The IRS SS-8 form plays a crucial role in determining the correct classification of a worker as either an independent contractor or an employee. Misclassification can lead to significant tax implications for both the worker and the employer, making this form an essential tool for clarity. When a business or individual is unsure about a worker's status, filing the SS-8 can provide a formal request for the IRS to review the situation. This process helps ensure compliance with tax laws and can prevent potential penalties. The form requires detailed information about the working relationship, including the nature of the work, the level of control exercised by the employer, and the financial arrangements in place. By completing the SS-8, parties can gain a clearer understanding of their responsibilities and rights under the law, which ultimately fosters a fairer working environment.

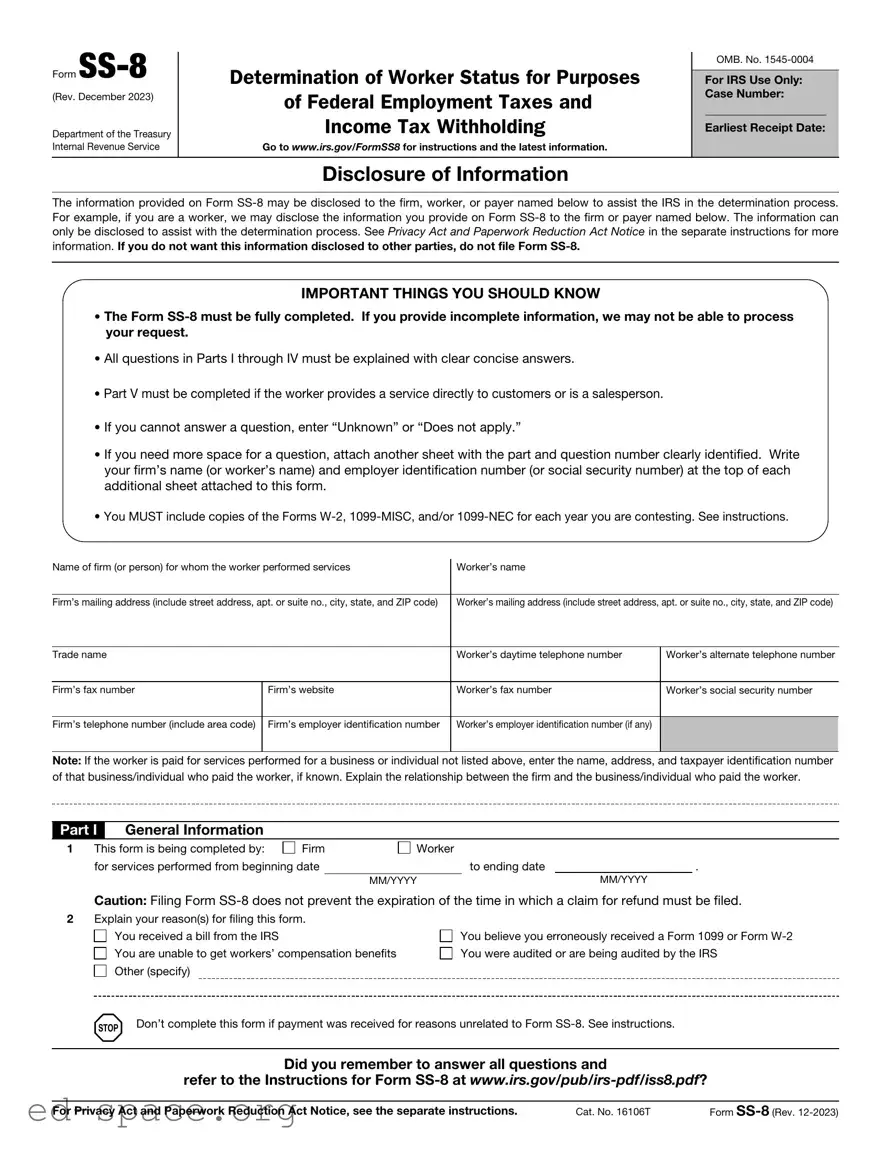

Form

(Rev. December 2023)

Department of the Treasury Internal Revenue Service

Determination of Worker Status for Purposes of Federal Employment Taxes and

Income Tax Withholding

Go to www.irs.gov/FormSS8 for instructions and the latest information.

OMB. No.

For IRS Use Only: Case Number:

Earliest Receipt Date:

Disclosure of Information

The information provided on Form

IMPORTANT THINGS YOU SHOULD KNOW

•The Form

•All questions in Parts I through IV must be explained with clear concise answers.

•Part V must be completed if the worker provides a service directly to customers or is a salesperson.

•If you cannot answer a question, enter “Unknown” or “Does not apply.”

•If you need more space for a question, attach another sheet with the part and question number clearly identified. Write your firm’s name (or worker’s name) and employer identification number (or social security number) at the top of each additional sheet attached to this form.

•You MUST include copies of the Forms

Name of firm (or person) for whom the worker performed services |

Worker’s name |

|

|

|

|

|

|

Firm’s mailing address (include street address, apt. or suite no., city, state, and ZIP code) |

Worker’s mailing address (include street address, apt. or suite no., city, state, and ZIP code) |

||

|

|

|

|

Trade name |

|

Worker’s daytime telephone number |

Worker’s alternate telephone number |

|

|

|

|

Firm’s fax number |

Firm’s website |

Worker’s fax number |

Worker’s social security number |

|

|

|

|

Firm’s telephone number (include area code) |

Firm’s employer identification number |

Worker’s employer identification number (if any) |

|

|

|

|

|

Note: If the worker is paid for services performed for a business or individual not listed above, enter the name, address, and taxpayer identification number of that business/individual who paid the worker, if known. Explain the relationship between the firm and the business/individual who paid the worker.

Part I General Information

1 |

This form is being completed by: |

Firm |

|

for services performed from beginning date |

|

Worker

to ending date |

|

. |

MM/YYYY |

MM/YYYY |

Caution: Filing Form

2Explain your reason(s) for filing this form. You received a bill from the IRS

You are unable to get workers’ compensation benefits

Other (specify)

You believe you erroneously received a Form 1099 or Form

Don’t complete this form if payment was received for reasons unrelated to Form

Did you remember to answer all questions and

refer to the Instructions for Form

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 16106T |

Form |

Form |

Page 2 |

|

Part I |

General Information (continued) |

|

3 Total number of workers who performed or are performing the same or similar services: |

. |

|

4How did the worker obtain the job? Attach any advertisement.

Application |

Bid |

Employment agency |

Other (specify) |

5Attach copies of all supporting documentation (for example, contracts; invoices; memos; Forms

aInform us of any current or past litigation concerning the worker’s status.

bIf no income reporting forms (Form

year(s) at issue $ |

. |

cIf both Form

6Describe the firm’s business.

7Did the worker receive pay from more than one entity (for example, two or more entities with different taxpayer identification numbers) because

of a business sale, merger, acquisition, or reorganization? |

No. Skip to line 8. |

Yes. Complete the rest of line 7. |

|

||

Name of the firm’s previous owner: |

|

|

|

|

|

Previous owner’s taxpayer identification number: |

Change was a: |

Sale |

Merger |

Acquisition |

Reorganization |

Other (specify) |

|

|

|

|

|

Description of above change: |

|

|

|

|

|

8

9

Date of change (MM/DD/YY):

What is the worker’s job title?

Describe the worker’s duties.

Which do you believe the worker is? Check only one. |

Employee |

Independent contractor |

Explain. |

|

|

10 |

Did the worker perform any services for the firm before or after the dates entered on line 1 on page 1 of this form? . . |

Yes |

No |

|

If “Yes,” what were the dates of service? |

|

|

|

If “Yes,” explain any differences between the services provided. |

|

|

11a |

Is the work done under a written agreement between the firm and the worker? |

Yes |

No |

|

If “Yes,” attach a copy (preferably signed by both parties). |

|

|

|

If “Yes,” describe the terms and conditions of the work arrangement. |

|

|

b |

Is the work done under an oral agreement? |

Yes |

No |

|

If “Yes,” describe the details of the agreement. |

|

|

Part II Behavioral Control (Provide names and titles of specific individuals, if applicable.)

1What specific training and/or instruction is the worker given by the firm?

2Who gives the worker work assignments?

How are the assignments received? |

In person |

Phone |

Other (specify) |

|

|

3Who determines the methods by which the assignments are performed?

4If problems or complaints arise, who is contacted? Who is responsible for their resolution?

Text message

Did you remember to answer all questions and

refer to the Instructions for Form

Form

Form |

Page 3 |

|

Part II |

Behavioral Control (Provide names and titles of specific individuals, if applicable.) (continued) |

|

5 |

Is the worker required to complete reports? |

. . . . . . . |

. . . . . . . |

Yes |

||

|

If “Yes,” attach examples. |

|

|

|

|

|

6a |

How frequently does the worker perform services? |

As scheduled |

As needed |

As available |

|

|

|

Other (specify) |

|

|

|

|

|

b |

Describe the worker’s primary services. |

Sales |

Timesheets |

Patient logs |

|

|

|

Other (specify) |

|

|

|

|

|

7Where are the services performed? If more than one location, what percentage of the worker’s time is spent at each location?

Firm premises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Worker’s office or shop . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Customer’s location . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Other (specify)

8a |

Is the worker required to attend meetings? |

. . . . . . . . . . . . . . . . . . |

Yes |

||

|

If “Yes,” what type of meetings? |

Sales |

Staff |

Other (specify) |

|

b |

Is the worker penalized if unable to attend a meeting? . . |

. . . . . . . . . . . . . . . . . . |

Yes |

||

|

If “Yes,” what is the penalty? |

|

|

|

|

No

%

%

%

%

No

No

9 |

Is the worker required to provide the services personally? |

Yes |

No |

|||

10 |

Can the worker hire substitutes or helpers? |

Yes |

No |

|||

11 |

If the worker hires the substitutes or helpers, is approval required? |

Yes |

No |

|||

|

If “Yes,” who approves the hiring? |

Firm |

Other (specify) |

|

|

|

12 |

Does the worker pay substitutes or helpers? |

Yes |

No |

|||

|

If “Yes,” is the worker reimbursed? |

Yes |

No |

|||

|

If the worker is reimbursed, explain who reimburses them. |

|

|

|||

Part III |

Financial Control (Provide names and titles of specific individuals, if applicable.) |

|

|

|||

1a |

List the supplies, equipment, materials, and property provided by |

|

|

|||

|

The firm: |

|

|

|

|

|

|

The worker: |

|

|

|

|

|

b |

Are supplies, equipment, materials, or property provided by another party? |

|||||

|

If “Yes,” explain. |

|

|

|

|

|

2 |

Does the worker lease equipment, space, or a facility? |

|||||

|

If “Yes,” what are the terms of the lease? (Attach a copy or explanatory statement.) |

|

||||

3 |

Are expenses incurred by the worker in the performance of services for the firm? |

|||||

|

If “Yes,” explain. |

|

|

|

|

|

4a |

Are expenses reimbursed by the firm? |

|||||

|

If “Yes,” provide the frequency and amount. |

|

|

|

|

|

b |

Are expenses reimbursed by another party? |

|||||

|

If “Yes,” explain. |

|

|

|

|

|

5a |

What type of pay does the worker receive? |

Salary |

Commission |

Hourly wage |

Piece work |

|

|

Other (specify) |

|

|

|

|

|

b |

If paid commission, does the firm guarantee a minimum amount of pay? |

|||||

|

If “Yes,” explain. |

|

|

|

|

|

6 |

Can the worker request advance pay? |

|||||

|

If “Yes,” how often? |

Daily |

Weekly |

Monthly |

Other (specify) |

|

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Lump sum |

|

Yes |

No |

Yes |

No |

7 |

Whom does the customer pay? |

|||

|

If worker, does the worker pay the total amount to the firm? |

Yes |

No |

If “No,” explain. |

Firm |

Worker |

8 |

Does the firm carry workers’ compensation insurance on the worker? |

Yes |

No |

Did you remember to answer all questions and

refer to the Instructions for Form

Form

Form |

|

Page 4 |

||

Part III |

Financial Control (Provide names and titles of specific individuals, if applicable.) (continued) |

|

|

|

9a |

Does the worker take a financial risk by performing services? |

Yes |

No |

|

|

If “Yes,” explain. |

|

|

|

b |

Can the worker suffer a financial loss by performing services? |

Yes |

No |

|

|

If “Yes,” explain. |

|

|

|

10a Who sets the rate of pay for the services performed?

bIf products are sold, who sets the product price?

Part IV Relationship of the Worker and Firm

Firm Firm

Worker Worker

Other (specify) Other (specify)

1 |

Are benefits made available to the worker? |

. . . . . . . . |

Yes |

No |

||

|

If “Yes,” which benefits are available? |

Paid vacations |

Sick pay |

Paid holidays |

|

|

|

Personal days |

Pensions |

Insurance benefits |

Bonuses |

|

|

|

Other (specify) |

|

|

|

|

|

2 |

Can the firm or worker end the work relationship without penalty? |

. . . . . . . . |

. . . . . . . . |

Yes |

No |

|

|

If “No,” explain. |

|

|

|

|

|

3 |

Did the worker perform similar services for others during the time period entered in Part I, line 1? |

|

If “Yes,” is the worker required to get approval from the firm? |

4 |

Is there an agreement prohibiting competition between the firm and the worker? |

|

If “Yes,” explain or attach available documentation. |

5Reserved for future use.

6 |

Does the worker advertise? |

|||||

|

If “Yes,” what type of advertising does the worker do? Provide copies, if available. |

|

|

|

||

7 |

Does the worker assemble or process a product at home? |

|||||

|

If “Yes,” who provides the materials and instructions or patterns? |

|

|

|

|

|

|

If “Yes,” what does the worker do with the finished product? |

Return to the firm |

Provide to another party |

|||

|

Other (specify) |

|

|

|

|

|

8a |

Does the firm introduce the worker to its customers? |

|||||

|

If “Yes,” how is the worker introduced? |

Employee |

Partner |

Representative |

Contractor |

|

|

Other (specify) |

|

|

|

|

|

b |

Under whose name are services performed? |

Firm |

Worker |

|

|

|

|

Other (specify) |

|

|

|

|

|

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Sell it |

|

Yes |

No |

9 |

Does the worker still perform services for the firm? |

. . . . . . . . . . . . |

. . . . . . . . . |

Yes |

No |

|

|

If “No,” how did the work relationship end? |

Firm ended the work relationship |

Worker ended the work relationship |

|

||

|

Job completed |

Contract ended |

Firm or worker went out of business |

|

|

|

|

Other (specify) |

|

|

|

|

|

Part V For Service Providers or Salespersons. You must complete this part if the worker provided a service directly to customers or is a salesperson.

1 |

Is the worker responsible for contacting potential new customers? |

Yes |

No |

||

|

If “Yes,” what are the worker’s specific responsibilities? |

|

|

|

|

2 |

Is the worker provided leads (names and contact information) for potential new customers? |

Yes |

No |

||

|

If “Yes,” who provides the leads? |

|

|

|

|

3 |

Is the worker required to report on potential new customers contacted? |

Yes |

No |

||

|

If “Yes,” what are the reporting requirements? |

|

|

|

|

4 |

Does the firm set terms and conditions of sale? |

Yes |

No |

||

|

If “Yes,” explain. |

|

|

|

|

5 |

Are orders submitted and subject to the firm’s approval? |

Yes |

No |

||

6 |

Who determines the worker’s sales territory? |

Firm |

Worker |

|

|

|

Other (specify) |

|

|

|

|

Did you remember to answer all questions and

refer to the Instructions for Form

Form

Form |

Page 5 |

Part V For Service Providers or Salespersons. You must complete this part if the worker provided a service directly to customers or is a salesperson. (continued)

7 |

Did the worker pay for the privilege of serving customers on the route or in the territory? . |

. . . . . |

. . . . |

Yes |

No |

||

|

If “Yes,” whom did the worker pay? |

|

|

|

|

|

|

|

If “Yes,” how much did the worker pay? |

. . . . . |

$ |

|

|

||

8 |

Where does the worker sell the product? |

Home |

Retail establishment |

Online |

|

|

|

|

Other (specify) |

|

|

|

|

|

|

9List the product and/or services distributed by the worker (for example, meat, vegetables, fruit, bakery products, beverages, or laundry or dry cleaning services). If more than one type of product and/or service is distributed, specify the principal one.

10 |

Does the worker sell life insurance full time? |

Yes |

No |

11 |

Does the worker sell other types of insurance for the firm? |

Yes |

No |

|

If “Yes,” enter the percentage of the worker’s total working time spent in selling other types of insurance |

|

% |

12Does the worker solicit orders from wholesalers, retailers, contractors, or operators of hotels, restaurants, or other similar

|

establishments? |

Yes |

No |

|

If “Yes,” what percentage of the worker’s time is spent in solicitation? |

|

% |

13 |

Is the merchandise purchased by the customers for resale or use in their business operations? |

Yes |

No |

|

Describe the merchandise and state whether it is equipment installed on the customers’ premises. |

|

|

Sign Here

Under penalties of perjury, I declare that I have examined this request, including accompanying documents, and to the best of my knowledge and belief, the facts presented are true, correct, and complete.

Print your name |

|

Signature |

|

Date |

Did you remember to answer all questions and

refer to the Instructions for Form

Did you sign Form

Did you attach copies of your Form

Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS SS-8 form is used to determine a worker's status as an employee or an independent contractor for tax purposes. |

| Who Can File | Any individual or business can file the SS-8 form if there is uncertainty about a worker's classification. |

| Filing Deadline | There is no specific deadline for filing the SS-8, but it should be submitted as soon as the classification issue arises. |

| Processing Time | The IRS typically takes about 30 days to process the SS-8 form and provide a determination. |

| Binding Decision | The IRS's determination is binding for federal tax purposes but may not apply to state tax classifications. |

| State-Specific Forms | Some states have their own forms for worker classification, governed by laws such as California's AB 5 and New York's Labor Law. |

| Additional Resources | The IRS provides guidance and FAQs on its website to help users understand how to complete the SS-8 form. |

Completing the IRS SS-8 form is an important step for individuals seeking clarity on their employment status. This form helps determine whether a worker is an independent contractor or an employee for tax purposes. After filling out the form, it will be submitted to the IRS for review, and a determination will be made regarding the classification.

What is the IRS SS-8 form?

The IRS SS-8 form is used to determine whether an individual is an independent contractor or an employee for federal tax purposes. This form helps clarify the classification of a worker's status, which can affect tax obligations and eligibility for certain benefits.

Who should file the SS-8 form?

Any worker who is uncertain about their employment status can file the SS-8 form. Additionally, employers may submit this form if they are unsure about the classification of a worker. It is important for both parties to ensure compliance with tax regulations.

How do I complete the SS-8 form?

