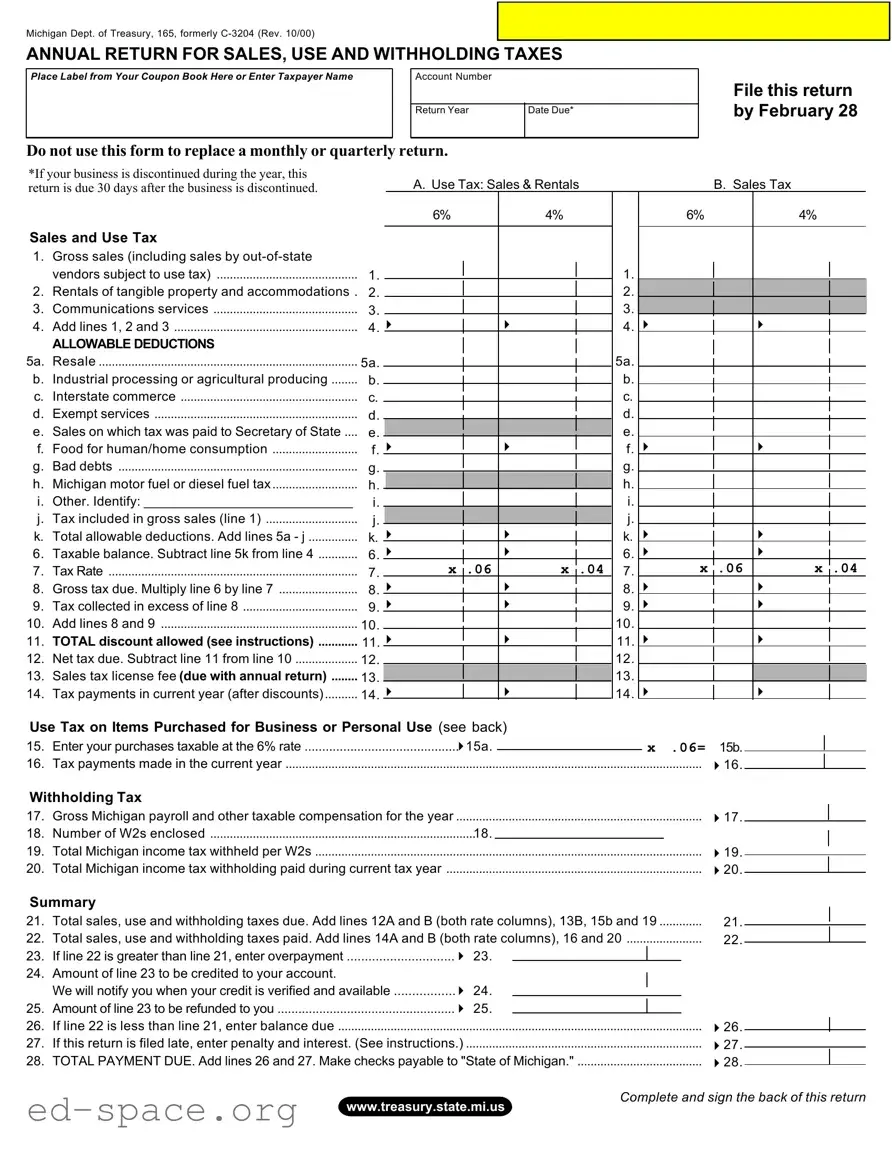

The Michigan C 3204 form is an essential document for businesses operating within the state, designed to streamline the reporting of sales, use, and withholding taxes. This annual return must be filed by February 28 each year, unless the business has been discontinued, in which case it is due 30 days after the closure. The form captures various aspects of a business's financial activities, including gross sales, rentals, and communications services, all of which are subject to specific tax rates. Allowable deductions are also a key feature, allowing businesses to reduce their taxable income by accounting for items such as resale, agricultural production, and certain exempt services. The form requires businesses to calculate their taxable balance, gross tax due, and any overpayments or balances owed. Additionally, it includes sections for reporting use tax on personal or business purchases and withholding tax on employee wages. Completing the C 3204 accurately is crucial for compliance and to ensure that businesses fulfill their tax obligations without incurring penalties.

Michigan Dept. of Treasury, 165, formerly

ANNUAL RETURN FOR SALES, USE AND WITHHOLDING TAXES

Place Label from Your Coupon Book Here or Enter Taxpayer Name |

|

Account Number |

|

|

|

|

|

|

|

Return Year |

Date Due* |

|

|

|

|

Do not use this form to replace a monthly or quarterly return.

