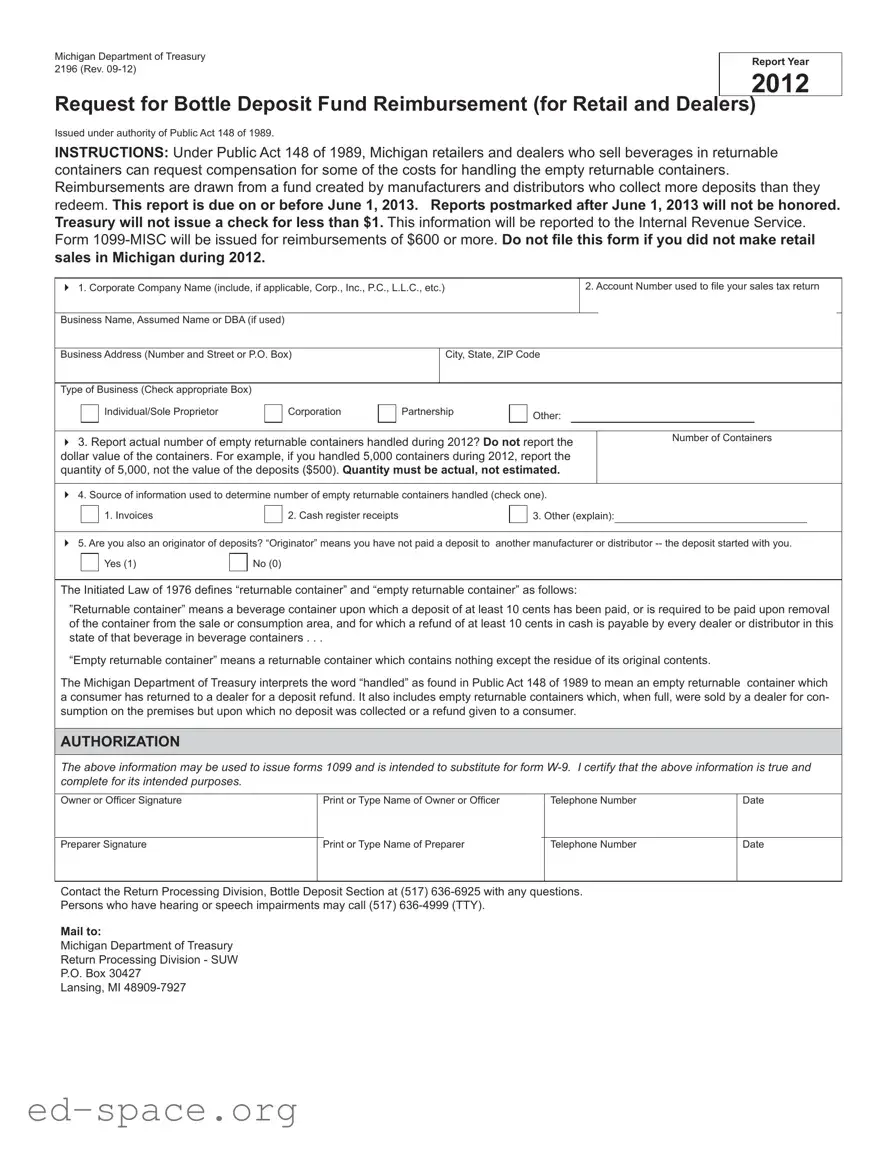

The Michigan 2196 form serves as a critical tool for retailers and dealers involved in the sale of beverages in returnable containers. This form allows these businesses to request reimbursement for the costs associated with handling empty returnable containers, as outlined in Public Act 148 of 1989. The reimbursement process is funded by manufacturers and distributors who collect more deposits than they redeem. To qualify, businesses must report the actual number of empty returnable containers they handled during the previous year, without estimating values. The form requires essential details such as the business name, account number, and type of business, ensuring accurate processing. It is important to note that the form must be submitted by June 1, 2013, and late submissions will not be accepted. Additionally, reimbursements under $1 will not be issued, and amounts of $600 or more will necessitate the issuance of a 1099-MISC form for tax purposes. For those who did not engage in retail sales in Michigan during the reporting year, filing the form is unnecessary. Understanding these requirements can help businesses navigate the reimbursement process effectively and ensure compliance with state regulations.

