The IRS W-7 (COA) form plays a crucial role for individuals who need to apply for an Individual Taxpayer Identification Number (ITIN) but may not have the required documentation to prove their foreign status. This form is specifically designed for those who are claiming a tax treaty benefit or need to file a U.S. tax return, but do not qualify for a Social Security number. Completing the W-7 (COA) involves providing personal information, such as your name, address, and date of birth, along with the reason for needing an ITIN. It’s important to attach the necessary supporting documents to verify your identity and foreign status. The IRS uses this information to process your application efficiently. Understanding the purpose and requirements of the W-7 (COA) can help streamline the process and ensure that you receive your ITIN in a timely manner, which is essential for meeting your tax obligations and accessing certain benefits in the U.S.

Form |

|

Certificate of Accuracy for IRS Individual |

OMB Number |

|||||||||

(July 2023) |

|

|

|

Taxpayer Identification Number |

||||||||

|

|

|

||||||||||

Department of the Treasury |

|

|

|

|

|

|

See Publication 4520 |

|||||

|

|

|

|

|

|

|

||||||

Internal Revenue Service |

Form use only by IRS Certifying Acceptance Agents when submitting Form |

|

||||||||||

|

|

|

|

|

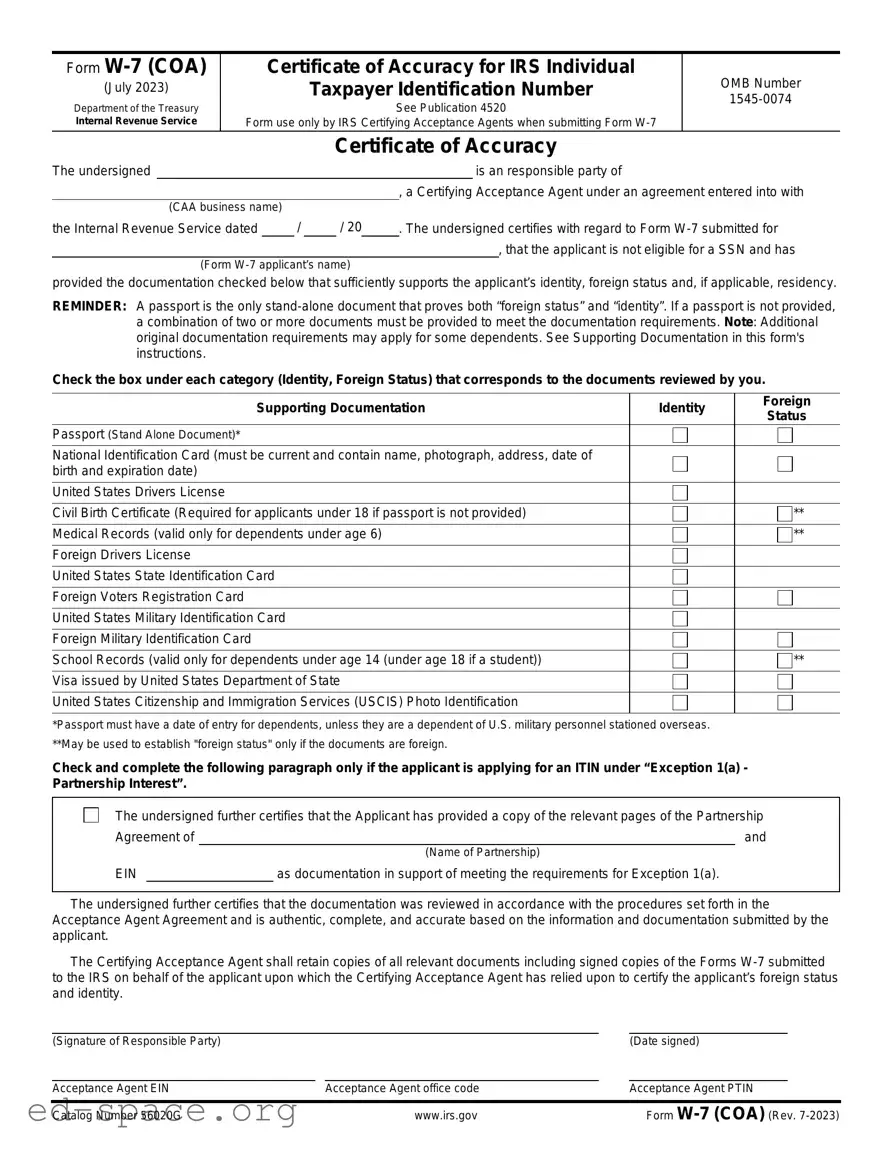

Certificate of Accuracy |

|

||||||

The undersigned |

|

|

|

|

|

|

|

|

|

is an responsible party of |

|

|

|

|

|

|

|

|

|

|

, a Certifying Acceptance Agent under an agreement entered into with |

||||

|

(CAA business name) |

|

|

|

|

|

|

|

|

|||

the Internal Revenue Service dated |

/ |

/ 20 |

. The undersigned certifies with regard to Form |

|||||||||

|

|

|

|

|

|

|

|

|

|

, that the applicant is not eligible for a SSN and has |

||

|

(Form |

|

|

|

|

|

||||||

provided the documentation checked below that sufficiently supports the applicant’s identity, foreign status and, if applicable, residency.

REMINDER: A passport is the only

Check the box under each category (Identity, Foreign Status) that corresponds to the documents reviewed by you.

Supporting Documentation |

Identity |

Foreign |

|

Status |

|||

|

|

||

Passport (Stand Alone Document)* |

|

|

|

National Identification Card (must be current and contain name, photograph, address, date of |

|

|

|

birth and expiration date) |

|

|

|

United States Drivers License |

|

|

|

|

|

|

|

Civil Birth Certificate (Required for applicants under 18 if passport is not provided) |

|

** |

|

Medical Records (valid only for dependents under age 6) |

|

** |

|

|

|

|

|

Foreign Drivers License |

|

|

|

|

|

|

|

United States State Identification Card |

|

|

|

|

|

|

|

Foreign Voters Registration Card |

|

|

|

|

|

|

|

United States Military Identification Card |

|

|

|

Foreign Military Identification Card |

|

|

|

|

|

|

|

School Records (valid only for dependents under age 14 (under age 18 if a student)) |

|

** |

|

|

|

|

|

Visa issued by United States Department of State |

|

|

|

|

|

|

|

United States Citizenship and Immigration Services (USCIS) Photo Identification |

|

|

|

|

|

|

*Passport must have a date of entry for dependents, unless they are a dependent of U.S. military personnel stationed overseas.

**May be used to establish "foreign status" only if the documents are foreign.

Check and complete the following paragraph only if the applicant is applying for an ITIN under “Exception 1(a) - Partnership Interest”.

The undersigned further certifies that the Applicant has provided a copy of the relevant pages of the Partnership

Agreement of |

|

|

and |

|

|

|

|

(Name of Partnership) |

|

EIN |

|

|

as documentation in support of meeting the requirements for Exception 1(a). |

|

The undersigned further certifies that the documentation was reviewed in accordance with the procedures set forth in the Acceptance Agent Agreement and is authentic, complete, and accurate based on the information and documentation submitted by the applicant.

The Certifying Acceptance Agent shall retain copies of all relevant documents including signed copies of the Forms

(Signature of Responsible Party) |

|

|

|

(Date signed) |

|

|

|

|

|

|

|

Acceptance Agent EIN |

|

Acceptance Agent office code |

|

Acceptance Agent PTIN |

|

|

|

|

|

|

|

Catalog Number 56020G |

|

www.irs.gov |

|

Form |

|

Instructions for Form

What is Form

Form

•The name of the designated responsible party of the CAA who is completing the Certificate of Accuracy (COA).

•The legal name of the business.

•The Employers Identification Number (EIN) and office code of the CAA.

•The date that the Acceptance Agent Agreement was approved.

•The name of the ITIN Applicant.

•The type(s) of supporting documentation reviewed by the CAA to prove the ITIN applicant’s “identity” and “foreign status”.

•A statement by the CAA that they have verified to the best of their knowledge, the authenticity, accuracy and completeness of the documentation they reviewed.

•The signature of the individual who has prepared the COA and the date that it was signed.

What is the purpose of Form

The COA is a certification by the CAA that they have reviewed the supporting documentation to prove the ITIN applicant’s “identity” and “foreign status” and to the best of their knowledge the documents are complete, authentic, and accurate. Note: With the exception of documentation to prove Exception 1(a) criteria, the only documents that should be included in the COA are those that were reviewed by you to prove the applicant’s claim of identity and foreign status. All other supplemental documentation supporting “Exception” criteria, (i.e. a copy of a withholding document, a letter from a financial institution, etc,) as well as a denial letter from the Social Security Administration (if applicable) must be attached to Form

Who must submit a COA?

All CAAs are required to complete and submit a separate COA for each Form

Who can sign the Certificate of Accuracy?

Only the designated responsible party of the business is permitted to sign the COA.

Where can I find Form

Form

Whose PTIN is required?

Only tax practitioners are required to have a PTIN. The approved responsible party of the business must provide their PTIN on Form

Supporting Documentation

You should check only the boxes that correspond to the documents which you reviewed and certified to support the ITIN applicant’s identity and foreign status. A passport is the only stand alone document for purposes of satisfying both the “identity” and “foreign status” criteria. A passport that doesn't have a date of entry won't be accepted as a

Definitions — The following chart represents definitions for phrases used in Form

Phrase |

Definition |

|

|

The Undersigned |

This is the name of the individual who is preparing and signing the Certificate of Accuracy. This person must be the |

|

individual who has been designated as the responsible party of the business. |

|

|

CAA Business Name |

This is the legal name of the business that was entered by you on Form 13551, Application to Participate in the |

|

ITIN Acceptance Agent Program. |

|

|

Agreement approved date |

This is the date that IRS approved your agreement. You can locate this date on your CAA Agreement. |

___ / ___ / 20__ |

|

|

|

Form |

This is the name of the individual for whom you are completing the Form |

|

|

Name of Partnership |

The name of the partnership should be entered on this line only if you are requesting an ITIN under Exception 1 |

|

(a) – Partners in a U.S. or foreign partnership that invests in the U.S. |

|

|

EIN, Office Code and PTIN |

This is the Employer’s Identification Number (EIN) that was assigned to the business by IRS. The office code is a |

|

number assigned by the ITIN Policy Section when the application for AA status is approved. Preparer Tax |

|

Identification Number (PTIN) is required for anyone who prepares or assists in preparing federal tax returns for |

|

compensation. This number should be entered on the line for Acceptance Agent PTIN |

|

|

Date signed |

This is the date that the Certificate of Accuracy is signed by the responsible party of the Business. |

|

|

For additional information regarding documentation, please refer to Publication 4520 Acceptance Agents Guide for Individual Taxpayer Identification Number (ITIN)

Catalog Number 56020G |

www.irs.gov |

Form |

| Fact Name | Description |

|---|---|

| Purpose | The IRS W-7 (COA) form is used to apply for an Individual Taxpayer Identification Number (ITIN). |

| Eligibility | Individuals who are not eligible for a Social Security Number but need to file taxes can apply using this form. |

| Supporting Documents | Applicants must submit documents that prove their identity and foreign status, such as a passport or birth certificate. |

| Submission Method | The completed form can be submitted by mail or in person at designated IRS offices. |

| Processing Time | Typically, it takes about 7 weeks to process the W-7 form, but this may vary during peak tax season. |

| Renewal | ITINs must be renewed if not used on a federal tax return for three consecutive years. |

| State-Specific Forms | Some states may require additional forms or documentation, governed by state tax laws. |

| Filing Requirement | The W-7 form must be filed along with a federal tax return, unless applying for an ITIN for a non-filing reason. |

| Common Mistakes | Common errors include missing signatures, incorrect information, and not providing sufficient identification documents. |

Completing the IRS W-7 (COA) form is an important step for individuals who need to apply for an Individual Taxpayer Identification Number (ITIN). After filling out the form, you will need to submit it along with the required documentation to the IRS for processing. Below are the steps to guide you through filling out the form.

What is the IRS W-7 (COA) form?

The IRS W-7 (COA) form is used to apply for an Individual Taxpayer Identification Number (ITIN) for individuals who are not eligible for a Social Security Number. This form is specifically for those who need an ITIN for tax purposes, such as non-resident aliens, their spouses, and dependents. The COA stands for "Certificate of Accuracy," which indicates that the application is accompanied by documentation that verifies the individual's foreign status and identity.

Who needs to fill out the W-7 (COA) form?

Individuals who are required to file a U.S. tax return but do not have a Social Security Number should complete the W-7 (COA) form. This includes foreign nationals, non-resident aliens, and their dependents who need an ITIN for tax reporting purposes. It is essential for anyone who receives income from U.S. sources or who is required to report certain types of income to the IRS.

What documents are required to submit with the W-7 (COA) form?

When submitting the W-7 (COA) form, applicants must provide original documents or certified copies that prove their identity and foreign status. Acceptable documents include a passport, national identification card, or other government-issued documents that contain the individual's name, photo, and address. It’s crucial that the documents are valid and not expired.

How long does it take to process the W-7 (COA) form?

The processing time for the W-7 (COA) form can vary. Generally, it takes about 7 weeks for the IRS to process the application. However, during peak tax season or if additional information is required, it may take longer. Applicants can check the status of their application by contacting the IRS after the processing time has elapsed.

Can I submit the W-7 (COA) form online?

No, the W-7 (COA) form cannot be submitted online. Applicants must mail the completed form along with the required documentation to the address specified in the form's instructions. Alternatively, individuals can apply in person at designated IRS Taxpayer Assistance Centers or through an Acceptance Agent authorized by the IRS.

Is there a fee to apply for an ITIN using the W-7 (COA) form?

There is no fee to submit the W-7 (COA) form itself. However, if you choose to use a tax professional or an Acceptance Agent to assist you in the application process, they may charge a fee for their services. It's always a good idea to inquire about any potential costs before proceeding.

What happens if my W-7 (COA) form is denied?

If the W-7 (COA) form is denied, the IRS will send a notice explaining the reason for the denial. Common reasons include missing documentation, incorrect information, or failure to meet eligibility requirements. Applicants can address the issues outlined in the notice and reapply by submitting a new W-7 (COA) form along with the necessary documentation.

Can I use an ITIN for identification purposes?

While an ITIN is primarily for tax purposes, it can sometimes be used as a form of identification. However, it is important to note that an ITIN does not grant the holder the same rights as a Social Security Number. It cannot be used for employment or to qualify for Social Security benefits. Always check specific requirements for identification in various contexts.

How often do I need to renew my ITIN?

ITINs do not expire as long as they are used on a federal tax return at least once in the last three years. However, if an ITIN is not used for tax purposes during that time, it may expire. The IRS recommends renewing your ITIN if you need to file a tax return and your ITIN has expired. To renew, you will need to submit a new W-7 form along with the required documentation.

Where can I find more information about the W-7 (COA) form?

For more detailed information about the W-7 (COA) form, applicants can visit the official IRS website. The site provides comprehensive guidance, including instructions for filling out the form, acceptable documents, and additional resources for individuals seeking an ITIN. It is always best to refer to the most current information directly from the IRS.

Failing to provide a valid reason for submitting the form. The IRS requires applicants to indicate the specific purpose for obtaining an Individual Taxpayer Identification Number (ITIN). Without this information, the application may be rejected.

Not including the required supporting documentation. The W-7 form mandates that applicants submit original documents or certified copies that prove their identity and foreign status. Omitting these documents can lead to delays or denials.

Inaccurate personal information. Common errors include misspellings of names, incorrect dates of birth, or wrong addresses. Such inaccuracies can create confusion and complicate the processing of the application.

Submitting the form without a signature. The W-7 must be signed by the applicant. A missing signature will result in the IRS not processing the application.

Using outdated forms. The IRS periodically updates its forms. Submitting an older version of the W-7 can lead to processing issues. Always check for the most current version.

Not following the instructions for completing the form. The IRS provides detailed instructions for filling out the W-7. Ignoring these guidelines may result in mistakes that can delay the application.

Submitting the application to the wrong address. The IRS has specific mailing addresses for different types of applications. Sending the W-7 to the incorrect location can prolong the review process.

The IRS W-7 (COA) form is used to apply for an Individual Taxpayer Identification Number (ITIN) for individuals who are not eligible for a Social Security Number. When submitting the W-7 form, several other documents may be required to support the application. Below is a list of common forms and documents that are often used in conjunction with the W-7 form.

Submitting the W-7 form with the appropriate supporting documents ensures a smoother application process for obtaining an ITIN. Careful attention to detail can help avoid delays in processing.

When filling out the IRS W-7 (COA) form, it’s important to follow certain guidelines to ensure your application is processed smoothly. Here are some dos and don'ts to consider:

The IRS W-7 form, also known as the Application for IRS Individual Taxpayer Identification Number (ITIN), has several misconceptions associated with it. Understanding these misconceptions can help individuals navigate the tax process more effectively.

This is not true. While the W-7 form is commonly used by non-resident aliens, it is also applicable for resident aliens who do not qualify for a Social Security Number (SSN).

This is incorrect. Individuals can apply for an ITIN for various reasons, including filing a tax return, even if they do not have a job.

Submitting a W-7 does not guarantee an ITIN. The application must meet all requirements, and the IRS reserves the right to deny the application.

This is false. The W-7 form can be submitted at any time of the year, although it is often associated with tax filing deadlines.

This is misleading. Supporting documentation that proves identity and foreign status is required when submitting the W-7 form.

This is incorrect. An ITIN is used for tax purposes only and does not provide eligibility for Social Security benefits or work authorization.

This is not accurate. While an ITIN can be used for tax purposes, it may not be accepted for all financial transactions, such as opening certain bank accounts.

This is misleading. ITINs that have not been used on a federal tax return for three consecutive years may expire and require renewal.

The IRS W-7 (COA) form is essential for individuals seeking to obtain an Individual Taxpayer Identification Number (ITIN). Here are some key takeaways to consider when filling out and using this form: