The Michigan 1028 form, officially known as the Annual Property Report, plays a crucial role for companies operating within the state, particularly railroads. This form is mandated under Michigan Public Act 282 of 1905, and its timely filing is essential for compliance with state tax regulations. Companies must be aware of the deadlines: those with annual gross receipts exceeding $1,000,000 must submit their reports by March 31, while those with lower gross receipts have a slightly earlier deadline of March 15. Failure to file on time can result in significant penalties, accumulating at $500 per day. The form requires detailed information about the company, including its name, address, and authorized contact person. It also includes schedules that cover various aspects of the company’s operations, such as the total cost of rolling stock, investment in road property, and railcar mileage. Additionally, companies must disclose any changes in ownership or significant financial activities from the previous year. This report not only helps the state assess property values but also ensures that companies remain accountable for their operations within Michigan. Understanding the nuances of the Michigan 1028 form is vital for compliance and effective financial planning.

1028 (Rev.

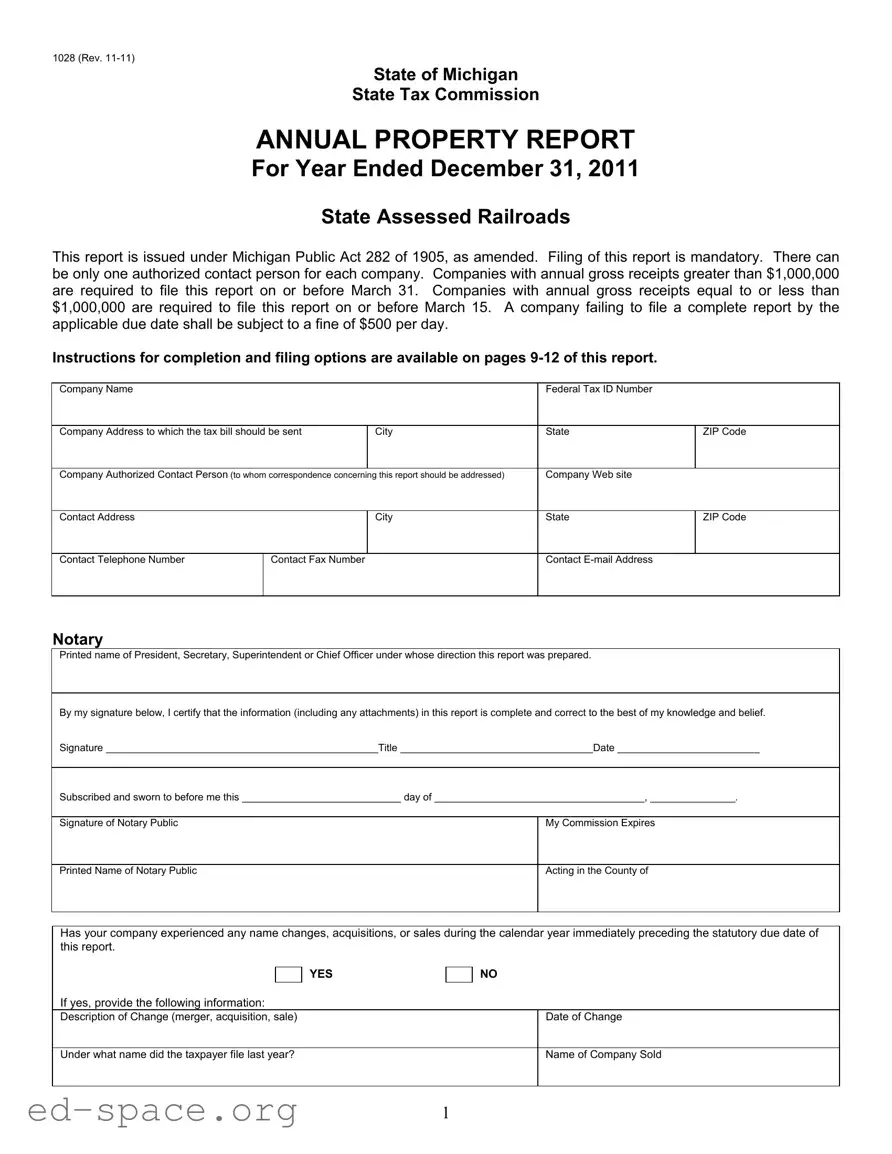

State of Michigan

State Tax Commission

ANNUAL PROPERTY REPORT

For Year Ended December 31, 2011

State Assessed Railroads

This report is issued under Michigan Public Act 282 of 1905, as amended. Filing of this report is mandatory. There can be only one authorized contact person for each company. Companies with annual gross receipts greater than $1,000,000 are required to file this report on or before March 31. Companies with annual gross receipts equal to or less than $1,000,000 are required to file this report on or before March 15. A company failing to file a complete report by the applicable due date shall be subject to a fine of $500 per day.