Michigan Department of Treasury |

Report Year |

|

2196 (Rev. |

||

2012 |

||

|

Request for Bottle Deposit Fund Reimbursement (for Retail and Dealers)

Issued under authority of Public Act 148 of 1989.

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers. Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem. This report is due on or before June 1, 2013. Reports postmarked after June 1, 2013 will not be honored. Treasury will not issue a check for less than $1. This information will be reported to the Internal Revenue Service. Form

1. Corporate Company Name (include, if applicable, Corp., Inc., P.C., L.L.C., etc.) |

|

|

|

|

2. Account Number used to fi le your sales tax return |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Name, Assumed Name or DBA (if used) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Business Address (Number and Street or P.O. Box) |

|

City, State, ZIP Code |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Business (Check appropriate Box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Individual/Sole Proprietor |

|

|

Corporation |

|

|

Partnership |

|

|

Other: |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Report actual number of empty returnable containers handled during 2012? Do not report the |

|

|

Number of Containers |

||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||

dollar value of the containers. For example, if you handled 5,000 containers during 2012, report the |

|

|

|

|

|

|

|||||||||||||||

quantity of 5,000, not the value of the deposits ($500). Quantity must be actual, not estimated. |

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4. Source of information used to determine number of empty returnable containers handled (check one). |

|

|

|

|

|

|

|||||||||||||||

|

|

1. Invoices |

|

|

2. Cash register receipts |

|

|

|

|

3. Other (explain): |

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

||||||||||||||||

5. Are you also an originator of deposits? “Originator” means you have not paid a deposit to |

another manufacturer or distributor |

||||||||||||||||||||

|

|

Yes (1) |

|

|

No (0) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

The Initiated Law of 1976 defi nes “returnable container” and “empty returnable container” as follows:

”Returnable container” means a beverage container upon which a deposit of at least 10 cents has been paid, or is required to be paid upon removal of the container from the sale or consumption area, and for which a refund of at least 10 cents in cash is payable by every dealer or distributor in this state of that beverage in beverage containers . . .

“Empty returnable container” means a returnable container which contains nothing except the residue of its original contents.

The Michigan Department of Treasury interprets the word “handled” as found in Public Act 148 of 1989 to mean an empty returnable container which a consumer has returned to a dealer for a deposit refund. It also includes empty returnable containers which, when full, were sold by a dealer for con- sumption on the premises but upon which no deposit was collected or a refund given to a consumer.

AUTHORIZATION

The above information may be used to issue forms 1099 and is intended to substitute for form

Owner or Offi cer Signature |

|

Print or Type Name of Owner or Officer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer Signature |

|

Print or Type Name of Preparer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact the Return Processing Division, Bottle Deposit Section at (517)

Persons who have hearing or speech impairments may call (517)

Mail to:

Michigan Department of Treasury

Return Processing Division - SUW

P.O. Box 30427

Lansing, MI

Bottle Deposit Fund Reimbursement Availability

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers.

Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem.

The payment is based on the number of empty returnable containers handled in a calendar year. Payment amounts will be known after Treasury determines how much money is available.

To apply, you must complete and mail a Request for Bottle Deposit Fund Reimbursement (Form 2196) to Treasury. Form 2196 is due on or before June 1, 2013. Use Form 2196 or contact Return Processing Division, Bottle Deposit Section, at (517)

Treasury will begin issuing checks after August 1.

| Fact Name | Details |

|---|---|

| Form Title | Request for Bottle Deposit Fund Reimbursement (for Retail and Dealers) |

| Governing Law | Issued under authority of Public Act 148 of 1989 |

| Eligibility | Michigan retailers and dealers selling beverages in returnable containers can apply for reimbursement. |

| Reimbursement Source | Funds are drawn from deposits collected by manufacturers and distributors that exceed the amount redeemed. |

| Submission Deadline | The report must be postmarked by June 1, 2013, to be honored. |

| Minimum Reimbursement | Treasury will not issue checks for amounts less than $1. |

| IRS Reporting | Reimbursements of $600 or more will be reported to the IRS via Form 1099-MISC. |

| Information Requirement | Actual number of empty returnable containers handled must be reported, not the dollar value. |

| Contact Information | For questions, contact the Return Processing Division, Bottle Deposit Section at (517) 636-6925. |

After completing the Michigan 2196 form, it must be mailed to the Michigan Department of Treasury by the deadline. Ensure all information is accurate to avoid delays in processing. Keep a copy for your records.

What is the Michigan 2196 form?

The Michigan 2196 form, officially titled "Request for Bottle Deposit Fund Reimbursement," is a document that Michigan retailers and dealers must complete to request compensation for handling empty returnable containers. This form is issued under Public Act 148 of 1989 and is intended for businesses that sell beverages in returnable containers. The reimbursements come from a fund established by manufacturers and distributors who collect more deposits than they redeem.

Who is eligible to file the Michigan 2196 form?

Eligibility to file the Michigan 2196 form is limited to retailers and dealers who sold beverages in returnable containers during the specified reporting year. If your business did not make retail sales in Michigan during that year, you should not file this form. It's important to ensure that you meet the criteria before completing the application.

When is the Michigan 2196 form due?

The completed Michigan 2196 form must be submitted by June 1, 2013. It is crucial to postmark your form by this deadline, as any reports submitted after June 1 will not be honored. This deadline is strictly enforced, so planning ahead is advisable to avoid any complications.

What information do I need to provide on the form?

The form requires several pieces of information, including your corporate name, account number for sales tax, business address, and type of business. Additionally, you will need to report the actual number of empty returnable containers you handled during the year and indicate the source of this information, such as invoices or cash register receipts. Accurate reporting is essential, as estimates are not accepted.

What happens if I submit a reimbursement request for less than $1?

The Michigan Department of Treasury will not issue a check for any reimbursement amount that is less than $1. Therefore, it is important to ensure that your claim meets this minimum threshold. If your total reimbursement request falls below this amount, it may be more beneficial to wait until you have a larger claim before submitting your request.

Will I receive a tax form for my reimbursement?

Yes, if your total reimbursement is $600 or more, the Treasury will issue a Form 1099-MISC for tax purposes. This form will be reported to the Internal Revenue Service, so it is important to keep accurate records of your reimbursements for your tax filings.

Who can I contact if I have questions about the Michigan 2196 form?

If you have any questions regarding the Michigan 2196 form or the reimbursement process, you can contact the Return Processing Division, Bottle Deposit Section at (517) 636-6925. For individuals with hearing or speech impairments, a TTY service is available at (517) 636-4999. They can provide assistance and clarify any uncertainties you may have.

Failing to include the correct corporate company name. Make sure to add any applicable designations such as Corp., Inc., or LLC.

Not providing the Account Number used for filing your sales tax return. This information is crucial for processing your request.

Omitting the business address. Ensure that the address is complete, including the city, state, and ZIP code.

Incorrectly reporting the number of empty returnable containers. Only report the actual quantity handled, not the monetary value.

Failing to check the source of information used to determine the number of containers handled. Select one option and provide additional details if necessary.

Not indicating whether you are an originator of deposits. This is essential to determine your eligibility for reimbursement.

Ignoring the deadline. The report must be postmarked by June 1, 2013, or it will not be honored.

Neglecting to sign the form. Both the owner or officer and the preparer must provide their signatures.

Not providing a telephone number for follow-up. This information is important for any necessary communication regarding your submission.

The Michigan 2196 form is essential for retailers and dealers seeking reimbursement for handling empty returnable containers. Alongside this form, several other documents may be necessary to ensure compliance and facilitate the reimbursement process. Below is a list of related forms and documents that are commonly used in conjunction with the Michigan 2196 form.

By gathering these documents, retailers and dealers can streamline their reimbursement requests and ensure compliance with Michigan's regulations. Always keep copies of all submitted forms and correspondence for your records.

When filling out the Michigan 2196 form, it is essential to follow specific guidelines to ensure your application is processed correctly. Below is a list of things you should and shouldn't do during this process.

By adhering to these guidelines, you can increase the likelihood of a smooth reimbursement process. If you have any questions, consider reaching out to the Return Processing Division for assistance.

Misconceptions about the Michigan 2196 form can lead to confusion among retailers and dealers. Here are eight common misunderstandings clarified:

Understanding these misconceptions can help retailers and dealers navigate the reimbursement process more effectively.

Filling out the Michigan 2196 form is a crucial step for retailers and dealers who handle returnable beverage containers. Here are some key takeaways to keep in mind:

Following these guidelines will help ensure that your request for reimbursement is processed smoothly and efficiently.