Navigating the complexities of tax season can be daunting for many, especially for corporations in the United States tasked with ensuring compliance with the Internal Revenue Service's (IRS) regulations. Central to this compliance is the IRS 1120 form, a critical document for U.S. corporations, including LLCs that elect to be treated as corporations. This form serves as the primary tool through which these entities report their income, gains, losses, deductions, and credits to the IRS. Beyond merely fulfilling a tax obligation, the careful preparation of the IRS 1120 form can uncover opportunities for tax savings and provide valuable insights into the financial health of a corporation. Failure to accurately complete this form can lead to penalties or audits, making it imperative for corporations to approach this task with diligence and an understanding of the form's nuances. As corporations endeavor to meet their tax responsibilities, the importance of the IRS 1120 form in maintaining compliance cannot be overstated, encompassing a myriad of components, each vital for the fiscal transparency and compliance of the filing entity.

| Fact Name | Description |

|---|---|

| Definition | The IRS Form 1120 is used by corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service. |

| Filing Requirement | All domestic corporations must file IRS Form 1120, unless they are exempt as per IRS guidelines. |

| Due Date | Typically, Form 1120 is due by the 15th day of the 4th month after the end of the corporation’s tax year. For corporations operating on a calendar year, this is April 15. |

| Extension Option | Corporations can apply for a six-month extension to file Form 1120 by submitting Form 7004 by the original due date of the 1120 form. |

| Tax Payment | Taxes due are expected to be paid by the original due date of Form 1120, regardless of an extension to file. |

| Electronic Filing | The IRS encourages corporations to file Form 1120 electronically for faster processing and increased accuracy. |

| Amended Returns | If a corporation needs to correct information on a previously filed Form 1120, they must file an amended return using Form 1120X. |

| State-Specific Forms | Many states require corporations to file state-specific income tax returns in addition to the federal Form 1120. The applicable laws and requirements vary by state. |

When the time comes to navigate the complexities of corporate taxes, the IRS Form 1120 serves as a critical tool. This form enables corporations to report their income, gains, losses, deductions, and credits, ensuring compliance with tax regulations. Filling out this document meticulously is paramount for any corporation looking to fulfill its tax obligations accurately. The process can appear daunting at first, but by breaking it down into manageable steps, the task becomes much more straightforward. Let's explore the steps needed to complete the IRS 1120 form, aiming to ease the burden and clarify the procedure. Following these guidelines will not only help in submitting a properly filled form but also in understanding the financial standing of your corporation.

Filing IRS Form 1120 is a critical but manageable task that ensures a corporation's tax liabilities are accurately reported and fulfilled. By following these organized steps, the process can be conducted smoothly, allowing for a more efficient handling of your corporation's tax responsibilities. Remember, when in doubt, seeking assistance from a tax professional can provide guidance through the intricacies of tax law and form preparation, ensuring compliance and peace of mind.

What is the IRS 1120 form?

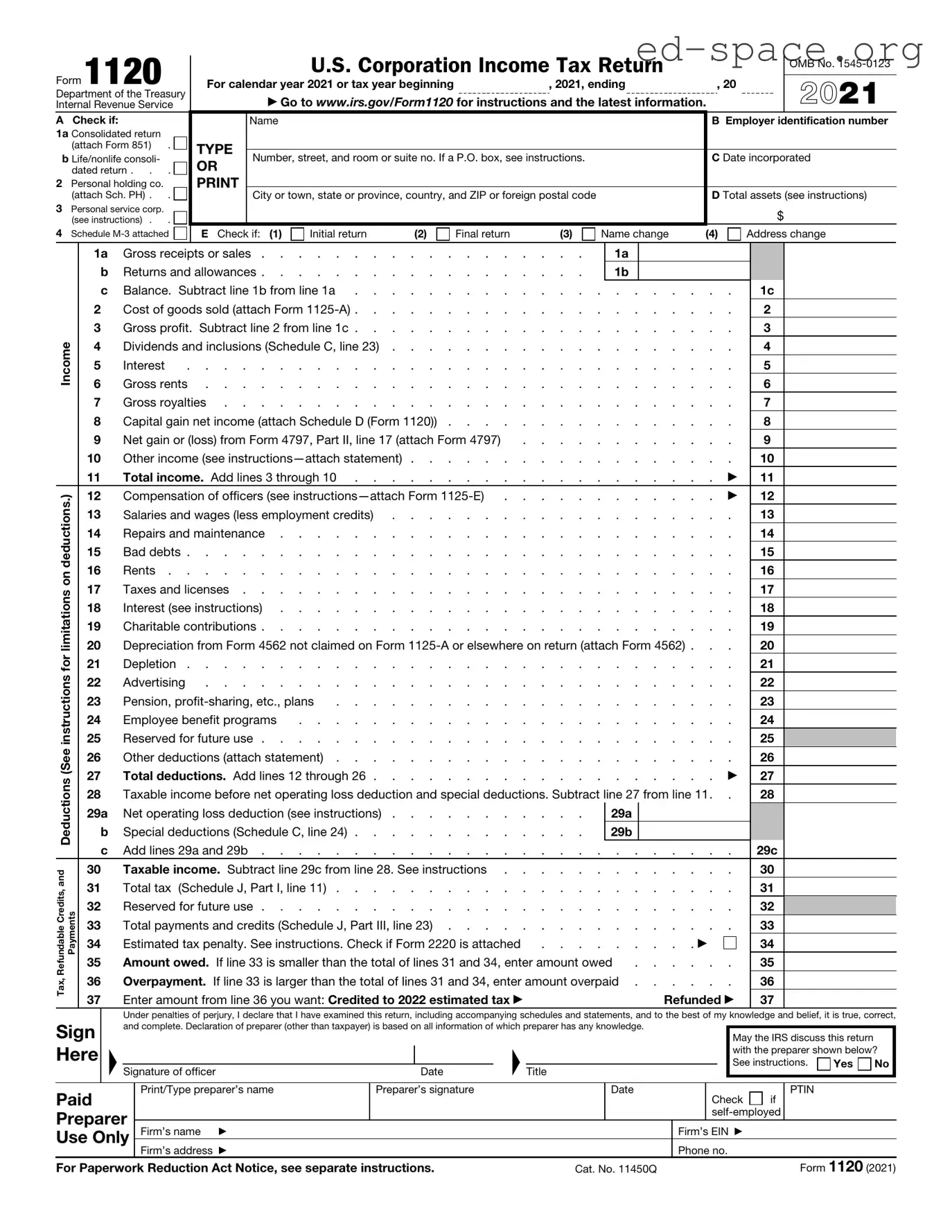

The IRS 1120 form, also known as the U.S. Corporation Income Tax Return, is a document that corporations in the United States use to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). This form helps the IRS assess the tax liability of corporations.

Who needs to file the IRS 1120 form?

Generally, all domestic corporations (including corporations in bankruptcy) must file an IRS 1120 form, regardless of their income. This requirement applies to both C corporations and S corporations, although S corporations file a specific version called the 1120S. The obligation to file is not dependent on the entity's profit margins; even corporations with zero income are required to submit this form.

When is the IRS 1120 form due?

The due date for filing the IRS 1120 form typically falls on the 15th day of the fourth month following the end of the corporation’s tax year. For corporations operating on a calendar year, this date is April 15th. It's important to note, however, that if the due date falls on a weekend or legal holiday, the deadline is extended to the next business day. Corporations can apply for a six-month extension if more time is needed, but the request must be filed before the original due date.

What information do I need to complete the IRS 1120 form?

Completing the IRS 1120 requires detailed financial information from the corporation. This includes the gross income, dividends, interest, any income from rents and royalties, capital gains, deductions (such as salaries, wages, repairs, and maintenance), and tax credits. Accurate financial statements and records are crucial for reporting and calculating the tax owed or refund due accurately.

Can I file the IRS 1120 form electronically?

Yes, corporations can file the IRS 1120 form electronically through the IRS e-file system. Electronic filing is encouraged by the IRS because it is faster and more secure than paper filing. In fact, certain corporations with assets of $10 million or more and that file at least 250 returns a year are required to file electronically. Filing electronically can also result in quicker processing times for any return or refund owed.

When businesses set out to fill the IRS 1120 form, which is essential for reporting their income, gains, losses, deductions, and credits to the Internal Revenue Service, a few common errors can occur. Avoiding these mistakes is crucial for ensuring the process is as smooth and accurate as possible.

Not incorporating all necessary schedules and forms - Many businesses overlook the need to attach necessary schedules and forms that support or are required alongside the main 1120 form. This can lead to incomplete filing and potential requests for more information from the IRS.

Misclassifying dividends and distributions - A frequent mistake involves improperly classifying dividends and distributions, which can impact how income is taxed. Businesses must pay close attention to the classification to ensure accurate tax treatment.

Incorrectly reporting income - Reporting business income requires attention to detail. Errors often occur when businesses fail to correctly report their total income or mistakenly include non-taxable income as taxable.

Overlooking deductions and credits - Businesses sometimes miss out on valuable deductions and credits due to a lack of knowledge or oversight. Properly identifying and claiming all eligible deductions and credits can significantly lower a company's tax liability.

Failing to sign and date the form - Although it may seem like a simple step, forgetting to sign and date the form is a common mistake that can delay processing. An unsigned form is considered incomplete and will not be processed by the IRS until corrected.

Being diligent and thorough when completing the IRS 1120 form is essential for any business. Taking the time to double-check information, include all necessary documentation, and understand the tax implications of income and deductions can help avoid the above mistakes. By doing so, businesses can ensure a smoother filing process and potentially save money on their taxes.

Filing taxes for a corporation involves more than just completing the IRS Form 1120, which is the U.S. Corporation Income Tax Return. Corporations are also required to complete additional forms and documents that provide further details about their financial activities throughout the tax year. These documents are crucial for the accurate assessment of the corporation's tax obligations and potential refunds. Here are some key forms and documents often used alongside Form 1120:

In conclusion, while the IRS Form 1120 is critical, the complete picture of a corporation's financial activities and tax obligations involves multiple forms and documents. Each document provides detailed information in specific areas, from compensation and benefits to asset depreciation and the sale of property. Corporations must ensure they complete all relevant forms accurately to comply with tax laws and optimize their tax positions.

When delving into the realm of corporate taxation in the United States, the IRS Form 1120 stands out as a primary document, required annually by the Internal Revenue Service (IRS) from corporations. It serves as the U.S. Corporation Income Tax Return, detailed in reporting a company's income, gains, losses, deductions, credits, and to calculate the income tax liability of corporations. Similar instruments exist within the tax code and beyond, each tailored to specific entities or purposes, but sharing core functionalities with the IRS 1120 form. Here are eight such documents:

Though each of these documents serves different types of entities or specific circumstances within the tax law, they are interconnected in the broader tapestry of U.S. tax compliance, reflecting the complexity and diversity of the American economic landscape. This array of forms underscores a unified goal: to report and regulate the financial activities of businesses and entities, ensuring fair contribution to the public coffers.

Filing the IRS 1120 form, also known as the U.S. Corporation Income Tax Return, is a critical task for corporations. It's important to approach this responsibility with diligence and accuracy to ensure compliance with tax laws. Here is a concise guide to help you navigate the process smoothly.

Do's:

Ensure accuracy of your Employer Identification Number (EIN). It's essential for the IRS to identify your business correctly.

Report all income accurately. This includes gross receipts, sales, dividends, and any other income your corporation has received.

Deduct eligible business expenses. Keep in mind only legitimate business expenses can be deducted.

Take advantage of tax credits. There are various credits available that can reduce your tax liability.

File on time. The deadline is typically April 15th, but if it falls on a weekend or holiday, it moves to the next business day.

Sign the form. An unsigned return is like an unsigned check – it's not valid.

Utilize electronic filing. It’s faster, more secure, and you get a confirmation receipt.

Keep a copy of your return. It's important for your records and future reference.

Report your assets and liabilities correctly. This includes your corporation’s balance sheet.

Seek professional help if needed. Consulting with a tax professional can provide guidance and ease the process.

Don'ts:

Don’t estimate figures. Use actual numbers to avoid discrepancies that could trigger an audit.

Don’t forget to report all income. Unreported income can lead to penalties and interest.

Don’t deduct personal expenses. Only business-related expenses are deductible.

Don’t overlook details. Small mistakes can cause delays or incorrect calculations of your tax liability.

Don’t miss out on deductions and credits. Do thorough research or consult with a professional.

Don’t file late. Late filing can result in penalties and interest charges.

Don’t ignore IRS notices. If you receive one, respond promptly and accurately.

Don’t submit incomplete forms. Ensure all required fields and schedules are filled out.

Don’t forget to review your return. Double-check all entries before submitting.

Don’t hesitate to amend if necessary. If you find an error after filing, you can correct it by filing an amended return.

All businesses must file an IRS 1120 form. This is a common misconception. The IRS Form 1120 is specifically for corporations, including C corporations. Sole proprietorships, partnerships, and S corporations have different forms to file, such as the 1040 (Schedule C), 1065, and 1120S forms, respectively.

Extensions to file give you more time to pay taxes owed. While filing for an extension grants corporations additional time to submit their 1120 form, it does not extend the deadline to pay any taxes owed. Taxes are due by the original filing deadline, and failure to pay them on time may result in interest and penalties.

Filing electronically is optional. Many believe filing electronically is a choice, but corporations with assets of $10 million or more and filing at least 250 returns a year are required to file the Form 1120 electronically. Electronic filing has become the standard for its efficiency and is encouraged for all others.

The 1120 form is just for reporting income. This is not entirely true. While the Form 1120 is used to report income, deductions, and credits, it also serves other purposes. For example, it is used to calculate the corporation's income tax liability and report other information such as dividends paid and accumulated earnings.

1120 forms do not need to be signed. A significant oversight is the assumption that the 1120 form does not require a signature. In fact, like many other tax forms, the IRS Form 1120 must be signed and dated by an officer of the corporation empowered to do so. Electronic signatures are accepted for electronically filed forms.

If your corporation didn't make money, you don't need to file Form 1120. This misconception can lead to trouble. Regardless of whether your corporation made or lost money, it is required to file a return. The lack of income does not exempt a corporation from filing Form 1120, as it may still be liable for other types of taxes or required to report certain information.

IRS Form 1120 is the same as Form 1120S. Though they sound similar, IRS Form 1120 and Form 1120S serve different purposes. Form 1120 is for C corporations, while Form 1120S is for S corporations, which are taxed differently under the United States tax code. It's essential to understand the distinctions to ensure compliance with IRS requirements.

The IRS 1120 form, also known as the U.S. Corporation Income Tax Return, is a critical document for corporations operating within the United States. It serves as the principal form that corporations use to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Understanding how to properly fill out and use this form is essential for maintaining compliance with U.S. tax law. Here are six key takeaways for anyone tasked with this responsibility:

Filling out and submitting the IRS 1120 form accurately is vital for any corporation. It not only ensures compliance with tax laws but also helps in managing the corporation's financial health. Seeking advice from tax professionals can provide additional guidance and reduce the risk of errors.

Al Cpt Instructions - It ensures that all actions taken are documented and reported to the court.

Alabama Llc Taxes - Taxpayers are encouraged to review the instructions carefully before submission.

State of Michigan 2022 Tax Forms - Income tax withholding amounts must also be included in the report.