The Illinois 700 form is essential for handling estate and generation-skipping transfer taxes for individuals who pass away on or after January 1, 2021. This form serves as the official return that must be filed with the Illinois Attorney General, outlining the decedent's estate and any taxes due. It can be submitted as an original return, a supplemental return if additional tax is owed, or an amended return if no extra tax is due. Key information required includes the decedent's date of death, address, Social Security number, and the name of the personal representative handling the estate. The form also asks whether a Federal Estate Tax Return is attached and if an Illinois QTIP election is being made. Additionally, it covers various scenarios regarding the estate's value and tax obligations, ensuring that all necessary details are included to avoid penalties. With proper completion, the Illinois 700 form helps manage the tax responsibilities effectively during a challenging time.

FORM 700

STATE OF ILLINOIS

ESTATE &

|

Original Return |

¨ |

|

Supplemental Return (Additional tax due.) |

¨ |

Amended Return (No additional tax due.) |

¨ |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

of: |

|

|

|

|

|

|

|

Date of Death |

||

|

Estate of: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Decedent’s Address (No. & Street): |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

Zip Code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Decedent’s Social Security Number: |

Name of Illinois County with Jurisdiction over Estate: |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Personal Representative or Person Filing Return: |

|

Telephone: |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (No. & Street): |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

Zip Code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Preparer: |

|

|

|

|

Telephone: |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (No. & Street): |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

Zip Code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

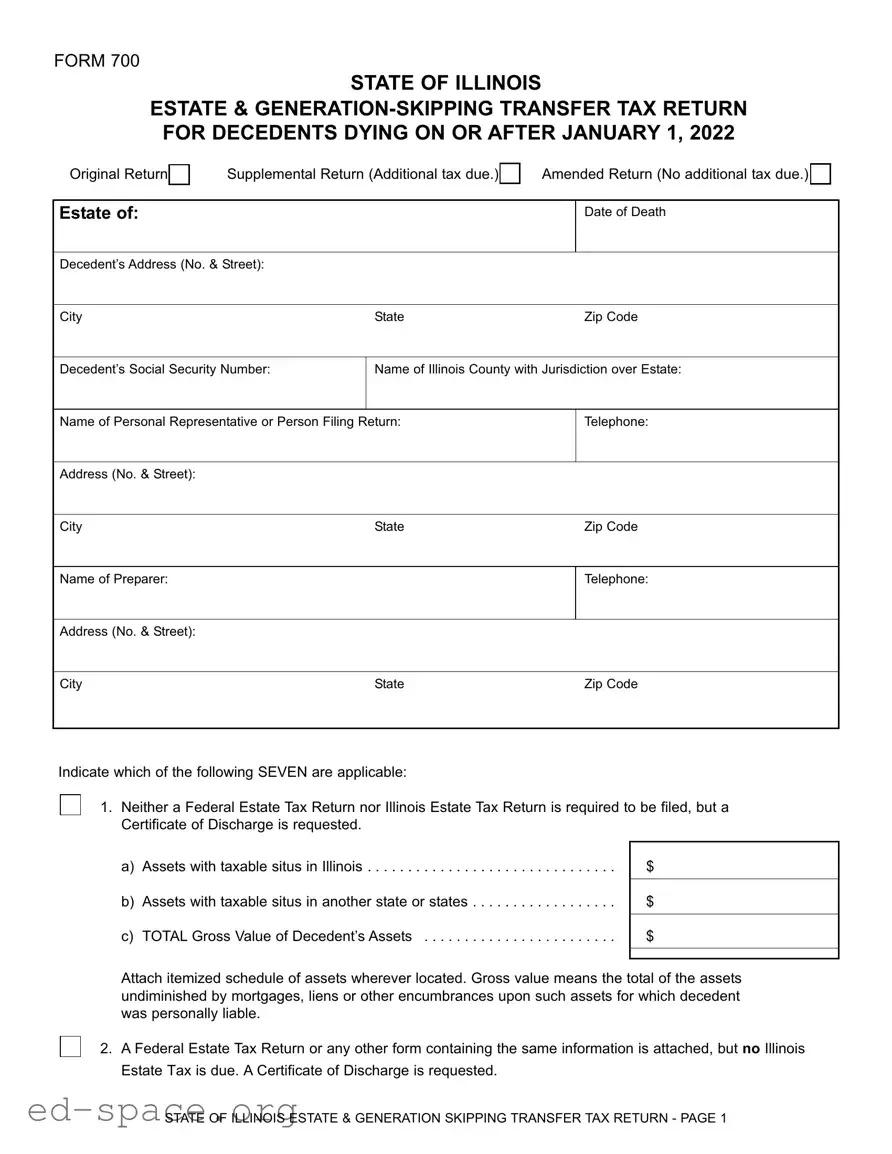

Indicate which of the following SEVEN are applicable:

1. Neither a Federal Estate Tax Return nor Illinois Estate Tax Return is required to be filed, but a Certificate of Discharge is requested.

a) Assets with taxable situs in Illinois . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

b) Assets with taxable situs in another state or states . . . . . . . . . . . . . . . . . .

c) TOTAL Gross Value of Decedent’s Assets . . . . . . . . . . . . . . . . . . . . . . . .

$

$

$

Attach itemized schedule of assets wherever located. Gross value means the total of the assets undiminished by mortgages, liens or other encumbrances upon such assets for which decedent was personally liable.

2.A Federal Estate Tax Return or any other form containing the same information is attached, but no Illinois Estate Tax is due. A Certificate of Discharge is requested.

STATE OF ILLINOIS ESTATE & GENERATION SKIPPING TRANSFER TAX RETURN - PAGE 1

3.A Federal Estate Tax Return or any other form containing the same information is attached (whether or not a Federal Estate Tax is due), and an Illinois Estate Tax is due. A Certificate of Discharge is requested. (Complete Recapitulation and Schedule A or B, whichever is applicable.)

4.An Illinois QTIP election is made for this estate.

Amount of Illinois QTIP election . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(Attach an itemized list of the Illinois QTIP property. If this includes trust property, state the percentage of the trust made subject to the election.)

Social Security Number of surviving spouse ____________________________

5.If a Section 6166 Election to Pay Tax in Installments is being requested, check box, attach an executed Form

Amount of deferred Illinois Estate Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$

$

6.This is an Amended or Supplemental Return.

(Complete Recapitulation and Schedule A or B, whichever is applicable, and attach copy of amended Federal Estate Tax Return or other applicable documents.)

Decedent was: |

|

|

||

|

|

|

|

|

|

|

a) |

a resident of Illinois, Year residency established |

a) |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

b) |

a |

b) |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

c) |

an alien, State of residence |

c) |

|

|

|||

|

|

|

|

|

|

|

|

|

|

Due date of this Return:

7. If an extension of time to file is being requested or if due date determined by extension of time to file Federal Estate Tax Return, check box and attach explanation for extension request or a copy of the Federal extension request. If based upon a Federal extension request, file a copy of approved extension request when available. This extension request should be filed within 9 months of date of death.

The undersigned declare, under penalties of perjury, that they have examined this return, including any and all accompanying schedules or attachments, and that they believe the same to be true and correct as to every material matter and further verify that any attached Federal Estate Tax Return and any other applicable Federal tax documents are true and corrected copies of the originals filed with the Internal Revenue Service.

The undersigned further certify that the attached Will (if decedent died testate) is a true and correct copy of the Will of the decedent.

Signature of decedent’s personal representative |

Title |

Date |

Signature of preparer |

Title |

Date |

STATE OF ILLINOIS ESTATE & GENERATION SKIPPING TRANSFER TAX RETURN - PAGE 2

SCHEDULE A – Resident Decedent’s Estate (Instructions on page 5.)

1. Tentative Taxable Estate from Federal Return (Line 3a, Form 706),

or other form containing the same information . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Illinois QTIP election

(Amount claimed as Illinois QTIP election in this estate or amount from prior estate’s Illinois QTIP election.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. Illinois Tentative Taxable Estate

(Line 1 minus Line 2 if the QTIP is elected in this estate; or line 1 plus line 2

if the QTIP was previously elected.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Adjusted taxable gifts

(Line 4, Form706, or any other form containing the same information.) . . . . . . . .

5. Illinois Tentative Taxable Estate plus adjusted taxable gifts

(Add Line 3 and Line 4.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Full amount computed for Illinois Estate Tax from website calculator before apportionment

(Use Lines 3 & 5 from this Form 700 for the website calculator.) . . . . . . . . . . . . .

7. Gross value of decedent’s estate having taxable situs in Illinois, plus amount added back from prior estate’s Illinois QTIP election . . . . . . . . . . . . . . . .

8. Gross value of decedent’s estate wherever located (Line 1, Form 706),

plus amount added back from prior estate’s Illinois QTIP election . . . . . . . . . . . .

9. Percent of estate having taxable situs in Illinois

(Line 7 divided by Line 8.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10. Amount of tax attributable to Illinois

(Line 6 multiplied by Line 9. Also enter on Line 1 in Recapitulation.) . . . . . . . . . .

1.$

2.$

3.$

4.$

5.$

6.$

7.$

8.$

9.%

10.$

With respect to the estate of a deceased resident of this State, all property included in the gross estate of the decedent for Federal Estate Tax purposes shall have a taxable situs in this State for purposes of this Section, excepting real estate and tangible personal property physically situated in another state (including any such property held in trust).

SCHEDULE B –

1. Tentative Taxable Estate from Federal Return (Line 3a, Form 706),

or other form containing the same information . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Illinois QTIP election

(Amount claimed as Illinois QTIP election in this estate or amount from prior estate’s Illinois QTIP election.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. Illinois Tentative Taxable Estate

(Line 1 minus Line 2 if the QTIP is elected in this estate; or line 1 plus line 2 if the QTIP was previously elected) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Adjusted taxable gifts

(Line 4, Form706, or any other form containing the same information.) . . . . . . . .

1.$

2.$

3$

4. $

Continued on Page 4.

STATE OF ILLINOIS ESTATE & GENERATION SKIPPING TRANSFER TAX RETURN - PAGE 3

SCHEDULE B –

5. Illinois Tentative Taxable Estate plus adjusted taxable gifts

(Add Line 3 and Line 4.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Full amount computed for Illinois Estate Tax from website calculator before apportionment

(Lines 3 & 5 from this Form 700 and applied to website calculator.) . . . . . . . . . .

7. Gross value of decedent’s estate having taxable situs in Illinois, plus amount added back from prior estate’s Illinois QTIP election . . . . . . . . . . . . . . . .

8. Gross value of decedent’s estate wherever located (Line 1, Form 706),

plus amount added back from prior estate’s Illinois QTIP election . . . . . . . . . . . .

9. Percent of estate having taxable situs in Illinois

(Line 7 divided by Line 8.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10. Amount of tax attributable to Illinois

(Line 6 multiplied by Line 9. Also enter on Line 1 in Recapitulation.) . . . . . . . . . .

5.$

6.$

7.$

8.$

9.%

10.$

In the case of a decedent who was a resident of this State at the time of death, all of the transferred property has a tax situs in this State, including any such property held in trust, except real or tangible personal property physically situated in another state.

In the case of a decedent who was not a resident of this State at the time of death, the transferred property having a tax situs in this State, including any such property held in trust, is only the real estate and tangible personal property physically situated in this State.

RECAPITULATION

1. Amount of tax payable to Illinois

(Schedule A Line 10 or Schedule B Line 10.) . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Late filing penalty

(5% of tax for each month or portion thereof - maximum penalty 25%.) . . . . . . .

3. Late payment penalty (1/2 of 1% of tax for each month

or portion thereof - maximum penalty 25%.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Interest at 10% per annum from 9 months

after death until date of payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Total Tax, penalties and interest payable

(Total of Lines 1, 2, 3 and 4.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Prior Payment

(Attach explanation.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. Balance due

(Line 5 minus Line 6.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1.$

2.$

3.$

4.$

5.$

6.$

7.$

STATE OF ILLINOIS ESTATE & GENERATION SKIPPING TRANSFER TAX RETURN - PAGE 4

FILING AND PAYMENT INSTRUCTIONS

For decedents dying prior to 2022, see the Returns previously posted on the Attorney General’s website covering the specific year of death.

For persons dying in 2022, the Federal exemption for Federal estate tax purposes is $12,060,000. The exclusion amount for Illinois estate tax purposes is $4,000,000. The exclusion amount operates as a taxable threshold and not as a credit against tax due. If an estate’s gross value exceeds $4 million after inclusion of adjusted taxable gifts, an Illinois Form 700 must be filed, whether or not a federal return is required by the Internal Revenue Service. The estate representative should prepare and submit the Illinois Form 700 with a Federal Form 706, including all schedules, appraisals, wills, trusts, attachments, etc. If an estate is not federally taxable and does not wish to submit a Form 706, the information may be presented in an alternate format as long as all necessary information is included. (See Ill. Admin Code tit. 86, §2000.110.) The Illinois estate tax will be determined using an interrelated calculation for 2022 decedents. The calculator at the Illinois Attorney General’s website (www.illinoisattorneygeneral.gov) may be used for this computation. To determine tax due, insert the amounts from Lines 3 and 5 of Schedule A or B, Form 700. Please note that the Calculator will not perform the computation unless amounts are entered into both fields.

When the tentative taxable estate plus adjusted taxable gifts exceeds $12,060,000 the Illinois Estate Tax Return, Form 700, must include a copy of the Federal Form 706 with all schedules and attachments.

For both resident and nonresident decedents, a preliminary tax prior to apportionment should be calculated assuming all assets are located within Illinois. (Line 6, Schedule A or B, Form 700). The apportioned tax can then be determined by multiplying that figure by the ratio of Illinois assets to total assets.

Illinois QTIP election (Qualified Terminable Interest Property):

For persons dying January 1, 2009 and after, the estate may make a QTIP election for Illinois purposes which is in addition to any Federal QTIP election. The Illinois QTIP must be elected on a timely filed Illinois return by checking the election box (pg. 2, box 4), inserting the dollar amount of the QTIP election, and providing the social security number of the surviving spouse. An itemized list of property included in the Illinois QTIP should be submitted with the return. The Illinois QTIP election will follow Federal statutes and rules for treatment of such elected property passing to the surviving spouse and inclusion for Illinois purposes on any Illinois Estate Tax Return of the surviving spouse, except as to the application of the Illinois Religious Freedom Protection and Civil Union Act to parties of a civil union for Illinois estate tax purposes.

THIS RETURN MUST BE FILED WITH THE ILLINOIS ATTORNEY GENERAL WITHIN NINE (9) MONTHS OF THE DATE OF DEATH. For Cook, DuPage, Lake, and McHenry Counties, file the original of the return with the Office of the Attorney General, Revenue Litigation Bureau, 100 West Randolph Street, 13th Floor, Chicago, Illinois 60601. For all other counties, file the original of the return with the Office of the Attorney General, Revenue Litigation Bureau, 500 South Second Street, Springfield, Illinois 62701.

PAYMENT OF ALL TAXES, INTEREST AND PENALTIES MUST BE MADE PAYABLE TO THE ILLINOIS STATE TREASURER WITH THE “ILLINOIS STATE TREASURER ESTATE TAX PAYMENT FORM” AT THE ADDRESS DESIGNATED THEREIN.

ALL PAYMENTS MUST BE MAILED TO OR DEPOSITED WITH THE STATE TREASURER IN ORDER TO BE CREDITED WITH TIMELY PAYMENT.

Printed by authority of the State of Illinois. (Revised: 07/22)

STATE OF ILLINOIS ESTATE & GENERATION SKIPPING TRANSFER TAX RETURN - PAGE 5

| Fact Name | Details |

|---|---|

| Purpose | The Illinois Form 700 is used to report estate and generation-skipping transfer taxes for decedents who died on or after January 1, 2021. |

| Filing Requirement | If the gross value of the estate exceeds $4 million, this form must be filed, regardless of federal filing requirements. |

| Governing Law | The form is governed by the Illinois Estate and Generation-Skipping Transfer Tax Act (35 ILCS 200/2-1 et seq.). |

| Types of Returns | There are three types of returns: Original, Supplemental (if additional tax is due), and Amended (if no additional tax is due). |

| Due Date | The return must be filed within nine months of the decedent's date of death. |

| QTIP Election | Estates may elect Illinois QTIP treatment, which allows certain property to qualify for marital deductions. |

| Filing Locations | For Cook, DuPage, Lake, and McHenry Counties, the return is filed in Chicago. For all other counties, it is filed in Springfield. |

| Penalties | Late filing incurs a penalty of 5% of the tax due for each month, up to a maximum of 25%. |

| Interest Rates | Interest on unpaid taxes accrues at a rate of 10% per annum from nine months after death until payment is made. |

| Payment Instructions | All taxes, interest, and penalties must be paid to the Illinois State Treasurer using the designated payment form. |

Filling out the Illinois 700 form is a crucial step in managing the estate of a decedent. This form must be completed accurately and submitted within the required timeframe. The following steps will guide you through the process of filling out the form effectively.

What is the purpose of the Illinois 700 form?

The Illinois 700 form is used to report the estate and generation-skipping transfer tax for individuals who have died on or after January 1, 2021. This form is necessary when the gross value of a decedent's estate exceeds $4 million, even if a federal estate tax return is not required. It helps the state assess any estate taxes due based on the value of the estate and the applicable laws.

Who is required to file the Illinois 700 form?

Any personal representative or executor of an estate must file the Illinois 700 form if the decedent's gross estate value exceeds $4 million. This requirement holds true regardless of whether a federal estate tax return is necessary. The form must be submitted within nine months of the decedent's death to avoid penalties. If the estate does not exceed this threshold, the form may not be required, but it can still be filed for other reasons, such as requesting a Certificate of Discharge.

What information is needed to complete the Illinois 700 form?

To complete the Illinois 700 form, you will need detailed information about the decedent's estate. This includes the decedent's name, address, Social Security number, and the date of death. You must also provide the total gross value of the decedent's assets, both in Illinois and elsewhere. If applicable, you will need to indicate whether a federal estate tax return is attached and whether any elections, such as the Illinois QTIP election, are being made. Additionally, information about the personal representative and preparer is required.

What happens if the Illinois 700 form is not filed on time?

If the Illinois 700 form is not filed within the nine-month period following the decedent's death, the estate may incur penalties. These include a late filing penalty of 5% of the tax due for each month the return is late, up to a maximum of 25%. There may also be late payment penalties and interest charges. To avoid these consequences, it is crucial to file the form on time and ensure that all taxes owed are paid promptly.

Incomplete Information: Failing to provide complete details can lead to delays. Ensure all sections are filled out accurately, including the decedent's address and Social Security number.

Incorrect Filing Type: Selecting the wrong return type—original, supplemental, or amended—can complicate the process. Review your circumstances carefully before making a selection.

Missing Attachments: Not including required documents, such as the Federal Estate Tax Return or itemized schedules, may result in rejection of the form. Double-check that all necessary attachments are included.

Errors in Financial Calculations: Miscalculating the gross value of the decedent’s assets can lead to incorrect tax assessments. Use the calculator provided on the Illinois Attorney General's website to ensure accuracy.

Ignoring Deadlines: Submitting the form after the nine-month deadline can incur penalties and interest. Mark your calendar to ensure timely filing.

Failure to Sign: Not signing the return can result in it being considered invalid. Ensure that both the personal representative and the preparer sign the form before submission.

The Illinois Form 700 is an essential document for reporting estate and generation-skipping transfer taxes for decedents who pass away on or after January 1, 2021. When filing this form, there are several other documents and forms that may be required or helpful to include in the process. Below is a list of commonly used forms and documents that accompany the Illinois Form 700.

Each of these documents plays a significant role in ensuring that the estate tax process is handled accurately and efficiently. Properly preparing and submitting these forms alongside the Illinois Form 700 can help avoid delays and complications in settling the estate.

When filling out the Illinois 700 form, it is crucial to approach the task with care and attention to detail. Here are six important do's and don'ts to consider:

This form is required for any estate with a gross value exceeding $4 million, regardless of whether it is considered large by other standards. If the estate surpasses this threshold, the form must be filed, even if no federal return is necessary.

Filing the form does not automatically mean that no tax is due. The estate must still be evaluated based on its total value and applicable deductions. If the taxable estate exceeds the exemption limit, taxes will be owed.

While the personal representative typically files the form, anyone with the necessary information can assist in its preparation. It is important that the filing is accurate and complete to avoid penalties.

The form must be filed within nine months of the date of death. This allows some time for the personal representative to gather the required information and complete the form accurately.

The Illinois Form 700 is required for estates of decedents who died on or after January 1, 2021, if the gross value exceeds $4 million.

Choose the correct type of return: Original, Supplemental, or Amended. Each type serves a different purpose.

Provide accurate information about the decedent, including their address and Social Security number. This information is crucial for processing.

Indicate which of the seven options apply to your situation. This will determine the tax obligations.

Attach a detailed schedule of assets. This should include all assets, regardless of their location.

If applicable, include a Federal Estate Tax Return. This is necessary if an Illinois Estate Tax is due.

File the return within nine months of the decedent's date of death to avoid penalties.

Payments for taxes, interest, and penalties must be made to the Illinois State Treasurer. Ensure that all payments are mailed or deposited correctly to be credited timely.