The IRS 8832 form is an essential tool for businesses looking to change their tax classification. By submitting this form, entities can elect to be treated as a corporation, partnership, or disregarded entity for federal tax purposes. This flexibility allows businesses to choose the tax structure that best fits their needs and goals. Understanding the implications of this choice is crucial, as it can affect how profits are taxed and how losses are handled. The form requires specific information about the entity, including its name, address, and the type of election being made. Additionally, it must be signed by an authorized person, ensuring that the decision is official and binding. Filing the IRS 8832 can seem daunting, but with the right information and guidance, it can be a straightforward process that opens up new opportunities for growth and financial management.

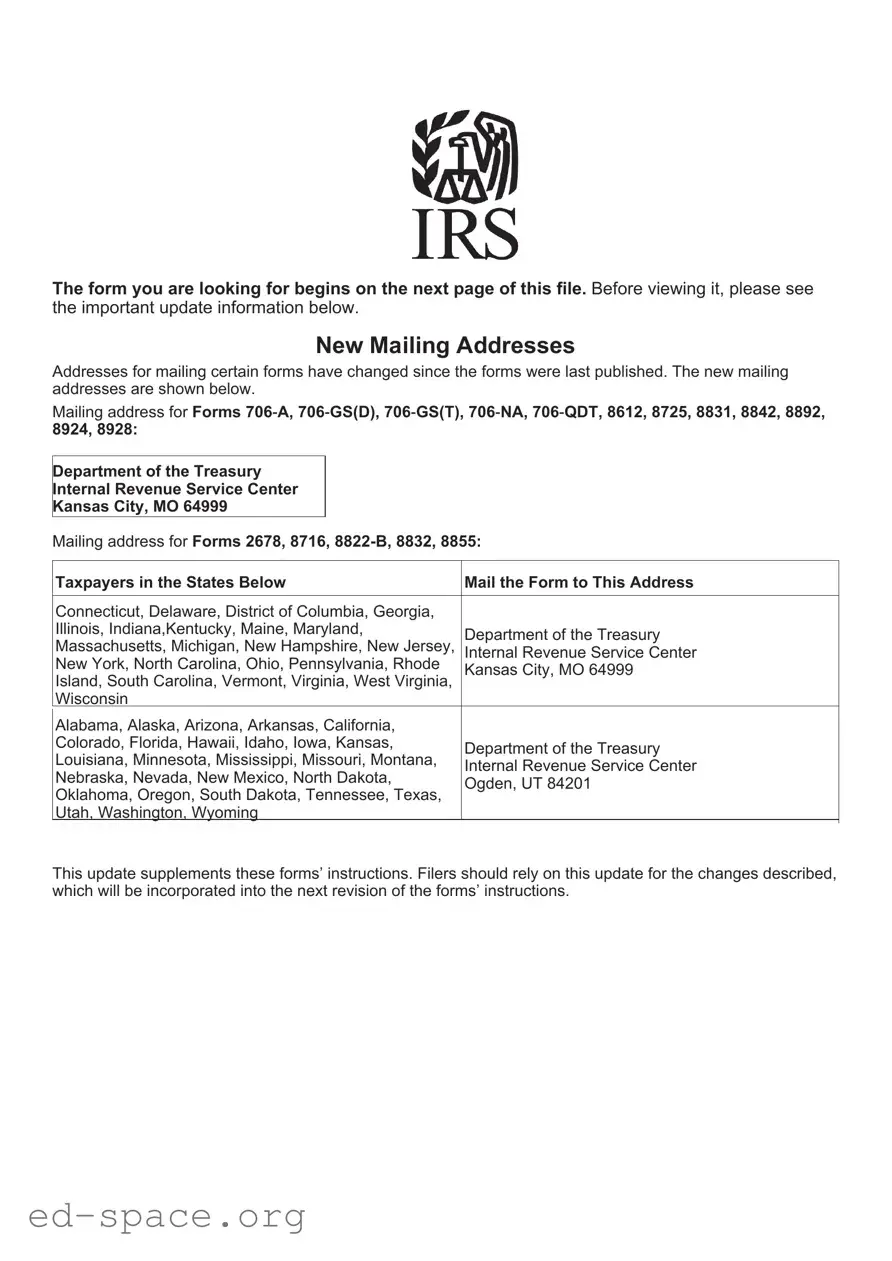

The form you are looking for begins on the next page of this file. Before viewing it, please see

the important update information below.

