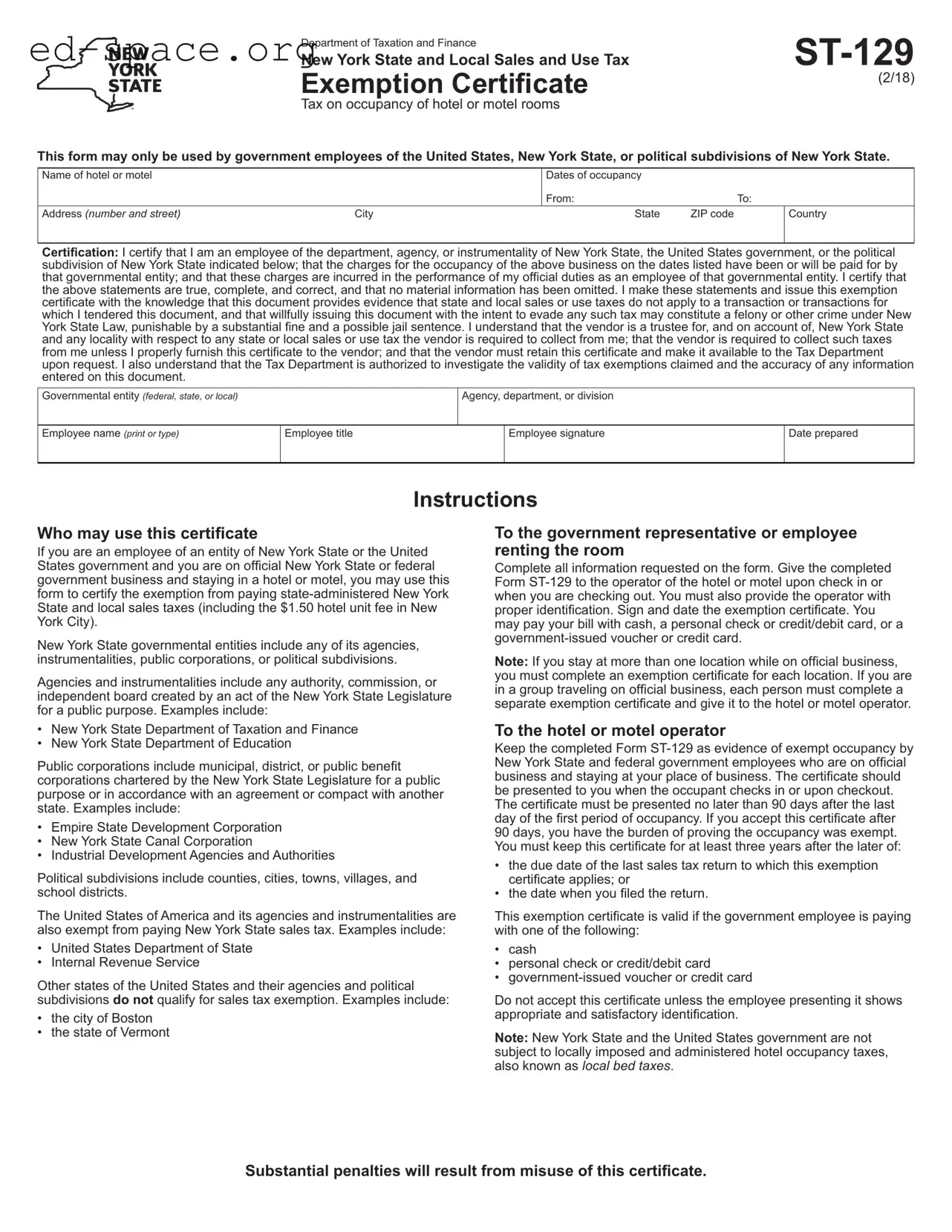

The New York Hotel Tax Exempt form, officially known as Form ST-129, serves as a vital tool for government employees traveling on official business. This form allows eligible individuals—specifically those employed by the United States, New York State, or its political subdivisions—to claim an exemption from state and local sales taxes on hotel accommodations. When filling out the form, users must provide essential information, including the name and address of the hotel, dates of occupancy, and the governmental entity they represent. Additionally, the employee must certify that their stay is for official duties and that the charges will be covered by their agency. The form not only protects the employee from incurring unnecessary tax expenses but also imposes strict requirements on both the employee and the hotel operator. For instance, hotel operators are required to retain the completed form for a minimum of three years and must ensure that it is presented within a specific timeframe. Misuse of this exemption can lead to significant penalties, emphasizing the importance of proper compliance. Understanding how to correctly utilize the New York Hotel Tax Exempt form can save government employees time and money while ensuring adherence to state regulations.

Department of Taxation and Finance |

|

New York State and Local Sales and Use Tax |

|

Exemption Certificate |

(2/18) |

|

Tax on occupancy of hotel or motel rooms

This form may only be used by government employees of the United States, New York State, or political subdivisions of New York State.

Name of hotel or motel |

|

Dates of occupancy |

|

|

|

|

|

|

|

|

From: |

|

|

|

To: |

|

|

Address (number and street) |

City |

|

State |

ZIP code |

|

|

Country |

|

|

|

|

|

|

|

|

|

|

Certification: I certify that I am an employee of the department, agency, or instrumentality of New York State, the United States government, or the political subdivision of New York State indicated below; that the charges for the occupancy of the above business on the dates listed have been or will be paid for by that governmental entity; and that these charges are incurred in the performance of my official duties as an employee of that governmental entity. I certify that the above statements are true, complete, and correct, and that no material information has been omitted. I make these statements and issue this exemption certificate with the knowledge that this document provides evidence that state and local sales or use taxes do not apply to a transaction or transactions for which I tendered this document, and that willfully issuing this document with the intent to evade any such tax may constitute a felony or other crime under New York State Law, punishable by a substantial fine and a possible jail sentence. I understand that the vendor is a trustee for, and on account of, New York State and any locality with respect to any state or local sales or use tax the vendor is required to collect from me; that the vendor is required to collect such taxes from me unless I properly furnish this certificate to the vendor; and that the vendor must retain this certificate and make it available to the Tax Department upon request. I also understand that the Tax Department is authorized to investigate the validity of tax exemptions claimed and the accuracy of any information entered on this document.

Governmental entity (federal, state, or local)

Agency, department, or division

Employee name (print or type)

Employee title

Employee signature

Date prepared

Instructions

Who may use this certificate

If you are an employee of an entity of New York State or the United States government and you are on official New York State or federal government business and staying in a hotel or motel, you may use this form to certify the exemption from paying

New York State governmental entities include any of its agencies, instrumentalities, public corporations, or political subdivisions.

Agencies and instrumentalities include any authority, commission, or independent board created by an act of the New York State Legislature for a public purpose. Examples include:

•New York State Department of Taxation and Finance

•New York State Department of Education

Public corporations include municipal, district, or public benefit corporations chartered by the New York State Legislature for a public purpose or in accordance with an agreement or compact with another state. Examples include:

•Empire State Development Corporation

•New York State Canal Corporation

•Industrial Development Agencies and Authorities

Political subdivisions include counties, cities, towns, villages, and school districts.

The United States of America and its agencies and instrumentalities are also exempt from paying New York State sales tax. Examples include:

•United States Department of State

•Internal Revenue Service

Other states of the United States and their agencies and political subdivisions do not qualify for sales tax exemption. Examples include:

•the city of Boston

•the state of Vermont

To the government representative or employee renting the room

Complete all information requested on the form. Give the completed Form

Note: If you stay at more than one location while on official business, you must complete an exemption certificate for each location. If you are in a group traveling on official business, each person must complete a separate exemption certificate and give it to the hotel or motel operator.

To the hotel or motel operator

Keep the completed Form

90 days, you have the burden of proving the occupancy was exempt. You must keep this certificate for at least three years after the later of:

•the due date of the last sales tax return to which this exemption certificate applies; or

•the date when you filed the return.

This exemption certificate is valid if the government employee is paying with one of the following:

•cash

•personal check or credit/debit card

•

Do not accept this certificate unless the employee presenting it shows appropriate and satisfactory identification.

Note: New York State and the United States government are not subject to locally imposed and administered hotel occupancy taxes, also known as local bed taxes.

Substantial penalties will result from misuse of this certificate.

| Fact Name | Details |

|---|---|

| Governing Law | This form is governed by New York State Tax Law and applicable federal regulations. |

| Eligible Users | Only government employees of the United States, New York State, or its political subdivisions may use this form. |

| Purpose | The form certifies exemption from state and local sales taxes on hotel or motel occupancy. |

| Form Identifier | The official name of the form is ST-129, New York State and Local Sales and Use Tax Exemption Certificate. |

| Submission Requirements | The completed form must be provided to the hotel or motel operator upon check-in or checkout. |

| Identification | Employees must present proper identification along with the completed exemption certificate. |

| Retention Period | Hotels and motels must retain the completed form for at least three years after the last sales tax return to which it applies. |

| Penalties for Misuse | Willful misuse of the exemption certificate may result in substantial fines or criminal charges under New York State Law. |

Completing the New York Hotel Tax Exempt form is a straightforward process for government employees on official business. This form allows you to certify that you are exempt from paying certain taxes while staying in a hotel or motel. After filling out the form, you will present it to the hotel operator along with proper identification.

What is the New York Hotel Tax Exempt form?

The New York Hotel Tax Exempt form, officially known as Form ST-129, is a certificate that allows employees of the United States government, New York State, or its political subdivisions to claim an exemption from state and local sales taxes when staying in hotels or motels for official business. This form must be completed and presented to the hotel operator at check-in or checkout to avoid tax charges on the occupancy of the room.

Who is eligible to use the New York Hotel Tax Exempt form?

Eligibility for the New York Hotel Tax Exempt form is limited to government employees. This includes employees of the United States government, New York State, and its political subdivisions. Examples of qualifying entities include state departments, public corporations, and local government agencies. Employees of other states or their subdivisions do not qualify for this exemption.

How should the New York Hotel Tax Exempt form be completed?

The form must be filled out completely by the government employee. Key information includes the name of the hotel, dates of occupancy, and details about the governmental entity and employee. The employee must sign and date the form, certifying that the charges will be paid by their governmental entity and that the stay is for official duties. Proper identification must also be provided to the hotel operator along with the completed form.

What happens if the form is not presented in a timely manner?

The completed Form ST-129 must be presented to the hotel operator no later than 90 days after the last day of the first period of occupancy. If the form is submitted after this period, the hotel operator may have difficulty proving that the occupancy was exempt from tax. This could lead to potential tax liabilities for the hotel.

How long should hotels keep the New York Hotel Tax Exempt form?

Hotels and motels are required to retain the completed Form ST-129 for at least three years. This retention period starts from the due date of the last sales tax return to which the exemption certificate applies or the date the return was filed, whichever is later. Keeping this documentation is essential for compliance with tax regulations.

Are there any penalties for misuse of the New York Hotel Tax Exempt form?

Yes, there are substantial penalties for the misuse of the New York Hotel Tax Exempt form. Willfully issuing the certificate with the intent to evade tax obligations may constitute a felony or other crime under New York State law. This can result in significant fines and possible jail time for the individual involved.

Incomplete Information: Many individuals fail to fill out all required fields on the form. Essential details such as the name of the hotel, dates of occupancy, and the governmental entity must be provided. Omitting any of these can lead to rejection of the exemption claim.

Incorrect Dates: Entering incorrect dates of occupancy is a common mistake. The form requires specific start and end dates for the stay. If these dates do not match the actual stay, the exemption may not be honored.

Failure to Sign: Not signing the exemption certificate is another frequent error. A signature is necessary to validate the form. Without it, the hotel or motel may not accept the exemption.

Improper Identification: Some employees neglect to provide proper identification when submitting the form. Hotels require that the employee present suitable identification along with the completed form to verify their status.

Use of the Form for Ineligible Entities: A significant mistake occurs when individuals from non-qualifying entities attempt to use the exemption form. Only government employees from the United States or New York State can use this certificate. Others, such as employees from different states, do not qualify.

Late Submission: Submitting the form after the 90-day deadline is a critical error. The hotel must receive the certificate no later than 90 days after the last day of occupancy. Late submissions may result in the hotel being unable to claim the exemption.

The New York Hotel Tax Exempt form, also known as Form ST-129, is essential for government employees to claim exemption from hotel occupancy taxes. Alongside this form, several other documents may be required to facilitate the tax exemption process. Below is a list of commonly used forms and documents that complement the New York Hotel Tax Exempt form.

Each of these documents plays a crucial role in ensuring compliance with tax exemption requirements. They help establish the legitimacy of the government employee's claim and ensure proper documentation is maintained for auditing purposes. It is important to gather all necessary forms before traveling to avoid complications during the hotel stay.

The New York Hotel Tax Exempt form, known as Form ST-129, shares similarities with various other tax exemption documents. Each of these forms serves a specific purpose and is designed to certify tax-exempt status for certain individuals or entities. Below is a list of ten documents that are similar to the New York Hotel Tax Exempt form:

Understanding these documents can help clarify the requirements for tax exemptions in various situations. Each form has its own specific use and requirements, but they all share a common goal of certifying tax-exempt status for eligible individuals or organizations.

When filling out the New York Hotel Tax Exempt form, it’s important to follow certain guidelines to ensure compliance and avoid issues. Here are six things you should and shouldn't do:

By following these guidelines, you can help ensure that your tax exemption process goes smoothly. Proper adherence to the rules not only protects you but also helps the hotel or motel operator comply with state regulations.

Misconception 1: Only federal government employees can use the ST-129 form.

This is not true. The ST-129 form can be used by employees of New York State, local government entities, and federal employees. Anyone on official government business can utilize this exemption.

Misconception 2: The form is valid for any hotel stay.

In reality, the ST-129 form is only applicable when the hotel stay is for official government business. Personal trips do not qualify for this exemption.

Misconception 3: You can submit the form after your stay.

This is a common misunderstanding. The ST-129 form must be presented to the hotel operator either at check-in or check-out. If you wait longer than 90 days after your stay, the exemption may not be valid.

Misconception 4: Any form of payment is acceptable when using the exemption.

While various payment methods are allowed, the ST-129 form must be accompanied by proper identification. It's crucial to ensure that the payment method is appropriate for the exemption.

Misconception 5: The hotel operator does not need to keep the ST-129 form.

This is incorrect. The hotel operator must retain the completed form for at least three years as evidence of exempt occupancy. This retention is essential for compliance with tax regulations.

Filling out and using the New York Hotel Tax Exempt form is straightforward, but there are important details to keep in mind. Here are some key takeaways:

By following these guidelines, you can ensure a smooth experience when using the tax exemption certificate. Understanding the process helps avoid potential issues and penalties.