The SS-8 form requires detailed information about the working relationship between the worker and the employer. This includes the nature of the work performed, the degree of control the employer has over the worker, and the financial arrangements. Each section must be filled out accurately to provide the IRS with the necessary context for their determination.

Where do I send the completed SS-8 form?

Once completed, the SS-8 form should be mailed to the address specified in the form's instructions. Typically, this is the IRS office that handles employment tax issues. It is advisable to keep a copy of the submitted form for your records.

How long does it take to receive a determination after filing the SS-8?

The IRS usually takes about 90 days to process the SS-8 form and issue a determination. However, the processing time may vary based on the volume of requests and the complexity of the case.

What happens after the IRS makes a determination?

After the IRS issues a determination, both the worker and employer will receive a written response. This letter will outline the classification of the worker as either an independent contractor or an employee, which will guide tax reporting and compliance moving forward.

Can I appeal the IRS's determination from the SS-8 form?

If a party disagrees with the IRS's determination, they may appeal the decision. The appeal process typically involves submitting additional documentation and may require a formal request for reconsideration. Specific procedures and timelines can be found in the IRS guidelines.

Is there a fee to file the SS-8 form?

There is no fee associated with filing the SS-8 form. It is a free service provided by the IRS to help clarify employment status and ensure proper tax treatment.

Not providing complete information. Many individuals fail to fill out all sections of the form, which can lead to delays in processing.

Incorrectly classifying the worker's status. Misunderstanding the difference between an independent contractor and an employee can result in the wrong designation.

Failing to attach necessary documentation. Supporting documents can help clarify the relationship and should be included when applicable.

Using outdated forms. It's essential to ensure that the most current version of the IRS SS-8 form is being used to avoid complications.

Neglecting to sign and date the form. An unsigned form will not be processed, so this step is crucial.

Providing inconsistent information. Discrepancies in the details can lead to confusion and may require additional clarification.

Not following the instructions carefully. Each section has specific requirements, and overlooking them can lead to mistakes.

The IRS SS-8 form is used to determine a worker's status as an independent contractor or employee for tax purposes. Along with the SS-8, several other forms and documents may be necessary to provide additional context or support. Here’s a list of related forms that you might encounter:

Understanding these forms can help clarify the relationship between workers and employers, especially when determining tax obligations and worker classification. Each document serves a specific purpose and contributes to a comprehensive understanding of employment and tax responsibilities.

The IRS SS-8 form is a crucial document used to determine a worker's classification as either an employee or an independent contractor. Several other documents serve similar purposes in various contexts. Below is a list of six documents that share similarities with the IRS SS-8 form:

When filling out the IRS SS-8 form, it’s important to be thorough and accurate. Here are some key dos and don’ts to keep in mind:

The IRS SS-8 form is often misunderstood. Here are ten common misconceptions about this important document.

This form is used to determine the status of a worker, whether they are an employee or an independent contractor. It applies to both categories.

The IRS will review the information provided and make a determination based on the facts. There is no guarantee of a particular classification.

This form can be filed proactively if you are unsure of your status, even without a dispute.

While it does have tax implications, the form is primarily used to clarify employment status under IRS guidelines.

Any worker can file the SS-8 form, regardless of their employer's actions.

There is no strict deadline, but it is advisable to file it as soon as you have concerns about your employment status.

It applies across all industries where there is a question about worker classification.

While legal advice can be helpful, individuals can complete and file the form on their own.

The IRS evaluates each case based on its merits and the information provided, regardless of the employer's position.

You can submit additional information or clarification if circumstances change after filing.

Understanding these misconceptions can help individuals navigate their employment status more effectively. The SS-8 form serves as a valuable tool for ensuring clarity and compliance with IRS regulations.

The IRS SS-8 form is used to determine the correct classification of workers as either employees or independent contractors. Below are key takeaways regarding its use and completion:

By understanding these key points, individuals and businesses can navigate the complexities of worker classification more effectively.