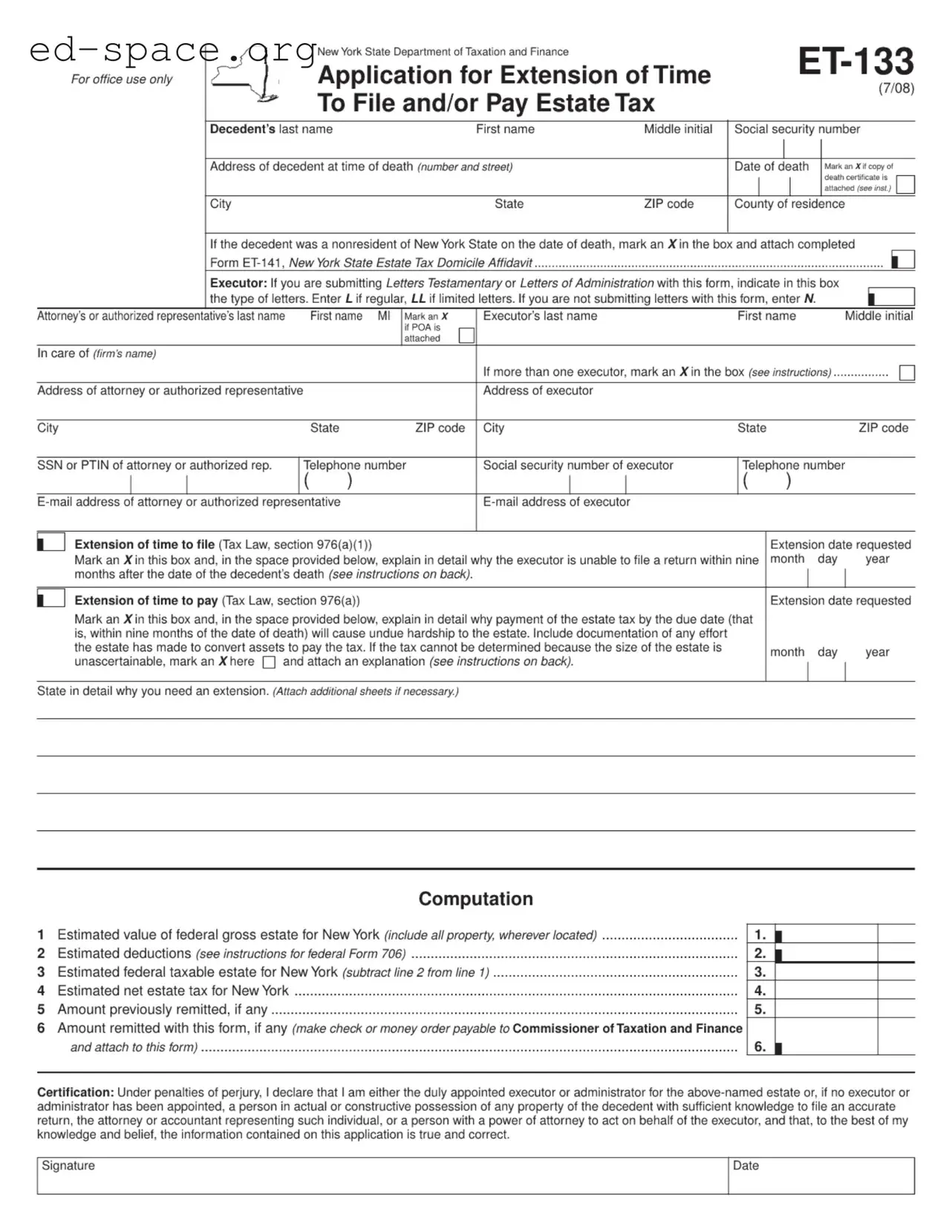

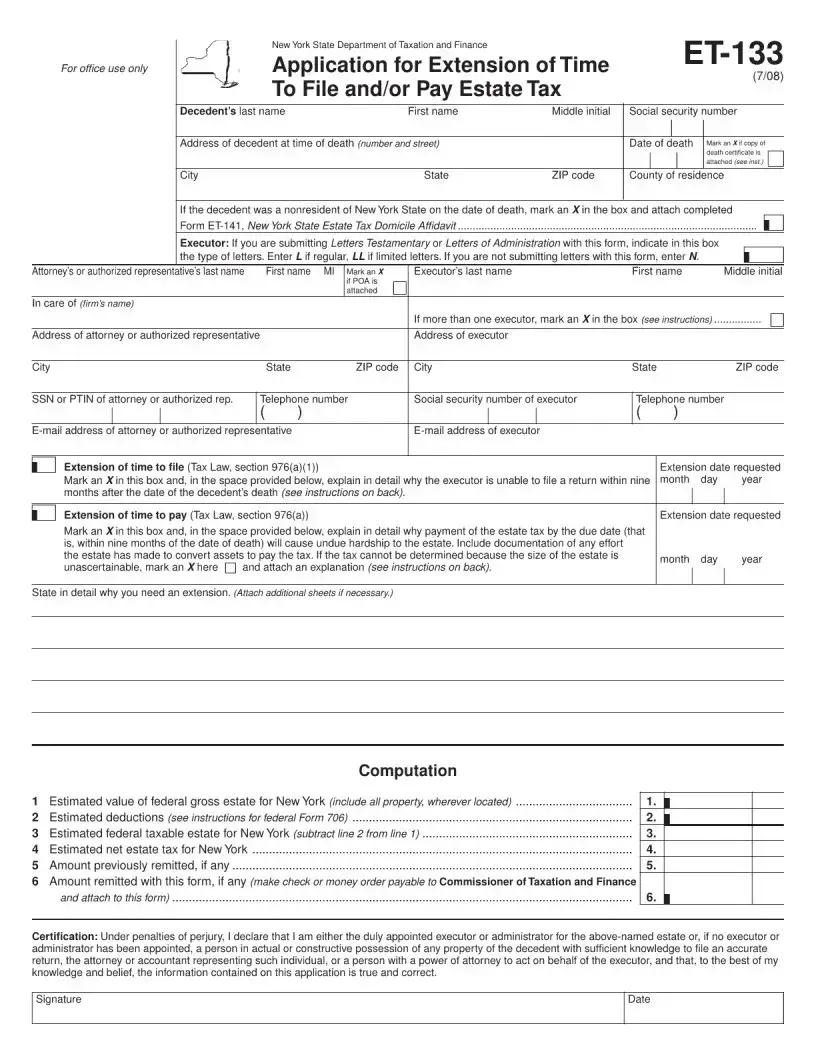

The New York ET-133 form is a crucial document for those managing the estate of a deceased individual in New York State. Executors, administrators, or authorized representatives can use this form to request an extension of time to file the estate tax return or to pay the estate tax. It is essential to submit this application within nine months of the decedent's death to avoid penalties. The form requires detailed information about the decedent, including their name, Social Security number, and address at the time of death. Additionally, it asks for information regarding the executor or authorized representative, including contact details and the nature of their authority. If the estate is facing challenges that hinder timely filing or payment, the form allows for explanations to be provided. This includes documenting any efforts made to liquidate assets for tax payment. Overall, the ET-133 form serves as a formal request for additional time, ensuring that executors can meet their obligations without undue hardship while complying with New York tax laws.

| Fact Name | Description |

|---|---|

| Form Purpose | The ET-133 form is used to apply for an extension of time to file and/or pay estate tax in New York State. |

| Governing Law | This form is governed by New York Tax Law, section 976. |

| Filing Deadline | Form ET-133 must be filed within nine months after the date of the decedent's death to avoid penalties. |

| Executor Definition | The term "executor" refers to the individual responsible for managing the decedent's estate, including executrix, administrator, or personal representative. |

