The IRS 8655 form plays a crucial role for tax professionals and businesses alike, serving as a tool for the designation of an authorized agent to act on behalf of a taxpayer. This form is particularly significant for those who require assistance in managing their tax responsibilities, as it allows the appointed agent to receive and respond to IRS notices and communications. The form ensures that the agent has the authority to handle specific tax matters, streamlining the process for both the taxpayer and the IRS. Additionally, it covers various aspects, including the identification of the taxpayer, the scope of authority granted to the agent, and the necessary signatures to validate the agreement. Understanding the implications of this form is essential for anyone looking to simplify their tax interactions and ensure compliance with IRS regulations.

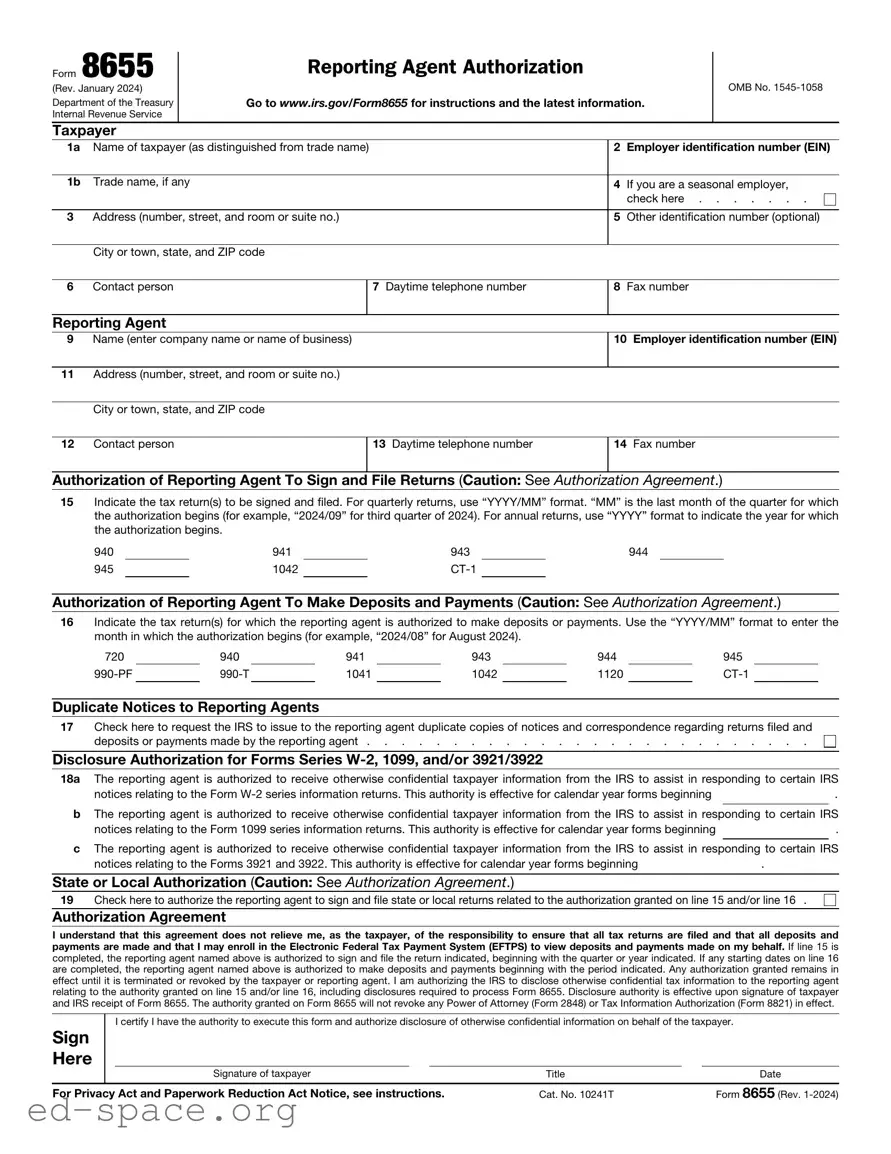

Form 8655

(Rev. January 2024)

Department of the Treasury

Internal Revenue Service

Taxpayer

Reporting Agent Authorization

Go to www.irs.gov/Form8655 for instructions and the latest information.

OMB No.

1a Name of taxpayer (as distinguished from trade name) |

2 |

Employer identification number (EIN) |

|

|

|

1b Trade name, if any |

4 |

If you are a seasonal employer, |

|

|

check here |

|

|

|

3 Address (number, street, and room or suite no.) |

5 |

Other identification number (optional) |

|

|

|

City or town, state, and ZIP code |

|

|

6Contact person

Reporting Agent

7Daytime telephone number

8Fax number

9 Name (enter company name or name of business) |

10 Employer identification number (EIN) |

11Address (number, street, and room or suite no.)