New Mailing Addresses

Addresses for mailing certain forms have changed since the forms were last published. The new mailing addresses are shown below.

Mailing address for Forms 706͈A, 706͈GS(D), 706͈GS(T), 706͈NA, 706͈QDT, 8612, 8725, 8831, 8842, 8892, 8924, 8928:

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999

Mailing address for Forms 2678, 8716,

|

Taxpayers in the States Below |

Mail the Form to This Address |

|

Connecticut, Delaware, District of Columbia, Georgia, |

|

|

Illinois, Indiana,Kentucky, Maine, Maryland, |

Department of the Treasury |

|

Massachusetts, Michigan, New Hampshire, New Jersey, |

|

|

Internal Revenue Service Center |

|

|

New York, North Carolina, Ohio, Pennsylvania, Rhode |

Kansas City, MO 64999 |

|

Island, South Carolina, Vermont, Virginia, West Virginia, |

|

|

Wisconsin |

|

|

Alabama, Alaska, Arizona, Arkansas, California, |

|

|

|

|

|

Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, |

Department of the Treasury |

|

Louisiana, Minnesota, Mississippi, Missouri, Montana, |

|

|

Internal Revenue Service Center |

|

|

Nebraska, Nevada, New Mexico, North Dakota, |

|

|

Ogden, UT 84201 |

|

|

Oklahoma, Oregon, South Dakota, Tennessee, Texas, |

|

|

|

|

|

Utah, Washington, Wyoming |

|

|

|

|

This update supplements these forms’ instructions. Filers should rely on this update for the changes described, which will be incorporated into the next revision of the forms’ instructions.

Form 8832

(Rev. December 2013)

Department of the Treasury Internal Revenue Service

Entity Classification Election

Information about Form 8832 and its instructions is at www.irs.gov/form8832.

OMB No.

Type

or

Name of eligible entity making election |

Employer identification number |

|

|

Number, street, and room or suite no. If a P.O. box, see instructions.

City or town, state, and ZIP code. If a foreign address, enter city, province or state, postal code and country. Follow the country’s practice for entering the postal code.

Check if:

Address change |

Late classification relief sought under Revenue Procedure |

Relief for a late change of entity classification election sought under Revenue Procedure

Part I Election Information

1Type of election (see instructions):

a Initial classification by a

b Change in current classification. Go to line 2a.

2a Has the eligible entity previously filed an entity election that had an effective date within the last 60 months?

Yes. Go to line 2b.

No. Skip line 2b and go to line 3.

2b

3

Was the eligible entity’s prior election an initial classification election by a newly formed entity that was effective on the date of formation?

Yes. Go to line 3.

No. Stop here. You generally are not currently eligible to make the election (see instructions).

Does the eligible entity have more than one owner?

Yes. You can elect to be classified as a partnership or an association taxable as a corporation. Skip line 4 and go to line 5.

No. You can elect to be classified as an association taxable as a corporation or to be disregarded as a separate entity. Go to line 4.

4If the eligible entity has only one owner, provide the following information:

aName of owner

bIdentifying number of owner

5If the eligible entity is owned by one or more affiliated corporations that file a consolidated return, provide the name and employer identification number of the parent corporation:

aName of parent corporation

bEmployer identification number

For Paperwork Reduction Act Notice, see instructions. |

Cat. No. 22598R |

Form 8832 (Rev. |

Form 8832 (Rev. |

Page 2 |

|

Part I |

Election Information (Continued) |

|

6Type of entity (see instructions):

a A domestic eligible entity electing to be classified as an association taxable as a corporation.

b A domestic eligible entity electing to be classified as a partnership.

c A domestic eligible entity with a single owner electing to be disregarded as a separate entity.

d A foreign eligible entity electing to be classified as an association taxable as a corporation.

e A foreign eligible entity electing to be classified as a partnership.

f A foreign eligible entity with a single owner electing to be disregarded as a separate entity.

7If the eligible entity is created or organized in a foreign jurisdiction, provide the foreign country of organization

8 Election is to be effective beginning (month, day, year) (see instructions) . . . . . . . . . . . .

9Name and title of contact person whom the IRS may call for more information

10Contact person’s telephone number

Consent Statement and Signature(s) (see instructions)

Under penalties of perjury, I (we) declare that I (we) consent to the election of the

Signature(s)

Date

Title

Form 8832 (Rev.

Form 8832 (Rev. |

Page 3 |

|

Part II |

Late Election Relief |

|

11Provide the explanation as to why the entity classification election was not filed on time (see instructions).

Under penalties of perjury, I (we) declare that I (we) have examined this election, including accompanying documents, and, to the best of my (our) knowledge and belief, the election contains all the relevant facts relating to the election, and such facts are true, correct, and complete. I (we) further declare that I (we) have personal knowledge of the facts and circumstances related to the election. I (we) further declare that the elements required for relief in Section 4.01 of Revenue Procedure

Signature(s)

Date

Title

Form 8832 (Rev.

Form 8832 (Rev. |

Page 4 |

General Instructions

Section references are to the Internal Revenue Code unless otherwise noted.

Future Developments

For the latest information about developments related to Form 8832 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/form8832.

What's New

For entities formed on or after July 1, 2013, the Croatian Dionicko Drustvo will always be treated as a corporation. See Notice

Purpose of Form

An eligible entity uses Form 8832 to elect how it will be classified for federal tax purposes, as a corporation, a partnership, or an entity disregarded as separate from its owner. An eligible entity is classified for federal tax purposes under the default rules described below unless it files Form 8832 or Form 2553, Election by a Small Business Corporation. See Who Must File below.

The IRS will use the information entered on this form to establish the entity’s filing and reporting requirements for federal tax purposes.

Note. An entity must file Form 2553 if making an election under section 1362(a) to be an S corporation

A new eligible entity should not file Form 8832 if it will be using its

TIP default classification (see Default Rules below).

Eligible entity. An eligible entity is a business entity that is not included in items 1, or 3 through 9, under the definition of corporation provided under Definitions. Eligible entities include limited liability companies (LLCs) and partnerships.

Generally, corporations are not eligible entities. However, the following types of corporations are treated as eligible entities:

1.An eligible entity that previously elected to be an association taxable as a corporation by filing Form 8832. An entity that elects to be classified as a corporation by filing Form 8832 can make another election to change its classification (see the

2.A foreign eligible entity that became an association taxable as a corporation under the foreign default rule described below.

Default Rules

Existing entity default rule. Certain domestic and foreign entities that were in existence before January 1, 1997, and have an established federal tax classification generally do not need to make an election to continue that classification. If an existing entity decides to change its classification, it may do so subject to the

Domestic default rule. Unless an election is made on Form 8832, a domestic eligible entity is:

1.A partnership if it has two or more members.

2.Disregarded as an entity separate from its owner if it has a single owner.

A change in the number of members of an eligible entity classified as an association (defined below) does not affect the entity’s classification. However, an eligible entity classified as a partnership will become a disregarded entity when the entity’s membership is reduced to one member and a disregarded entity will be classified as a partnership when the entity has more than one member.

Foreign default rule. Unless an election is made on Form 8832, a foreign eligible entity is:

1.A partnership if it has two or more members and at least one member does not have limited liability.

2.An association taxable as a corporation if all members have limited liability.

3.Disregarded as an entity separate from its owner if it has a single owner that does not have limited liability.

However, if a qualified foreign entity (as defined in section 3.02 of Rev. Proc.

1.The qualified entity's owner and purported owners file amended returns that are consistent with the treatment of the entity as a disregarded entity;

2.The amended returns are filed before the close of the period of limitations on assessments under section 6501(a) for the relevant tax year; and

3.The corrected Form 8832, with the box checked entitled: Relief for a late change of entity classification election sought under Revenue Procedure

Also, if the qualified foreign entity (as defined in section 3.02 of Rev. Proc.

1.The qualified entity files information returns and the actual owners file original or amended returns consistent with the treatment of the entity as a partnership;

2.The amended returns are filed before the close of the period of limitations on assessments under section 6501(a) for the relevant tax year; and

3.The corrected Form 8832, with the box checked entitled: Relief for a late change of

entity classification election sought under Revenue Procedure

Definitions

Association. For purposes of this form, an association is an eligible entity taxable as a corporation by election or, for foreign eligible entities, under the default rules (see Regulations section

Business entity. A business entity is any entity recognized for federal tax purposes that is not properly classified as a trust under Regulations section

Corporation. For federal tax purposes, a corporation is any of the following:

1.A business entity organized under a federal or state statute, or under a statute of a federally recognized Indian tribe, if the statute describes or refers to the entity as incorporated or as a corporation, body corporate, or body politic.

2.An association (as determined under Regulations section

3.A business entity organized under a

state statute, if the statute describes or refers to the entity as a

4.An insurance company.

5.A

6.A business entity wholly owned by a state or any political subdivision thereof, or a business entity wholly owned by a foreign government or any other entity described in Regulations section

7.A business entity that is taxable as a corporation under a provision of the Code other than section 7701(a)(3).

8.A foreign business entity listed on page 7. See Regulations section

9.An entity created or organized under the laws of more than one jurisdiction (business entities with multiple charters) if the entity is treated as a corporation with respect to any one of the jurisdictions. See Regulations section

Disregarded entity. A disregarded entity is an eligible entity that is treated as an entity not separate from its single owner for income tax purposes. A “disregarded entity” is treated as separate from its owner for:

•Employment tax purposes, effective for wages paid on or after January 1, 2009; and

•Excise taxes reported on Forms 720, 730, 2290,

Form 8832 (Rev. |

Page 5 |

See the employment tax and excise tax return instructions for more information.

Limited liability. A member of a foreign eligible entity has limited liability if the member has no personal liability for any debts of or claims against the entity by reason of being a member. This determination is based solely on the statute or law under which the entity is organized (and, if relevant, the entity’s organizational documents). A member has personal liability if the creditors of the entity may seek satisfaction of all or any part of the debts or claims against the entity from the member as such. A member has personal liability even if the member makes an agreement under which another person (whether or not a member of the entity) assumes that liability or agrees to indemnify that member for that liability.

Partnership. A partnership is a business entity that has at least two members and is not a corporation as defined above under Corporation.

Who Must File

File this form for an eligible entity that is one of the following:

•A domestic entity electing to be classified as an association taxable as a corporation.

•A domestic entity electing to change its current classification (even if it is currently classified under the default rule).

•A foreign entity that has more than one owner, all owners having limited liability, electing to be classified as a partnership.

•A foreign entity that has at least one owner that does not have limited liability, electing to be classified as an association taxable as a corporation.

•A foreign entity with a single owner having limited liability, electing to be an entity disregarded as an entity separate from its owner.

•A foreign entity electing to change its current classification (even if it is currently classified under the default rule).

Do not file this form for an eligible entity that is:

•

•A real estate investment trust (REIT), as defined in section 856; or

•Electing to be classified as an S corporation. An eligible entity that timely files Form 2553 to elect classification as an S corporation and meets all other requirements to qualify as an S corporation is deemed to have made an election under Regulations section

All three of these entities are deemed to

have made an election to be classified as an association.

Effect of Election

The federal tax treatment of elective changes in classification as described in Regulations section

•If an eligible entity classified as a partnership elects to be classified as an association, it is deemed that the partnership contributes all of its assets and liabilities to the association in exchange for stock in the association, and immediately thereafter, the partnership liquidates by distributing the stock of the association to its partners.

•If an eligible entity classified as an association elects to be classified as a partnership, it is deemed that the association distributes all of its assets and liabilities to its shareholders in liquidation of the association, and immediately thereafter, the shareholders contribute all of the distributed assets and liabilities to a newly formed partnership.

•If an eligible entity classified as an association elects to be disregarded as an entity separate from its owner, it is deemed that the association distributes all of its assets and liabilities to its single owner in liquidation of the association.

•If an eligible entity that is disregarded as an entity separate from its owner elects to be classified as an association, the owner of the eligible entity is deemed to have contributed all of the assets and liabilities of the entity to the association in exchange for the stock of the association.

Note. For information on the federal tax consequences of elective changes in classification, see Regulations section

When To File

Generally, an election specifying an eligible entity’s classification cannot take effect more than 75 days prior to the date the election is filed, nor can it take effect later than 12 months after the date the election is filed. An eligible entity may be eligible for late election relief in certain circumstances. For more information, see Late Election Relief, later.

Where To File

File Form 8832 with the Internal Revenue Service Center for your state listed later.

In addition, attach a copy of Form 8832 to the entity’s federal tax or information return for the tax year of the election. If the entity is not required to file a return for that year, a copy of its Form 8832 must be attached to the federal tax returns of all direct or indirect owners of the entity for the tax year of the owner that includes the date on which the election took effect. An indirect owner of the electing entity does not have to attach a copy of the Form 8832 to its tax return if an entity in which it has an interest is already filing a copy of the Form 8832 with its return. Failure to attach a copy of Form 8832 will not invalidate an otherwise valid election, but penalties may be assessed against persons who are required to, but do not, attach Form 8832.

Each member of the entity is required to file the member's return consistent with the entity election. Penalties apply to returns filed inconsistent with the entity’s election.

If the entity’s principal |

Use the following |

|

business, office, or |

Internal Revenue |

|

agency is located in: |

Service Center |

|

|

address: |

|

Connecticut, Delaware, |

|

|

District of Columbia, |

|

|

Florida, Illinois, Indiana, |

|

|

Kentucky, Maine, |

|

|

Maryland, Massachusetts, |

|

|

Michigan, New Hampshire, |

Cincinnati, OH 45999 |

|

New Jersey, New York, |

|

|

North Carolina, Ohio, |

|

|

Pennsylvania, Rhode |

|

|

Island, South Carolina, |

|

|

Vermont, Virginia, West |

|

|

Virginia, Wisconsin |

|

|

|

|

|

If the entity’s principal |

Use the following |

|

business, office, or |

Internal Revenue |

|

agency is located in: |

Service Center |

|

|

address: |

|

|

|

|

Alabama, Alaska, Arizona, |

|

|

Arkansas, California, |

|

|

Colorado, Georgia, Hawaii, |

|

|

Idaho, Iowa, Kansas, |

|

|

Louisiana, Minnesota, |

|

|

Mississippi, Missouri, |

Ogden, UT 84201 |

|

Montana, Nebraska, |

||

|

||

Nevada, New Mexico, |

|

|

North Dakota, Oklahoma, |

|

|

Oregon, South Dakota, |

|

|

Tennessee, Texas, Utah, |

|

|

Washington, Wyoming |

|

|

|

|

|

A foreign country or U.S. |

Ogden, UT |

|

possession |

Note. Also attach a copy to the entity’s federal income tax return for the tax year of the election.

Acceptance or Nonacceptance of Election

The service center will notify the eligible entity at the address listed on Form 8832 if its election is accepted or not accepted. The entity should generally receive a determination on its election within 60 days after it has filed Form 8832.

Care should be exercised to ensure that the IRS receives the election. If the entity is not notified of acceptance or nonacceptance of its election within 60 days of the date of filing, take

If the IRS questions whether Form 8832 was filed, an acceptable proof of filing is:

•A certified or registered mail receipt (timely postmarked) from the U.S. Postal Service, or its equivalent from a designated private delivery service;

•Form 8832 with an accepted stamp;

•Form 8832 with a stamped IRS received date; or

•An IRS letter stating that Form 8832 has been accepted.

Form 8832 (Rev. |

Page 6 |

Specific Instructions

Name. Enter the name of the eligible entity electing to be classified.

Employer identification number (EIN). Show the EIN of the eligible entity electing to be classified.

Do not put “Applied For” on F! this line.

CAUTION

Note. Any entity that has an EIN will retain that EIN even if its federal tax classification changes under Regulations section

If a disregarded entity’s classification changes so that it becomes recognized as a partnership or association for federal tax purposes, and that entity had an EIN, then the entity must continue to use that EIN. If the entity did not already have its own EIN, then the entity must apply for an EIN and not use the identifying number of the single owner.

A foreign entity that makes an election under Regulations section

(d)must also use its own taxpayer identifying number. See sections 6721 through 6724 for penalties that may apply for failure to supply taxpayer identifying numbers.

If the entity electing to be classified using Form 8832 does not have an EIN, it must apply for one on Form

F |

Do not apply for a new EIN for an |

|

existing entity that is changing its |

||

! |

||

classification if the entity already |

||

CAUTION |

has an EIN. |

Address. Enter the address of the entity electing a classification. All correspondence regarding the acceptance or nonacceptance of the election will be sent to this address. Include the suite, room, or other unit number after the street address. If the Post Office does not deliver mail to the street address and the entity has a P.O. box, show the box number instead of the street address. If the electing entity receives its mail in care of a third party (such as an accountant or an attorney), enter on the street address line “C/O” followed by the third party’s name and street address or P.O. box.

Address change. If the eligible entity has changed its address since filing Form

Relief for a late change of entity classification election sought under Revenue Procedure

Part I. Election Information

Complete Part I whether or not the entity is seeking relief under Rev. Proc.

Line 1. Check box 1a if the entity is choosing a classification for the first time (i.e., the entity does not want to be classified under the applicable default classification). Do not file this form if the entity wants to be classified under the default rules.

Check box 1b if the entity is changing its current classification.

Lines 2a and 2b.

Once an eligible entity makes an election to change its classification, the entity generally cannot change its classification by election again during the 60 months after the effective date of the election. However, the IRS may (by private letter ruling) permit the entity to change its classification by election within the

Note. The

Line 4. If an eligible entity has only one owner, provide the name of its owner on line 4a and the owner’s identifying number (social security number, or individual taxpayer identification number, or EIN) on line 4b. If the electing eligible entity is owned by an entity that is a disregarded entity or by an entity that is a member of a series of tiered disregarded entities, identify the first entity (the entity closest to the electing eligible entity) that is not a disregarded entity. For example, if the electing eligible entity is owned by disregarded entity A, which is owned by another disregarded entity B, and disregarded entity B is owned by partnership C, provide the name and EIN of partnership C as the owner of the electing eligible entity. If the owner is a foreign person or entity and does not have a U.S. identifying number, enter “none” on line 4b.

Line 5. If the eligible entity is owned by one or more members of an affiliated group of corporations that file a consolidated return, provide the name and EIN of the parent corporation.

Line 6. Check the appropriate box if you are changing a current classification (no matter how achieved), or are electing out of a default classification. Do not file this form if you fall within a default classification that is the desired classification for the new entity.

Line 7. If the entity making the election is created or organized in a foreign jurisdiction, enter the name of the foreign country in which it is organized. This information must be provided even if the entity is also organized under domestic law.

Line 8. Generally, the election will take effect on the date you enter on line 8 of this form,

or on the date filed if no date is entered on line 8. An election specifying an entity’s classification for federal tax purposes can take effect no more than 75 days prior to the date the election is filed, nor can it take effect later than 12 months after the date on which the election is filed. If line 8 shows a date more than 75 days prior to the date on which the election is filed, the election will default to 75 days before the date it is filed. If line 8 shows an effective date more than 12 months from the filing date, the election will take effect 12 months after the date the election is filed.

Consent statement and signature(s). Form

8832 must be signed by:

1.Each member of the electing entity who is an owner at the time the election is filed; or

2.Any officer, manager, or member of the electing entity who is authorized (under local law or the organizational documents) to make the election. The elector represents to having such authorization under penalties of perjury.

If an election is to be effective for any period prior to the time it is filed, each person who was an owner between the date the election is to be effective and the date the election is filed, and who is not an owner at the time the election is filed, must sign.

If you need a continuation sheet or use a separate consent statement, attach it to Form 8832. The separate consent statement must contain the same information as shown on Form 8832.

Note. Do not sign the copy that is attached to your tax return.

Part II. Late Election Relief

Complete Part II only if the entity is requesting late election relief under Rev. Proc.

An eligible entity may be eligible for late election relief under Rev. Proc.

1.The entity failed to obtain its requested classification as of the date of its formation (or upon the entity's classification becoming relevant) or failed to obtain its requested change in classification solely because Form 8832 was not filed timely.

2.Either:

a.The entity has not filed a federal tax or information return for the first year in which the election was intended because the due date has not passed for that year's federal tax or information return; or

b.The entity has timely filed all required federal tax returns and information returns (or if not timely, within 6 months after its due date, excluding extensions) consistent with its requested classification for all of the years the entity intended the requested election to be effective and no inconsistent tax or information returns have been filed by or with respect to the entity during any of the tax years. If the eligible entity is not required to file a federal tax return or information return, each affected person who is required to file a federal tax return or information return must have timely filed all such returns (or if not timely, within 6 months after its due date, excluding extensions) consistent with the

Form 8832 (Rev. |

Page 7 |

entity's requested classification for all of the years the entity intended the requested election to be effective and no inconsistent tax or information returns have been filed during any of the tax years.

3.The entity has reasonable cause for its failure to timely make the entity classification election.

4.Three years and 75 days from the requested effective date of the eligible entity's classification election have not passed.

Affected person. An affected person is either:

•with respect to the effective date of the eligible entity's classification election, a person who would have been required to attach a copy of the Form 8832 for the eligible entity to its federal tax or information return for the tax year of the person which includes that date; or

•with respect to any subsequent date after the entity's requested effective date of the classification election, a person who would have been required to attach a copy of the Form 8832 for the eligible entity to its federal tax or information return for the person's tax year that includes that subsequent date had the election first become effective on that subsequent date.

For details on the requirement to attach a copy of Form 8832, see Rev. Proc.

To obtain relief, file Form 8832 with the applicable IRS service center listed in Where To File, earlier, within 3 years and 75 days from the requested effective date of the eligible entity's classification election.

If Rev. Proc.

entity may seek relief for a late entity election by requesting a private letter ruling and paying a user fee in accordance with Rev. Proc.

Line 11. Explain the reason for the failure to file a timely entity classification election.

Signatures. Part II of Form 8832 must be signed by an authorized representative of the eligible entity and each affected person. See Affected Persons, earlier. The individual or individuals who sign the declaration must have personal knowledge of the facts and circumstances related to the election.

Foreign Entities Classified as Corporations for Federal Tax Purposes:

American

People’s Republic of

Youxian Gongsi

Republic of China (Taiwan)

Costa

Anonima

El

European Economic Area/European Union

Hong

New

Northern Mariana

Puerto

Obshchestvo

Saudi

Slovak

South

Switzerland— Aktiengesellschaft

Trinidad and

United

United States Virgin

Anonima

See Regulations section F!

exceptions and inclusions to items CAUTION on this list and for any revisions made to this list since these instructions were printed.

Paperwork Reduction Act Notice

We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated average time is:

Recordkeeping . . . . 2 hr., 46 min.

Learning about the

law or the form . . . . 3 hr., 48 min.

Preparing and sending

the form to the IRS . . . . . 36 min.

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can write to the Internal Revenue Service, Tax Forms and Publications, SE:W:CAR:MP:TFP,

1111 Constitution Ave. NW,

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 8832 allows eligible entities to choose how they want to be classified for federal tax purposes. |

| Eligibility | Entities such as limited liability companies (LLCs) and partnerships can file this form to elect to be treated as a corporation or partnership. |

| Filing Deadline | The form must be filed within 75 days of the entity's formation or within 75 days of the desired effective date for the classification change. |

| State-Specific Forms | Some states have their own forms or requirements for entity classification. Check with your state’s tax authority for details. |

| Governing Laws | State-specific laws vary. For example, California requires compliance with the California Revenue and Taxation Code. |

| Impact on Taxes | The choice made on Form 8832 can significantly affect how an entity is taxed at both federal and state levels. |

| Revocation | Once an election is made, it can be revoked, but there are specific rules and timelines that must be followed for revocation. |

Filling out IRS Form 8832 is an important step in electing how your business will be classified for tax purposes. After completing the form, you will submit it to the IRS to formalize your election. Make sure to keep a copy for your records.

What is IRS Form 8832?

IRS Form 8832, also known as the Entity Classification Election, is a form that allows eligible entities to choose how they will be classified for federal tax purposes. Entities can elect to be treated as a corporation, partnership, or disregarded entity. This classification can significantly impact how the entity is taxed, so understanding your options is crucial.

Who needs to file Form 8832?

Any eligible entity that wishes to change its classification for tax purposes must file Form 8832. This typically includes limited liability companies (LLCs), partnerships, and certain corporations. If your entity is already classified as a corporation or partnership and you want to change that classification, you will need to submit this form.

When should Form 8832 be filed?

Form 8832 should be filed within 75 days of the date you want the classification change to take effect. If you miss this window, you may have to wait until the next tax year or follow additional steps to request late election relief. It’s important to plan ahead to ensure timely submission.

What information is required on Form 8832?

When completing Form 8832, you will need to provide basic information about your entity, including its name, address, and Employer Identification Number (EIN). Additionally, you must indicate the desired classification and provide the effective date of the election. Ensure that all information is accurate to avoid delays in processing.

Is there a fee to file Form 8832?

No, there is no fee associated with filing Form 8832. However, while the form itself is free, you may incur other costs related to tax advice or accounting services if you choose to seek assistance in completing the form or understanding the implications of your classification choice.

Can Form 8832 be revoked or changed?

Yes, once you file Form 8832 and your classification is effective, you can revoke or change your election. However, doing so may require additional forms and adherence to specific rules set by the IRS. Generally, you must wait five years before making another election unless you meet certain exceptions.

What are the tax implications of filing Form 8832?

The tax implications of filing Form 8832 depend on the classification you choose. For example, if you elect to be treated as a corporation, you may face double taxation on profits—once at the corporate level and again when dividends are distributed to shareholders. On the other hand, being classified as a partnership or disregarded entity can allow for pass-through taxation, where income is reported on the owners' personal tax returns. It’s advisable to consult with a tax professional to understand the best classification for your specific situation.

Where can I find Form 8832 and instructions for filing?

You can find IRS Form 8832 and its instructions on the official IRS website. The form is available for download in PDF format, and the instructions provide detailed guidance on how to complete the form accurately. Make sure to review the instructions carefully to ensure compliance with all requirements.

Incorrect Entity Type Selection: Many individuals mistakenly choose the wrong entity type when filling out the form. It's crucial to select the correct classification to avoid complications with the IRS.

Missing Signatures: Some forget to sign the form. A missing signature can lead to delays or rejections, so double-check that all required signatures are included.

Incorrect Tax Year: Entering the wrong tax year can cause significant issues. Ensure that the tax year you indicate matches the year you intend to elect for your entity.

Failure to Provide Required Information: Omitting essential details, such as the entity’s name, address, or Employer Identification Number (EIN), can lead to processing delays.

Not Understanding the Election Process: Some individuals do not fully grasp the implications of making an election. Researching or consulting a tax professional can provide clarity.

Incorrectly Filling Out the Form: Errors in data entry, such as typos or incorrect numbers, can lead to confusion. Take your time to review each section carefully.

Ignoring Deadlines: Many people miss the deadline for filing the form. Being aware of the timeline is essential to ensure your election is valid.

Not Keeping Copies: Failing to keep a copy of the submitted form can be problematic. Always retain a copy for your records to reference in the future.

Inadequate Supporting Documentation: Some forget to include necessary documents. Providing the right paperwork can help support your election and smooth the process.

Assuming IRS Will Contact You: Many believe that the IRS will reach out if there are issues. In reality, it’s your responsibility to follow up and ensure everything is in order.

The IRS Form 8832, also known as the Entity Classification Election, is crucial for businesses that want to change their tax classification. When filing this form, there are several other documents that may be necessary to ensure compliance with IRS regulations. Below is a list of commonly used forms and documents that often accompany Form 8832.

When preparing to file Form 8832, ensure that you have all relevant documents in order. This will streamline the process and help avoid potential delays or complications with the IRS.

The IRS Form 8832 allows entities to elect how they are classified for federal tax purposes. Several other forms and documents serve similar functions in terms of entity classification or tax election. Below is a list of eight documents that share similarities with Form 8832:

Each of these documents plays a role in how entities are classified and taxed, reflecting the importance of proper documentation in compliance with tax regulations.

When filling out the IRS Form 8832, which is used to elect how a business entity will be classified for federal tax purposes, there are important guidelines to follow. Here’s a list of things you should and shouldn’t do:

Following these guidelines can help ensure that your Form 8832 is processed smoothly and that your business is classified correctly for tax purposes.

The IRS Form 8832, also known as the Entity Classification Election, can be a source of confusion for many. Below are some common misconceptions about this form, along with clarifications to help you better understand its purpose and requirements.

Understanding these misconceptions can help you navigate the complexities of Form 8832 more effectively. Always consider consulting a tax professional for personalized advice tailored to your specific situation.

The IRS 8832 form is essential for entities that want to elect their tax classification. Here are key takeaways to consider when filling out and using this form:

Taking these points into account will help ensure that your use of the IRS 8832 form is effective and compliant.