| Power of Attorney | An authorized attorney or representative can file the form on behalf of the executor if they hold a power of attorney. |

| Documentation Requirement | If applicable, a copy of the death certificate must be attached to the ET-133 form when it is submitted. |

| Extension Explanation | The form requires a detailed explanation of why the executor cannot file or pay the estate tax by the due date. |

Completing the New York ET-133 form requires careful attention to detail. This application is essential for those seeking an extension of time to file or pay estate tax. Following the steps outlined below will help ensure that the form is filled out correctly and submitted on time.

Once the form is completed, it must be mailed to the NYS Estate Tax Processing Center. Ensure that all necessary attachments, such as the death certificate and letters testamentary, are included. By following these steps, the executor can effectively submit the application for an extension.

What is the New York ET-133 form?

The New York ET-133 form is an application for an extension of time to file and/or pay estate tax. Executors of an estate can use this form to request more time if they are unable to meet the original deadlines set by the state. It is important for the executor to provide details about why the extension is needed.

Who can file the ET-133 form?

The ET-133 form can be filed by the executor of the estate. This includes executors, executrices, administrators, or personal representatives. If no executor has been appointed, any person in possession of the decedent’s property can file. An attorney or accountant with power of attorney can also file on behalf of the executor.

When should the ET-133 form be filed?

