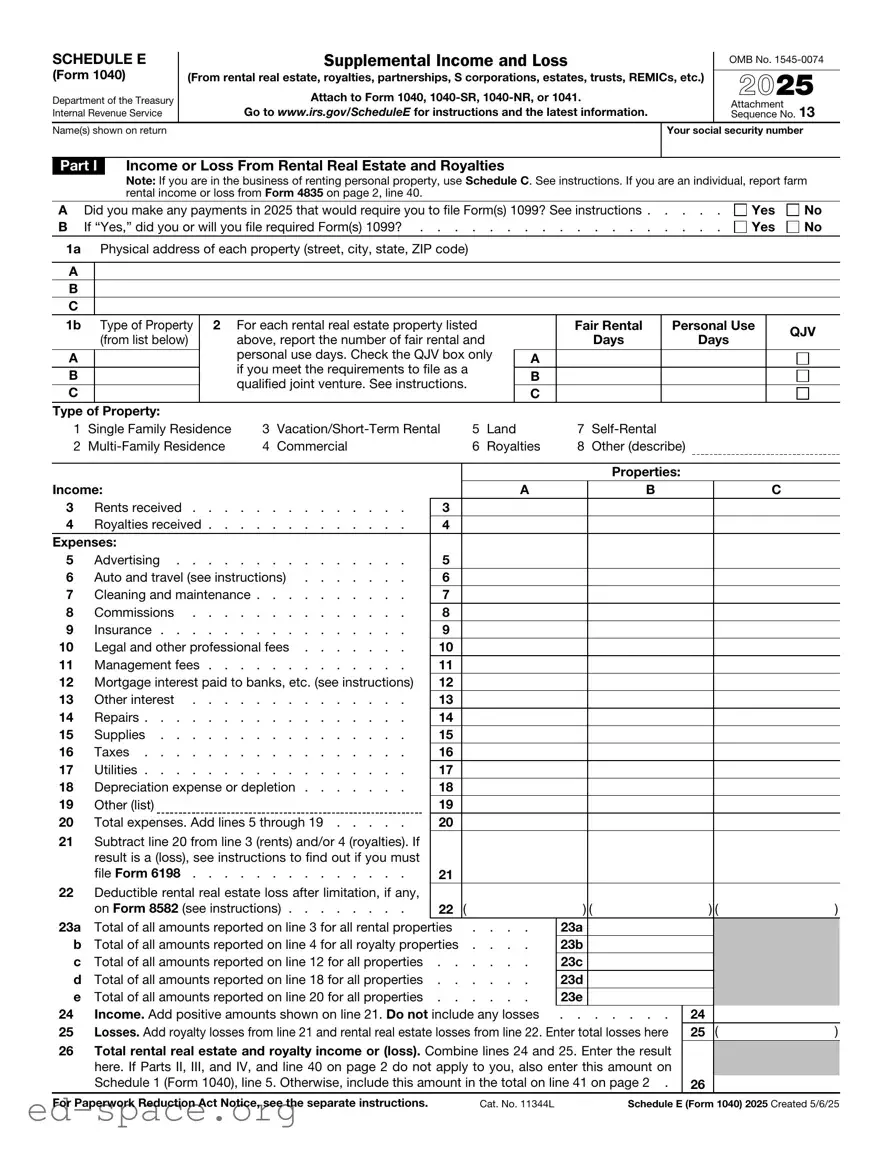

The IRS Schedule E (Form 1040) serves as an important tool for individuals who earn income from various sources beyond traditional employment. This form is primarily used to report income or loss from rental real estate, partnerships, S corporations, estates, trusts, and other pass-through entities. Taxpayers must provide detailed information about their income and expenses related to these activities, ensuring that all relevant financial information is accurately captured. Additionally, Schedule E allows for the deduction of certain expenses, which can help reduce the overall taxable income. Understanding the nuances of this form is crucial for anyone involved in rental properties or business partnerships, as it impacts their tax obligations and financial planning. Proper completion of Schedule E not only aids in compliance with tax laws but also provides an opportunity for individuals to optimize their tax situation.

SCHEDULE E |

|

|

|

|

Supplemental Income and Loss |

|

|

|

|

OMB No. |

||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||

(Form 1040) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

(From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) |

|

2025 |

||||||||||||||||||||

Department of the Treasury |

|

|

|

|

Attach to Form 1040, |

|

|

|

||||||||||||||||

Internal Revenue Service |

|

|

|

Go to www.irs.gov/ScheduleE for instructions and the latest information. |

|

|

Attachment |

|

13 |

|||||||||||||||

|

|

|

|

|

Sequence No. |

|||||||||||||||||||

Name(s) shown on return |

|

|

|

|

|

|

|

|

|

|

|

Your social security number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Part I |

|

Income or Loss From Rental Real Estate and Royalties |

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

Note: If you are in the business of renting personal property, use Schedule C. See instructions. If you are an individual, report farm |

||||||||||||||||||||

|

|

|

|

rental income or loss from Form 4835 on page 2, line 40. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

A |

Did you make any payments in 2025 that would require you to file Form(s) 1099? See instructions . |

. . . . |

Yes |

|

No |

|||||||||||||||||||

B |

If “Yes,” did you or will you file required Form(s) 1099? . |

. . . . . . . . . . . . . |

. . . . |

Yes |

|

No |

||||||||||||||||||

1a Physical address of each property (street, city, state, ZIP code) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

Type of Property |

2 |

For each rental real estate property listed |

|

|

|

|

Fair Rental |

Personal Use |

|

QJV |

||||||||||||

|

|

(from list below) |

|

above, report the number of fair rental and |

|

|

|

|

|

Days |

Days |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

personal use days. Check the QJV box only |

|

|

|

|

|

|

|

|

|

|

|

|||||

A |

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

if you meet the requirements to file as a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

qualified joint venture. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Type of Property: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

1 |

Single Family Residence |

3 |

5 |

Land |

|

|

7 |

|

|

|

|

|

|

|||||||||||

2 |

4 |

Commercial |

|

|

6 |

Royalties |

8 |

Other (describe) |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Properties: |

|

|

|

|

||

Income: |

|

|

|

|

|

|

|

|

|

|

|

A |

|

B |

|

|

|

C |

|

|

||||

3 |

|

Rents received |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

4 |

|

Royalties received |

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

Advertising |

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

6 |

|

Auto and travel (see instructions) |

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

7 |

|

Cleaning and maintenance |

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

8 |

|

Commissions |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

9 |

|

Insurance |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

10 |

|

Legal and other professional fees |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

11 |

|

Management fees |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

12 |

|

Mortgage interest paid to banks, etc. (see instructions) |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

13 |

|

Other interest |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

14 |

|

Repairs |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

15 |

|

Supplies |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

16 |

|

Taxes |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

17 |

|

Utilities |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

18 |

|

Depreciation expense or depletion |

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

19 |

|

Other (list) |

|

|

19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

20 |

|

Total expenses. Add lines 5 through 19 |

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

21Subtract line 20 from line 3 (rents) and/or 4 (royalties). If result is a (loss), see instructions to find out if you must

file Form 6198 |

21 |

22Deductible rental real estate loss after limitation, if any,

|

on Form 8582 (see instructions) |

22 ( |

) ( |

|

) ( |

) |

23a |

Total of all amounts reported on line 3 for all rental properties . . . . |

23a |

|

|

|

|

b |

Total of all amounts reported on line 4 for all royalty properties . . . . |

23b |

|

|

|

|

c |

Total of all amounts reported on line 12 for all properties |

23c |

|

|

|

|

d |

Total of all amounts reported on line 18 for all properties |

23d |

|

|

|

|

e |

Total of all amounts reported on line 20 for all properties |

23e |

|

|

|

|

24 |

Income. Add positive amounts shown on line 21. Do not include any losses |

. . . . . . . |

24 |

|

|

|

25 |

Losses. Add royalty losses from line 21 and rental real estate losses from line 22. Enter total losses here |

25 |

( |

) |

||

26Total rental real estate and royalty income or (loss). Combine lines 24 and 25. Enter the result here. If Parts II, III, and IV, and line 40 on page 2 do not apply to you, also enter this amount on

Schedule 1 (Form 1040), line 5. Otherwise, include this amount in the total on line 41 on page 2 . |

26 |

||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11344L |

Schedule E (Form 1040) 2025 Created 5/6/25 |

|

Schedule E (Form 1040) 2025 |

Attachment Sequence No. 13 |

Page 2 |

Name(s) shown on return. Do not enter name and social security number if shown on other side. |

Your social security number |

|

Caution: The IRS compares amounts reported on your tax return with amounts shown on Schedule(s)

Part II Income or Loss From Partnerships and S Corporations

Note: If you report a loss, receive a distribution, dispose of stock, or receive a loan repayment from an S corporation, you must check the box in column (e) on line 28 and attach the required basis computation. If you report a loss from an

27Are you reporting any loss not allowed in a prior year due to the

passive activity (if that loss was not reported on Form 8582), or unreimbursed partnership expenses? If you answered “Yes,”

see instructions before completing this section |

Yes |

No |

28

A

B

C

D

(a)Name

(b)Enter P for partnership; S

for S corporation

(c)Check if foreign

partnership

(d)Employer

identification number

(e)Check if

basis computation

is required

(f)Check if any amount is

not at risk

|

|

Passive Income and Loss |

Nonpassive Income and Loss |

|

|||||

|

(g) Passive loss allowed |

(h) Passive income |

(i) Nonpassive loss allowed |

|

(j) Section 179 expense |

(k) Nonpassive income |

|||

|

(attach Form 8582 if required) |

from Schedule |

(see Schedule |

|

deduction from Form 4562 |

from Schedule |

|||

A |

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

29a |

Totals |

|

|

|

|

|

|

|

|

b |

Totals |

|

|

|

|

|

|

|

|

30 |

Add columns (h) and (k) of line 29a |

. . . . . . . . . |

|

. . . . . . |

30 |

|

|

||

31 |

Add columns (g), (i), and (j) of line 29b |

. . . . . . . . . |

|

. . . . . . |

31 ( |

) |

|||

32 |

Total partnership and S corporation income or (loss). Combine lines 30 and 31 |

. . . . . |

32 |

|

|

||||

Part III Income or Loss From Estates and Trusts

33

A

B

(a)Name

(b)Employer

identification number

|

|

|

Passive Income and Loss |

|

Nonpassive Income and Loss |

|

|||||

|

|

(c) Passive deduction or loss allowed |

|

(d) Passive income |

|

(e) Deduction or loss |

|

(f) Other income from |

|

||

|

|

|

(attach Form 8582 if required) |

|

from Schedule |

|

from Schedule |

|

Schedule |

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

34a |

Totals |

|

|

|

|

|

|

|

|

|

|

b |

Totals |

|

|

|

|

|

|

|

|

|

|

35 |

Add columns (d) and (f) of line 34a |

. . . . . . . . . . . . |

35 |

|

|

||||||

36 |

Add columns (c) and (e) of line 34b |

. . . . . . . . . . . . |

36 |

( |

) |

||||||

37 |

Total estate and trust income or (loss). Combine lines 35 and 36 |

37 |

|

|

|||||||

Part IV |

Income or Loss From Real Estate Mortgage Investment Conduits |

Holder |

|

||||||||

38 |

|

|

(a) Name |

|

(b) Employer |

(c) Excess inclusion from |

(d) Taxable income |

(e) Income from |

|

||

|

|

|

|

identification number |

Schedules Q, line 2c |

(net loss) from |

|

Schedules Q, line 3b |

|

||

|

|

|

|

|

(see instructions) |

Schedules Q, line 1b |

|

||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

||||

39 |

Combine columns (d) and (e) only. Enter |

the result here and include in the total on line 41 below . |

39 |

|

|

||||||

Part V |

Summary |

|

|

|

|

|

|

|

|

||

40 |

Net farm rental income or (loss) from Form 4835. Also, complete line 42 below |

40 |

|

|

|||||||

41Total income or (loss). Combine lines 26, 32, 37, 39, and 40. Enter the result here and on Schedule

1 (Form 1040), line 5 |

. . . . . . . . . |

41 |

|

42 Reconciliation of farming and fishing income. Enter your gross |

|

|

|

farming and fishing income reported on Form 4835, line 7; Schedule |

|

|

|

(Form 1065), box 14, code B; Schedule |

|

|

|

AN; and Schedule |

42 |

|

|

43 Reconciliation for real estate professionals. If you were a real estate |

|

|

|

professional (see instructions), enter the net income or (loss) you |

|

|

|

reported anywhere on Form 1040, Form |

|

|

|

from all rental real estate activities in which you materially participated |

|

|

|

under the passive activity loss rules |

43 |

|

|

Schedule E (Form 1040) 2025

| Fact Name | Description |

|---|---|

| Purpose | Schedule E is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and more. |

| Filing Requirement | Taxpayers must file Schedule E if they receive income from rental properties or pass-through entities. |

| Income Reporting | All rental income must be reported, including payments received for services related to rental properties. |

| Expenses | Taxpayers can deduct expenses related to the rental activity, such as repairs, property management fees, and mortgage interest. |

| Loss Limitations | Passive activity loss rules may limit the ability to deduct losses from rental properties against other income. |

| State-Specific Forms | Some states require additional forms for reporting rental income. Check state tax laws for specific requirements. |

| Filing Deadline | Schedule E must be filed by the tax return deadline, typically April 15, unless an extension is granted. |

| Record Keeping | Taxpayers should maintain accurate records of income and expenses to support the information reported on Schedule E. |

Filling out the IRS Schedule E (Form 1040) is an important step for individuals reporting income from rental properties, partnerships, S corporations, estates, trusts, and more. Once you have completed this form, you will be able to accurately report your income and expenses, which can impact your overall tax liability.

What is IRS Schedule E used for?

IRS Schedule E is primarily used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs (Real Estate Mortgage Investment Conduits). This form allows taxpayers to detail their earnings from these sources and helps the IRS assess the appropriate tax obligations. It is an essential part of the Form 1040, which is the standard individual income tax return.

Who needs to file Schedule E?

Individuals who earn income from rental properties, partnerships, or other similar sources must file Schedule E. If you own rental real estate, you need to report any rental income and expenses associated with that property. Additionally, if you are a partner in a partnership or a shareholder in an S corporation, you must report your share of the income or loss from those entities on this form.

What information do I need to complete Schedule E?

To fill out Schedule E, gather details about your rental properties or other income sources. This includes the address of the property, the total rental income received, and any expenses incurred, such as repairs, maintenance, property management fees, and mortgage interest. If you are reporting income from a partnership or S corporation, you will need the Schedule K-1 form, which outlines your share of the income or loss from that entity.

Can I deduct expenses on Schedule E?

Yes, you can deduct a variety of expenses related to your rental properties or other income-generating activities on Schedule E. Common deductible expenses include property management fees, repairs, depreciation, mortgage interest, and property taxes. It is important to keep accurate records of all expenses to ensure that you can substantiate your deductions if required by the IRS.

How does Schedule E affect my overall tax return?

The information reported on Schedule E flows through to your Form 1040, impacting your total taxable income. If you report a profit, it will increase your taxable income, potentially raising your tax liability. Conversely, if you report a loss, it may reduce your overall taxable income, potentially lowering your tax bill. Understanding how your rental or partnership income interacts with your overall financial situation is crucial for effective tax planning.

Not Reporting All Rental Income: Many individuals forget to include all sources of rental income. This can include payments received for renting out a room, vacation properties, or even short-term rentals. It’s crucial to report every dollar earned to avoid penalties.

Incorrectly Categorizing Expenses: Some people misclassify their expenses. For instance, repairs and maintenance costs might be mixed up with improvements. Understanding the difference can significantly affect your tax liability.

Failing to Keep Accurate Records: Without proper documentation, it becomes challenging to substantiate your claims. Keeping receipts and records of all transactions related to your rental properties is essential for accurate reporting.

Omitting Depreciation: Depreciation is a valuable deduction that many overlook. Failing to calculate and report depreciation can lead to missed tax benefits. It’s important to understand how to apply this deduction correctly.

Ignoring Passive Activity Loss Rules: Some taxpayers do not consider the passive activity loss rules. These rules limit the amount of losses you can deduct from your rental properties. Being aware of these restrictions can help avoid unexpected tax consequences.

Not Consulting Tax Professionals: Many individuals attempt to fill out Schedule E without seeking professional help. This can lead to mistakes that may have been easily avoided with expert advice. Consulting a tax professional can provide clarity and ensure compliance.

Missing Deadlines: Filing Schedule E on time is crucial. Missing the deadline can result in penalties and interest on unpaid taxes. Staying organized and aware of filing dates can prevent these issues.

When preparing your tax return, especially if you're reporting income or losses from rental properties or partnerships, you may need to use several other forms and documents in conjunction with the IRS Schedule E (Form 1040). Each of these documents serves a specific purpose and helps ensure that your tax return is complete and accurate.

Understanding these forms and documents can simplify the tax preparation process. By gathering the necessary information and ensuring that all relevant forms are completed, you can help make your tax filing experience smoother and more efficient.

The IRS Schedule E (Form 1040) is primarily used to report income or loss from rental real estate, partnerships, S corporations, estates, trusts, and other sources. Here are four documents that are similar to Schedule E, along with explanations of how they relate:

When filling out the IRS Schedule E (Form 1040), it is essential to approach the task with care. Here are some important dos and don'ts to keep in mind:

By following these guidelines, you can help ensure that your Schedule E is filled out correctly and completely, minimizing the risk of errors and potential issues with the IRS.

Understanding the IRS Schedule E (Form 1040) can be challenging. Here are eight common misconceptions about this form, along with clarifications to help you navigate it more easily.

While many landlords use Schedule E to report rental income, it also applies to individuals with income from partnerships, S corporations, estates, trusts, and royalties.

In addition to rental expenses, you can deduct certain expenses related to partnerships and other income-generating activities reported on Schedule E.

Not all rental income is fully taxable. For example, if you rent out a property for less than 15 days in a year, you may not need to report that income.

While it may seem complex, many individuals can complete Schedule E on their own with proper documentation and understanding of their income sources.

In fact, you can claim depreciation on rental properties, which can significantly reduce your taxable income.

You do need to report income and expenses, but not every expense needs to be itemized separately. You can group similar expenses.

Entities like partnerships and S corporations also use Schedule E to report their income and losses.

Filing this form does not automatically trigger an audit. Audits are based on various factors, not just the forms you file.

By clearing up these misconceptions, you can approach your tax filing with more confidence and accuracy.

When filling out and using the IRS Schedule E (Form 1040), keep these key takeaways in mind: