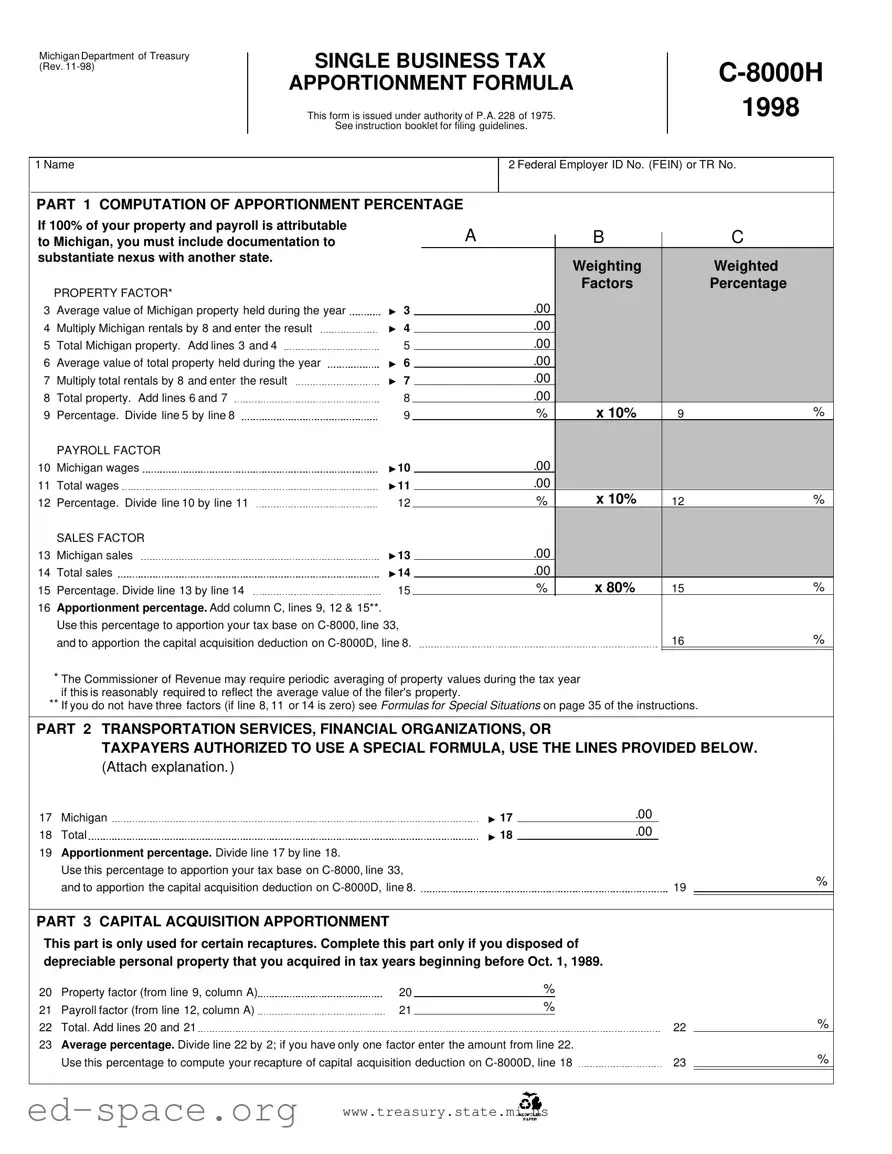

The Michigan C 8000H form serves as a crucial tool for businesses operating within the state, specifically designed to calculate the apportionment percentage of their single business tax. This form, issued under the authority of Public Act 228 of 1975, allows businesses to fairly allocate their tax obligations based on their presence and economic activity in Michigan. It requires businesses to provide essential information, including their Federal Employer Identification Number (FEIN) or Taxpayer Registration Number (TR No.), and to compute various factors that contribute to the overall apportionment percentage. The form is divided into three main parts: the computation of the apportionment percentage based on property, payroll, and sales factors; specific guidelines for transportation services and financial organizations; and a section dedicated to capital acquisition apportionment for certain recaptures. Each part necessitates careful calculation and documentation, ensuring that businesses accurately reflect their economic ties to the state. The importance of this form cannot be overstated, as it directly influences the tax base for the single business tax and the capital acquisition deduction, making it essential for compliance and financial planning.

Michigan Department of Treasury (Rev.

SINGLE BUSINESS TAX APPORTIONMENT FORMULA

This form is issued under authority of P.A. 228 of 1975.

See instruction booklet for filing guidelines.

1998

1 Name

2 Federal Employer ID No. (FEIN) or TR No.

PART 1 COMPUTATION OF APPORTIONMENT PERCENTAGE

If 100% of your property and payroll is attributable |

|

|

|

|

A |

|

B |

|

C |

|

to Michigan, you must include documentation to |

|

|

|

|

|

|

||||

substantiate nexus with another state. |

|

|

|

|

|

|

Weighting |

|

Weighted |

|

|

|

|

|

|

|

|

|

|

||

|

PROPERTY FACTOR* |

|

|

|

|

|

|

Factors |

|

Percentage |

|

|

|

|

|

|

|

|

|

|

|

3 |

Average value of Michigan property held during the year |

▼ |

3 |

|

|

|

.00 |

|

|

|

4 |

Multiply Michigan rentals by 8 and enter the result |

▼ |

4 |

|

|

|

.00 |

|

|

|

5 |

Total Michigan property. Add lines 3 and 4 |

|

5 |

|

|

|

.00 |

|

|

|

6 |

Average value of total property held during the year |

▼ |

6 |

|

|

|

.00 |

|

|

|

7 |

Multiply total rentals by 8 and enter the result |

▼ |

7 |

|

|

|

.00 |

|

|

|

8 |

Total property. Add lines 6 and 7 |

|

8 |

|

|

|

.00 |

|

|

|

9 |

Percentage. Divide line 5 by line 8 |

|

9 |

|

|

|

% |

x 10% |

9 |

% |

|

PAYROLL FACTOR |

|

|

|

|

|

|

|

|

|

10 |

Michigan wages |

▼ |

10 |

|

|

|

.00 |

|

|

|

11 |

Total wages |

▼ |

11 |

|

|

|

.00 |

|

|

|

12 |

Percentage. Divide line 10 by line 11 |

|

12 |

|

|

|

% |

x 10% |

12 |

% |

|

SALES FACTOR |

|

|

|

|

|

|

|

|

|

13 |

Michigan sales |

▼ |

13 |

|

|

|

.00 |

|

|

|

14 |

Total sales |

▼ |

14 |

|

|

|

.00 |

|

|

|

15 |

Percentage. Divide line 13 by line 14 |

|

15 |

|

|

|

% |

x 80% |

15 |

% |

16 |

Apportionment percentage. Add column C, lines 9, 12 & 15**. |

|

|

|

|

|

|

|

|

|

|

Use this percentage to apportion your tax base on |

|

|

|

|

|||||

|

and to apportion the capital acquisition deduction on |

|

|

16 |

% |

|||||

|

|

|

|

|

|

|

|

|

|

|

*The Commissioner of Revenue may require periodic averaging of property values during the tax year if this is reasonably required to reflect the average value of the filer's property.

**If you do not have three factors (if line 8, 11 or 14 is zero) see Formulas for Special Situations on page 35 of the instructions.

PART 2 TRANSPORTATION SERVICES, FINANCIAL ORGANIZATIONS, OR

TAXPAYERS AUTHORIZED TO USE A SPECIAL FORMULA, USE THE LINES PROVIDED BELOW.

(Attach explanation. )

17 Michigan

▼

17

.00

18Total

19Apportionment percentage. Divide line 17 by line 18.

Use this percentage to apportion your tax base on

▼

18

.00

19 |

% |

|

PART 3 CAPITAL ACQUISITION APPORTIONMENT

This part is only used for certain recaptures. Complete this part only if you disposed of depreciable personal property that you acquired in tax years beginning before Oct. 1, 1989.

20 |

Property factor (from line 9, column A) |

20 |

% |

|

|

|

21 |

Payroll factor (from line 12, column A) |

21 |

% |

|

|

|

22 |

Total. Add lines 20 and 21 |

|

|

|

22 |

% |

23 |

Average percentage. Divide line 22 by 2; if you have only one factor enter the amount from line 22. |

|

|

|||

|

Use this percentage to compute your recapture of capital acquisition deduction on |

23 |

% |

|||

www.treasury.state.mi.us

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Michigan C 8000H form is used to calculate the apportionment percentage for the Single Business Tax. |

| Governing Law | This form is issued under the authority of Public Act 228 of 1975. |

| Filing Guidelines | Filing guidelines are provided in an instruction booklet that accompanies the form. |

| Property Factor | The property factor is calculated based on the average value of Michigan property held during the year. |

| Payroll Factor | The payroll factor is determined by dividing Michigan wages by total wages. |

| Sales Factor | The sales factor is calculated by dividing Michigan sales by total sales. |

| Apportionment Percentage | The final apportionment percentage is derived from the sum of the three factors: property, payroll, and sales. |

| Special Situations | If a taxpayer lacks three factors, specific formulas for special situations are provided in the instructions. |

Completing the Michigan C 8000H form involves several steps to accurately report your business's apportionment percentage. This percentage is crucial for determining your tax obligations. Follow these steps carefully to ensure all required information is provided.

After filling out the form, review all entries for accuracy. Ensure that all calculations are correct and that you have attached any necessary documentation. Once confirmed, submit the form as instructed in the accompanying guidelines.

What is the purpose of the Michigan C 8000H form?

The Michigan C 8000H form is used to calculate the apportionment percentage for the Single Business Tax. This percentage is essential for determining how much of a business's tax base is subject to Michigan taxation. The form includes factors such as property, payroll, and sales to help establish this percentage.

Who needs to file the C 8000H form?

What factors are considered in the apportionment calculation?

The C 8000H form considers three main factors: property, payroll, and sales. Each factor is weighted differently in the final calculation. The property and payroll factors contribute 10% each, while the sales factor contributes 80% to the overall apportionment percentage.

How is the property factor calculated?

The property factor is determined by averaging the value of Michigan property held during the year and adjusting for Michigan rentals. Specifically, the average value of Michigan property is added to eight times the value of Michigan rentals. This total is then divided by the total property held to find the percentage.

What should I do if I do not have all three factors?

If a business does not have all three factors, such as if there are no Michigan sales, payroll, or property, it should refer to the special instructions provided in the C 8000H form booklet. There are specific formulas for special situations that can help determine the apportionment percentage in these cases.

What is the significance of the apportionment percentage?

The apportionment percentage calculated using the C 8000H form is crucial for determining the amount of tax liability a business has in Michigan. This percentage is applied to the tax base reported on the C-8000 form and is also used for calculating the capital acquisition deduction on the C-8000D form.

Can transportation services or financial organizations use a different formula?

Yes, transportation services, financial organizations, or other taxpayers authorized to use a special formula can complete the specific lines provided in Part 2 of the C 8000H form. They must attach an explanation detailing their unique circumstances and how they arrived at their apportionment percentage.

What is the capital acquisition apportionment section for?

This section is only relevant for businesses that disposed of depreciable personal property acquired in tax years beginning before October 1, 1989. It helps calculate the recapture of the capital acquisition deduction. The capital acquisition apportionment uses the property and payroll factors to determine the appropriate percentage for recapture.

Where can I find more information about filing the C 8000H form?

More information about filing the C 8000H form, including detailed instructions and guidelines, can be found on the Michigan Department of Treasury's website. The instruction booklet accompanying the form provides comprehensive guidance on the filing process and the calculations involved.

Neglecting to include the Federal Employer ID Number (FEIN): Failing to provide this essential identifier can lead to processing delays or outright rejection of the form.

Incorrectly calculating property factors: Many individuals miscalculate the average value of Michigan property or total property, resulting in inaccurate apportionment percentages.

Omitting documentation for nexus: If claiming 100% of property and payroll in Michigan, it is crucial to include supporting documentation for nexus with other states. Without it, the claim may be deemed invalid.

Failing to average property values: The Commissioner of Revenue may require periodic averaging of property values. Ignoring this requirement can lead to discrepancies in reported values.

Misunderstanding the sales factor calculation: Confusion often arises in dividing Michigan sales by total sales, leading to incorrect percentages that affect the overall apportionment.

Leaving lines blank: Not filling in all required lines, especially those related to payroll and sales, can result in an incomplete form and possible penalties.

Incorrectly applying the apportionment percentages: Mistakes in applying the calculated percentages to the C-8000 and C-8000D forms can lead to significant tax miscalculations.

Ignoring special formulas for specific taxpayers: Certain taxpayers, such as transportation services or financial organizations, may need to use a special formula. Failing to do so can result in improper apportionment.

Not reviewing the instruction booklet: Skipping the instruction booklet can lead to misunderstandings about filing guidelines and requirements, which are crucial for accurate completion of the form.

The Michigan C 8000H form is used for the apportionment of the Single Business Tax. Alongside this form, several other documents may be necessary to ensure compliance with state tax regulations. Below is a list of commonly used forms and documents that accompany the C 8000H form.

Understanding these forms and their purposes can help businesses navigate the complexities of tax reporting in Michigan. Proper completion and submission of these documents are crucial for compliance and to avoid potential penalties.

The Michigan C 8000H form serves as a critical tool for businesses in determining their single business tax apportionment. Several other documents share similarities with this form, particularly in their purpose of calculating tax obligations based on various factors. Below is a list of ten documents that are comparable to the C 8000H form, along with explanations of their similarities.

Each of these documents plays a role in the broader context of tax compliance and apportionment, emphasizing the importance of accurately reporting business activities and financial data to determine tax obligations.

When filling out the Michigan C 8000H form, it’s important to follow specific guidelines to ensure accuracy and compliance. Here’s a list of what you should and shouldn’t do:

Following these guidelines can help avoid delays or issues with your tax filings.

Understanding the Michigan C 8000H form can be challenging, and several misconceptions can lead to confusion. Here are four common misunderstandings about this form:

This is not true. The C 8000H form is applicable to any business entity that needs to apportion its tax base in Michigan, regardless of size. Small businesses also need to ensure they comply with the requirements outlined in this form.

This is a common error. Even if all your property is located in Michigan, you still need to calculate the payroll and sales factors. These factors are essential for determining the overall apportionment percentage.

While it may seem logical, this isn't accurate. The apportionment percentage is calculated based on property, payroll, and sales factors. Even if your business is entirely in Michigan, the percentages from these factors must still be considered.

This misconception can lead to complications. If your business claims 100% of its property in Michigan, you must still provide documentation to substantiate your nexus with other states. This helps ensure compliance with tax regulations.

When filling out the Michigan C 8000H form, it's crucial to pay attention to several key aspects to ensure accuracy and compliance. Here are some important takeaways:

Completing the C 8000H form correctly can significantly impact your tax obligations. Be diligent and thorough in your calculations and documentation.