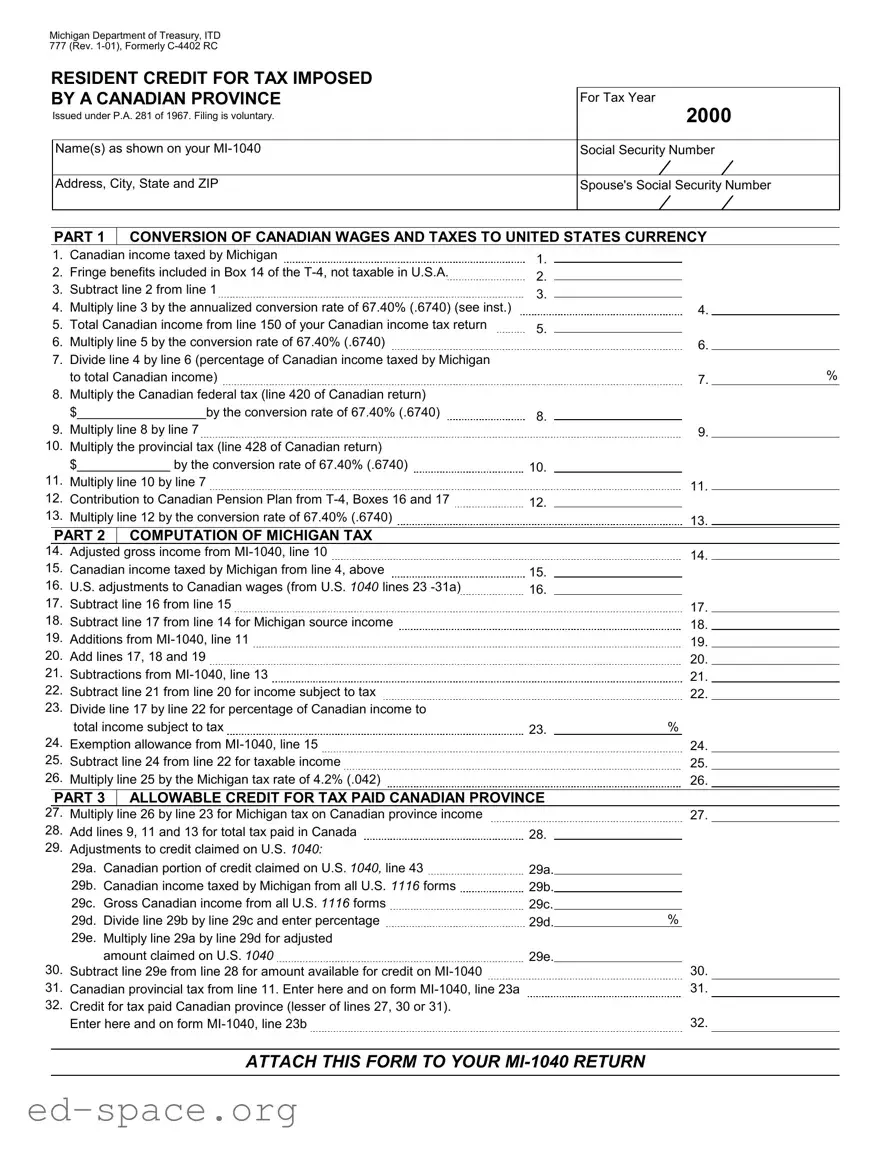

The Michigan 777 form, officially known as the Resident Credit for Tax Imposed by a Canadian Province, serves as a vital tool for residents of Michigan who earn income from Canadian sources. This form, issued under Public Act 281 of 1967, allows taxpayers to claim a credit for taxes paid to Canadian provinces, ensuring that they are not taxed twice on the same income. While filing this form is voluntary, it can significantly benefit those who have worked in Canada or received income from Canadian sources. The form consists of several parts, each designed to guide taxpayers through the process of converting Canadian wages and taxes into U.S. currency, computing Michigan tax, and determining the allowable credit for taxes paid to Canada. Individuals must provide their personal information, including names, Social Security numbers, and details of their Canadian income, in order to accurately complete the form. By carefully following the instructions and completing each section, taxpayers can ensure they receive the appropriate credit, thus alleviating some of the financial burdens associated with cross-border income. The Michigan 777 form ultimately aims to foster fairness in taxation for residents who navigate the complexities of earning income in two different countries.

Michigan Department of Treasury, ITD

777 (Rev.

RESIDENT CREDIT FOR TAX IMPOSED |

|

|

|

BY A CANADIAN PROVINCE |

For Tax Year |

Issued under P.A. 281 of 1967. Filing is voluntary. |

2000 |

|

|

Name(s) as shown on your |

Social Security Number |

|

|

Address, City, State and ZIP |

Spouse's Social Security Number |

|

|

PART 1

CONVERSION OF CANADIAN WAGES AND TAXES TO UNITED STATES CURRENCY

1. |

Canadian income taxed by Michigan |

1. |

|

|

|

2. |

Fringe benefits included in Box 14 of the |

2. |

|

|

|

3. |

Subtract line 2 from line 1 |

3. |

|

|

|

4. |

Multiply line 3 by the annualized conversion rate of 67.40% (.6740) (see inst.) |

|

5. |

Total Canadian income from line 150 of your Canadian income tax return |

5. |

|

|

6.Multiply line 5 by the conversion rate of 67.40% (.6740)

7.Divide line 4 by line 6 (percentage of Canadian income taxed by Michigan to total Canadian income)

8.Multiply the Canadian federal tax (line 420 of Canadian return)

|

$__________________by the conversion rate of 67.40% (.6740) |

8. |

|

|

|

9. |

Multiply line 8 by line 7 |

|

10. |

Multiply the provincial tax (line 428 of Canadian return) |

|

|

$_____________ by the conversion rate of 67.40% (.6740) |

10. |

11. |

Multiply line 10 by line 7 |

|

12. |

Contribution to Canadian Pension Plan from |

12. |

13. |

Multiply line 12 by the conversion rate of 67.40% (.6740) |

|

4.

6.

7.%

11.

13.

PART 2 COMPUTATION OF MICHIGAN TAX

14.Adjusted gross income from

15.Canadian income taxed by Michigan from line 4, above

16.U.S. adjustments to Canadian wages (from U.S. 1040 lines 23

17.Subtract line 16 from line 15

18.Subtract line 17 from line 14 for Michigan source income

19.Additions from

20.Add lines 17, 18 and 19

21.Subtractions from

22.Subtract line 21 from line 20 for income subject to tax

23.Divide line 17 by line 22 for percentage of Canadian income to

total income subject to tax

24.Exemption allowance from

25.Subtract line 24 from line 22 for taxable income

26.Multiply line 25 by the Michigan tax rate of 4.2% (.042)

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.%

24.

25.

26.

PART 3 ALLOWABLE CREDIT FOR TAX PAID CANADIAN PROVINCE

27. |

Multiply line 26 by line 23 for Michigan tax on Canadian province income |

|

|

28. |

Add lines 9, 11 and 13 for total tax paid in Canada |

28. |

|

29. |

Adjustments to credit claimed on U.S. 1040: |

|

|

|

29a. |

Canadian portion of credit claimed on U.S. 1040, line 43 |

29a. |

|

29b. |

Canadian income taxed by Michigan from all U.S. 1116 forms |

29b. |

|

29c. |

Gross Canadian income from all U.S. 1116 forms |

29c. |

|

29d. |

Divide line 29b by line 29c and enter percentage |

29d. |

|

29e. |

Multiply line 29a by line 29d for adjusted |

|

|

|

amount claimed on U.S. 1040 |

29e. |

30.Subtract line 29e from line 28 for amount available for credit on

31.Canadian provincial tax from line 11. Enter here and on form

32.Credit for tax paid Canadian province (lesser of lines 27, 30 or 31). Enter here and on form

27.

%

30.

31.

32.

ATTACH THIS FORM TO YOUR

| Fact Name | Details |

|---|---|

| Form Title | Michigan Department of Treasury, ITD 777 (Rev. 1-01) |

| Purpose | This form is used to claim a resident credit for taxes imposed by a Canadian province. |

| Governing Law | Issued under Public Act 281 of 1967. |

| Filing Status | Filing is voluntary for taxpayers who qualify. |

| Conversion Rate | The form uses a conversion rate of 67.40% for Canadian wages and taxes to U.S. currency. |

| Attachment Requirement | This form must be attached to the MI-1040 return when submitted. |

Completing the Michigan 777 form is an important step in filing your taxes if you have income from a Canadian province. After filling out the form, you will attach it to your MI-1040 return. Follow these steps carefully to ensure accuracy.

Next, move to Part 1, which involves converting Canadian wages and taxes to U.S. currency.

Proceed to Part 2 to compute your Michigan tax.

Finally, complete Part 3 to determine the allowable credit for tax paid to the Canadian province.

Once completed, attach this form to your MI-1040 return for submission.

What is the Michigan 777 form and who needs to file it?

The Michigan 777 form, also known as the Resident Credit for Tax Imposed by a Canadian Province, is a document that allows Michigan residents to claim a credit for taxes paid to a Canadian province. This form is issued under Public Act 281 of 1967. It is voluntary to file, meaning that individuals who have paid taxes to a Canadian province and are residents of Michigan may choose to submit this form to receive a credit on their Michigan tax return.

How do I convert Canadian wages and taxes to U.S. currency on the Michigan 777 form?

To convert Canadian wages and taxes to U.S. currency, you will need to follow several steps outlined in Part 1 of the form. First, you will report your Canadian income that has been taxed by Michigan. Next, you will account for any fringe benefits that are included in Box 14 of your T-4 but are not taxable in the U.S. After calculating the necessary conversions using the annualized conversion rate of 67.40%, you will complete the required calculations to determine the percentage of Canadian income taxed by Michigan compared to your total Canadian income. This process ensures that the amounts are accurately represented in U.S. dollars.

What calculations are involved in determining my Michigan tax on Canadian income?

Part 2 of the Michigan 777 form involves several calculations to determine your Michigan tax on Canadian income. You will begin by reporting your adjusted gross income from your MI-1040. Then, you will subtract any U.S. adjustments to your Canadian wages. After calculating your Michigan source income, you will add any required additions and subtractions from your MI-1040. The final steps involve determining your taxable income and applying the Michigan tax rate of 4.2%. These calculations will help you understand your tax liability related to your Canadian income.

How do I claim the credit for taxes paid to a Canadian province?

To claim the credit for taxes paid to a Canadian province, you will need to complete Part 3 of the Michigan 777 form. This section requires you to calculate the Michigan tax on your Canadian province income and determine the total tax paid in Canada. You will also need to make adjustments based on the credit claimed on your U.S. 1040 form. Finally, you will enter the lesser of the calculated amounts to determine the credit for tax paid to the Canadian province. Ensure that you attach this form to your MI-1040 return when filing.

Incorrect Personal Information: Failing to accurately fill out your name, Social Security Number, and address can lead to processing delays or rejections.

Missing Tax Year: Forgetting to specify the tax year on the form can create confusion and may result in your submission being invalid.

Improper Currency Conversion: Miscalculating the conversion of Canadian wages and taxes to U.S. currency is a common mistake. Ensure you use the correct conversion rate of 67.40%.

Omitting Fringe Benefits: Not including fringe benefits from Box 14 of the T-4 can lead to an inaccurate income calculation.

Errors in Line Calculations: Simple math errors in any of the lines can throw off your entire submission. Double-check each calculation.

Neglecting U.S. Adjustments: Failing to account for U.S. adjustments to Canadian wages can result in an incorrect taxable income.

Ignoring Additions and Subtractions: Not properly adding or subtracting amounts from your MI-1040 can lead to misreporting your income subject to tax.

Incorrect Exemption Allowance: Miscalculating the exemption allowance can affect your taxable income and ultimately your tax liability.

Not Attaching the Form: Forgetting to attach the Michigan 777 form to your MI-1040 return can result in processing issues.

Failure to Review: Skipping a final review of the form before submission can lead to overlooked mistakes that may delay your tax return.

The Michigan 777 form is used to claim a credit for taxes imposed by a Canadian province on income that is also taxed by Michigan. When filing this form, there are several other documents that may be necessary to support your tax return. Below is a list of commonly used forms and documents that complement the Michigan 777 form.

Gathering these forms and documents can help ensure a smooth filing process when submitting your Michigan 777 form. Always check for the most current requirements and guidelines to ensure compliance with tax laws.

The Michigan 777 form is designed for claiming a credit for taxes imposed by a Canadian province. It has similarities to several other tax-related documents. Here are eight forms that share common features with the Michigan 777:

Each of these forms shares a common purpose of helping taxpayers navigate complex tax situations, ensuring that they receive the appropriate credits and deductions available to them.

When filling out the Michigan 777 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are five things you should do and five things you shouldn't do:

Understanding the Michigan 777 form can be challenging, and several misconceptions may lead to confusion. Here are seven common misunderstandings about this form:

By clarifying these misconceptions, taxpayers can better navigate the process and ensure compliance with Michigan tax regulations. Understanding the nuances of the Michigan 777 form is essential for accurate reporting and maximizing potential credits.

When filling out the Michigan 777 form, keep the following key points in mind: