The IRS 1023-EZ form plays a crucial role for small nonprofit organizations seeking tax-exempt status under section 501(c)(3) of the Internal Revenue Code. Designed to simplify the application process, this streamlined form allows eligible organizations to apply for recognition of exemption without the extensive documentation required by the standard IRS Form 1023. To qualify for the 1023-EZ, an organization must meet specific criteria, including having gross receipts of $50,000 or less in the past three years and total assets not exceeding $250,000. The form requires basic information about the organization, such as its structure, purpose, and activities, along with a declaration of its eligibility. By using the 1023-EZ, organizations can save time and resources, making it an appealing option for many small charities and nonprofits. However, it is important to ensure that all eligibility requirements are met before submission, as errors or omissions can lead to delays or denials in obtaining tax-exempt status.

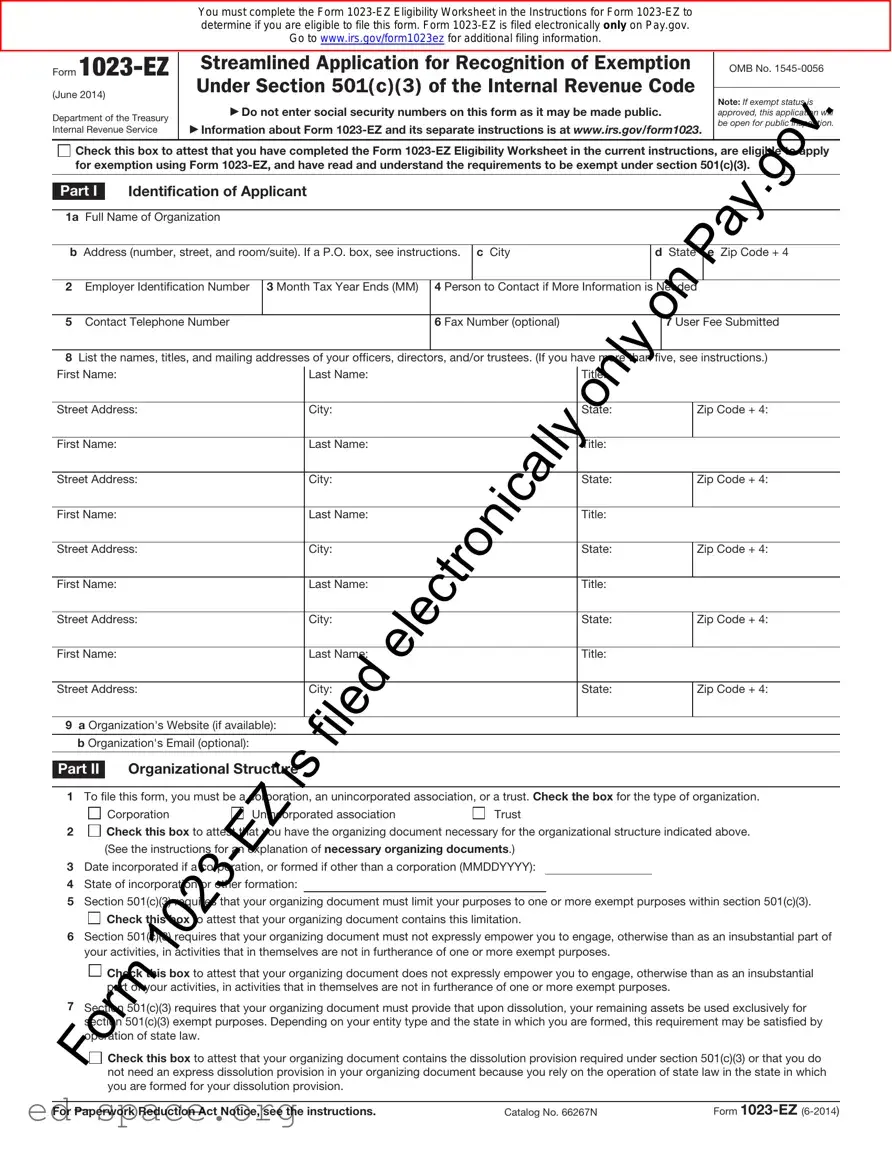

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Form

(June 2014)

Department of the Treasury Internal Revenue Service

Streamlined Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code

Do not enter social security numbers on this form as it may be made public.

Information about Form

OMB No.

Note: If exempt status is approved, this application will be open for public inspection.

Check this box to attest that you have completed the Form

Part I Identification of Applicant

1a Full Name of Organization

bAddress (number, street, and room/suite). If a P.O. box, see instructions.

cCity

dState

eZip Code + 4

2 |

Employer Identification Number |

3 Month Tax Year Ends (MM) |

4 Person to Contact if More Information is Needed |

|

|

|

|

|

|

5 |

Contact Telephone Number |

|

6 Fax Number (optional) |

7 User Fee Submitted |

|

|

|

|

|

8List the names, titles, and mailing addresses of your officers, directors, and/or trustees. (If you have more than five, see instructions.)

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Name: |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

First Name: |

Last Nam : |

Title: |

|

|

|

|

|

Street Address: |

City: |

State: |

Zip Code + 4: |

|

|

|

|

9 a Organization's Website (if available): |

|

|

|

|

|

|

|

b Organization's Email (optional): |

|

|

|

|

|

|

|

Part II Organizational Structure

1To file this form, you must be a corporation, an unincorporated association, or a trust. Check the box for the type of organization.

|

Corporation |

Unincorporated association |

Trust |

2 |

Check this box to attest that you have the organizing document necessary for the organizational structure indicated above. |

||

(See the instructions for an explanation of necessary organizing documents.)

3Date incorporated if a corporation, or formed if other than a corporation (MMDDYYYY):

4State of incorporation or other formation:

5Section 501(c)(3) requires that your organizing document must limit your purposes to one or more exempt purposes within section 501(c)(3).

Check this box to attest that your organizing document contains this limitation.

6Section 50 (c)(3) requires that your organizing document must not expressly empower you to engage, otherwise than as an insubstantial part of your activities, in activities that in themselves are not in furtherance of one or more exempt purposes.

Check this box to attest that your organizing document does not expressly empower you to engage, otherwise than as an insubstantial part of your activities, in activities that in themselves are not in furtherance of one or more exempt purposes.

7Section 501(c)(3) requires that your organizing document must provide that upon dissolution, your remaining assets be used exclusively for secti n 501(c)(3) exempt purposes. Depending on your entity type and the state in which you are formed, this requirement may be satisfied by

peration of state law.

Check this box to attest that your organizing document contains the dissolution provision required under section 501(c)(3) or that you do not need an express dissolution provision in your organizing document because you rely on the operation of state law in the state in which you are formed for your dissolution provision.

For Paperwork Reduction Act Notice, see the instructions. |

Catalog No. 66267N |

Form |

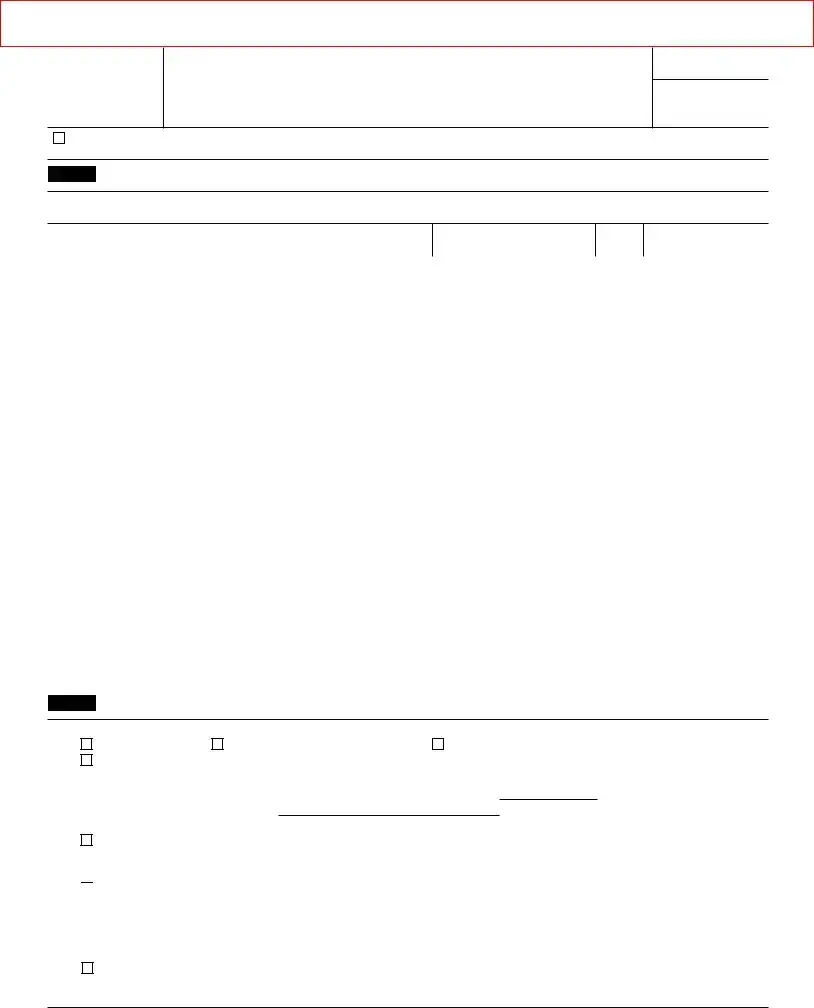

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Form |

Page 2 |

Part III Your Specific Activities

1Enter the appropriate

2 To qualify for exemption as a section 501(c)(3) organization, you must be organized and operated exclusively to further one or more f the following purposes. By checking the box or boxes below, you attest that you are organized and operated exclusively to further the purp ses indicated. Check all that apply.

Charitable |

Religious |

Educational |

Scientific |

Literary |

Testing for public safety |

To foster national or international amateur sports competition |

Prevention of cruelty to children or animals |

|

3To qualify for exemption as a section 501(c)(3) organization, you must:

•Refrain from supporting or opposing candidates in political campaigns in any way.

•Ensure that your net earnings do not inure in whole or in part to the benefit of private shareholders or individuals (that is, board members, officers, key management employees, or other insiders).

•Not further

•Not be organized or operated for the primary purpose of conducting a trade or business that is not related to y ur exempt purpose(s).

• Not devote more than an insubstantial part of your activities attempting to influence legislation or, if ou made a section 501(h) election, not normally make expenditures in excess of expenditure limitations outlined in section 501(h).

•Not provide

Check this box to attest that you have not conducted and will not conduct activities that violate these prohibitions and restrictions.

4 |

Do you or will you attempt to influence legislation? |

|

Yes |

|

No |

|

(If yes, consider filing Form 5768. See the instructions for more details.) |

|

|

|

|

5 |

Do you or will you pay compensation to any of your officers, directors, or trustees? |

|

Yes |

|

No |

|

|

||||

|

(Refer to the instructions for a definition of compensation.) |

|

|

|

|

6 |

Do you or will you donate funds to or pay expenses for individual(s)? |

|

Yes |

|

No |

|

|

||||

7 |

Do you or will you conduct activities or provide grants or other assistance to individu l(s) or organization(s) outside the |

|

|

|

|

8 |

United States? |

|

Yes |

|

No |

Do you or will you engage in financial transactions (for example, loans, payme ts, rents, etc.) with any of your officers, |

|

|

|

|

|

|

directors, or trustees, or any entities they own or control? |

|

Yes |

|

No |

9 |

Do you or will you have unrelated business gross income of $1,000 or m e during a tax year? |

|

Yes |

|

No |

|

|

||||

10 |

Do you or will you operate bingo or other gaming activities? |

|

Yes |

|

No |

|

|

||||

11 |

Do you or will you provide disaster relief? |

|

Yes |

|

No |

Part IV is designed to classify you as an organization thatelectronicallyis either private foundation or a public charity. Public charity status is a more favorable tax status than private foundation status.

Part IV Foundation Classification

1 If you qualify for public charity status, check the appropriate box (1a – 1c below) and skip to Part V below.

a

Check this box to attest that you normally r c ive at least

b

Check this box to attest that you normally receive more than

c |

Check this box to attest that you are operated for the benefit of a college or university that is owned or operated by a governmental unit. |

|

Sections 509(a)(1) and 170(b)(1)(A)(iv). |

2If you are not described in items 1a – 1c above, you are a private foundation. As a private foundation, you are required by section 508(e) to have specific provisions in your organizing document, unless you rely on the operation of state law in the state in which you were formed to meet these requirements. These specific provisions require that you operate to avoid liability for private foundation excise taxes under sections

Check this box to attest that your organizing document contains the provisions required by section 508(e) or that your organizing document does not need to include the provisions required by section 508(e) because you rely on the operation of state law in your particular state to meet the requirements of section 508(e). (See the instructions for explanation of the section 508(e) requirements.)

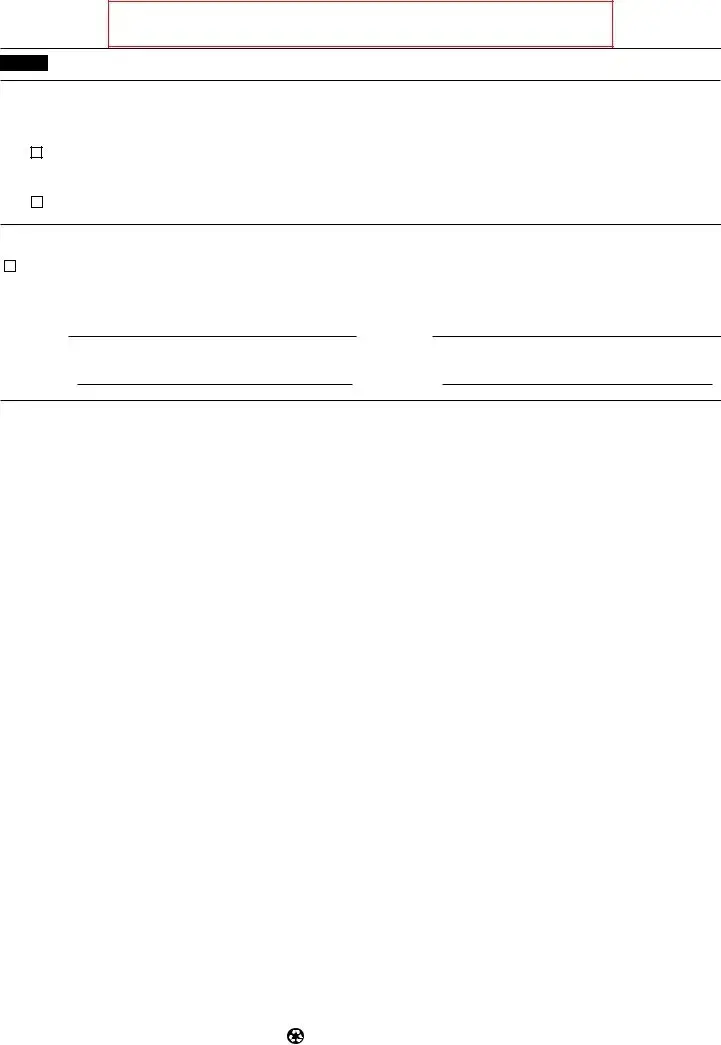

Form

Form

You must complete the Form

Go to www.irs.gov/form1023ez for additional filing information.

Page 3

Part V Reinstatement After Automatic Revocation

Complete this section only if you are applying for reinstatement of exemption after being automatically revoked for failure to file required annual returns or notices for three consecutive years, and you are applying for reinstatement under section 4 or 7 of Revenue Procedure

1

2

Check this box if you are seeking retroactive reinstatement under section 4 of Revenue Procedure

Check this box if you are seeking reinstatement under section 7 of Revenue Procedure

Part VI |

Signature |

|

|

I declare under the penalties of perjury that I am authorized to sign this application on behalf of the above organization and that I have examined this application, and to the best of my knowledge it is true, correct, and complete.

PLEASE SIGN HERE

(Type name of signer)

F(Signature of Officer, Director, Trustee, or other authorized official)

(Type title or authority of signer)

F(Date)

Form

Printed on recycled paper

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1023-EZ is used by small tax-exempt organizations to apply for 501(c)(3) status. |

| Eligibility | Organizations with gross receipts of $50,000 or less and total assets under $250,000 can use this form. |

| Filing Fee | The filing fee for Form 1023-EZ is $275 as of the latest guidelines. |

| Online Submission | Form 1023-EZ must be filed online through the IRS website. |

| Processing Time | Typically, the IRS processes Form 1023-EZ within 2 to 4 weeks. |

| State-Specific Forms | Some states require additional forms for tax-exempt status. For example, California requires Form CT-1. |

| Governing Law | State-specific governing laws vary. For California, refer to the California Nonprofit Corporation Law. |

| Common Mistakes | Incomplete applications and incorrect eligibility checks are common pitfalls. |

| Resources | The IRS provides a user guide and FAQs for further assistance with Form 1023-EZ. |

Filling out the IRS 1023-EZ form is an important step toward obtaining tax-exempt status for your organization. It’s essential to have all the necessary information ready before you begin. This process can seem daunting, but by following these steps, you will be able to complete the form accurately and efficiently.

After submitting the form, you will need to wait for a response from the IRS. They will review your application and may contact you for additional information. Patience is essential during this time, as processing can take several months. Stay organized and keep track of any correspondence you receive from the IRS.

What is the IRS 1023-EZ form?

The IRS 1023-EZ form is a streamlined application for small tax-exempt organizations to obtain recognition of their tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. This simplified form allows eligible organizations to apply for tax-exempt status without the extensive documentation required by the standard Form 1023. It is designed for organizations with annual gross receipts of $50,000 or less and total assets of $250,000 or less.

Who is eligible to file the 1023-EZ form?

Eligibility to file the 1023-EZ form is limited to organizations that meet specific criteria. To qualify, an organization must be a nonprofit corporation or unincorporated association, have a stated purpose that aligns with charitable, educational, religious, or scientific purposes, and meet the financial thresholds mentioned earlier. Additionally, certain types of organizations, such as those that are foreign entities or those that have previously had their tax-exempt status revoked, cannot use this form.

How long does it take to process the 1023-EZ form?

Processing times for the 1023-EZ form can vary, but they are generally quicker than the standard Form 1023. Many organizations report receiving a determination letter from the IRS within 2 to 4 weeks after submission. However, processing times may be longer during peak periods or if the application requires additional review. It is advisable to check the IRS website for current processing times and updates.

What happens after the IRS approves the 1023-EZ form?

Once the IRS approves the 1023-EZ form, the organization will receive a determination letter confirming its tax-exempt status. This letter is important for establishing eligibility for tax-deductible donations and for applying for grants. Organizations must also comply with ongoing requirements, such as filing annual returns and maintaining their nonprofit status, to retain their tax-exempt status.

Inaccurate Eligibility Determination: Many applicants fail to properly assess whether they meet the eligibility criteria for using the 1023-EZ form. This can lead to delays or denials.

Incomplete Information: Some individuals do not provide all required information. Omitting details can result in rejection or requests for additional documentation.

Incorrect Financial Data: Errors in reporting financial data, such as revenue or expenses, can create significant issues. Double-check figures to ensure accuracy.

Failure to Sign: Neglecting to sign the form can lead to automatic rejection. Ensure that all required signatures are included before submission.

Not Following Instructions: Some applicants overlook specific instructions provided with the form. Adhering to guidelines is crucial for a smooth application process.

Misunderstanding the Purpose: Misinterpreting the purpose of the 1023-EZ can lead to filing the wrong form. Understand the requirements before proceeding.

Ignoring State Requirements: Some applicants forget that state-level regulations may also apply. Research local laws to ensure compliance.

Submitting Without Review: Rushing the submission without a thorough review can result in mistakes. Take the time to proofread the entire application.

Missing Deadlines: Failing to submit the application within required timelines can jeopardize the status. Be aware of all relevant deadlines.

The IRS 1023-EZ form is a streamlined application for organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. When completing this form, several other documents may be required to support the application and provide additional context about the organization. Below is a list of common forms and documents that are often submitted alongside the IRS 1023-EZ form.

Providing these documents along with the IRS 1023-EZ form can enhance the application’s clarity and strengthen the case for tax-exempt status. It is important to ensure that all submitted materials are accurate and reflect the organization’s commitment to its mission.

The IRS Form 1023-EZ is a streamlined application for organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Several other documents serve similar purposes in various contexts. Below are four documents that share similarities with the 1023-EZ form:

When filling out the IRS 1023-EZ form, it’s essential to approach the task with care. This form is used by small organizations to apply for tax-exempt status under section 501(c)(3) of the Internal Revenue Code. Here’s a list of things you should and shouldn’t do to ensure a smooth application process.

Following these guidelines can significantly improve your chances of a successful application. Taking the time to do it right pays off in the long run.

The IRS 1023-EZ form is a simplified application for small tax-exempt organizations seeking 501(c)(3) status. Despite its straightforward nature, several misconceptions can lead to confusion. Below is a list of common misunderstandings about the 1023-EZ form, along with clarifications.

Understanding these misconceptions can help organizations navigate the process more effectively and increase their chances of successfully obtaining tax-exempt status.

The IRS 1023-EZ form is a streamlined application for small organizations seeking tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Here are some key takeaways to keep in mind when filling out and using this form:

Understanding these points can greatly enhance your experience with the IRS 1023-EZ form, ensuring a smoother application process for your organization.