The importance of understanding the IRS W-2 form cannot be overstated for both employers and employees in the United States. This crucial document, which must be issued by employers to every employee who received a salary, wages, or other types of compensation, serves as a key player in the annual tax filing process. Detailing the amount of money earned by an employee and the taxes withheld from their paycheck throughout the tax year, the W-2 form is indispensable for accurately reporting income and calculating taxes owed or refunds due to taxpayers. Furthermore, it plays a pivotal role in ensuring employees can fully account for their earnings and taxes paid, thus avoiding potential issues with the IRS. Employers are also required to send a copy of this form to the IRS, ensuring that reported earnings match those recorded by the government, which underscores its critical role in the tax reporting ecosystem. The multifaceted aspects of the W-2 form, from its contributions to employee tax filings to its significance in maintaining the integrity of the tax system, highlight the necessity for both employers and employees to fully grasp its contents and implications.

| Fact Name | Description |

|---|---|

| Purpose of Form W-2 | The W-2 form is used by employers to report an employee's annual wages and the amount of taxes withheld from their paycheck. |

| Who Must File | Employers must file a W-2 form for each employee from whom Income, Social Security, or Medicare tax was withheld. |

| Filing Deadline | Employers are required to send the W-2 form to employees by January 31st of the year following the reporting year. |

| Electronic Filing | Employers filing 250 or more W-2 forms are required to submit them electronically to the Social Security Administration. |

| Correction Form | If an employer makes a mistake on a W-2, they must file a W-2c form to correct the information. |

| State-Specific Forms | Some states have their own requirements for state tax reporting, which may involve additional forms or filings beyond the federal W-2. |

| Governing Law(s) | The IRS governs the use and filing of Form W-2 under the Internal Revenue Code. State-specific requirements may be governed by each state's tax code or revenue department guidelines. |