File this return by February 28

*If your business is discontinued during the year, this |

|

|

|

A. Use Tax: Sales & Rentals |

|

|

|

|

|

|

B. Sales Tax |

|

|

|

|

|||||||||||

return is due 30 days after the business is discontinued. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

6% |

|

|

|

4% |

|

|

|

6% |

|

|

|

|

|

4% |

|

|

|

||||

Sales and Use Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. |

Gross sales (including sales by |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

vendors subject to use tax) |

1. |

|

|

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2. |

Rentals of tangible property and accommodations . |

2. |

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Communications services |

3. |

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Add lines 1, 2 and 3 |

4. |

4 |

|

|

|

|

4 |

|

|

4. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

ALLOWABLE DEDUCTIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5a. |

Resale |

5a. |

|

|

|

|

|

|

|

|

|

|

5a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

b. |

Industrial processing or agricultural producing |

b. |

|

|

|

|

|

|

|

|

|

|

b. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

c. |

Interstate commerce |

c. |

|

|

|

|

|

|

|

|

|

|

c. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

d. |

Exempt services |

d. |

|

|

|

|

|

|

|

|

|

|

d. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

e. |

Sales on which tax was paid to Secretary of State .... |

e. |

|

|

|

|

|

|

|

|

|

|

e. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

||||||

f. |

Food for human/home consumption |

f. |

|

|

|

|

|

|

f. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

g. |

Bad debts |

g. |

|

|

|

|

|

|

|

|

|

|

g. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

h. |

Michigan motor fuel or diesel fuel tax |

h. |

|

|

|

|

|

|

|

|

|

|

h. |

|

|

|

|

|

|

|

|

|

|

|

|

|

i. |

Other. Identify: ____________________________ |

i. |

|

|

|

|

|

|

|

|

|

|

i. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

j. |

Tax included in gross sales (line 1) |

j. |

|

|

|

|

|

|

|

|

|

|

j. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

||||||

k. |

Total allowable deductions. Add lines 5a - j |

k. |

|

|

|

|

|

|

k. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

6. |

Taxable balance. Subtract line 5k from line 4 |

6. |

4 |

|

|

|

|

4 |

|

|

6. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

X |

|

.06 |

|

X |

|

.04 |

|

|

|

X |

|

.06 |

|

X |

|

.04 |

||||||||

7. |

Tax Rate |

7. |

|

|

|

|

|

7. |

|

|

|

|

|

|

||||||||||||

8. |

Gross tax due. Multiply line 6 by line 7 |

8. |

4 |

|

|

|

|

4 |

|

|

8. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4 |

|

|

|

|

4 |

|

|

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||||||

9. |

Tax collected in excess of line 8 |

9. |

|

|

|

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

10. |

Add lines 8 and 9 |

10. |

|

|

|

|

|

|

|

|

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

11. |

TOTAL discount allowed (see instructions) |

11. |

4 |

|

|

|

|

4 |

|

|

11. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

12. |

Net tax due. Subtract line 11 from line 10 |

12. |

|

|

|

|

|

|

|

|

|

|

12. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

13. |

Sales tax license fee (due with annual return) |

13. |

|

|

|

|

|

|

|

|

|

|

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

Tax payments in current year (after discounts) |

14. |

4 |

|

|

|

|

4 |

|

|

14. |

4 |

|

|

|

|

|

|

4 |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Use Tax on Items Purchased for Business or Personal Use (see back) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

15. |

Enter your purchases taxable at the 6% rate |

|

|

415a. |

|

|

|

|

|

|

X .06= |

|

|

15b. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

16. |

Tax payments made in the current year |

|

|

|

|

................................................................. |

|

|

|

|

|

|

|

|

|

416. |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Withholding Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17. |

...........................................................................Gross Michigan payroll and other taxable compensation for the year |

|

|

|

|

|

|

|

|

|

417. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

18. |

Number of W2s enclosed |

|

|

|

18. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

19. |

Total Michigan income tax withheld per W2s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

419. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

20. |

Total Michigan income tax withholding paid during current tax year |

|

|

|

|

|

|

|

|

|

420. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Summary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

21. |

Total sales, use and withholding taxes due. Add lines 12A and B (both rate columns), 13B, 15b and 19 |

21. |

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||||

22. |

Total sales, use and withholding taxes paid. Add lines 14A and B (both rate columns), 16 and 20 |

|

|

|

|

22. |

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

23. |

If line 22 is greater than line 21, enter overpayment |

|

|

4 23. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

24. |

Amount of line 23 to be credited to your account. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

We will notify you when your credit is verified and available |

4 24. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

25. |

Amount of line 23 to be refunded to you |

|

|

4 25. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

26. |

If line 22 is less than line 21, enter balance due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

426. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

27. |

If this return is filed late, enter penalty and interest. (See instructions.) |

|

|

|

|

|

|

|

|

|

427. |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

28. |

TOTAL PAYMENT DUE. Add lines 26 and 27. Make checks payable to "State of Michigan." |

|

|

|

|

|

428. |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Complete and sign the back of this return

www.treasury.state.mi.us

Type of Business Ownership (check one only)

Individual

Husband - Wife

Partnership

Registered Partnership, Agreement Date:

Limited Partnership

Limited Liability Company

Domestic (Michigan)

Professional

Foreign

Michigan Corporation

Subchapter S

Professional

Trust or Estate (Fiduciary)

Joint Stock Club or Investment Company Social Club or Fraternal Organization Other (Explain)

Signature

I declare, under penalty of perjury, that this return is true and complete to the best of my knowledge.

I authorize Treasury to discuss my return with my preparer. Do not discuss my return with my preparer.

Taxpayer's Signature

Taxpayer's Social Security Number |

Telephone Number |

|

|

( |

) |

|

|

|

Taxpayer's Title |

Date |

|

|

|

|

I declare, under penalty of perjury, that this return is based on all information of which I have any knowledge.

Preparer's Signature, Address and Phone and ID Number

If you are enclosing payment with your return, MAIL TO: Sales, Use and Withholding Taxes

Michigan Department of Treasury

Lansing, MI 48922

If your return is for a refund, credit or has no tax due, MAIL TO: Sales, Use and Withholding Taxes

Michigan Department of Treasury

Lansing, MI 48930

*Use Tax on Items Purchased for Business or Personal Use

Use lines 15 and 16 to report purchases made for use in your business or for items removed from your inventory for personal use. Do not repeat the amounts from Column A, lines 1 - 4 here.

| Fact Name | Details |

|---|---|

| Form Title | Annual Return for Sales, Use and Withholding Taxes |

| Governing Law | Michigan Compiled Laws, Act 167 of 1933 |

| Filing Deadline | February 28 of the following year, or 30 days after business discontinuation |

| Tax Rates | Sales Tax: 6%, Use Tax: 6%, Withholding Tax: 4% |

| Purpose | To report and pay sales, use, and withholding taxes collected during the year |

| Allowable Deductions | Includes resale, industrial processing, and exempt services |

| Signature Requirement | Taxpayer must sign under penalty of perjury |

| Submission Addresses | Different addresses for payments and refunds |

Completing the Michigan C 3204 form requires careful attention to detail. This form is essential for reporting your annual sales, use, and withholding taxes. Make sure to have all necessary information and documents ready before starting. Follow these steps to ensure accurate completion of the form.

What is the Michigan C 3204 form used for?

The Michigan C 3204 form is an annual return for reporting sales, use, and withholding taxes. It is specifically designed for businesses operating in Michigan to report their gross sales, allowable deductions, and the taxes due. This form must be filed by February 28 each year, unless the business is discontinued, in which case the return is due 30 days after the business ceases operations. It is important to note that this form should not be used to replace monthly or quarterly returns.

Who needs to file the Michigan C 3204 form?

What information do I need to complete the Michigan C 3204 form?

What happens if I file the Michigan C 3204 form late?

Neglecting to Sign the Form: Many individuals forget to sign the form, which can lead to processing delays or rejections. Always ensure that the taxpayer's signature is included.

Incorrect Account Number: Entering an incorrect taxpayer account number is a common mistake. Double-check the number to avoid complications with the processing of your return.

Miscalculating Gross Sales: Failing to accurately report gross sales, including those from out-of-state vendors, can result in significant errors. Review all sales records thoroughly before entering this figure.

Omitting Allowable Deductions: Some filers forget to include all applicable deductions. Ensure you list every deduction, such as food for human consumption or bad debts, to minimize your taxable amount.

Not Filing on Time: Missing the deadline can incur penalties and interest. Mark your calendar for February 28, or 30 days after discontinuing your business, to avoid late fees.

Failing to Include Payment Details: If you owe taxes, be sure to include the correct payment amount. Mistakes in this area can lead to complications and additional charges.

Inaccurate Contact Information: Providing incorrect contact information can hinder communication. Always verify that your phone number and address are correct to ensure you receive any necessary follow-up.

When filing the Michigan C 3204 form, it is essential to be aware of other forms and documents that may be necessary to ensure compliance with state tax regulations. Each of these documents serves a specific purpose and can help streamline the filing process.

Understanding these additional forms and documents can significantly aid in the accurate and timely filing of your tax obligations. Staying organized and informed is key to avoiding penalties and ensuring compliance with Michigan tax laws.

The Michigan C 3204 form serves as an important document for businesses to report their sales, use, and withholding taxes. Several other forms share similarities with the C 3204, primarily in their purpose and structure. Here are six such documents:

When filling out the Michigan C 3204 form, it's important to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Understanding the Michigan C 3204 form can be challenging. Here are some common misconceptions about this form:

By clarifying these misconceptions, taxpayers can better understand their responsibilities and ensure compliance with Michigan tax laws.

Filling out the Michigan C 3204 form is an important task for businesses that need to report their sales, use, and withholding taxes. Understanding how to properly complete this form can help ensure compliance with state tax regulations. Below are key takeaways to consider when working with the Michigan C 3204 form.

Completing the Michigan C 3204 form accurately is essential for maintaining good standing with state tax authorities. By following these key takeaways, businesses can navigate the process with greater confidence and clarity.