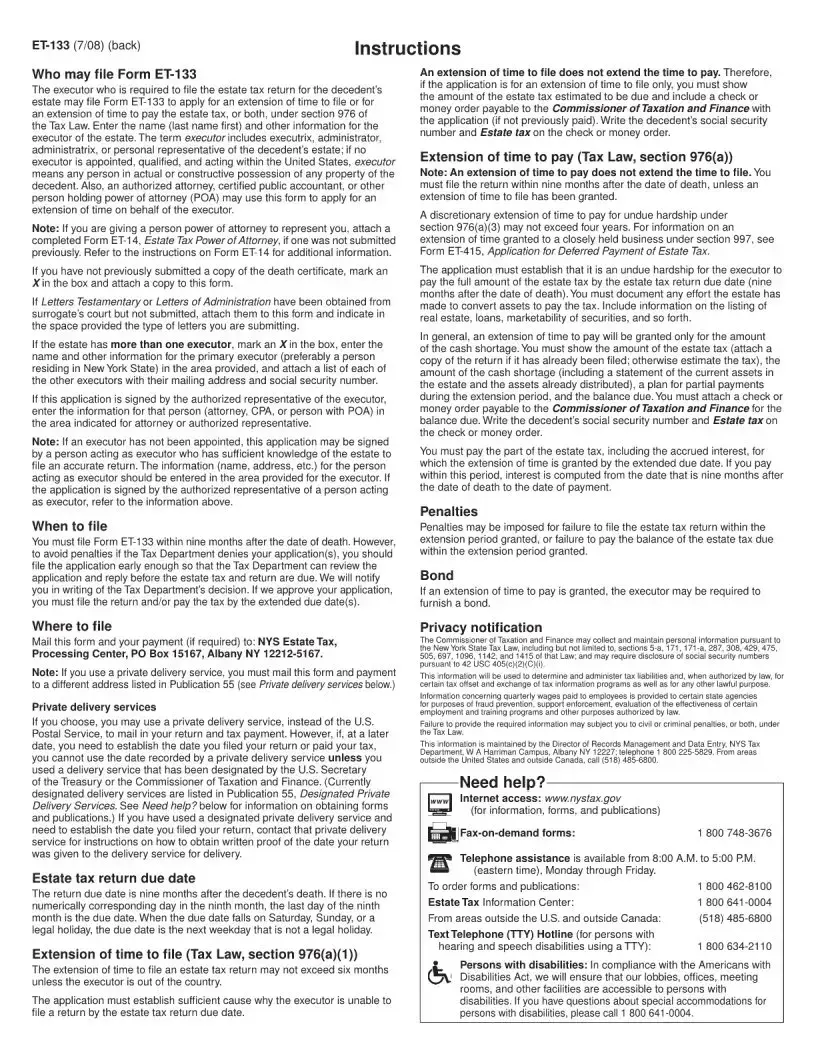

The ET-133 form must be filed within nine months after the date of the decedent's death. It is advisable to submit the form early to avoid penalties, as the Tax Department needs time to review the application and respond before the estate tax is due.

What information is required on the ET-133 form?

When completing the ET-133 form, you will need to provide the decedent's name, social security number, and address at the time of death. You must also include details about the executor, such as their name and contact information. If you are requesting an extension, you need to explain why you cannot file or pay on time.

Where should the ET-133 form be sent?

You should mail the completed ET-133 form to the NYS Estate Tax Processing Center at PO Box 15167, Albany NY 12212-5167. If you are using a private delivery service, you will need to check Publication 55 for the correct address to use.

What happens after I submit the ET-133 form?

Once you submit the ET-133 form, the Tax Department will review your application and notify you in writing of their decision. If your application is approved, you will receive an extended deadline for filing the estate tax return and/or making the payment.

Incomplete Personal Information: Many individuals fail to provide all required details about the decedent, such as the full name, social security number, or address at the time of death. Missing any of this information can delay the processing of the application.

Neglecting to Attach Necessary Documents: A common mistake is not attaching the death certificate or other essential documents like Letters Testamentary. These documents are crucial for verifying the application and should always be included when submitting the form.

Insufficient Explanation for Extensions: When requesting an extension, applicants often provide vague or incomplete explanations. It is important to clearly outline the reasons for needing more time to file or pay estate taxes, along with any supporting documentation.

Incorrect Filing Method: Some people mistakenly use a private delivery service without ensuring it is designated by the U.S. Secretary of the Treasury. This can lead to complications in establishing the filing date, which is important for meeting deadlines.

The New York ET-133 form is a crucial document for executors seeking an extension of time to file or pay estate tax. However, it is often accompanied by several other important forms and documents that help facilitate the estate tax process. Below is a list of these documents, along with a brief description of each.

Understanding the various forms and documents that accompany the New York ET-133 form is essential for executors navigating the estate tax process. Each document plays a unique role in ensuring compliance with state tax laws and facilitating the efficient management of the decedent's estate.

When filling out the New York ET-133 form, it is crucial to follow certain guidelines to ensure your application is processed smoothly. Here are four important things to do and avoid:

By adhering to these guidelines, you can help ensure a more efficient process when submitting your ET-133 form.

Many people have misconceptions about the New York ET-133 form. Understanding these can help clarify the process and ensure compliance. Here are seven common misconceptions:

By addressing these misconceptions, individuals can better navigate the complexities of the ET-133 form and fulfill their responsibilities effectively.

Filling out and using the New York ET-133 form requires careful attention to detail. Here are some key takeaways to consider: