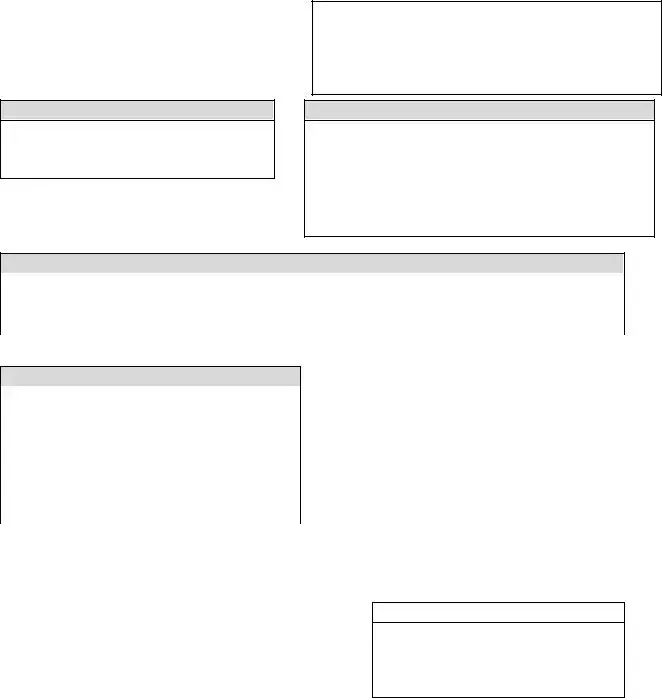

Understanding one's mortgage statement is crucial when it comes to managing a home loan efficiently. At the core of this document provided by the servicer, the statement outlines critical information starting with the servicer’s name, contact details, and the borrower's name and address, ensuring a personalized and direct communication channel. The statement date alongside the account number aligns the document's period and identifies the specific loan. With details such as the payment due date and the amount due, borrowers get a clear picture of their current obligations, including any late fees that apply if the payment is not received by the specified date. Furthermore, the form delves deeper into the financial specifics, breaking down the outstanding principal, interest rate, and any conditions regarding prepayment penalties. It provides a comprehensive overview of the amount due, separating principal, interest, and escrow responsibilities for taxes and insurance, which collectively emphasize the borrower's monthly financial commitment. The form also meticulously records transaction activities, including any payments received or fees charged, and a section dedicated to comparing past payments, thus offering a historical perspective on the borrower’s payment habits. Highlighting to borrowers are notifications on the implications of making partial payments and the consequences of delinquency, such as fees and potential foreclosure, while also offering guidance and resources for those experiencing financial difficulties. This orderly presentation of detailed and actionable information empowers borrowers to manage their mortgage effectively, providing a transparent snapshot of their loan at any given time.

| Fact | Description |

|---|---|

| Basic Information | Includes servicer name, customer service contact information, borrower's name and address, statement date, account number, payment due date, and amount due. |

| Account Information | Details the outstanding principal, interest rate until a specified date, if a prepayment penalty applies, and the breakdown of the amount due including principal, interest, escrow, regular monthly payment, total fees charged, and total amount due. |

| Transaction Activity | Records transactions within a specific period, including dates, descriptions of the activity (e.g., late fee charged, payment received), charges, and payments. |

| Important Messages | Contains essential notices about partial payments being held in a suspense account until full balance is paid, delinquency warnings including the number of days late and consequences of failure to bring loan current, and information for those experiencing financial difficulty including mortgage counseling. |

Filling out a Mortgage Statement form is a straightforward process that ensures your mortgage account details are up to date. This form is a crucial tool for maintaining transparency between you and your servicer, helping both parties keep track of payments, fees, and any changes to your mortgage terms. Below, we've outlined the steps to complete the form accurately. Remember, this document is not only a record of your mortgage status but also a legal document that could affect your financial future. Follow the instructions carefully to ensure that all information is correct and up to date.

Once you have completed all these steps, double-check the form for accuracy. This form is a critical component of your mortgage documentation, serving as a record of your payment history and current status. Accurate completion and timely submission can help you avoid unnecessary fees and maintain a good standing on your mortgage.

What is a Mortgage Statement?

A Mortgage Statement is an essential document provided by your mortgage servicer that outlines important details about your mortgage account. It includes your outstanding balance, interest rate, monthly payment, and more. This statement is crucial for tracking your loan progress and managing your budget.

How often will I receive my Mortgage Statement?

Mortgage statements are typically sent monthly. However, some servicers may offer electronic statements or quarterly updates. It's important to review each statement to monitor changes or updates to your loan.

What should I do if I notice a mistake on my statement?

If you spot any discrepancies or errors on your mortgage statement, contact your servicer immediately. Providing detailed information and documentation can help resolve issues quickly. Regularly reviewing your statement can prevent potential problems.

Can I make additional payments on my principal or escrow?

Yes, you can make additional payments towards your principal or escrow. These extra payments can reduce your principal balance faster and potentially save on interest. Inform your servicer about how to apply these extra funds correctly.

What happens if I make a late payment?

If your payment is received after the due date, a late fee will be charged. This fee varies by loan terms and state regulations. Timely payments are crucial for maintaining a good credit score and avoiding additional fees.

What is a Prepayment Penalty, and does my loan have one?

A Prepayment Penalty is a fee charged for paying off your loan early. Not all loans include this penalty. Refer to your mortgage statement or contact your servicer to determine if this applies to your loan.

What is included in the "Escrow" portion of my payment?

The "Escrow" portion of your payment is allocated for taxes and insurance related to your property. Your servicer uses these funds to pay your property taxes and homeowners insurance on your behalf.

What should I do if I'm having trouble making my mortgage payments?

If you're experiencing financial difficulties, it's important to act promptly. Contact your servicer to discuss available options, such as modification, forbearance, or refinancing. There may be assistance programs to help you navigate through tough times.

What is a Suspense Account mentioned in my statement?

A Suspense Account is where partial payments are temporarily held until there's enough to cover a full monthly payment. It's vital to understand that these funds will not be applied to your loan until a complete payment is made.

How can I bring my loan current if I'm behind on payments?

To bring your loan current, you must pay the total due amount outlined in your statement. This includes any late fees or additional charges that may have accrued. Contact your servicer to discuss a plan and avoid potential foreclosure.

Filling out the Mortgage Statement form correctly is crucial for a good understanding of your mortgage details and avoiding potential issues. Here are five common mistakes people make:

Properly filling out and understanding your mortgage statement is essential. It helps you keep track of your payments, interest rates, and any fees or penalties, ensuring you can manage your loan effectively and maintain your financial stability.

When managing a mortgage, a Mortgage Statement form offers vital information regarding the loan's status, including details such as the outstanding principal, interest rates, and the breakdown of the current payment due. However, to thoroughly understand one's mortgage and maintain accurate records, several other forms and documents frequently accompany the Mortgage Statement. These essential pieces of paperwork contribute to a comprehensive understanding of the mortgage process, from application to potential modification and even refinancing. Below is a list of documents often used alongside the Mortgage Statement form:

Together, these documents help borrowers navigate the complexities of managing their mortgage, ensuring they stay informed and in control of their home financing. It's crucial for homeowners to understand and retain these documents, as they each play a role in the broader narrative of homeowner finance, from the onset of the loan application to the fulfillment of the mortgage terms or any necessary adjustments along the way.

Loan Amortization Schedule: Similar to a mortgage statement, a loan amortization schedule displays the breakdown of payments over the life of a loan, including principal and interest components. Both documents detail how payments are applied to the loan over time, highlighting the reduction in principal owed.

Annual Mortgage Statement: This document recaps the payments made over the past year on a mortgage, showing the principal, interest, escrow amounts paid, and the outstanding balance, much like a monthly mortgage statement, but on an annual basis.

Escrow Statement: An escrow statement, similar to the escrow section of a mortgage statement, outlines the taxes and insurance payments made from an escrow account. Both provide details on the escrow account's activity over a specified period.

Credit Card Statement: Like a mortgage statement, a credit card statement includes transaction details, payments made, fees charged, and the total amount due. Each serves to inform the borrower of the current account status and any action required.

Loan Servicing Disclosure Statement: This document provides information about the handling of a loan, details on fees, and payment processes, similar to the information found on a mortgage statement regarding how payments are applied and the presence of any late fees.

Home Equity Line of Credit (HELOC) Statement: A HELOC statement and a mortgage statement offer similar information in terms of outstanding balance, interest rate, and payment details. Both aim to keep the borrower informed about the loan status and any costs incurred.

Rent Statement: Rent statements and mortgage statements both detail amounts due for a specific period, late fees, and payment history. While one pertains to rent and the other to mortgage, each serves a similar purpose in providing a financial summary to the owing party.

Utility Bill: Although covering different types of charges, both a utility bill and a mortgage statement specify the total amount due, breakdown of charges/payments, and consequences of late payments, keeping consumers informed of their account status.

Auto Loan Statement: This document shares similarities with a mortgage statement in detailing the principal and interest portions of the payments, the outstanding loan balance, and interest rate, providing crucial loan information to the borrower.

Insurance Premium Statement: Like a mortgage statement, an insurance premium statement shows the amount due, payment deadline, and details of the coverage period. Both serve to inform the policyholder or borrower of financial obligations and the status of the account.

When filling out a Mortgage Statement form, it is crucial to adhere to certain dos and don'ts to ensure the accuracy and completeness of the information provided. This guidance not only helps in avoiding common mistakes but also facilitates better communication between borrowers and servicers.

Things You Should Do

Things You Shouldn't Do

When it comes to understanding your mortgage statement, there's a fair share of confusion out there. Let's clarify four common misconceptions that can help homeowners better navigate their mortgage responsibilities:

Some people think the principal amount listed on their mortgage statement is the total amount they owe on their loan. However, the principal amount shown only represents the outstanding balance of the loan itself, excluding future interest, potential fees, or any escrow balances that might be due. To get a complete picture of what you owe, you'll need to look at the entire statement, including interest, fees, and escrow details.

Another common area of confusion is the interest rate. Many assume that the rate listed on their statement is locked in until their mortgage is fully paid off. This might be true if you have a fixed-rate mortgage. However, if you have an adjustable-rate mortgage (ARM), your interest rate can change over time based on prevailing economic conditions. It’s important to understand which type of rate applies to your loan and when it might adjust.

When you see a late fee outlined in your mortgage statement, you might think it's either negotiable or can be waived with a simple phone call to your mortgage servicer. While some servicers may work with you during financial hardships, late fees are generally a standard part of mortgage agreements and are enforced according to the terms of your loan. Being proactive and communicating with your servicer before a payment is late might present more options.

A tricky part of mortgage management is handling partial payments. You might expect that any amount paid would chip away at your mortgage balance immediately. However, what often happens is that partial payments are held in a separate account (referred to as a suspense account) until the full payment amount can be made. Knowing this can help prevent misunderstandings about your balance and payment status.

Understanding these aspects of your mortgage statement can demystify the process, helping you to navigate your payments more effectively and avoid common pitfalls. Always reach out to your mortgage servicer with specific questions or concerns; they're there to help guide you through the intricacies of your mortgage account.

Understanding your mortgage statement is crucial for managing your home loan effectively. Here are seven key takeaways to help you navigate the details of your Mortgage Statement form:

Furthermore, the statement highlights critical messages for homeowners in financial difficulty, including the potential for fees and foreclosure if the loan remains delinquent, and provides information on mortgage counseling and assistance. Keeping these key takeaways in mind will help you better understand your mortgage statement and manage your home loan more effectively.

Permanent Partial Disability Ohio - Accurate reporting ensures timely processing of claims.

Consignment Contract - The form requires disclosure of any existing lien holders.

What Number Do I Call for Food Stamp Interview in Florida - Each submission contributes to the overall mission of supporting families in need.