The IRS 8300 form plays a crucial role in the realm of financial transactions, particularly those involving cash payments. This form is designed to help the Internal Revenue Service monitor large cash transactions and prevent money laundering and other illicit activities. Whenever a business receives more than $10,000 in cash from a single customer during a single transaction or a series of related transactions, it is required to file this form. The information collected includes details about the payer, the amount received, and the nature of the transaction. Businesses must submit the IRS 8300 form within 15 days of the transaction, ensuring timely reporting to the IRS. Failure to comply can lead to significant penalties, underscoring the importance of understanding the requirements associated with this form. By accurately completing and submitting the IRS 8300, businesses not only adhere to legal obligations but also contribute to the integrity of the financial system.

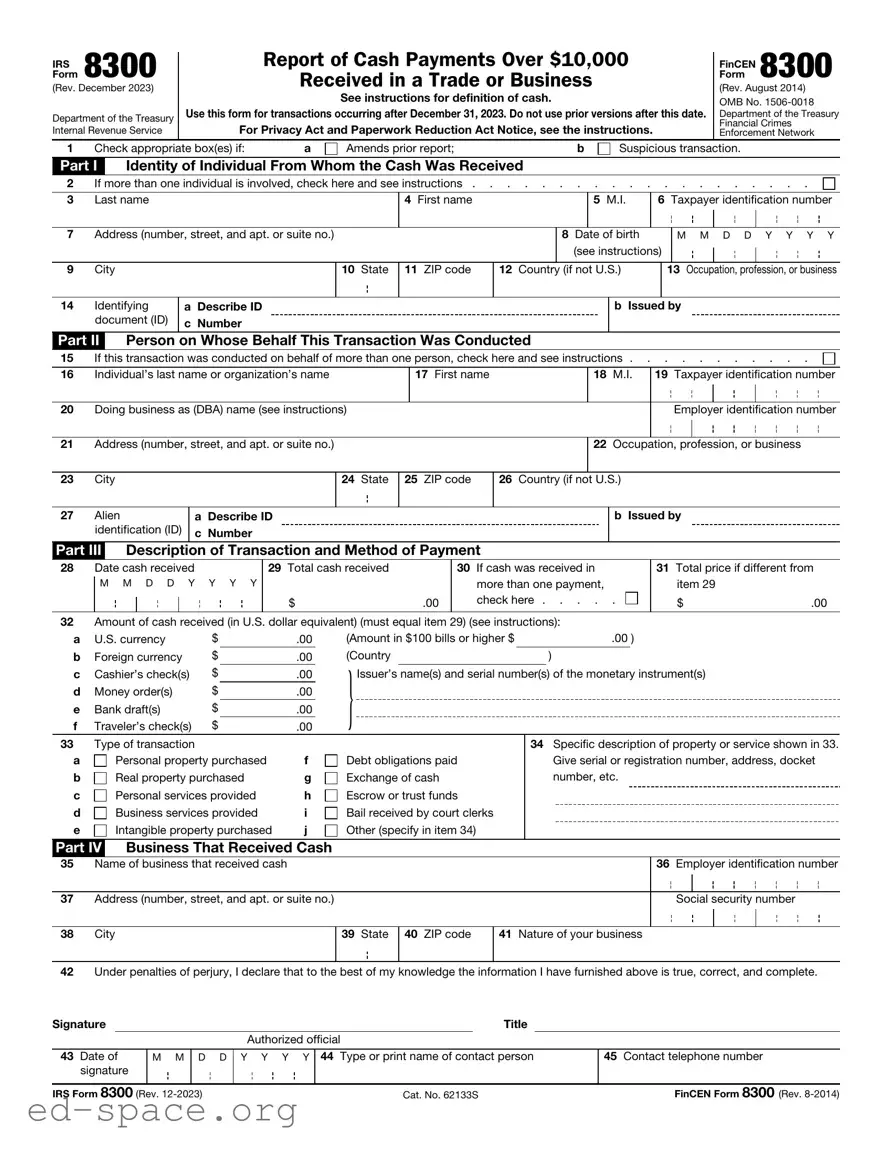

IRS 8300

Form

(Rev. December 2023)

Department of the Treasury Internal Revenue Service

Report of Cash Payments Over $10,000

Received in a Trade or Business

See instructions for definition of cash.

Use this form for transactions occurring after December 31, 2023. Do not use prior versions after this date.

For Privacy Act and Paperwork Reduction Act Notice, see the instructions.

FinCEN 8300 Form

(Rev. August 2014)

OMB No.

Department of the Treasury

Financial Crimes

Enforcement Network

1 Check appropriate box(es) if: |

a |

Amends prior report; |

b |

Part I Identity of Individual From Whom the Cash Was Received

Suspicious transaction.

2 |

If more than one individual is involved, check here and see instructions |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

4 First name |

|

|

5 M.I. |

6 Taxpayer identification number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

|

8 Date of birth |

|

|

M M D D Y Y Y Y |

|||

|

|

|

|

|

(see instructions) |

|

|||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

9 |

City |

10 State |

11 ZIP code |

12 Country |

(if not U.S.) |

|

13 Occupation, profession, or business |

||||

|

|

|

|

|

|

|

|

|

|

|

|

14 Identifying |

a |

Describe ID |

document (ID) |

c |

Number |

Part II Person on Whose Behalf This Transaction Was Conducted

b Issued by

15 |

If this transaction was conducted on behalf of more than one person, check here and see instructions |

|||

|

|

|

|

|

16 |

Individual’s last name or organization’s name |

17 First name |

18 M.I. |

19 Taxpayer identification number |

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27 Alien |

a |

Describe ID |

identification (ID) |

c |

Number |

Part III Description of Transaction and Method of Payment

b Issued by

28Date cash received

M M D D Y Y Y Y

29Total cash received

$.00

30If cash was received in more than one payment, check here . . . . .

31Total price if different from item 29

$.00

32Amount of cash received (in U.S. dollar equivalent) (must equal item 29) (see instructions):

a |

U.S. currency |

$ |

.00 |

(Amount in $100 bills or higher $ |

.00 ) |

||||

b |

Foreign currency |

$ |

.00 |

(Country |

) |

|

|||

|

|

$ |

|

} |

|

|

|

||

c |

Cashier’s check(s) |

.00 |

Issuer’s name(s) and serial number(s) of the monetary instrument(s) |

||||||

d |

Money order(s) |

$ |

.00 |

|

|

|

|

|

|

e |

Bank draft(s) |

$ |

.00 |

|

|

|

|

|

|

f |

Traveler’s check(s) |

$ |

.00 |

|

|

|

|

|

|

33Type of transaction

a |

Personal property purchased |

f |

b |

Real property purchased |

g |

c |

Personal services provided |

h |

d |

Business services provided |

i |

e |

Intangible property purchased |

j |

Part IV |

Business That Received Cash |

|

Debt obligations paid Exchange of cash Escrow or trust funds

Bail received by court clerks Other (specify in item 34)

34Specific description of property or service shown in 33. Give serial or registration number, address, docket number, etc.

35Name of business that received cash

36Employer identification number

37Address (number, street, and apt. or suite no.)

Social security number

38City

39State

40ZIP code

41Nature of your business

42Under penalties of perjury, I declare that to the best of my knowledge the information I have furnished above is true, correct, and complete.

Signature |

|

|

|

|

|

Title |

|

|

|

|

|

|

Authorized official |

|

|

||

|

|

|

|

|

|

|

||

43 Date of |

M M |

D D |

Y Y Y Y |

44 Type or print name of contact person |

|

45 Contact telephone number |

||

signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

IRS Form 8300 (Rev. |

|

Cat. No. 62133S |

|

FinCEN Form 8300 (Rev. |

||||

IRS Form 8300 (Rev. |

Page 2 |

FinCEN Form 8300 (Rev. |

Multiple Parties

(Complete applicable parts below if box 2 or 15 on page 1 is checked.)

Part I

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

Part II

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

Comments – Please use the lines provided below to comment on or clarify any information you entered on any line in Parts I, II, III, and IV

IRS Form 8300 (Rev. |

FinCEN Form 8300 (Rev. |

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS Form 8300 is used to report cash payments over $10,000 received in a trade or business. |

| Filing Requirement | Businesses must file Form 8300 if they receive cash payments exceeding $10,000 in a single transaction or related transactions. |

| Deadline for Filing | The form must be filed within 15 days of receiving the cash payment. |

| Penalties for Non-Compliance | Failure to file Form 8300 can result in significant penalties, including fines for each violation. |

| Record Keeping | Businesses are required to keep records of cash transactions for at least five years. |

| State-Specific Forms | Some states may have their own reporting requirements. For example, California requires reporting under the California Revenue and Taxation Code. |

| Privacy Considerations | Information submitted on Form 8300 is confidential and protected under IRS regulations, but it can be shared with law enforcement agencies. |

After obtaining the IRS 8300 form, it is important to complete it accurately and submit it according to the guidelines. This process ensures compliance with IRS regulations regarding cash transactions. Follow the steps below to fill out the form correctly.

Once the form is completed, review it for accuracy and ensure all required fields are filled. Submit the form to the IRS as instructed, keeping a copy for your records.

What is the IRS Form 8300?

The IRS Form 8300 is a document that businesses must file when they receive more than $10,000 in cash in a single transaction or a series of related transactions. This form helps the government track large cash transactions to prevent money laundering and other illegal activities.

Who needs to file Form 8300?

Any business that receives more than $10,000 in cash must file Form 8300. This requirement applies to various types of businesses, including retail stores, car dealerships, and service providers. It is important for businesses to be aware of their reporting obligations to avoid penalties.

What constitutes "cash" for Form 8300?

For the purposes of Form 8300, "cash" includes not only physical currency but also cashier's checks, money orders, and traveler's checks. If a business receives these forms of payment totaling more than $10,000, it must file the form.

When is Form 8300 due?

Form 8300 must be filed within 15 days of receiving the cash payment. Timely filing is crucial to avoid potential penalties. Businesses should keep records of cash transactions to ensure compliance with this requirement.

What information is required on Form 8300?

The form requires specific information, including the name, address, and taxpayer identification number of the business and the person making the cash payment. Additionally, details about the transaction, such as the date and amount received, must be included.

What happens if a business fails to file Form 8300?

Failure to file Form 8300 can result in significant penalties. The IRS may impose fines, which can increase depending on the duration of the failure to file. It is essential for businesses to understand their obligations to avoid these consequences.

Can Form 8300 be filed electronically?

Yes, businesses can file Form 8300 electronically using the IRS's e-file system. Electronic filing can streamline the process and ensure that the form is submitted on time. Businesses should check the IRS website for specific instructions on electronic filing.

Is there a way to correct an error on Form 8300?

If a business discovers an error after filing Form 8300, it can correct the mistake by submitting a new Form 8300 with the correct information. It is important to clearly indicate that it is a correction to ensure proper processing by the IRS.

Where can I find more information about Form 8300?

Additional information about Form 8300 can be found on the IRS website. The site provides resources, instructions, and guidance on filing the form, as well as answers to frequently asked questions.

Failing to provide accurate information about the payer. This includes incorrect names, addresses, or taxpayer identification numbers.

Not reporting all cash transactions. If a transaction exceeds $10,000 in cash, it must be reported, regardless of whether it is a single payment or multiple payments that total over that amount.

Missing the filing deadline. The IRS requires the form to be filed within 15 days of receiving cash payments exceeding $10,000.

Neglecting to sign the form. A signature is necessary to validate the information provided on the form.

Providing incomplete information. Ensure all required fields are filled out completely to avoid delays or penalties.

Not keeping a copy of the filed form. Retaining a copy is essential for record-keeping and for any potential audits.

Failing to understand the reporting requirements. Many individuals and businesses are unaware of the specific thresholds and conditions that necessitate filing.

Not consulting with a tax professional when in doubt. Seeking guidance can prevent mistakes and ensure compliance with IRS regulations.

The IRS 8300 form is crucial for reporting cash payments over $10,000 received in a trade or business. However, several other forms and documents may accompany it to ensure compliance with various regulations. Below is a list of commonly used documents that can support the information provided in the IRS 8300 form.

In summary, while the IRS 8300 form is essential for reporting large cash transactions, the accompanying documents play a vital role in ensuring transparency and compliance. Proper documentation can protect businesses from potential audits and penalties, making it important to maintain thorough records.

The IRS Form 8300 is used to report cash payments over $10,000 received in a trade or business. Several other documents serve similar purposes in reporting financial transactions. Here are four documents that share similarities with Form 8300:

When it comes to filling out the IRS 8300 form, there are several important dos and don'ts to keep in mind. This form is used to report cash payments over $10,000 received in a trade or business. Here’s a helpful list to guide you through the process:

By following these guidelines, you can navigate the IRS 8300 form process more smoothly and ensure compliance with tax regulations.

The IRS 8300 form is an important document for businesses that receive cash payments over a certain threshold. However, there are several misconceptions surrounding this form that can lead to confusion. Here are ten common misunderstandings about the IRS 8300 form:

Understanding these misconceptions can help businesses navigate their responsibilities more effectively and avoid potential pitfalls related to cash transactions.

Filling out the IRS 8300 form is an important step for businesses and individuals who receive large cash payments. Here are some key takeaways to keep in mind:

Understanding these key points can help ensure compliance and avoid potential issues with the IRS. Always consider consulting with a tax professional if you have questions about your specific situation.