Instructions for completion and filing options are available on pages

Company Name |

|

|

Federal Tax ID Number |

|

|

|

|

|

|

Company Address to which the tax bill should be sent |

City |

State |

ZIP Code |

|

|

|

|

|

|

Company Authorized Contact Person (to whom correspondence concerning this report should be addressed) |

Company Web site |

|

||

|

|

|

|

|

Contact Address |

|

City |

State |

ZIP Code |

|

|

|

|

|

Contact Telephone Number |

Contact Fax Number |

|

Contact |

|

|

|

|

|

|

Notary

Printed name of President, Secretary, Superintendent or Chief Officer under whose direction this report was prepared.

By my signature below, I certify that the information (including any attachments) in this report is complete and correct to the best of my knowledge and belief.

Signature ________________________________________________Title __________________________________Date _________________________

Subscribed and sworn to before me this ____________________________ day of _____________________________________, _______________.

Signature of Notary Public |

My Commission Expires |

Printed Name of Notary Public

Acting in the County of

Has your company experienced any name changes, acquisitions, or sales during the calendar year immediately preceding the statutory due date of this report.

YES

If yes, provide the following information:

NO

Description of Change (merger, acquisition, sale)

Date of Change

Under what name did the taxpayer file last year?

Name of Company Sold

1

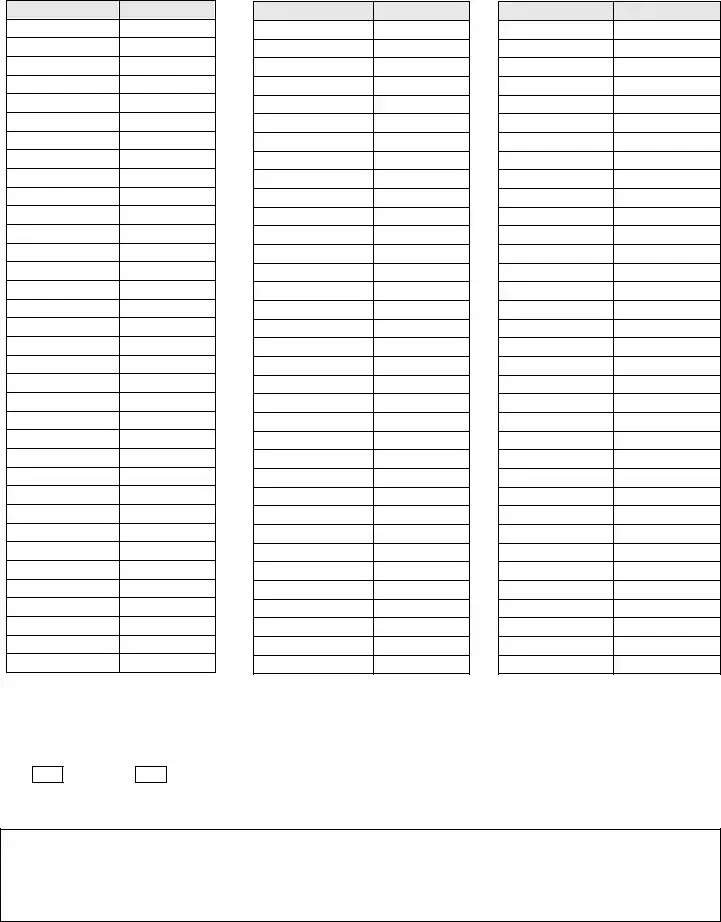

Schedule 1, Statement of Total Cost of Rolling Stock Owned or Leased by Year of Acquisition (Includes Locomotives, Freight Cars, Passenger Cars, Highway and Work Equipment)

|

|

|

|

|

|

|

|

TRUE |

|

|

|

|

|

|

|

|

CASH |

|

No. of |

COSTS |

|

|

|

REPORTABLE |

|

VALUE |

YEAR OF |

Units |

REPORTED |

LOSSES |

ADDITIONS |

|

COSTS |

|

(office |

ACQUISITION |

Reported |

PRIOR |

(office use |

(office use |

NO. OF |

CURRENT |

|

use |

|

Prior Year |

YEAR |

only) |

only) |

UNITS |

YEAR |

MULTIPLIER |

only) |

|

|

(office use) |

|

|

|

|

|

|

2011 |

|

|

|

|

|

|

0.8900 |

|

2010 |

|

|

|

|

|

|

0.7600 |

|

2009 |

|

|

|

|

|

|

0.6700 |

|

2008 |

|

|

|

|

|

|

0.6000 |

|

2007 |

|

|

|

|

|

|

0.5400 |

|

2006 |

|

|

|

|

|

|

0.4900 |

|

2005 |

|

|

|

|

|

|

0.4500 |

|

2004 |

|

|

|

|

|

|

0.4200 |

|

2003 |

|

|

|

|

|

|

0.3800 |

|

2002 |

|

|

|

|

|

|

0.3600 |

|

2001 |

|

|

|

|

|

|

0.3300 |

|

2000 |

|

|

|

|

|

|

0.3100 |

|

1999 |

|

|

|

|

|

|

0.2900 |

|

1998 |

|

|

|

|

|

|

0.2800 |

|

Prior |

|

|

|

|

|

|

0.2300 |

|

TOTALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule 1 Total True Cash Value

Schedule 2, Investment in Road Property Used in Transportation Service with Additions and Retirements for the Year (Michigan Only)

Column A |

Column B |

Column C |

Column D |

Column E |

Column F |

Column G |

Column H |

Previous |

Original Cost |

Accumulated |

Expenditures for |

Depreciation |

Plant Balance |

Accumulated |

Net Book Value |

Year |

of |

Depreciation of |

Additions During |

of New Additions |

at Year End |

Depreciation |

= F - G |

Plant Balance |

Retirements |

Retirements at |

the Calendar |

During the |

= A - B + D |

at Year End |

|

from last |

Made During |

Beginning of |

Year |

Calendar Year |

|

|

|

Year’s |

Calendar |

Calendar Year |

|

|

|

|

|

Column F |

Year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If your prior year plant ending balance is not equivalent to the amount in Column A that was carried forward from last year’s report, please indicate the revised amount and provide an explanation.

Revised Column A: _________

Explanation: |

_______ |

_ |

_ |

|

|

|

plus |

Construction in Progress (CIP) |

x .50 = Adjusted CIP |

||

|

_________ |

|

|

(incurred cost to date) |

equals |

||

_________

Schedule 2 True Cash Value

_________

Note: Inventory is exempt from assessment. Inventory does not include personal property under lease or principally intended for lease or rental (operating), rather than sale. Property allowed a cost recovery allowance or depreciation under the Internal Revenue Code is not inventory. Motor vehicles registered with the Michigan Secretary of State on Tax Day (December 31st) are exempt.

2

Schedule 3

A. Interest Paid on Debt From Railway Operations (National)

|

Last Four Year Results as Previously Reported |

|

|

Balance at Close of |

|

|

|

|

||||

|

|

|

Calendar Year |

|

|

Five Year Average |

|

|||||

|

|

|

(office use only) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

(December 31st) |

|

|||||

|

|

|

|

|

|

|

|

|

|

(office use only) |

|

|

|

year - 4 |

|

year - 3 |

year - 2 |

year - 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

B. Total Net Operating from Railway Operations (National)

Last Four Year Results as Previously Reported

(office use only)

year - 4 |

year - 3 |

year - 2 |

year - 1 |

|

|

|

|

Balance at Close of

Calendar Year

(December 31st)

Five Year Average

(office use only)

Schedule 4, Statement of Allocation Factors

Note: "National" includes all North American Activity (U.S., Canada, and Mexico), "Michigan" only includes those items attributable to the State of Michigan.

|

Ar e y ou r op e r a t ion s e n t ir e ly w it h in t h e St a t e of M ich ig a n ? |

|

|

|||||||

|

Yes |

_ _ _ |

|

No |

_ _ _ |

|

|

|

|

|

|

I f Yes, y ou do not need t o pr ov ide t he follow ing in for m at ion . |

|

|

|||||||

|

I f No, please pr ov ide t he follow in g in for m at ion below ( Car Miles an d Rev en u es) . |

|

||||||||

|

Car Miles |

|

|

|

|

National |

Michigan |

|||

|

1. |

Freight Car Miles (Loaded and Empty) |

|

|

|

|||||

|

2. |

All Other Car Miles |

|

|

|

|

|

|

||

|

3. |

Total Car Miles (1+2) |

|

|

|

|

|

|

||

|

4. |

Percentage Attributable to Michigan |

|

|

|

|||||

|

Revenues (please enter full dollar amounts) |

National |

Michigan |

|||||||

|

1. |

Freight Revenue |

|

|

|

|

|

|

||

|

2. |

All Other Revenue from Operation |

|

|

|

|||||

|

3. |

Total Operating Revenue (1+2) |

|

|

|

|||||

|

4. |

Percentage Attributable to Michigan |

|

|

|

|||||

Schedule 5, Sales and Transfers of Car Marks

Did any sales or transfers of car marks occur during the calendar year immediately preceding the statutory due date of this report?

Yes |

____ |

No |

____ |

If Yes, describe any sales or transfers that occurred.

__________________________________________________________________________________

__________________________________________________________________________________

__________________________________________________________________________________

__________________________________________________________________________________

3

Schedule 6, Statement of Railcar Mileage Traveled Over Track Operated by your Company (itemize by Car Mark)

Car Mark

Mileage

Car Mark

Mileage

Car Mark

Mileage

Schedule 7, Real Property

Have there been any changes (additions or losses) to your Real Property in the calendar year immediately preceding the statutory filing date of this report?

Yes ____

No ____

If yes, please describe losses and/or additions in box below:

4

NOTE

All summary calculations will be completed AFTER the Assessment and Certification Division has reviewed and processed the information contained in this Annual Property Report. Once all processing is complete, you may view the summary calculations (worksheets) by requesting a personal identification number (PIN) and accessing your company's secure, online account. For additional information on how to request a PIN to access your account, please refer to the "How to file this report" section of the instructions.

Tentative values will be posted on or about May 15, and final values will be posted on or about June 15. Each state assessed company will receive a final tax bill by mail and any taxes due are payable on July 1.

5

2012

Application for Tax Credit for Maintenance and Improvement of Rights of Way

Section 13 of PA 282 of 1905, as amended allows credit for eligible expenses incurred in the State of Michigan by railroad companies for maintenance or improvement of rights of way, including those items, except depreciation, in the official

Eligibility Requirements

In order to be eligible for the tax credit for maintenance and improvement of rights of way under MCL 207.13(2), the railroad companies must fulfill the statutory requirements detailed in Section 13 of PA 282 of 1905 (MCL 207.13(3)). In addition to providing the requested summary information on this application for credit, each company must complete and file [3 copies of] the report described in Section 13 with the State Tax Commission that includes, but is not limited to, detailed information of the nature and location of expenses. A summary of the eligibility and reporting requirements are listed in the attached instructions on pages

Eligible and

Examples of Eligible and

Maximum Credit Available

The maintenance of way expense credits are not refundable or deferrable. Expenses in excess of a company's property tax liability are not eligible for credit against prior or subsequent years' liability.