City or town, state, and ZIP code

12 Contact person |

13 Daytime telephone number |

14 Fax number |

Authorization of Reporting Agent To Sign and File Returns (Caution: See Authorization Agreement.)

15Indicate the tax return(s) to be signed and filed. For quarterly returns, use “YYYY/MM” format. “MM” is the last month of the quarter for which the authorization begins (for example, “2024/09” for third quarter of 2024). For annual returns, use “YYYY” format to indicate the year for which the authorization begins.

940 |

|

941 |

|

943 |

|

944 |

945 |

|

1042 |

|

|

|

Authorization of Reporting Agent To Make Deposits and Payments (Caution: See Authorization Agreement.)

16Indicate the tax return(s) for which the reporting agent is authorized to make deposits or payments. Use the “YYYY/MM” format to enter the month in which the authorization begins (for example, “2024/08” for August 2024).

720 |

|

940 |

|

941 |

|

943 |

|

944 |

|

945 |

|

|

1041 |

|

1042 |

|

1120 |

|

Duplicate Notices to Reporting Agents

17Check here to request the IRS to issue to the reporting agent duplicate copies of notices and correspondence regarding returns filed and

deposits or payments made by the reporting agent . . . . . . . . . . . . . . . . . . . . . . . . . .

Disclosure Authorization for Forms Series

18a The reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Form |

. |

bThe reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Form 1099 series information returns. This authority is effective for calendar year forms beginning |

. |

cThe reporting agent is authorized to receive otherwise confidential taxpayer information from the IRS to assist in responding to certain IRS

notices relating to the Forms 3921 and 3922. This authority is effective for calendar year forms beginning |

. |

State or Local Authorization (Caution: See Authorization Agreement.)

19 Check here to authorize the reporting agent to sign and file state or local returns related to the authorization granted on line 15 and/or line 16 .

Authorization Agreement

I understand that this agreement does not relieve me, as the taxpayer, of the responsibility to ensure that all tax returns are filed and that all deposits and payments are made and that I may enroll in the Electronic Federal Tax Payment System (EFTPS) to view deposits and payments made on my behalf. If line 15 is completed, the reporting agent named above is authorized to sign and file the return indicated, beginning with the quarter or year indicated. If any starting dates on line 16 are completed, the reporting agent named above is authorized to make deposits and payments beginning with the period indicated. Any authorization granted remains in effect until it is terminated or revoked by the taxpayer or reporting agent. I am authorizing the IRS to disclose otherwise confidential tax information to the reporting agent relating to the authority granted on line 15 and/or line 16, including disclosures required to process Form 8655. Disclosure authority is effective upon signature of taxpayer and IRS receipt of Form 8655. The authority granted on Form 8655 will not revoke any Power of Attorney (Form 2848) or Tax Information Authorization (Form 8821) in effect.

I certify I have the authority to execute this form and authorize disclosure of otherwise confidential information on behalf of the taxpayer.

Sign

Here

|

Signature of taxpayer |

|

|

Title |

|

Date |

|

|

|

|

|||

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Cat. No. 10241T |

|

Form 8655 (Rev. |

|||

Form 8655 (Rev. |

Page 2 |

Instructions

What’s New

Forms

15.Beginning with filings for tax year 2023, former filers of Form

940(sp), 941 (sp), and 943 (sp) will be usable by any employer that prefers their form in Spanish, whether they are located in the United States, Puerto Rico, or one of the other territories.

Purpose of Form

Use Form 8655 to authorize a reporting agent to:

•Sign and file certain returns. Reporting agents must file returns electronically except as provided under Rev. Proc.

•Make deposits and payments for certain returns. Reporting agents must make deposits and payments electronically, generally through the Electronic Federal Tax Payment System (EFTPS) at EFTPS.gov. See Pub. 4169, Tax Professional Guide to the EFTPS, and Rev. Proc.

•Receive duplicate copies of tax information, notices, and other written and/or electronic communication regarding any authority granted; and

•Provide the IRS with information to aid in penalty relief determinations related to the authority granted on Form 8655.

Note: An authorization does not relieve the taxpayer of the responsibility (or from liability for failing) to ensure that all tax returns are filed timely and that all federal tax deposits (FTDs) and federal tax payments (FTPs) are made timely. A reporting agent must notify its client of that fact and must recommend that it enroll in EFTPS to view EFTPS deposits and payments made on the client’s behalf. A reporting agent must provide this notification, in writing, upon entering into an agreement with the client and at least quarterly thereafter for as long as it provides services to that client. Sample language and other details may be found in Rev. Proc.

Authority Granted

Once Form 8655 is signed, any authority granted is effective beginning with the period indicated on lines 15, 16, 18a, 18b, and/or 18c and continues indefinitely unless terminated or revoked by the taxpayer or reporting agent. No authorization or authority is granted for periods prior to the period(s) indicated on Form 8655.

Where authority is granted for any form, it is also effective for related forms such as the corresponding

Disclosure authority is effective upon signature of taxpayer and IRS receipt of Form 8655. Any authority granted on Form 8655 does not revoke and has no effect on any authority granted on Form 2848 or 8821, or any

To increase the authority granted to a reporting agent by a Form 8655 already in effect, submit another signed Form 8655, completing lines

Where To File

Send Form 8655 to:

Internal Revenue Service

Accounts Management Service Center MS 6748 RAF Team

1973 North Rulon White Blvd. Ogden, UT 84404

You can fax Form 8655 to the IRS. The number is

Additional Information

Additional information concerning reporting agent authorizations may be found in:

•Pub. 1474, Technical Specifications Guide for Reporting Agent Authorization and Federal Tax Depositors.

•Rev. Proc.

Substitute Form 8655

If you want to prepare and use a substitute Form 8655, see Pub. 1167, General Rules and Specifications for Substitute Forms and Schedules. If your substitute Form 8655 is approved, the form approval number must be printed in the lower left margin of each substitute Form 8655 you file with the IRS.

Terminating or Revoking an Authorization

If you have a valid Form 8655 on file with the IRS, the filing of a new Form 8655 indicating a new reporting agent terminates the authority of the prior reporting agent beginning with the period indicated on the new Form 8655. However, the prior reporting agent is still an authorized reporting agent and retains any previously granted disclosure authority for the periods prior to the beginning period of the new reporting agent’s authorization unless specifically revoked.

If the taxpayer wants to revoke an existing authorization, such that the reporting agent would no longer be authorized to act or receive information for previously authorized tax periods, send a copy of the previously executed Form 8655 to the IRS at the address under Where To File, above.

A reporting agent may terminate its authority by filing a statement with the IRS, either on paper or using a delete process. A reporting agent wanting to revoke its authority must submit the request in writing. The statement must be signed by the reporting agent (if filed on paper) and identify the name and address of the taxpayer and authorization(s) from which the reporting agent is withdrawing. For information on the delete process, see Pub. 1474.

Form 8655 (Rev. |

Page 3 |

Who Must Sign

Electronic signature. For guidance on optional electronic signature methods, including approved methods of authentication and signature and additional items that must appear on the Form 8655, see Pub. 1474, section 01.03.

Sole proprietorship. The individual owning the business.

Corporation (including a limited liability company (LLC) treated as a corporation). Generally, Form 8655 can be signed by (a) an officer having legal authority to bind the corporation, (b) any person designated by the board of directors or other governing body, (c) any officer or employee on written request by any principal officer, and (d) any other person authorized to access information under section 6103(e).

Partnership (including an LLC treated as a partnership) or an unincorporated organization. Generally, Form 8655 can be signed by any person who was a member of the partnership during any part of the tax period covered by Form 8655.

Single member LLC treated as a disregarded entity. The owner of the LLC.

Trust or estate. The fiduciary.

Privacy Act and Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. Our authority to request this information is Internal Revenue Code sections 6011, 6061, 6109, and 6302 and the regulations thereunder. We use this information to identify you and record your reporting agent authorization. You are not required to authorize a reporting agent to act on your behalf. However, if you choose to authorize

a reporting agent, you are required to provide the information requested, including your identification number. Failure to provide all the information requested may prevent or delay processing of your authorization; providing false or fraudulent information may subject you to penalties.

Routine uses of this information include giving it to the Department of Justice for civil and criminal litigation, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement agencies and intelligence agencies to combat terrorism.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law.

The time needed to complete and file Form 8655 will vary depending on individual circumstances. The estimated average time is 1 hour, 7 minutes.

If you have comments concerning the accuracy of this time estimate or suggestions for making Form 8655 simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/FormComments. Or you can send your comments to Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 8655 is used to authorize a third party to act on behalf of a taxpayer for certain tax matters. |

| Who Can Use It | Any individual or business entity can use Form 8655 to designate an authorized representative. |

| Types of Representation | The form allows for representation in various tax matters, including filing returns and making payments. |

| Filing Requirement | Form 8655 must be filed with the IRS, but it does not need to be submitted with a tax return. |

| Duration of Authorization | The authorization remains in effect until revoked by the taxpayer or the representative. |

| State-Specific Forms | Some states have their own forms for tax representation, such as California's Form 3520. |

| Governing Law | State forms are governed by their respective state tax codes, such as California Revenue and Taxation Code. |

| Signature Requirement | Both the taxpayer and the authorized representative must sign the form for it to be valid. |

| Revocation Process | A taxpayer can revoke the authorization by submitting a written notice to the IRS. |

| Where to Obtain | Form 8655 can be obtained from the IRS website or through tax professionals. |

After gathering the necessary information, you can proceed with filling out the IRS 8655 form. This form is essential for designating a third party to act on your behalf regarding tax matters. Follow these steps to ensure accurate completion.

What is the IRS Form 8655?

The IRS Form 8655, also known as the "Reporting Agent Authorization," allows a business to authorize a reporting agent to act on its behalf. This form is typically used by employers who want a third-party service to handle payroll tax reporting and payments. By completing this form, the reporting agent can file tax returns and make payments for the business.

Who needs to fill out Form 8655?

Businesses that wish to designate a reporting agent for payroll tax purposes should fill out Form 8655. This includes employers who want to streamline their payroll processes by allowing a third-party service to manage their tax filings. It’s particularly useful for small businesses that may not have the resources to handle these tasks in-house.

How do I complete Form 8655?

To complete Form 8655, you will need to provide basic information about your business, including the name, address, and Employer Identification Number (EIN). You will also need to include details about the reporting agent, such as their name and contact information. After filling out the form, both the business owner and the reporting agent must sign it. Ensure all information is accurate to avoid any issues with the IRS.

Where do I send Form 8655?

Once completed, Form 8655 should be sent directly to the IRS. The address may vary depending on your location, so it’s important to check the latest instructions on the IRS website. Typically, you will send it to the address listed for your specific type of business or the one indicated in the form instructions.

Is there a deadline for submitting Form 8655?

There is no specific deadline for submitting Form 8655. However, it’s best to submit the form as soon as you decide to authorize a reporting agent. This ensures that the agent can begin handling your payroll tax responsibilities without delay. Keep in mind that the IRS may require the form to be submitted before the reporting agent can file any returns on your behalf.

Can I revoke the authorization granted by Form 8655?

Yes, you can revoke the authorization at any time. To do so, you must submit a written notice to the reporting agent and the IRS. It’s advisable to use the IRS Form 8655 again to indicate the revocation. This ensures that the IRS updates their records and that the reporting agent is no longer authorized to act on your behalf.

What happens if I don’t submit Form 8655?

If you do not submit Form 8655 and choose to use a reporting agent, you will remain responsible for all tax filings and payments. Without this authorization, the reporting agent cannot legally file returns or make payments on your behalf. This could lead to missed deadlines and potential penalties for your business.

Not providing accurate taxpayer information. Ensure that the name, address, and taxpayer identification number (TIN) are correct. Any errors can delay processing.

Forgetting to sign the form. A signature is essential for validation. Without it, the IRS won't accept the form.

Missing the date. It's important to date the form when signing. An unsigned or undated form may be rejected.

Incorrectly identifying the type of authorization. Make sure to select the correct box that reflects the type of authorization you are requesting.

Providing incomplete information about the representative. If you are designating someone to act on your behalf, include their full name, address, and TIN.

Not checking for additional requirements. Depending on your situation, there may be additional documents needed to accompany the form.

Failing to keep a copy of the submitted form. Retaining a copy is crucial for your records and future reference.

Ignoring the submission method. Be aware of whether you need to mail the form or if it can be submitted electronically.

Overlooking the deadlines. Timeliness is key. Submit the form within the required timeframe to avoid penalties.

Not reviewing the form before submission. A quick review can help catch mistakes or missing information that could cause issues.

The IRS Form 8655, also known as the "Reporting Agent Authorization," is a crucial document for businesses that wish to authorize an agent to act on their behalf regarding federal tax matters. When filing this form, there are several other documents that may be necessary to ensure compliance and proper representation. Below is a list of commonly used forms and documents that accompany the IRS 8655.

Understanding the role of these forms can significantly ease the process of managing tax responsibilities. Each document serves a unique purpose, contributing to a comprehensive approach to tax compliance and representation. It is essential to ensure that all necessary forms are completed accurately to avoid complications in dealings with the IRS.

The IRS Form 8655, also known as the "Reporting Agent Authorization," allows taxpayers to authorize a reporting agent to act on their behalf for specific tax matters. Several other IRS forms serve similar purposes in terms of granting authority or designating representatives. Here’s a list of eight documents that share similarities with Form 8655:

Each of these forms plays a role in facilitating communication and representation between taxpayers and the IRS, reflecting the importance of clear authorization in tax matters.

When filling out the IRS 8655 form, it’s essential to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

By following these guidelines, you can help ensure a smooth filing process for the IRS 8655 form.

The IRS Form 8655, also known as the "Reporting Agent Authorization," is often misunderstood. Here are nine common misconceptions about this form:

Understanding these misconceptions can help you navigate the process more effectively and make informed decisions about your tax representation.

The IRS Form 8655, also known as the "Reporting Agent Authorization," is an important document for taxpayers and tax professionals. Below are key takeaways regarding its use and completion.