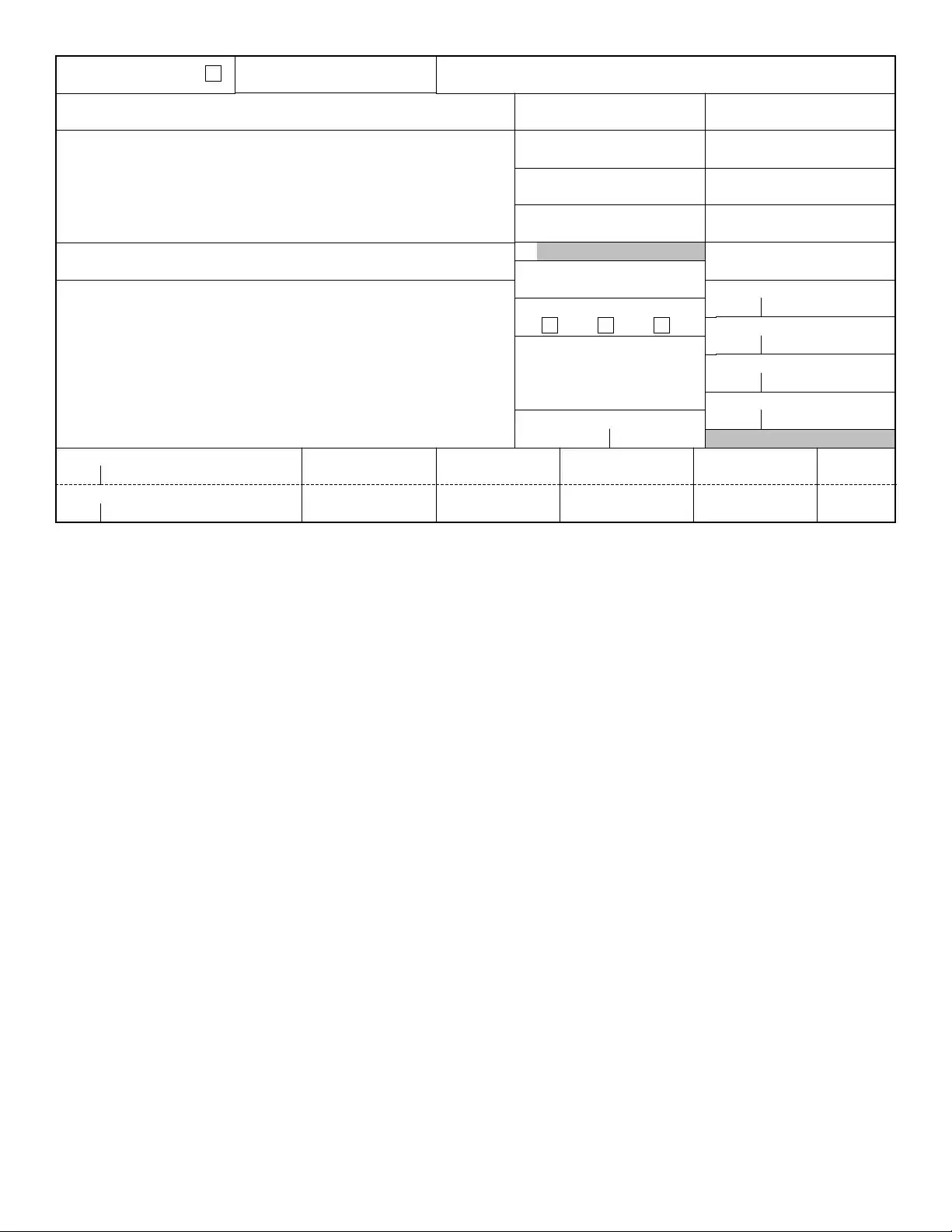

Every year, employers are required to provide a W-2 form to each of their employees. This form plays a critical role in tax filing, as it documents the employee's annual wages and the amount of taxes withheld from their paycheck. Completing the W-2 form accurately is paramount for both the employer's adherence to tax regulation and the employee's ability to file their taxes correctly. The process involves entering detailed financial data. Failure to precisely complete this form can lead to penalties for businesses and confusion for individuals. Here are the crucial steps to fill out the IRS W-2 form:

Completing the W-2 form accurately is essential for ensuring that employees can properly file their taxes and that employers meet their tax filing obligations. It's a yearly task that requires careful attention to detail to avoid issues down the line. Employers should take their time to review the information thoroughly before submitting the forms to their employees and the IRS.

What is a W-2 form?

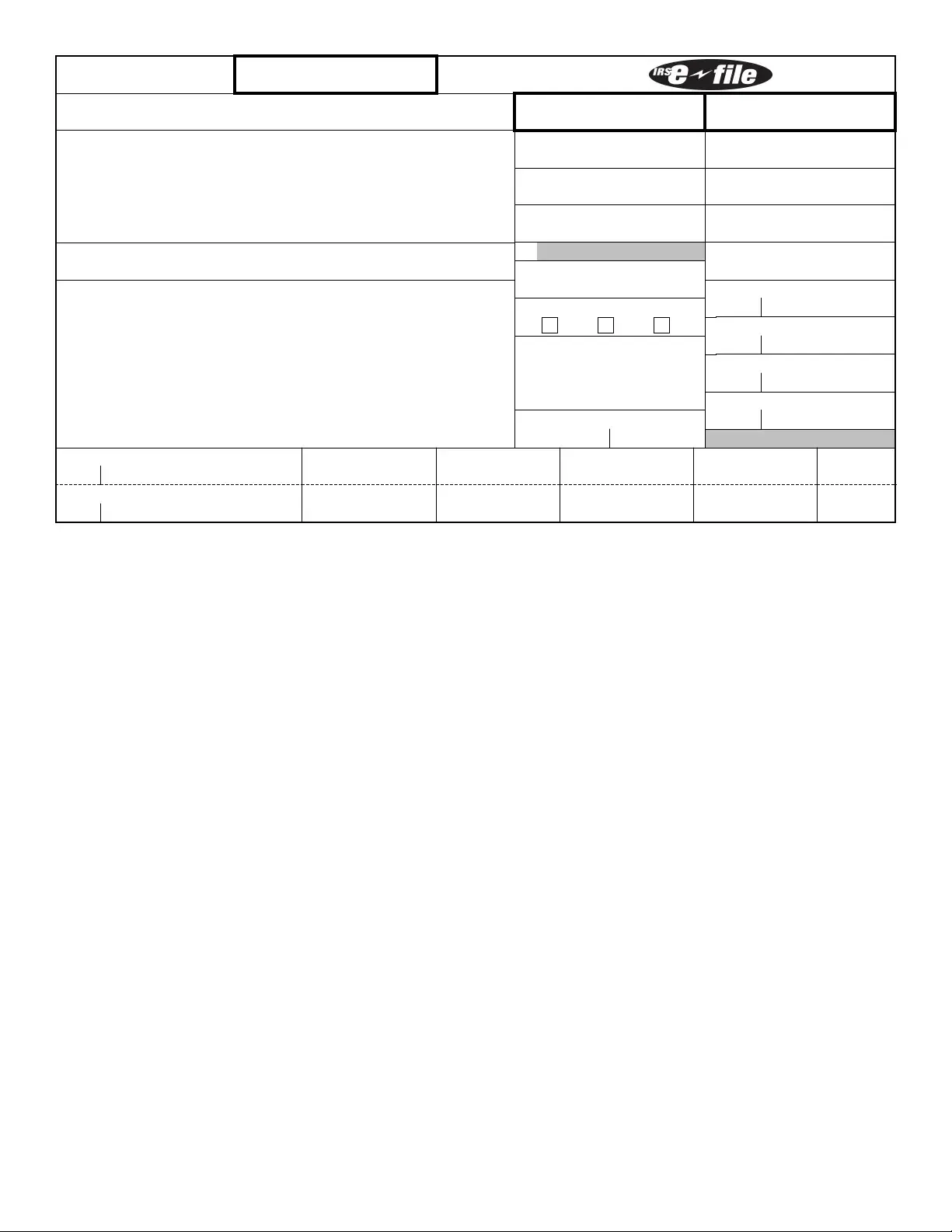

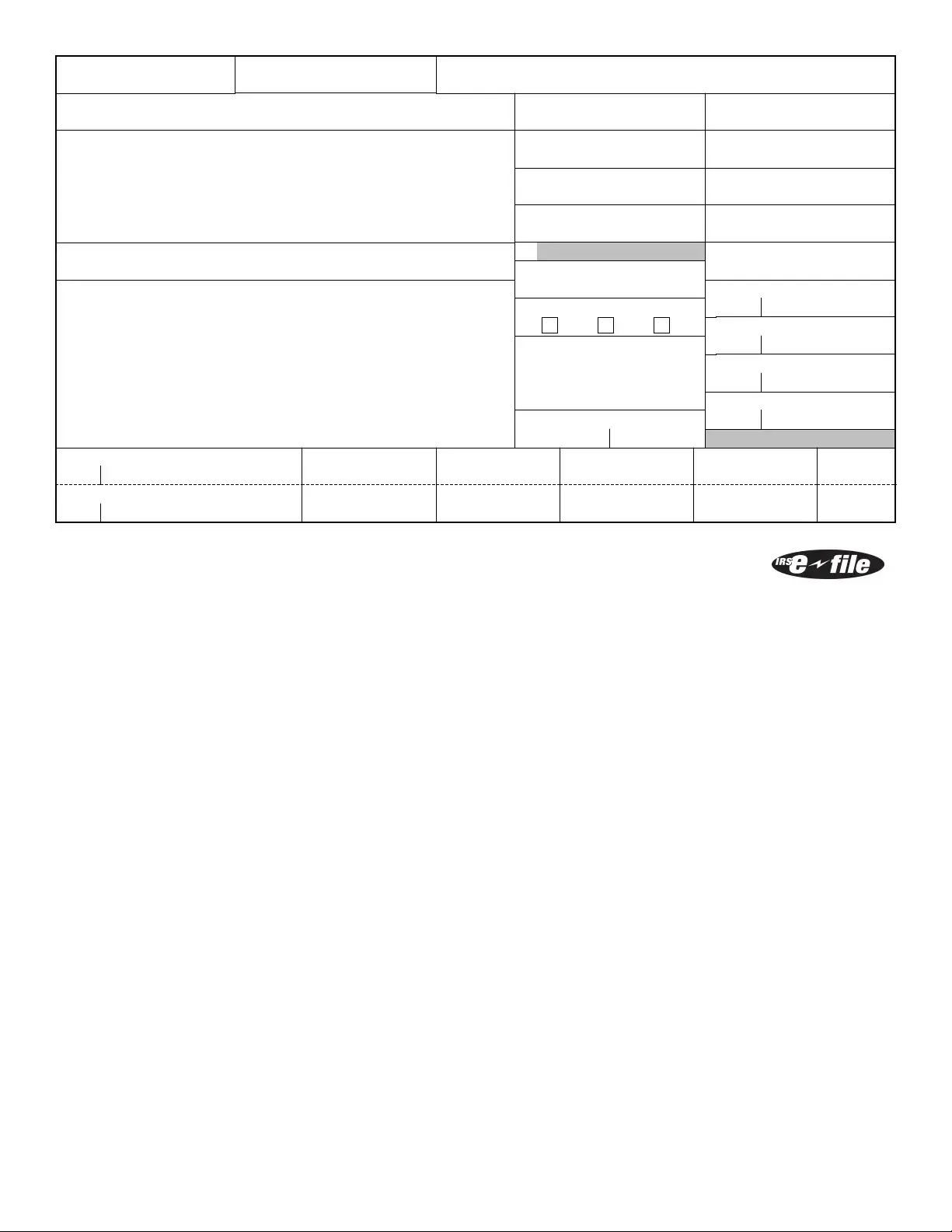

The W-2 form, also known as the Wage and Tax Statement, is a document employers are required to send to each of their employees and the Internal Revenue Service (IRS) at the end of each year. It reports the employee's annual wages and the amount of taxes withheld from their paycheck.

Who receives a W-2 form?

Any employee who has earned a salary, wage, or other compensation from an employer should receive a W-2 form. This applies if you are a full-time or part-time worker and regardless of how long you worked during the year.

When is the W-2 form issued?

Employers are required to send out W-2 forms to their employees by January 31st of the year following the reporting year. For example, for the 2022 tax year, the W-2 forms should be mailed by January 31, 2023.

What should I do if I haven't received my W-2 form?

If you haven't received your W-2 by mid-February, you should first contact your employer to ensure they have your correct address and to request a reissued W-2. If you still do not receive your W-2, you can contact the IRS for assistance.

How is the W-2 form used for tax filing?

The information on the W-2 form is used to fill out your tax return. It includes vital data such as the amount of income you earned, the taxes withheld from your earnings, and contributions to retirement plans, which are necessary for accurately reporting your annual income and determining how much you owe in taxes or how much of a refund you may receive.

What if there are mistakes on my W-2?

If you discover errors on your W-2 form, such as incorrect income or tax amounts, you should immediately contact your employer to issue a corrected W-2. It's important to wait for the corrected W-2 before filing your tax return to avoid processing delays with the IRS.

Can I file my taxes without a W-2?

If you have not received your W-2 in time for tax filing, you may use Form 4852, Substitute for Form W-2, Wage and Tax Statement. However, you should attempt to obtain your W-2 by contacting your employer or the IRS first as estimates can lead to errors in tax filing.

Are there electronic versions of the W-2 form?

Yes, many employers offer electronic versions of the W-2 form through secure websites. Employees can opt to receive their W-2 electronically instead of by mail. These electronic versions are valid documents for tax filing purposes.

What is the difference between a W-2 form and a 1099 form?

The W-2 form is issued to employees whose employer withholds payroll taxes from their earnings. Meanwhile, the 1099 form is used for independent contractors who are responsible for paying their own taxes. The key difference lies in the employment relationship and tax treatment.

How long should I keep my W-2 forms?

It's recommended to keep your W-2 forms for at least three years from the date you filed your income tax return. Holding onto them is important for referencing past income and taxes paid, and they may be needed to amend a previous year's tax return or to apply for certain loans.

Filling out IRS forms, such as the W-2, requires attention to detail and an understanding of tax-related information. Mistakes made during this process can lead to complications with the Internal Revenue Service (IRS) and potentially affect an individual's tax liabilities and financial well-being. Here are four common errors that people often make when completing the W-2 form:

Incorrect Social Security Numbers: One of the most critical yet frequently made errors is providing an incorrect Social Security number. This mistake can lead to misfiled taxes and complications in the individual’s tax record, potentially affecting future benefits.

Failure to Report All Income: Individuals might not report all their income due to oversight or misunderstanding of what constitutes taxable income. This oversight can lead to inaccurate tax reports and potential penalties.

Misclassification of Employees: Employers may mistakenly classify workers as independent contractors instead of employees, or vice versa, leading to improper reporting of wages and taxes withheld. This error impacts not only the employer’s tax liabilities but also the rights and benefits entitled to the worker.

Incorrect Tax Year Information: Another common mistake is filling in information for the wrong tax year. This can happen when forms are prepared manually or preprinted forms from a previous year are used. Such an error complicates the filing process and may lead to the rejection of the form by the IRS.

To ensure accuracy when completing the W-2 form, individuals and employers should double-check the Social Security numbers and tax year, review all documentation for correct income reporting, and understand the distinctions between employee classifications. These steps can help avoid the mistakes listed above and promote a smoother interaction with the IRS.

When tax season approaches, it's important to gather all the necessary documents to ensure a smooth filing process. One of the most well-known forms is the IRS W-2, which reports an employee's annual wages and the amount of taxes withheld from their paycheck. However, to provide a comprehensive view of your financial situation to the IRS, other forms and documents often come into play. These additional documents help clarify your income sources, tax deductions, and investment incomes, among other financial activities.

In addition to the IRS W-2 form, these documents serve as a foundation for individuals to report their financial activities accurately and optimize their tax situation. Gathering all relevant forms and documents before filing taxes can help avoid errors and maximize any potential refunds or reduce tax liabilities. Understanding the purpose of each document can empower one to navigate through tax season with confidence and ease.

IRS Form 1099-MISC: This form is akin to the W-2 in that it reports income. However, while W-2 forms are for employees, 1099-MISC forms are used for independent contractors or freelancers to report payments received for services rendered during the tax year. Both forms are essential for preparing income tax returns.

IRS Form 1099-NEC: Recently distinguished from the 1099-MISC, the 1099-NEC is used to report non-employee compensation, specifically. It parallels the W-2 in its function to report income but is designed for individuals who are not considered employees of the payer, carving out a distinct use similar yet separate from the 1099-MISC.

IRS Form 1099-DIV: This document reports dividends and distributions from investments, comparable to how a W-2 reports wages. Both forms detail income that individuals must report on their tax returns, though the sources of income differ.

IRS Form 1099-INT: Similar to the W-2's role in reporting wages, the 1099-INT form reports interest income from banks and other financial institutions. It's crucial for taxpayers to include information from both forms when filing their annual income tax returns.

IRS Form W-4: The W-4 form is complementary to the W-2 in the employment and tax documentation process. Employees use the W-4 to determine the amount of federal income tax to be withheld from their paychecks, which is later reported on the W-2 form provided by the employer, summarizing the yearly wages and taxes withheld.

IRS Form 1040: The 1040 is the main tax form for individuals, into which information from the W-2 is entered. This form compiles all income types, deductions, and credits to calculate the total tax owed or refund due. The completion of Form 1040 relies on accurate information from forms such as the W-2.

State Income Tax Forms: Many states have their own versions of income tax forms that residents must complete, using information from their W-2 forms. These documents are similar to the W-2 in that they report income and taxes withheld, but are specific to state tax liabilities and credits.

Filling out the IRS W-2 form is an essential task for employers at the beginning of the year, detailing employees' wages and taxes withheld. To ensure accuracy and compliance, it's important to keep in mind what you should and shouldn't do. Here's a helpful guide:

Things You Should Do:

Things You Shouldn't Do:

By following these dos and don'ts, you’ll ensure the W-2 forms are filled out accurately and submitted on time, maintaining compliance and fostering a trustworthy relationship with your employees.

Understanding the IRS W-2 form is crucial for both employees and employers. However, many misconceptions exist about this fundamental document. Let's clear up some of the most common misunderstandings.

Only full-time employees receive a W-2. This is not true. Regardless of whether you are a full-time or part-time employee, if you have received wages, you should receive a W-2 form from your employer. This form reports your annual wages and the amount of taxes withheld from your paycheck.

Freelancers and contractors receive W-2 forms. Actually, freelancers and independent contractors will not receive a W-2. Instead, they should expect to receive a 1099 form from their clients, which details the income they received for services performed.

W-2 forms are only necessary for tax filing. While it's true that the W-2 form is essential for preparing your tax return, it also serves other purposes. For example, it may be required when applying for loans or financial aid, as it provides verification of your income.

Employers have until the end of February to send out W-2 forms. In fact, the deadline for employers to send out W-2 forms to employees is January 31. This ensures that employees have sufficient time to file their taxes before the April 15 tax deadline.

If you don't receive your W-2, you can't file your taxes. If you haven't received your W-2 by mid-February, you should first contact your employer to request a copy. If it's still not received by the end of February, you can contact the IRS for assistance. You may also file your taxes using Form 4852 as a substitute for the W-2.

Incorrect information on a W-2 form is the employee's responsibility. While employees should report any discrepancies or errors to their employer as soon as possible, it is ultimately the employer's responsibility to correct any information on the W-2 forms. Amended forms, known as W-2c, are to be issued for any corrections.

It's important for both employees and employers to be well-informed about the W-2 form to ensure compliance with tax laws and to smooth the tax filing process. Understanding these common misconceptions is a good starting point.

Understanding and accurately completing the IRS W-2 form is crucial for both employers and employees, ensuring compliance with tax regulations and avoiding potential penalties. Here are key takeaways to keep in mind when dealing with the W-2 form:

By attending to these essential points, both employers and employees can navigate the intricacies of the W-2 process more smoothly, maintaining compliance and ensuring the accuracy of their financial records.

Da Form 5988-e - The DA 5988 E form is used for aircraft equipment inspection and maintenance.

Crybaby Complaint Form - List any witnesses who were sympathetic to your feelings.