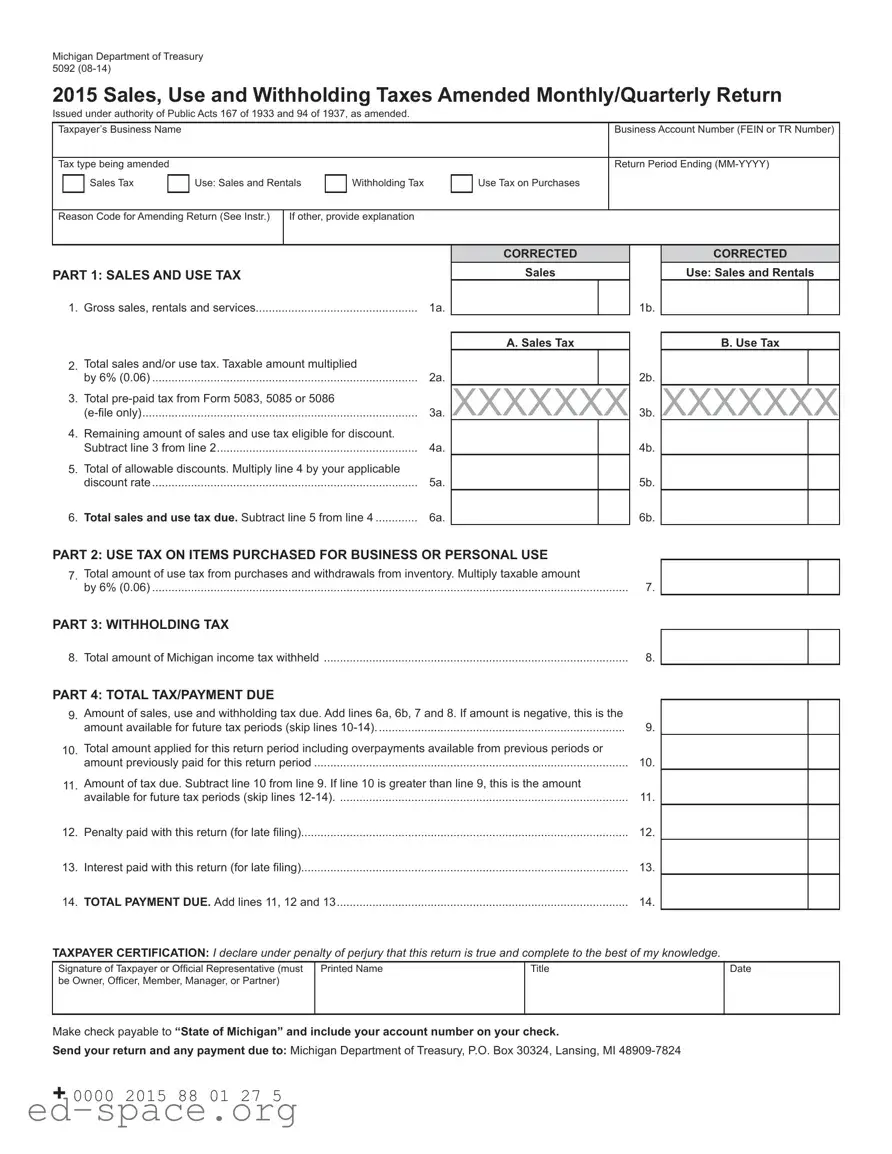

The Michigan 5092 form serves as a critical tool for businesses and individuals seeking to amend their sales, use, and withholding tax returns for specific monthly or quarterly periods. Issued by the Michigan Department of Treasury, this form is underpinned by the authority of public acts that date back to the 1930s. It allows taxpayers to correct previously submitted tax returns by providing updated figures and necessary explanations for the amendments. Key sections of the form include detailed calculations for gross sales, taxable amounts, and the corresponding tax due, which is calculated at a rate of 6%. Additionally, the form incorporates provisions for claiming allowable discounts, thereby incentivizing timely payments. Taxpayers must also indicate the reason for amending their returns, selecting from a predefined list of codes that cover scenarios such as increasing or decreasing tax liabilities and correcting erroneous information. The 5092 form not only facilitates compliance with tax obligations but also serves as a declaration of the taxpayer's commitment to accuracy and transparency, as it requires a certification under penalty of perjury. Understanding the intricacies of this form is essential for effective tax management and avoiding potential penalties associated with late filings or inaccuracies.

Michigan Department of Treasury 5092

2015 Sales, Use and Withholding Taxes Amended Monthly/Quarterly Return

Issued under authority of Public Acts 167 of 1933 and 94 of 1937, as amended.

Taxpayer’s Business Name |

|

|

|

|

|

Business Account Number (FEIN or TR Number) |

|||

|

|

|

|

|

|

|

|

|

|

Tax type being amended |

|

|

|

|

|

Return Period Ending |

|||

|

|

|

|

|

|

|

|

|

|

|

|

Sales Tax |

|

Use: Sales and Rentals |

|

Withholding Tax |

|

Use Tax on Purchases |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reason Code for Amending Return (See Instr.)

If other, provide explanation

PART 1: SAlES AnD USE TAx

1. Gross sales, rentals and services |

1a. |

CORRECTED

Sales

1b.

CORRECTED

Use: Sales and Rentals

2.Total sales and/or use tax. Taxable amount multiplied

by 6% (0.06) ..................................................................................

3.Total

4.Remaining amount of sales and use tax eligible for discount. Subtract line 3 from line 2..............................................................

5.Total of allowable discounts. Multiply line 4 by your applicable discount rate..................................................................................

6.Total sales and use tax due. Subtract line 5 from line 4 .............

2a.

3a.

4a.

5a.

6a.

A. Sales Tax

XXXXXXX

2b.

3b.

4b.

5b.

6b.

B. Use Tax

XXXXXXX

PART 2: USE TAx On ITEMS PURChASED fOR BUSInESS OR PERSOnAl USE

7. Total amount of use tax from purchases and withdrawals from inventory. Multiply taxable amount |

|

by 6% (0.06) |

7. |

PART 3: WIThhOlDIng TAx

8. Total amount of Michigan income tax withheld |

8. |

PART 4: TOTAl TAx/PAyMEnT DUE

9. |

Amount of sales, use and withholding tax due. Add lines 6a, 6b, 7 and 8. If amount is negative, this is the |

|

|

amount available for future tax periods (skip lines |

9. |

10. |

Total amount applied for this return period including overpayments available from previous periods or |

|

|

amount previously paid for this return period |

10. |

11. |

Amount of tax due. Subtract line 10 from line 9. If line 10 is greater than line 9, this is the amount |

|

|

available for future tax periods (skip lines |

11. |

12. |

Penalty paid with this return (for late iling) |

12. |

13. |

Interest paid with this return (for late iling) |

13. |

14. |

TOTAl PAyMEnT DUE. Add lines 11, 12 and 13 |

14. |

TAxPAyER CERTIfICATIOn: I declare under penalty of perjury that this return is true and complete to the best of my knowledge.

Signature of Taxpayer or Oficial Representative (must be Owner, Oficer, Member, Manager, or Partner)

Printed Name

Title

Date

Make check payable to “State of Michigan” and include your account number on your check.

Send your return and any payment due to: Michigan Department of Treasury, P.O. Box 30324, Lansing, MI

+ 0000 2015 88 01 27 5

Instructions for Sales, Use and Withholding Taxes Amended Monthly/Quarterly Return (form 5092)

NOTE: You must use Form 165 to amend tax years prior to 2015.

Form 5092 is used to amend monthly/quarterly periods in the current year. Complete the return with the corrected figures. Check the box for each tax type you are amending and provide the amended reason code located in the instructions. If the reason code is “Other,” write an explanation for the amendment.

IMPORTANT: This is a return for Sales Tax, Use Tax, and/ or Withholding Tax. If the taxpayer inserts a zero on (or leaves blank) any line for reporting Sales Tax, Use Tax, or Withholding Tax, the taxpayer is certifying that no tax is owed for that tax type. If it is determined that tax is owed, the taxpayer will be liable for the deficiency as well as penalty and interest.

Reason code for amending return: Using the table below, select the

01Increasing tax liability

02Decreasing tax liability

03Incorrect information/igures reported on original return

04Original return was missing information/incomplete

05Claiming previously unclaimed

06Dispute an adjustment

07Tax Exempt

08Other

PART 1: SAlES AnD USE TAx

Line 1a: Total gross sales for tax period being reported. Enter the total of your Michigan sales of tangible personal property including cash, credit and installment transactions and any costs incurred before ownership of the property is transferred to the buyer (including shipping, handling, and delivery charges).

Line 1b: This line is used to report the following:

•

•Lessors of tangible personal property: Enter amount of total rental receipts.

•Persons providing accommodations: This would include but not limited to hotel, motel, and vacation home rentals. This also includes assessments imposed under the Convention and Tourism Act, the Convention Facility Development Act, the Regional Tourism Marketing Act, the Community Convention or Tourism Marketing Act.

•Telecommunications Services: Enter gross income from telecommunications services.

Line 2a: Total sales tax. Negative figures are not allowed or valid.

Line 2b: Total use tax. Negative figures not allowed or valid.

Line 5: Enter total allowable discounts. Discounts apply only to 2/3 (0.6667) of the sales and/or use tax collected at the 6 percent tax rate. See below to calculate your discount based on filing frequency:

Monthly Filer

•If the tax is less than $9, calculate the discount by multiplying the tax by 2/3 (.6667).

•Enter $6 if tax is $9 to $1,200 and paid by the 12th, or $9 to $1,800 and paid by the 20th .

•If the tax is more than $1,200 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

•If the tax is more than $1,800 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Quarterly Filer

•If the tax is less than $27, calculate the discount by multiplying the tax by 2/3 (.6667)

•Enter $18 if tax is $27 to $3,600 and paid by the 12th, or $27 to $5,400 and paid by the 20th.

•If the tax is more than $3,600 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

•If the tax is more than $5,400 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Accelerated Filer

•If the tax is paid by the 12th, calculate discount using this formula: (Tax x .6667 x .0075).

•If the tax is paid by the 20th, calculate discount using this formula: (Tax x .6667 x .005).

PART 2: USE TAx On ITEMS PURChASED fOR BUSInESS OR PERSOnAl USE

Line 7: To determine your use tax due from purchases and withdrawals, multiply the total amount of your inventory value by 6% (0.06) and enter here.

PART 3: WIThhOlDIng TAx

Line 8: Enter the total Michigan income tax withheld for the tax period.

PART 4: TOTAl TAx/PAyMEnT DUE

Line 9: If amount is negative, this is the amount available for

future tax periods (skip lines

Line 10: Enter any payments you submitted for this period, enter any payments for this period including any overpayments available from previous periods. If you are using an overpayment from a previous period only enter the amount needed to pay the total liability for this return. In the event an overpayment still exists declare it on the next return you file with a liability. (Liability minus overpayments/prior payment for this period must be greater than or equal to zero).

how to Compute Penalty and Interest

If your return is filed with additional tax due, include penalty and interest with your payment. Penalty is 5% of the tax due and increases by an additional 5% per month or fraction thereof, after the second month, to a maximum of 25%. Interest is charged daily using the average prime rate, plus 1 percent.

Refer to www.michigan.gov/taxes for current interest rate information or help in calculating late payment fees.

| Fact Name | Details |

|---|---|

| Form Purpose | The Michigan 5092 form is used to amend monthly or quarterly returns for Sales, Use, and Withholding Taxes. |

| Governing Laws | This form is issued under the authority of Public Acts 167 of 1933 and 94 of 1937, as amended. |

| Tax Types | It addresses Sales Tax, Use Tax, and Withholding Tax. Taxpayers must specify which type they are amending. |

| Amendment Reason Codes | Taxpayers must provide a reason code for the amendment, which can include increasing or decreasing tax liability. |

| Discount Eligibility | Taxpayers may be eligible for discounts on sales and use tax, depending on their filing frequency and the amount due. |

| Filing Frequency | The form can be used for monthly or quarterly filings, and specific calculations apply based on the frequency. |

| Penalties for Late Filing | Late filing incurs penalties starting at 5% of the tax due, which increases monthly, up to a maximum of 25%. |

| Submission Instructions | Returns and payments should be sent to the Michigan Department of Treasury, P.O. Box 30324, Lansing, MI 48909-7824. |

Completing the Michigan 5092 form requires careful attention to detail. This form is essential for amending sales, use, and withholding tax returns for the specified period. Once the form is filled out, it must be submitted along with any payment due to the Michigan Department of Treasury.

For Part 1, Sales and Use Tax:

For Part 2, Use Tax on Items Purchased for Business or Personal Use:

For Part 3, Withholding Tax:

For Part 4, Total Tax/Payment Due:

Finally, sign the form in the Taxpayer Certification section, providing your printed name, title, and date. Ensure that payment is made out to "State of Michigan," and include your account number on the check. Submit the completed form and payment to the Michigan Department of Treasury at the specified address.

What is the Michigan 5092 form used for?

The Michigan 5092 form is used to amend monthly or quarterly returns for sales, use, and withholding taxes. If a taxpayer needs to correct previous tax filings for the current year, this form is the appropriate document to use. It allows for adjustments to be made to sales tax, use tax, and withholding tax amounts reported earlier.

Who needs to file the Michigan 5092 form?

Any business or individual who has previously submitted a sales, use, or withholding tax return in Michigan and needs to make corrections should file the Michigan 5092 form. This includes those who may have discovered errors in their reported figures or wish to claim previously unreported tax credits.

What information is required on the Michigan 5092 form?

When filling out the form, you will need to provide your business name, account number, the tax type being amended, and the return period ending date. Additionally, you must report corrected figures for gross sales, total tax, and any discounts. If you are amending for a specific reason, you must select a reason code and provide an explanation if necessary.

How do I calculate the total tax due on the Michigan 5092 form?

To calculate the total tax due, you need to add together the amounts from several lines on the form. This includes sales and use tax amounts and any withholding tax. If you have any allowable discounts, subtract those from the total tax calculated. If your total tax due is negative, this indicates an amount available for future tax periods.

What happens if I file the Michigan 5092 form late?

If you file the form late and owe additional tax, you will incur penalties and interest. The penalty starts at 5% of the tax due and increases by an additional 5% for each month it remains unpaid, up to a maximum of 25%. Interest is also charged daily based on the average prime rate plus 1%. This can add up quickly, so timely filing is crucial.

Can I use the Michigan 5092 form to amend returns from prior years?

No, the Michigan 5092 form is only for amending returns from the current year. If you need to amend tax returns from years prior to 2015, you must use Form 165. It is essential to use the correct form for the correct tax year to ensure compliance with Michigan tax laws.

Where do I send my completed Michigan 5092 form?

Once you have completed the Michigan 5092 form, you should mail it along with any payment due to the Michigan Department of Treasury at P.O. Box 30324, Lansing, MI 48909-7824. Be sure to include your account number on your payment to ensure it is processed correctly.

Failing to include the Taxpayer’s Business Name and Business Account Number. This information is crucial for processing the return correctly.

Leaving the Return Period Ending date blank or incorrectly filled. This can lead to confusion about which tax period the return applies to.

Not selecting the correct Tax type being amended. Ensure you check the appropriate box for Sales Tax, Use Tax, or Withholding Tax.

Incorrectly calculating the Total sales and/or use tax. Make sure to multiply the taxable amount by 6% accurately.

Omitting the Reason Code for Amending Return. This code is essential for the processing of the amendment.

Reporting negative figures on lines where they are not allowed, such as Total sales tax or Total use tax. Negative amounts can lead to rejection of the return.

Forgetting to calculate allowable discounts correctly. Discounts apply only to a portion of the tax collected, so ensure calculations are accurate.

Not signing the return. The Taxpayer Certification requires a signature from the taxpayer or an official representative.

Neglecting to include any penalty or interest due with the return. This can lead to additional fees and complications.

Sending the return and payment to the wrong address. Always verify the correct mailing address to avoid delays.

The Michigan 5092 form is an essential document for businesses needing to amend their sales, use, and withholding tax returns. In addition to this form, several other documents may be required to ensure compliance with state tax regulations. Below is a brief overview of these related forms and documents.

Understanding these forms and documents is vital for businesses navigating the complexities of tax amendments in Michigan. Each plays a unique role in ensuring compliance and accuracy in tax reporting. By being diligent in completing these forms, taxpayers can avoid potential penalties and ensure their tax obligations are met effectively.

The Michigan 5092 form serves as an amended return for sales, use, and withholding taxes. Several other documents share similarities with this form in terms of purpose and structure. Here are four such documents:

When filling out the Michigan 5092 form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do.

Understanding the Michigan 5092 form can be challenging. Here are four common misconceptions about this important tax document.

This is incorrect. The Michigan 5092 form is specifically designed to amend monthly or quarterly tax returns for the current year only. For tax years prior to 2015, taxpayers must use Form 165.

While it may seem straightforward, entering a zero or leaving a line blank certifies that no tax is owed for that category. If it is later determined that tax is owed, the taxpayer may face penalties and interest for the deficiency.

Discounts are not a one-size-fits-all solution. They vary based on the filing frequency and specific conditions. Taxpayers must calculate discounts according to established formulas that depend on the amount of tax due and the payment date.

This is misleading. Taxpayers must provide a reason code for any amendments made on the form. Failure to do so could lead to complications and may delay processing.

Key Takeaways for Filling Out and Using the Michigan 5092 Form:

Following these guidelines will help ensure that your form is completed correctly and submitted on time. Be proactive in addressing any issues to avoid penalties.