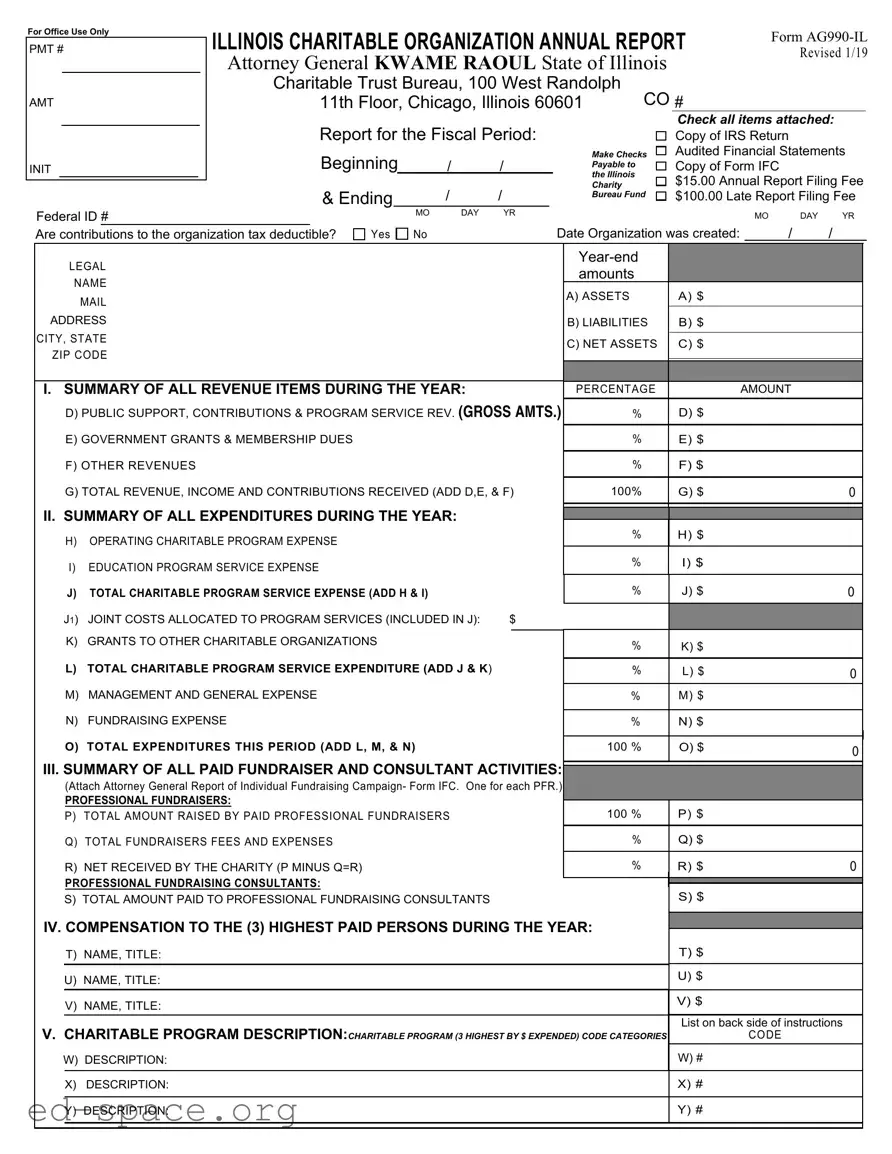

The Illinois AG990 form serves as an essential tool for charitable organizations operating within the state. This annual report is mandated by the Illinois Attorney General's office and provides a comprehensive overview of an organization's financial activities during the fiscal year. Key components of the form include detailed summaries of revenue and expenditures, allowing organizations to report public support, contributions, government grants, and various other income sources. Furthermore, it requires organizations to disclose their liabilities and net assets, ensuring transparency regarding their financial health. The AG990 also emphasizes accountability by necessitating information about fundraising activities, including amounts raised by professional fundraisers and the associated fees. Additionally, organizations must report compensation for their highest-paid personnel and provide descriptions of their charitable programs. The form also includes a series of yes-or-no questions aimed at identifying any legal or financial irregularities, which could impact the organization's standing. Timely submission of the AG990 is crucial, as late filings incur penalties, underscoring the importance of compliance for maintaining good standing with state authorities.

For Office Use Only

PMT #

AMT

INIT

ILLINOIS CHARITABLE ORGANIZATION ANNUAL REPORT |

Form |

|||||||||||||||

|

Revised 1/19 |

|||||||||||||||

Attorney General KWAME RAOUL State of Illinois |

|

|

||||||||||||||

|

|

|

|

|||||||||||||

Charitable Trust Bureau, 100 West Randolph |

|

|

|

|

||||||||||||

11TH Floor, Chicago, Illinois 60601 |

CO # |

|

|

|

||||||||||||

Report for the Fiscal Period: |

|

|

|

|

|

|

Check all items attached: |

|

||||||||

|

|

|

|

|

|

Copy of IRS Return |

|

|

||||||||

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

Audited Financial Statements |

||||||

Beginning |

/ |

/ |

|

|

Make Checks |

|

|

|||||||||

|

|

|

||||||||||||||

|

|

Payable to |

|

|

|

Copy of Form IFC |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

the Illinois |

|

|

|

$15.00 Annual Report Filing Fee |

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||

& Ending |

/ |

/ |

|

|

Charity |

|

|

|||||||||

|

|

|

||||||||||||||

|

|

Bureau Fund |

|

|

|

|

|

$100.00 Late Report Filing Fee |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Federal ID # |

|

|

MO |

DAY |

YR |

|

|

MO |

DAY |

YR |

|

||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

Date Organization was created: |

/ |

/ |

|

||||

Are contributions to the organization tax deductible? |

|

Yes |

|

No |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LEGAL |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

amounts |

|

|

|

|

|

||||

|

NAME |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

A) ASSETS |

A) $ |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

ADDRESS |

|

|

|

|

|

|

|

B) LIABILITIES |

B) $ |

|

|

|

|||||

CITY, STATE |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

C) NET ASSETS |

C) $ |

|

|

|

||||||

ZIP CODE |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I. SUMMARY OF ALL REVENUE ITEMS DURING THE YEAR: |

|

|

|

PERCENTAGE |

AMOUNT |

|

|

||||||||||

|

D) PUBLIC SUPPORT, CONTRIBUTIONS & PROGRAM SERVICE REV. (GROSS AMTS.) |

% |

D) $ |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E) GOVERNMENT GRANTS & MEMBERSHIP DUES |

|

|

|

|

|

|

|

% |

E) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

F) OTHER REVENUES |

|

|

|

|

|

|

|

% |

F) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

G) TOTAL REVENUE, INCOME AND CONTRIBUTIONS RECEIVED (ADD D,E, & F) |

100% |

G) $ |

|

0 |

|

|||||||||||

II. SUMMARY OF ALL EXPENDITURES DURING THE YEAR: |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

H) OPERATING CHARITABLE PROGRAM EXPENSE |

|

|

|

|

|

|

|

% |

H) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

I) EDUCATION PROGRAM SERVICE EXPENSE |

|

|

|

|

|

|

|

% |

I) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

J) TOTAL CHARITABLE PROGRAM SERVICE EXPENSE (ADD H & I) |

|

|

|

|

% |

J) $ |

|

0 |

|

|||||||

J1) JOINT COSTS ALLOCATED TO PROGRAM SERVICES (INCLUDED IN J): |

$ |

|

|

|

|

|

|

|

|||||||||

|

K) GRANTS TO OTHER CHARITABLE ORGANIZATIONS |

|

|

|

|

% |

K) $ |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

L) TOTAL CHARITABLE PROGRAM SERVICE EXPENDITURE (ADD J & K) |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

% |

L) $ |

|

0 |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

M) MANAGEMENT AND GENERAL EXPENSE |

|

|

|

|

|

|

|

% |

M) $ |

|

|

|

||||

|

N) FUNDRAISING EXPENSE |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

% |

N) $ |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

O) TOTAL EXPENDITURES THIS PERIOD (ADD L, M, & N) |

|

|

|

|

100 % |

O) $ |

|

0 |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

III. SUMMARY OF ALL PAID FUNDRAISER AND CONSULTANT ACTIVITIES: |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

||||||||||||

|

(Attach Attorney General Report of Individual Fundraising Campaign- Form IFC. One for each PFR.) |

|

|

|

|

|

|

||||||||||

|

PROFESSIONAL FUNDRAISERS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

P) TOTAL AMOUNT RAISED BY PAID PROFESSIONAL FUNDRAISERS |

|

|

|

|

100 % |

P) $ |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q) TOTAL FUNDRAISERS FEES AND EXPENSES |

|

|

|

|

|

|

|

% |

Q) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R) NET RECEIVED BY THE CHARITY (P MINUS Q=R) |

|

|

|

|

|

|

|

% |

R) $ |

|

0 |

|

||||

|

PROFESSIONAL FUNDRAISING CONSULTANTS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

S) $ |

|

|

|

|||||

|

S) TOTAL AMOUNT PAID TO PROFESSIONAL FUNDRAISING CONSULTANTS |

|

|

|

|

|

|

|

|||||||||

IV. COMPENSATION TO THE (3) HIGHEST PAID PERSONS DURING THE YEAR: |

|

|

|

|

|

||||||||||||

|

|

|

|

|

|||||||||||||

T) $ |

|

|

|

||||||||||||||

|

T) NAME, TITLE: |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

U) NAME, TITLE: |

|

|

|

|

|

|

|

|

U) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

V) NAME, TITLE: |

|

|

|

|

|

|

|

|

V) $ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

V. CHARITABLE PROGRAM DESCRIPTION:CHARITABLE PROGRAM (3 HIGHEST BY $ EXPENDED) CODE CATEGORIES |

List on back side of instructions |

|

|||||||||||||||

|

CODE |

|

|

|

|||||||||||||

W) DESCRIPTION: |

|

|

|

|

|

|

|

|

W) # |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

X) DESCRIPTION: |

|

|

|

|

|

|

|

|

X) # |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Y) DESCRIPTION: |

|

|

|

|

|

|

|

|

Y) # |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

IF THE ANSWER TO ANY OF THE FOLLOWING IS YES, ATTACH A DETAILED EXPLANATION: |

YES NO |

1. WAS THE ORGANIZATION THE SUBJECT OF ANY COURT ACTION, FINE, PENALTY OR JUDGMENT? |

1. |

2.HAS THE ORGANIZATION OR A CURRENT DIRECTOR, TRUSTEE, OFFICER OR EMPLOYEE THEREOF, EVER BEEN CONVICTED BY ANY COURT OF ANY MISDEMEANOR INVOLVING THE MISUSE OR

MISAPPROPRIATION OF FUNDS OR ANY FELONY? |

2 |

3.DID THE ORGANIZATION MAKE A GRANT AWARD OR CONTRIBTION TO ANY ORGANIZATION IN WHICH ANY OF ITS OFFICERS, DIRECTORS OR TRUSTEES OWNS AN INTEREST; OR WAS IT A PARTY TO ANY TRANSACTION IN WHICH ANY OF ITS OFFICERS, DIRECTORS OR TRUSTEES HAS A MATERIAL FINANCIAL INTEREST; OR DID

