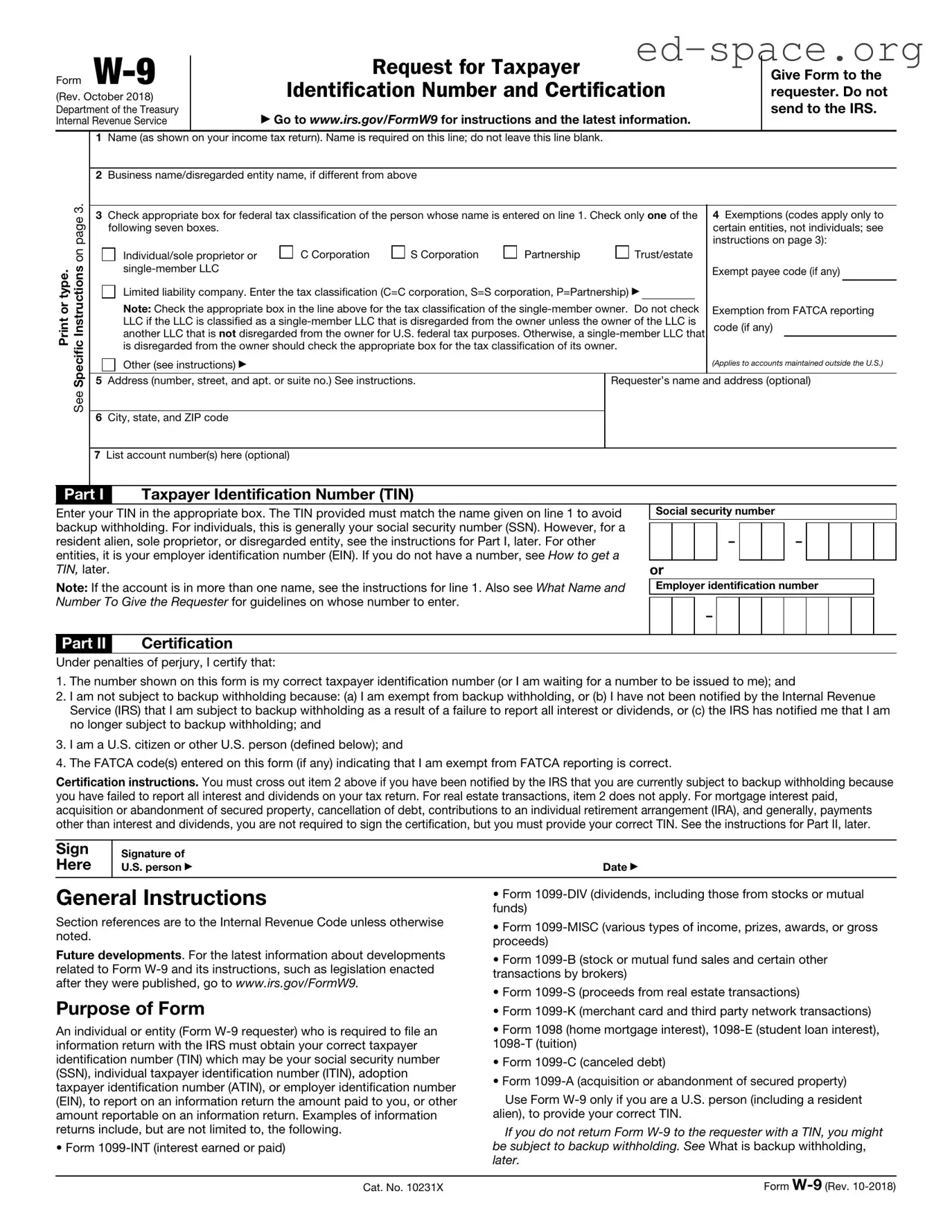

For many individuals and entities navigating the complexities of tax documentation, the IRS W-9 form stands as a critical pillar in ensuring compliance and facilitating smooth financial operations. Broadly, this form is essential for accurately reporting tax information between parties. Whether it's a freelancer embarking on a new client relationship, a financial institution setting up an account, or a business engaging with independent contractors, the W-9 form plays a pivotal role. It serves not only as a means for collecting necessary identifying details, such as taxpayer identification number (TIN) and certification that the information provided is correct but also as a safeguard for both parties against potential tax-related missteps. The obligation to accurately complete and update this document as required underscores its importance in maintaining transparency and accountability in financial dealings. As such, understanding the form's nuances, including when and how to properly complete it, becomes indispensable for anyone involved in transactions where proving U.S. tax status is requisite.

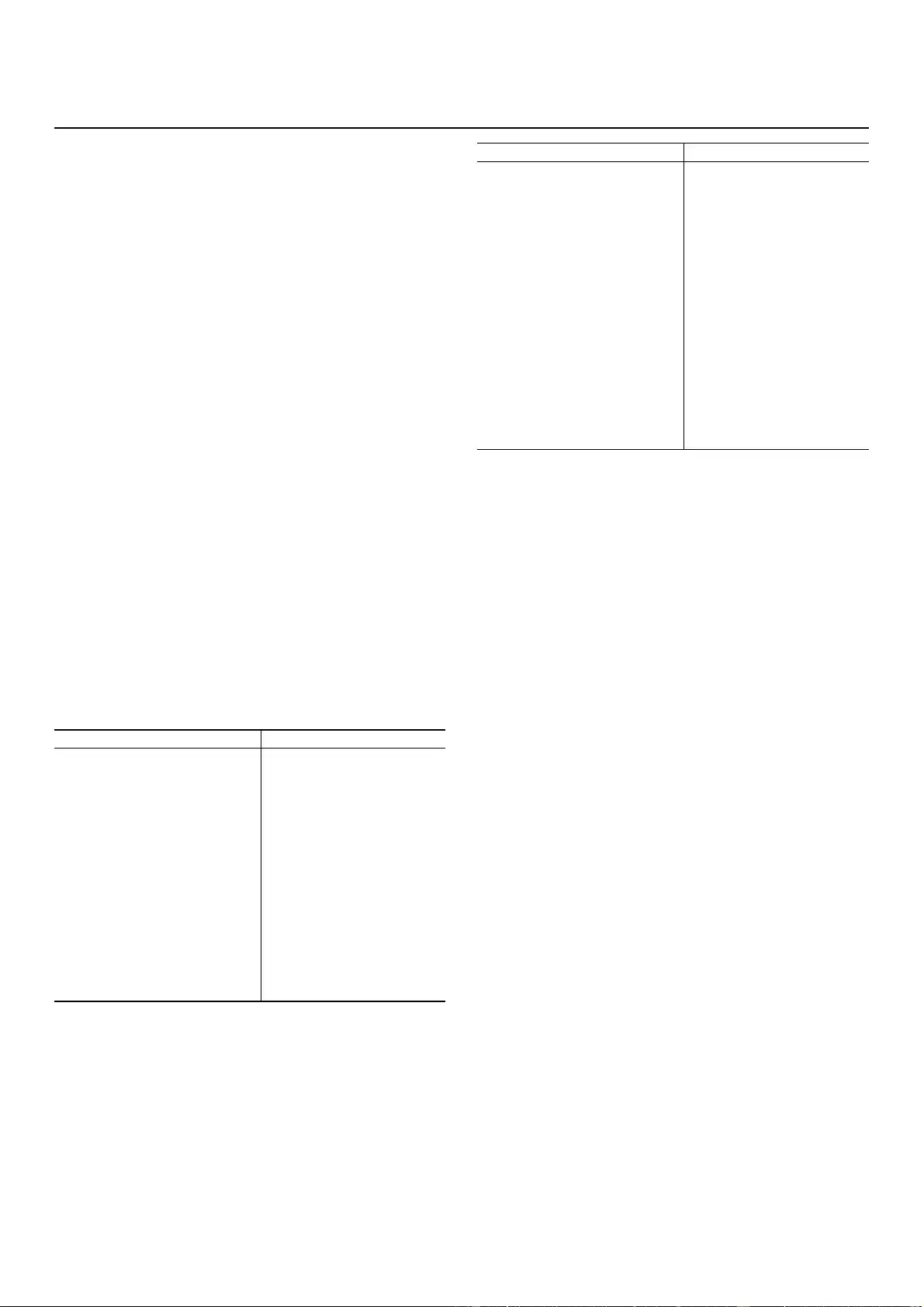

| Fact Number | Description | Governing Law(s) |

|---|---|---|

| 1 | The IRS W-9 form is officially titled "Request for Taxpayer Identification Number and Certification". | Internal Revenue Code |

| 2 | It is used by individuals and entities to provide their Taxpayer Identification Number (TIN) to entities that will pay them income. | Internal Revenue Code |

| 3 | Employers use the information to prepare Form 1099-MISC, reporting non-employee compensation. | Internal Revenue Code |

| 4 | Banks may require a completed W-9 form to open an interest-bearing account. | Internal Revenue Code |

| 5 | Freelancers and independent contractors often need to fill out this form for their clients. | Internal Revenue Code |

| 6 | Failing to provide a W-9 when requested can result in backup withholding, where the payee must withhold 24% of income for taxes. | Internal Revenue Code |

| 7 | The W-9 form is not sent to the IRS but kept by the requester for informational purposes and to respond to notices from the IRS if needed. | Internal Revenue Code |

| 8 | Personal information including the TIN (which may be a Social Security Number), name, and address, are filled in on the form. | Internal Revenue Code |

| 9 | For state-specific reporting requirements, some states may have forms similar to the W-9 but follow their own regulations. | Varies by State |

Filling out the IRS W-9 form is a standard procedure for anyone beginning a new job, working as a freelancer, or conducting business that generates income requiring tax documentation. This form is crucial for taxpayers to provide their correct Taxpayer Identification Number (TIN) to the person who is required to file an information return with the IRS. Failure to complete the form accurately can lead to backup withholding and other tax complications. To ensure the process is as smooth as possible, follow these simple step-by-step instructions.

After completing the form, you should provide it to the requester and keep a copy for your records. Do not send it directly to the IRS. For individuals who might require a different version of the form due to changes in tax law or for other specific situations, it's always recommended to verify with a tax professional or consult the IRS website for guidance.

What is an IRS W-9 form and who needs to fill it out?

The IRS W-9 form, officially titled "Request for Taxpayer Identification Number and Certification," is a document that individuals or entities use to provide their correct Taxpayer Identification Number (TIN) to entities that will pay them. It is needed by independent contractors, freelancers, and other non-employees so that businesses can properly report their income to the IRS. If you are asked to fill out a W-9, it typically means you will receive payments from the requester that will not be subject to withholding tax.

How do I fill out and submit a W-9 form?

Filling out a W-9 form is straightforward. You need to provide your name, business name (if applicable), your Tax Identification Number (TIN) which may be your Social Security Number (SSN) or Employer Identification Number (EIN), and your address. After completing the form, sign and date it to certify that the information is correct. Submission methods can vary; the requester might accept it via mail, email, or a secure upload portal. Make sure to follow their instructions to ensure your data is protected.

Is my personal information safe when I submit a W-9 form?

Your concerns about security are valid since the W-9 form contains sensitive information. Requesters are obliged to keep your information secure and confidential. However, it's also important for you to submit your W-9 form through secure methods. Be wary of scams and only provide your W-9 to trusted parties that you have personally verified. If you have concerns about the legitimacy of a request, it's advisable to perform due diligence before submission.

Do I need to submit a new W-9 form each year?

Typically, you do not need to submit a new W-9 form each year to the same requester. However, you are required to provide an updated form if any of your information changes, such as your name, address, or TIN. Additionally, if you start working with a new payer, you will need to complete a W-9 for them.

What should I do if I made a mistake on a submitted W-9 form?

If you realize that you have made an error on a W-9 form after submitting it, you should immediately correct the mistake and send a new form to the requester. This ensures that the information reported to the IRS is accurate, which is crucial for your tax records. It's better to be proactive in correcting errors to avoid any potential issues with your tax filings.

Filling out the IRS W-9 form, a crucial document requested by companies paying for services rendered by freelancers, consultants, and various other contractors, is a process that seems straightforward but is often fraught with errors. This form is essential for accurately reporting income to the Internal Revenue Service (IRS) and ensuring the correct amount of taxes are paid. However, mistakes can lead to delays, incorrect tax withholding, and potential penalties. Here are five common mistakes people make when filling out the IRS W-9 form:

Incorrect Taxpayer Identification Number (TIN): One of the most critical components of the W-9 form is the Taxpayer Identification Number, which can be either a Social Security Number (SSN) or an Employer Identification Number (EIN). People often inadvertently transpose numbers or mistakenly use an incorrect identification type. This error can cause significant issues, including incorrect tax reporting and potential mismatch letters from the IRS.

Not using the legal name associated with the TIN: The name entered on the W-9 must match the name associated with the provided TIN. Discrepancies often occur when individuals use nicknames, abbreviations, or business DBAs (Doing Business As) without understanding that the legal name tied to the SSN or EIN must be used. This mistake can lead to mismatches in IRS records and delayed payments.

Failing to sign the form: Although it might seem obvious, many people forget to sign the W-9 form. An unsigned form is considered invalid and can result in the requester withholding payments until a valid, signed form is received. A signature certifies that the information provided is accurate and truthful, thereby ignoring this step can introduce unnecessary complications.

Skipping the “Exempt Payee” box: Not appropriately understanding or indicating one's exempt status can lead to improper tax withholding. Some entities are exempt from backup withholding and need to check the box labeled “Exempt Payee” to communicate their status. However, misunderstanding about whether one qualifies can result in either unexpected tax liabilities or over-withholding.

Using an outdated form: Individuals sometimes mistakenly use an outdated version of the W-9 form. The IRS periodically updates its forms, and using the most current version is essential to comply with the latest tax reporting requirements. An outdated form may lack new fields or contain obsolete information, leading to processing delays or requests for a new form submission.

Making sure to avoid these common pitfalls when completing the IRS W-9 form will help ensure that the process is smooth, with minimal delays and corrections needed. It's always beneficial to double-check the form against the most recent guidelines provided by the IRS and seek clarification if uncertain about any information requested on the form.

The IRS W-9 form is crucial for collecting taxpayer identification numbers and certification from individuals or entities that receive payments other than wages, salaries, and tips. It's commonly used in various transactions including employment and freelancing. Nevertheless, the W-9 form is rarely the only document needed in these circumstances. Several other forms and documents often accompany it, ensuring compliance with tax laws and employment regulations. Below is a list of these forms and documents, offering a brief description of each.

Together with the IRS W-9 form, these documents create a comprehensive package for tax and employment related matters, ensuring that individuals and businesses alike can navigate these processes with increased accuracy and legality. Whether hiring an employee, engaging a freelancer, or conducting other transactions requiring tax reporting, these forms support clarity and compliance.

IRS Form W-4: Similar to Form W-9, the IRS Form W-4 is used by employees to inform their employer of their tax situation, specifically how much federal income tax to withhold from their paychecks. While the W-9 is for independent contractors to provide their tax identification numbers (TINs) to the entities for whom they work, the W-4 gathers employees' filing status and allowances to calculate withholding tax.

IRS Form 1099-MISC: The IRS Form 1099-MISC is closely tied to the information gathered by the W-9. It is used by businesses to report payments made to independent contractors, freelancers, and other non-employees. In essence, the information provided on a W-9 enables the payers to accurately fill out and send the appropriate 1099 form, reporting the income paid to the individual or entity during the tax year.

IRS Form W-8BEN: The IRS Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding, is used by foreign individuals or entities to certify their non-U.S. status. Similar to the W-9, which collects taxpayer information for U.S. persons, the W-8BEN gathers details to establish the correct withholding tax rate under U.S. tax law for non-U.S. individuals and entities.

IRS Form 1040: While significantly broader in purpose, the IRS Form 1040, U.S. Individual Income Tax Return, shares a fundamental connection with the W-9 in that it deals directly with taxpayer identification and income reporting. Individuals use Form 1040 to file their annual income tax returns, which could include reporting income from sources for which a W-9 had been previously provided.

IRS Form SS-4: The IRS Form SS-4, Application for Employer Identification Number (EIN), is used by entities to apply for an EIN, a necessary identifier for businesses. Similar to how individual contractors provide their Social Security Number (SSN) or EIN via the W-9, businesses use Form SS-4 to obtain an EIN that they may need to supply when working with other businesses or contractors, establishing a parallel in purpose for identification and tax reporting.

The IRS W-9 form is a crucial document in the financial ecosystem of the United States, facilitating the correct reporting of taxes and other financial information between parties. It's often required in situations such as starting a new job, opening a bank account, or engaging in freelance work. When completing this form, accuracy and attention to detail are not just recommended; they are imperative. Here, we present a curated list of dos and don’ts to guide you through the process of filling out the W-9 form properly.

Do:

Provide accurate information: Ensure all the data you provide, including your name, address, and Taxpayer Identification Number (SSN, EIN, or ITIN), accurately matches the records held by the IRS.

Use your legal name: The name you put on the form should match the name on your tax return to avoid any discrepancies and potential issues with the IRS.

Double-check your Taxpayer Identification Number (TIN): This is crucial for tax reporting purposes. Any mistake here could lead to bureaucratic headaches or even tax penalties.

Sign and date the form: An unsigned or undated W-9 form is considered invalid. Your signature attests that all the information provided is correct to the best of your knowledge.

Update your information when necessary: If your personal or business information changes, such as your address or TIN, submit a new W-9 form to reflect these updates.

Keep your form secure: While the W-9 contains sensitive information, ensure that you're only providing it to legitimate and trusted entities.

Review the form for errors before submission: It’s always a good idea to give it one last look to catch any mistakes or omitted information.

Don't:

Leave blank fields: Incomplete forms may be rejected, so make sure you answer every applicable section and question.

Use nicknames or abbreviations: This form requires your legal name to match IRS records, so refrain from using any informal variations.

Ignore requests to fill out or update a W-9 form: Prompt compliance is necessary to prevent any interruption in payments or transactions.

Send the form via unsecured or unencrypted email: Given the sensitive nature of the information on the W-9, sending it through insecure means can put your data at risk.

Forget to make necessary updates: If your situation changes, such as a new address or a change in your business structure, failing to communicate these changes can lead to incorrect tax filings.

Assume it’s okay to submit an outdated form: Always make sure you are using the most current version of the form to comply with the latest IRS regulations and requirements.

Overlook the instructions provided by the IRS for the W-9 form: These instructions can answer many common questions and clarify what information is needed for each field.

Remember, the W-9 form is a foundational document that supports transparent and lawful financial operations, ensuring that all parties comply with U.S. tax law. By observing these guidelines, individuals and entities can avoid complications with tax reporting, setting a solid ground for their fiscal responsibilities.

When it comes to understanding the IRS W-9 form, several misconceptions commonly arise. This form is crucial for independent contractors, freelancers, and other entities engaging in business activities. As we dive into these misconceptions, it's essential we clarify and correct them to ensure compliance and proper tax reporting.

Only employees need to fill it out. One widespread misconception is that W-9 forms are only for employees. In reality, the W-9 is for independent contractors, freelancers, and vendors to provide their taxpayer identification number (TIN) to entities they work with. This information is used to report payments to the IRS.

It must be submitted to the IRS. Many believe that after completing a W-9, it needs to be sent directly to the IRS. However, the form should actually be given to the person or business that requested it, not to the IRS. They use it to prepare 1099-MISC forms if necessary.

Filling it out once covers all jobs. Some think that you only need to fill out a W-9 form once for all your freelance or independent contractor gigs. The truth is, you must complete a W-9 for each new client who pays you more than $600 in a calendar year, as each company needs your information to report payments accurately.

There's no need to update it. Another common myth is that once a W-9 is filled out, it doesn't need to be updated. In fact, you should submit a new W-9 to your clients if your name, business name, address, or tax ID number changes to ensure that they have your most current information for accurate tax reporting.

Electronic signatures are not allowed. Some people are under the impression that W-9 forms cannot be signed electronically and must be signed in ink. The IRS does allow electronic signatures that meet their requirements, making the process more convenient for remote work and digital communication.

There's a filing deadline. Unlike tax returns that have a specific filing deadline, the W-9 does not have a deadline set by the IRS. It should be completed and provided to the requester as part of the business engagement process, often at the start of a working relationship or at the time of payment.

It's only for U.S. citizens. While it's true that the W-9 form is primarily for U.S. residents and citizens, it's also relevant for resident aliens and certain types of entities with a U.S. tax presence. Non-resident aliens, on the other hand, may have to fill out forms like the W-8BEN.

Personal information is not at risk. Many individuals overlook the importance of safeguarding their W-9 forms. Because these forms contain sensitive information such as your TIN or Social Security number, it's vital to only provide this form to trusted parties and to be cautious of phishing scams.

Tax advisors are unnecessary. Lastly, there's a misconception that the simplicity of the W-9 form means tax advisors or professionals are not needed. In reality, consulting with a tax professional can ensure that you understand your tax obligations and rights, especially in complex situations or where penalties for noncompliance might arise.

Addressing these misconceptions about the IRS W-9 form helps ensure that individuals and entities can navigate their tax reporting responsibilities more effectively. Accurate understanding and compliance benefit all parties involved by fostering informed business decisions and adherence to tax laws.

The IRS W-9 form, officially titled "Request for Taxpayer Identification Number and Certification," is a standard tax document used in the United States. Primarily, it's requested by companies that pay you to ensure they have the correct information to report income paid to you and others to the IRS. Here are ten key takeaways to understand when filling out and using the W-9 form.

Understanding these key aspects of the W-9 form can help individuals and businesses navigate tax reporting requirements more efficiently, ensuring compliance with IRS rules and avoiding common pitfalls.

Vehicle Ownership Declaration - Make sure to check all boxes relevant to your vehicle type.

Georgia Form G-1003 - Accurate reporting on the G 1003 contributes to the integrity of state tax records.

Cbp Security Area Identification - Each applicant's situation is assessed individually based on the information provided.