***NOTE*** Filing of this credit application does not relieve the company of the statutory requirement of filing [3 copies] of the detailed expense report described in Section 13(3). You are still required to provide that to the State Tax Commission at the following address:

|

|

Mailing Address: |

For Overnight Package Delivery: |

Michigan Department of Treasury |

Michigan Department of Treasury |

Michigan State Tax Commission |

Michigan State Tax Commission |

P O Box 30471 |

Austin Building |

Lansing, MI |

430 W. Allegan Street |

|

Lansing, MI 48922 |

|

|

Company Name

Eligibilty

Has your company incurred eligible expenses, and submitted three (3) copies of the required expense report as described above?

Yes ___

No ___

If Yes, please enter total eligible expenses below.

If No, you are NOT ELIGIBLE for credit. DO NOT SUBMIT EXPENSES.

Total Eligible Expenses for Maintenance and Improvement of Rights of Way in Michigan which you have reported in the above described report.

$

___________________________

6

2012

Application for Tax Credit for Maintenance and Improvement

of Qualified Rolling Stock in Michigan

Section 13a of Public Act 282 of 1905, as amended, allows a credit for eligible expenses incurred in the State of Michigan by railroad and car companies for maintenance or improvement of eligible companies' qualified rolling stock.

Eligible Company is defined as:

Railroad companies, union station and depot companies, sleeping car companies, express companies, car loaning companies, stock car companies, refrigerator car companies, fast freight line companies, and all other companies owning, leasing, running, or operating any freight, stock, refrigerator, or any other cars not the exclusive property of a railroad company paying taxes upon its rolling stock under this act, over or upon the line or lines of any railroad in this state.

Eligible Expenses are expenses for repairs and maintenance that satisfy all of the following criteria:

1.Eligible expenses must have been incurred during the calendar year immediately preceding the statutory due date of this report.

2.Eligible expenses must have been incurred in the State of Michigan.

3.Eligible expenses must be made for the maintenance or improvement of rolling stock which are subject to taxation by the State under PA 282 of 1905 as amended.

Examples of Eligible and

Maximum Credit Available:

This credit is not refundable or deferrable. Expenses in excess of a company's property tax liability are not eligible for credit against prior or subsequent years' liability.

Company Name

Eligibility

Are you an "eligible company" which has incurred expenses that satisfy ALL of the requirements listed above?

Yes ___

No ___

If Yes, please enter total eligible expenses below.

If No, you are NOT ELIGIBLE for credit. DO NOT SUBMIT EXPENSES.

Total Eligible Expenses for Maintenance and Improvement of Qualified Rolling Stock in Michigan (include labor, material, overhead, and payments to others for work done).

$

7

Instructions for Completion of the Annual Report by State Assessed Railroads

Who must file this report? (MCL 207.6)

All railroad companies, union station and depot companies, and switching and terminal companies operating in the State of Michigan pursuant to Section 6 of PA 282 of 1905.

When is this report due? (MCL 207.6)

If your annual gross receipts exceed $1,000,000, this report is due by March 31st.

If your annual gross receipts do not exceed $1,000,000, this report is due by March 15th.

How to submit this report:

This report may be submitted electronically or mailed in paper format. If you wish to submit this form electronically, please visit the following web site at www.michigan.gov/stateassessedproperty or you may call (517)

If submitting this form by mail, please complete and sign the declaration on page one and send the entire completed form to:

Mailing Address: |

For Overnight Package Delivery: |

Michigan Department of Treasury |

Michigan Department of Treasury |

Michigan State Tax Commission |

Michigan State Tax Commission |

P O Box 30471 |

Austin Building |

Lansing, MI |

430 W. Allegan Street |

|

Lansing, MI 48922 |

What property is subject to taxation? (MCL 207.5)

The term "property having a situs in this state", includes all property, real and personal, of the persons, corporations, companies,

Schedule 1

List all rolling stock which is owned or leased by you. List the number of units reported as well as reportable current year costs. Property must be listed at its full original cost new, in the year that it was new. If the original/new acquisition cost of a railcar that was initially purchased by another company can be obtained, that information must be reported. If the original/new acquisition cost of a railcar that was initially purchased by another company cannot be obtained, then the original/new acquisition cost shall be equal to the subsequent price paid by the reporting company upon acquiring the used railcar. All betterments, including capital improvements, mandated betterments, capital upgrades, safety features, and mandated repairs should be reported in the year the expenditure is booked as a fixed asset.

The "Costs Reported Prior Year", "Losses", "Additions", and "True Cash Value" columns are for Assessment and Certification Division (ACD) use only. To view the values and calculations entered by the Assessment and Certification Division, please fill out form 4435 to obtain a Personal Identification Number (PIN) for access to the online reporting form available at www.michigan.gov/taxes (please see "How to submit this report" section above for specific website location). Tentative Values will be electronically posted on or about May 15th, and Final Values will be electronically posted on or about June 15th.

Schedule 2

This is to be submitted by all railroads and calls for summary data relating to investment for the company(s) properties in Michigan. Investment in account 732 (improvements on leased property) shall also be reported on Schedule 2. The "Previous Year Plant Balance" column is for Assessment and Certification Division office use only. List any retirements that have occurred during the calendar year immediately preceding the statutory due date of this report. List the accumulated depreciation for those retirements in the column designated.

8

List any expenditures for additions that occurred during the calendar year immediately preceding the statutory due date of this report. Exclude

In the Accumulated Depreciation column, list the accumulated depreciation for assets in place at year end.

List the balance of costs at calendar year end (December 31st). The "True Cash Value" column is for Assessment and Certification division office use only.

List the current year construction in progress. Report all costs that have been incurred including overheads, installation costs incurred, sales tax and freight. Reporting of costs should be separated by project. Property which is placed in service on or before December 31st is considered placed in service that year and should be entirely reported on the line which represents the year that it was considered placed in service. Similarly, the cost of all assets must be reported as acquired in the year that they were placed in service, rather than the year of purchase, if those years differ. The adjusted construction in progress and the Schedule 2 True Cash Value will be calculated by the Assessment and Certification Division.

Schedule 3

A.Enter the Total Interest Paid to service debt to finance railway operations. Interest must be for short term and long term debt. The columns provide for the amounts from the last four years. The

B.Enter the Total Net Operating Income from Railway Operations. The columns provide for the amounts reported from the last four years.

Schedule 4

If your company's property (whether owned or leased) is used entirely within the State of Michigan, you are not required to provide allocation information. If your company's property (whether owned or leased) is used partly within and partly without the State of Michigan, provide the allocation information based on the system as a whole, and the portion attributable to Michigan. For further details on reporting specifications, consult the Uniform System of Accounts for Railroad Companies. (49 CFR 1201 et.seq.)

Schedule 5

Please check the appropriate box indicating whether any sales or transfers of car marks have occurred in the calendar year immediately preceding the statutory due date of this report. If you select yes, please describe any sales and transfers of car marks that occurred.

Schedule 6

Enter the total annual mileage traveled during the calendar year immediately preceding the statutory due date of this report, over track that you operate (whether owned or leased). Please provide the mileage by individual car mark.

Schedule 7

Indicate whether there have been any changes to your real property as compared to the prior year’s information and provide information about any changes in the reporting box.

Losses to Real Property

Losses mean the decrease in value which has not been reflected in the assessment unit’s immediately preceding year’s assessment roll. Losses include removal or destruction of real property, newly exempt property, or newly contaminated property.

Additions to Real Property

Additions mean an increase in value which has not been reflected on the assessment unit’s immediately preceding year’s assessment roll. Additions include omitted property, new or replacement construction, and increases in value due to new public services and/or contamination remediation.

9

Instructions for Tax Credit for Maintenance and Improvement of Right of Way

Sec. 13 of PA 282 of 1905, as amended, (more specifically MCL 207.13(2) and MCL 207.13a(5)(b)(ii)), allows credit against the tax imposed, for eligible expenses incurred in the State of Michigan by railroad companies for maintenance or improvement of rights of way, including those items, except depreciation, in the official

Additional Statutory Requirements for Eligibility (MCL 207.13(2) - (5))

In order to be eligible for the tax credit for maintenance and improvement of rights of way, the railroad companies must complete and file [3 COPIES OF] an annual report with the State Tax Commission that includes the following:

1.Detailed data of right of way work conducted in this state during the past calendar year separated by costs of labor and materials on each project and itemized in the following categories:

(a)Miles of track laid

(b)Tons of new ballast installed

(c)Number of ties installed

(d)Miles of track surfaced

(e)Signals installed

(f)Under drainage work done

2.The number of notices of violation from the railway inspectors by railroad section,

3.A detailed account of the location and nature of the work defined by railroad section or mile posts surrounding the work area plus the county, city, or township in which the work was performed,

4. Demonstration that the highest priority of expenditures for the maintenance and improvement of rights of way has been given to rail lines that handle hazardous materials, especially those that are located in urban or residential areas, and detailed data on the tonnages of hazardous materials handled in relation to tonnages of other traffic handled over the rail line for which a tax credit is being applied.

In addition, the company must grant to another railroad company, upon application by the latter, trackage rights over its line for trains, providing that the train operations do not interfere with the movement of Michigan freight using the same trackage, if operations can be accomplished safely in the opinion of the grantor and if trackage arrangements and train operations are approved by the interstate commerce commission.

***NOTE*** Filing of the credit application does not relieve you of the requirement of filing 3 copies of the above defined report with the State Tax Commission. You are still required to provide the above information in a separate report.

What expenses are eligible for credit against the tax levied? MCL 207.13(2)

Eligible Expenses:

1.Eligible expenses must have been incurred during the calendar year immediately preceding the statutory due date of this report.

2.Eligible expenses must have been incurred in the State of Michigan.

3.Examples of Eligible Capital Expenses for Road and Equipment include, but are not limited to items from the following categories:

(1) |

Engineering exp. directly related to R & E Property |

(23) |

Wharves and Docks |

(3) |

Other |

(24) |

Coal and Ore Wharves |

(4) |

Grading |

(25) |

TOFC/COFC Terminals |

(5) |

Tunnels and Subways |

(26) |

Communication Systems |

(6) |

Bridges, trestles, and culverts |

(27) |

Signals and Interlockers |

(7) |

Elevated Structures |

(37) |

Roadway Machines |

(8, 9, 10, 11) Ties, Rails and other Track Material |

(38) |

Roadway small tools |

|

(12) Track Laying and Surfacing |

(39) |

Public Improvements - Construction |

|

(13) Fences, Snowsheds, and Signs |

(43) |

Other Expenses - Road |

|

(17) Roadway Buildings (portion housing MOW equipment and engineering)

10

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Michigan 1028 form is used for the Annual Property Report for state-assessed railroads. |

| Governing Law | This report is governed by Michigan Public Act 282 of 1905, as amended. |

| Filing Requirement | Filing the Michigan 1028 form is mandatory for applicable companies. |

| Contact Person | Each company must designate one authorized contact person for correspondence regarding the report. |

| Filing Deadlines | Companies with gross receipts over $1,000,000 must file by March 31; those with receipts of $1,000,000 or less must file by March 15. |

| Late Filing Penalty | A fine of $500 per day applies for companies that fail to file a complete report by the due date. |

| Notary Requirement | The report must be signed and notarized by an authorized company officer. |

| Inventory Exemption | Inventory is exempt from assessment, except for certain leased personal property. |

| Accessing Summary Calculations | After processing, companies can view summary calculations online by requesting a personal identification number (PIN). |

Filling out the Michigan 1028 form is a crucial step for companies that need to report their annual property information. After completing the form, it must be submitted by the specified deadlines to avoid penalties. Companies with annual gross receipts over $1,000,000 must file by March 31, while those with lower receipts must submit by March 15. Failure to file on time can result in daily fines.

What is the Michigan 1028 form?

The Michigan 1028 form, known as the Annual Property Report, is a mandatory filing for companies assessed by the State of Michigan. It is specifically designed for railroads and must be submitted annually. This report collects essential information about the company's property and operations for tax assessment purposes.

Who is required to file the Michigan 1028 form?

Companies with annual gross receipts greater than $1,000,000 must file the Michigan 1028 form by March 31. Those with receipts equal to or less than $1,000,000 have a slightly earlier deadline of March 15. Failure to file on time can result in significant penalties, including a fine of $500 per day.

What information do I need to provide on the form?

The form requires various details, including the company name, Federal Tax ID number, and address for tax bills. You must also designate an authorized contact person. Additionally, the report asks for information about rolling stock, road property, and any changes in company ownership or structure during the previous calendar year.

What happens if I miss the filing deadline?

If you miss the filing deadline, your company may incur a fine of $500 for each day the report is late. This penalty can accumulate quickly, so it’s crucial to file on time to avoid unnecessary financial burdens.

Are there exemptions I should be aware of?

Yes, certain properties are exempt from assessment. For example, inventory is generally exempt, as are motor vehicles registered with the Michigan Secretary of State on Tax Day (December 31). Additionally, specific computer software purchases may also qualify for exemption if they meet certain criteria.

How can I access my company's summary calculations after filing?

After the Assessment and Certification Division processes your report, you can access summary calculations by requesting a personal identification number (PIN). This PIN allows you to log into your company's secure online account to view the results. Tentative values will be available around May 15, with final values posted by June 15.

Missing Deadlines: One common mistake is failing to submit the Michigan 1028 form by the required deadlines. Companies with gross receipts over $1,000,000 must file by March 31, while those with lower receipts must file by March 15.

Incomplete Information: Providing incomplete information can lead to delays or fines. Ensure every section of the form is filled out accurately, including company name and tax ID.

Incorrect Contact Person: Only one authorized contact person is allowed. Failing to designate the correct individual can complicate communication and lead to misunderstandings.

Ignoring Changes: If your company underwent any name changes, acquisitions, or sales, it’s essential to disclose this. Not doing so may result in penalties.

Misreporting Financials: Accurate reporting of financial data is crucial. Mistakes in the reported costs or revenues can lead to significant issues with the tax commission.

Neglecting Notary Requirements: The form must be notarized. Failing to include a notary signature can render the submission invalid.

Forgetting Attachments: If additional documentation is required, ensure it is attached. Missing attachments can delay processing.

Confusing Inventory Rules: Understanding what qualifies as inventory is vital. Misclassifying items can lead to incorrect assessments.

Overlooking Schedule Details: Each schedule in the form has specific requirements. Ignoring these details can lead to incomplete submissions.

Failing to Review: Before submitting, review the form thoroughly. Errors often go unnoticed without a careful final check.

The Michigan 1028 form is a crucial document for companies assessed by the state for property tax purposes. When filing this report, several other forms and documents may also be required or beneficial for proper compliance. Below is a list of related documents often used alongside the Michigan 1028 form.

These documents work in conjunction with the Michigan 1028 form to provide a comprehensive overview of a company's property and operational status. Accurate completion of all relevant forms is essential to avoid penalties and ensure compliance with state regulations.

The Michigan 1028 form is an important document for state-assessed railroads, serving as an annual property report. Several other documents share similarities with the Michigan 1028 form, particularly in their purpose and structure. Here’s a look at seven such documents:

Understanding these documents can help businesses and organizations navigate their compliance obligations more effectively. Each serves a unique purpose but shares common threads of accountability and transparency.

When filling out the Michigan 1028 form, it's important to ensure accuracy and completeness. Here’s a list of things to do and avoid to help you navigate the process smoothly.

By following these guidelines, you can help ensure that your Michigan 1028 form is filled out correctly and submitted on time, minimizing the risk of penalties or issues with your filing.

Misconceptions about the Michigan 1028 form can lead to confusion and potential penalties. Here are five common misconceptions clarified:

Filling out the Michigan 1028 form is a crucial process for companies involved in railroad operations. Here are some key takeaways to keep in mind: