When it comes to borrowing or lending money in Hawaii, a Promissory Note serves as a crucial document that outlines the terms of the loan agreement between the parties involved. This legal form details essential information, such as the amount borrowed, the interest rate, and the repayment schedule, ensuring that both the lender and borrower are on the same page. The Promissory Note also specifies any collateral that may secure the loan, offering additional protection for the lender. In Hawaii, this document must comply with state laws, which can include specific requirements regarding signatures and notarization. By clearly stating the obligations of both parties, the Promissory Note helps to prevent misunderstandings and disputes down the line, making it an indispensable tool in personal and business finance. Understanding how to properly complete and utilize this form can empower individuals and businesses alike to engage in financial transactions with confidence and clarity.

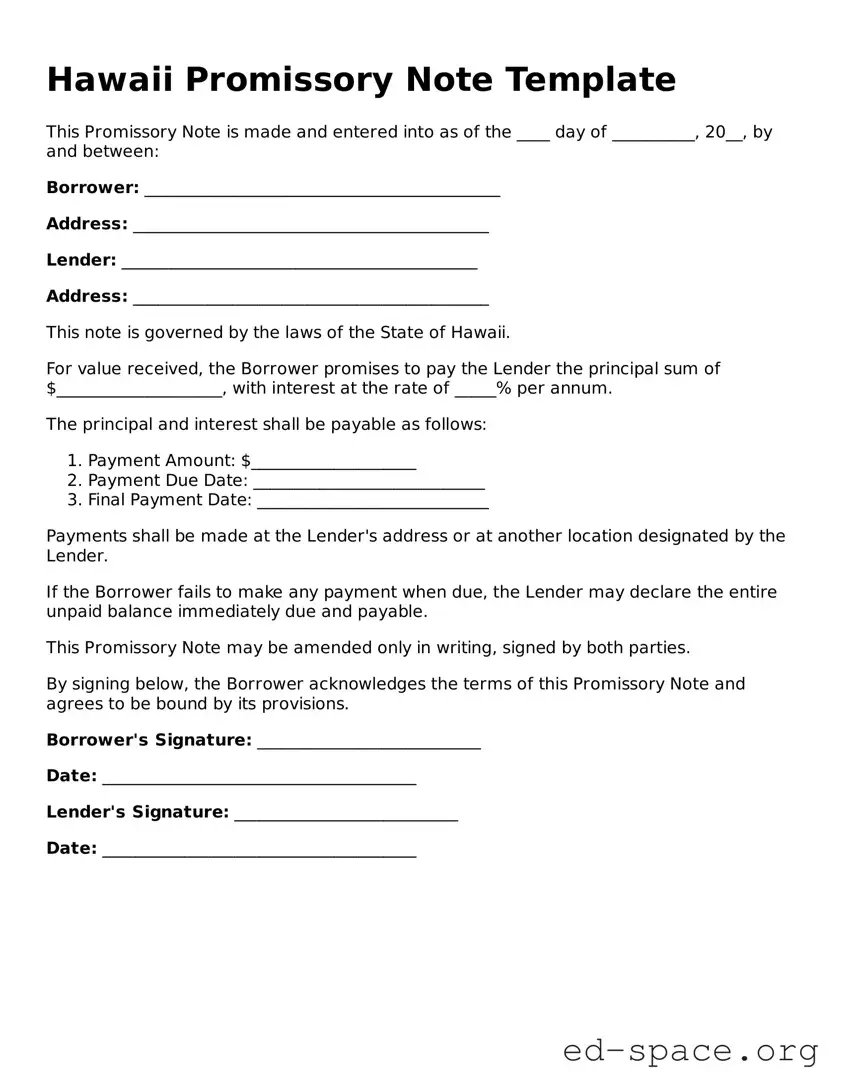

Hawaii Promissory Note Template

This Promissory Note is made and entered into as of the ____ day of __________, 20__, by and between:

Borrower: ___________________________________________

Address: ___________________________________________

Lender: ___________________________________________

Address: ___________________________________________

This note is governed by the laws of the State of Hawaii.

For value received, the Borrower promises to pay the Lender the principal sum of $____________________, with interest at the rate of _____% per annum.

The principal and interest shall be payable as follows:

Payments shall be made at the Lender's address or at another location designated by the Lender.