ANY OFFICER, DIRECTOR OR TRUSTEE RECEIVE ANYTHING OF VALUE NOT REPORTED AS COMPENSATION? |

3. |

4. HAS THE ORGANIZATION INVESTED IN ANY CORPORATE STOCK IN WHICH ANY OFFICER, DIRECTOR OR |

|

TRUSTEE OWNS MORE THAN 10% OF THE OUTSTANDING SHARES? |

4. |

5.IS ANY PROPERTY OF THE ORGANIZATION HELD IN THE NAME OF OR COMMINGLED WITH THE

PROPERTY OF ANY OTHER PERSON OR ORGANIZATION? |

|

5. |

|

6. DID THE ORGANIZATION USE THE SERVICES OF A PROFESSIONAL FUNDRAISER? |

( ATTACH FORM IFC ) |

6. |

|

7a. DID THE ORGANIZATION ALLOCATE THE COST OF ANY SOLICITATION, MAILING, ADVERTISEMENT OR |

|

||

LITERATURE COSTS BETWEEN PROGRAM SERVICE AND FUNDRAISING EXPENSES? |

|

7. |

|

|

|

||

7b. IF "YES", ENTER (i) THE AGGREGATE AMOUNT OF THESE JOINT COSTS $ |

;(ii) THE AMOUNT |

||

ALLOCATED TO PROGRAM SERVICES $ |

; (iii) THE AMOUNT ALLOCATED TO MANAGEMENT |

||

AND GENERAL $ |

;AND (iv) THE AMOUNT ALLOCATED TO FUNDRAISING $ |

|

|

8. DID THE ORGANIZATION EXPEND ITS RESTRICTED FUNDS FOR PURPOSES OTHER THAN RESTRICTED |

|

||

PURPOSES? |

|

|

8. |

|

|

|

|

9. HAS THE ORGANIZATION EVER BEEN REFUSED REGISTRATION OR HAD ITS REGISTRATION OR TAX EXEMPTION |

|

||

SUSPENDED OR REVOKED BY ANY GOVERNMENTAL AGENCY? |

|

9. |

|

10. WAS THERE OR DO YOU HAVE ANY KNOWLEDGE OF ANY KICKBACK, BRIBE, OR ANY THEFT, DEFALCATION, |

|

||

MISAPPROPRIATION, COMMINGLING OR MISUSE OF ORGANIZATIONAL FUNDS? |

|

10. |

|

11.LIST THE NAME AND ADDRESS OF THE FINANCIAL INSTITUTIONS WHERE THE ORGANIZATION MAINTAINS ITS THREE LARGEST ACCOUNTS:

12.NAME AND TELEPHONE NUMBER OF CONTACT PERSON:

ALL ATTACHMENTS MUST ACCOMPANY THIS REPORT - SEE INSTRUCTIONS

UNDER PENALTY OF PERJURY, I (WE) THE UNDERSIGNED DECLARE AND CERTIFY THAT I (WE) HAVE EXAMINED THIS ANNUAL REPORT AND THE ATTACHED DOCUMENTS, INCLUDING ALL THE SCHEDULES AND STATEMENTS, AND THE FACTS THEREIN STATED ARE TRUE AND COMPLETE AND FILED WITH THE ILLINOIS ATTORNEY GENERAL FOR THE PURPOSE OF HAVING THE PEOPLE OF THE STATE OF ILLINOIS RELY THEREUPON. I HEREBY FURTHER AUTHORIZE AND AGREE TO SUBMIT MYSELF AND THE REGISTRANT HEREBY TO THE JURISDICTION OF THE STATE OF ILLINOIS.

BE SURE TO INCLUDE ALL FEES DUE:

1.)REPORTS ARE DUE WITHIN SIX MONTHS OF YOUR FISCAL YEAR END.

2.)FOR FEES DUE SEE INSTRUCTIONS.

3.)REPORTS THAT ARE LATE OR INCOMPLETE ARE SUBJECT TO A $100.00 PENALTY.

PRESIDENT or TRUSTEE (PRINT NAME) |

SIGNATURE |

DATE |

|

|

|

TREASURER or TRUSTEE (PRINT NAME) |

SIGNATURE |

DATE |

PREPARER (PRINT NAME) |

SIGNATURE |

DATE |

| Fact Name | Description |

|---|---|

| Form Purpose | The Illinois AG990 form serves as the annual report for charitable organizations operating within the state. It provides essential financial information to the Attorney General's office. |

| Governing Law | This form is governed by the Illinois Charitable Trust Act, which mandates reporting requirements for charitable organizations. |

| Filing Fee | Organizations must pay a $15.00 filing fee when submitting the AG990 form. A late fee of $100.00 applies if the report is submitted after the deadline. |

| Tax Deductibility | The form includes a question regarding the tax deductibility of contributions made to the organization, which is crucial for donors. |

| Revenue Reporting | Organizations must summarize all revenue received during the fiscal year, categorizing it into public support, government grants, and other revenues. |

| Expenditure Details | The AG990 form requires a detailed breakdown of expenditures, including operating expenses, charitable program expenses, and fundraising costs. |

Completing the Illinois AG990 form is an important step for charitable organizations to report their annual financial activities. The following steps outline how to accurately fill out the form to ensure compliance with state regulations.

What is the Illinois AG990 form?

The Illinois AG990 form is an annual report required for charitable organizations operating in Illinois. This form provides the Attorney General's office with essential information about the organization's financial activities, including revenue, expenditures, and governance. It ensures transparency and accountability for nonprofits in the state.

Who needs to file the AG990 form?

Any charitable organization that operates in Illinois and is registered with the Attorney General's office must file the AG990 form. This includes organizations that receive contributions or grants, as well as those that engage in fundraising activities. Compliance is necessary to maintain good standing and tax-exempt status.

When is the AG990 form due?

The AG990 form is due within six months of the end of the organization’s fiscal year. It is crucial for organizations to be aware of their fiscal year-end date to ensure timely filing. Late submissions may incur penalties.

What are the fees associated with filing the AG990 form?

There is a $15.00 annual report filing fee required when submitting the AG990 form. If the report is filed late, a penalty of $100.00 may apply. Organizations should ensure that all fees are paid to avoid complications with their registration status.

What information is required on the AG990 form?

The AG990 form requires detailed financial information, including assets, liabilities, revenue sources, and expenditures. Organizations must provide summaries of public support, government grants, and other revenues, as well as a breakdown of expenses related to charitable programs, management, and fundraising.

Are contributions to organizations filing the AG990 form tax-deductible?

Whether contributions to an organization are tax-deductible depends on the organization's tax status. The AG990 form includes a question to indicate if contributions are tax-deductible. Organizations must check this box accordingly based on their IRS classification.

What happens if an organization does not file the AG990 form?

Failure to file the AG990 form can result in penalties and may jeopardize the organization’s registration status with the Attorney General's office. This can lead to loss of tax-exempt status and potential legal repercussions. It is essential for organizations to adhere to filing requirements to avoid these consequences.

What should organizations do if they have questions about completing the AG990 form?

If organizations have questions about the AG990 form, they can contact the Charitable Trust Bureau of the Illinois Attorney General’s office for guidance. It is advisable to review the instructions carefully and seek assistance if needed to ensure accurate and complete submissions.

Where can organizations find the AG990 form?

The AG990 form can be obtained from the Illinois Attorney General's website. Organizations should ensure they are using the most recent version of the form and follow the instructions provided for completing and submitting it correctly.

Incorrect Financial Information: Many people fail to provide accurate financial figures. This includes miscalculating total revenue, expenses, or net assets. Double-checking these numbers is essential to avoid discrepancies.

Missing Attachments: Some individuals forget to include necessary documents. These may include the IRS return or audited financial statements. Omitting these can lead to delays or rejections of the report.

Inaccurate Dates: Entering incorrect dates for the fiscal period or the organization’s creation is a common mistake. Ensure that all dates are accurate to maintain compliance with reporting requirements.

Failure to Answer All Questions: Some people overlook questions that require a yes or no answer. Each question is important and must be addressed to provide a complete picture of the organization’s activities.

Not Signing the Form: Lastly, neglecting to sign the form is a frequent error. Both the president and treasurer must sign to certify the accuracy of the report. Without these signatures, the form cannot be processed.

The Illinois AG990 form serves as an annual report for charitable organizations operating within the state. It provides a comprehensive overview of the organization's financial activities, ensuring transparency and accountability. Alongside this form, several other documents may be required or beneficial for a complete submission. Below are five commonly associated forms and documents.

Incorporating these documents alongside the Illinois AG990 form can enhance the overall clarity and integrity of the information presented. Properly completing and submitting these forms is essential for compliance and for fostering trust with donors and the community at large.

When completing the Illinois AG990 form, there are specific guidelines to follow to ensure accuracy and compliance. Below is a list of important dos and don'ts.

Following these guidelines will help ensure a smooth filing process for the Illinois AG990 form.

The Illinois AG990 form is a crucial document for charitable organizations operating in the state. However, several misconceptions surround its purpose and requirements. Here are six common misunderstandings:

This is not true. All charitable organizations, regardless of size, must file the AG990 form annually. It ensures transparency and accountability, which are essential for maintaining public trust.

While IRS registration is important, it does not exempt organizations from filing the AG990 form. State laws require this annual report to be submitted to the Illinois Attorney General’s office.

In addition to financial information, the form includes sections on governance, fundraising activities, and compliance with legal requirements. This comprehensive approach helps provide a full picture of the organization’s operations.

Contrary to this belief, late filings are subject to a $100 penalty. Organizations should be diligent in meeting the six-month deadline following their fiscal year-end to avoid these fees.

This is incorrect. Organizations must attach various documents, such as IRS returns and audited financial statements, to ensure the AG990 form is complete and valid.

Both the president and treasurer, or designated trustees, must sign the form. This requirement emphasizes the shared responsibility for the organization’s compliance and integrity.