If the Borrower fails to make any payment when due, the Lender may declare the entire unpaid balance immediately due and payable.

This Promissory Note may be amended only in writing, signed by both parties.

By signing below, the Borrower acknowledges the terms of this Promissory Note and agrees to be bound by its provisions.

Borrower's Signature: ___________________________

Date: ______________________________________

Lender's Signature: ___________________________

Date: ______________________________________

| Fact Name | Description |

|---|---|

| Definition | A Hawaii Promissory Note is a written promise to pay a specific amount of money to a designated party at a specified time or on demand. |

| Governing Law | The Hawaii Promissory Note is governed by Hawaii Revised Statutes, Chapter 478. |

| Interest Rates | The maximum interest rate allowed in Hawaii is 10% per annum unless otherwise agreed upon in writing. |

| Enforceability | To be enforceable, the note must be signed by the borrower and include essential terms such as the amount, interest rate, and payment schedule. |

Once you have gathered the necessary information, you can begin filling out the Hawaii Promissory Note form. Completing this form accurately is essential for establishing a clear understanding between the parties involved. Follow these steps carefully to ensure that all required information is provided.

After completing the form, review it carefully for any errors or omissions. It is advisable to keep a copy for your records and provide a copy to the other party involved in the agreement. This will help ensure that both parties have a clear understanding of the terms and obligations outlined in the Promissory Note.

What is a Hawaii Promissory Note?

A Hawaii Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It includes important details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. This document serves as evidence of the debt and can be used in court if necessary.

Who can use a Promissory Note in Hawaii?

Anyone can use a Promissory Note in Hawaii, including individuals, businesses, and organizations. It is commonly used for personal loans, business loans, and real estate transactions. Both the lender and borrower should be clear about the terms before signing the document to avoid misunderstandings.

What are the key components of a Hawaii Promissory Note?

A well-drafted Promissory Note should include the names and addresses of the borrower and lender, the principal amount, interest rate, payment schedule, and maturity date. It may also outline any collateral securing the loan, late fees, and the governing law. Clarity in these components helps protect both parties.

Do I need a lawyer to create a Promissory Note in Hawaii?

While it is not legally required to have a lawyer draft a Promissory Note, consulting one can be beneficial. A lawyer can ensure that the document meets all legal requirements and accurately reflects the intentions of both parties. This can help prevent potential disputes in the future.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has several options. They may choose to pursue repayment through negotiation or mediation. If that fails, the lender can file a lawsuit to recover the owed amount. Having a well-drafted Promissory Note strengthens the lender's position in court.

Incomplete Information: Many individuals fail to provide all necessary details. This includes missing names, addresses, or dates. Omitting such information can lead to confusion or disputes later on.

Incorrect Amounts: Errors in the principal amount or interest rate are common. Double-checking these figures is crucial, as inaccuracies can affect the terms of repayment.

Not Signing the Document: A frequent oversight is neglecting to sign the form. Without a signature, the note may not be legally enforceable, rendering it ineffective.

Failure to Specify Terms: Some individuals do not clearly outline the repayment schedule or consequences of default. Clarity in these areas is essential to avoid misunderstandings in the future.

When dealing with a Hawaii Promissory Note, there are several other forms and documents that may be necessary. These documents help clarify terms, protect interests, and ensure all parties understand their obligations. Below is a list of commonly used forms that accompany a Promissory Note.

Having these documents ready can streamline the lending process and protect all parties involved. Understanding each form’s purpose will help ensure a smoother transaction and clearer communication between the lender and borrower.

When filling out the Hawaii Promissory Note form, it is essential to follow certain guidelines to ensure accuracy and compliance. Below is a list of dos and don’ts that can help streamline the process.

By adhering to these guidelines, individuals can avoid common pitfalls and ensure that the Hawaii Promissory Note form is completed accurately and effectively.

When dealing with a Hawaii Promissory Note, several misconceptions can cloud understanding and lead to confusion. Here are eight common misunderstandings about this important financial document.

Understanding these misconceptions can help individuals navigate the complexities of promissory notes in Hawaii more effectively. Being informed empowers borrowers and lenders alike to make sound financial decisions.

When filling out and using the Hawaii Promissory Note form, there are several important aspects to consider. Below are key takeaways to help guide you through the process:

By paying attention to these key points, individuals can ensure that the promissory note serves its intended purpose effectively.