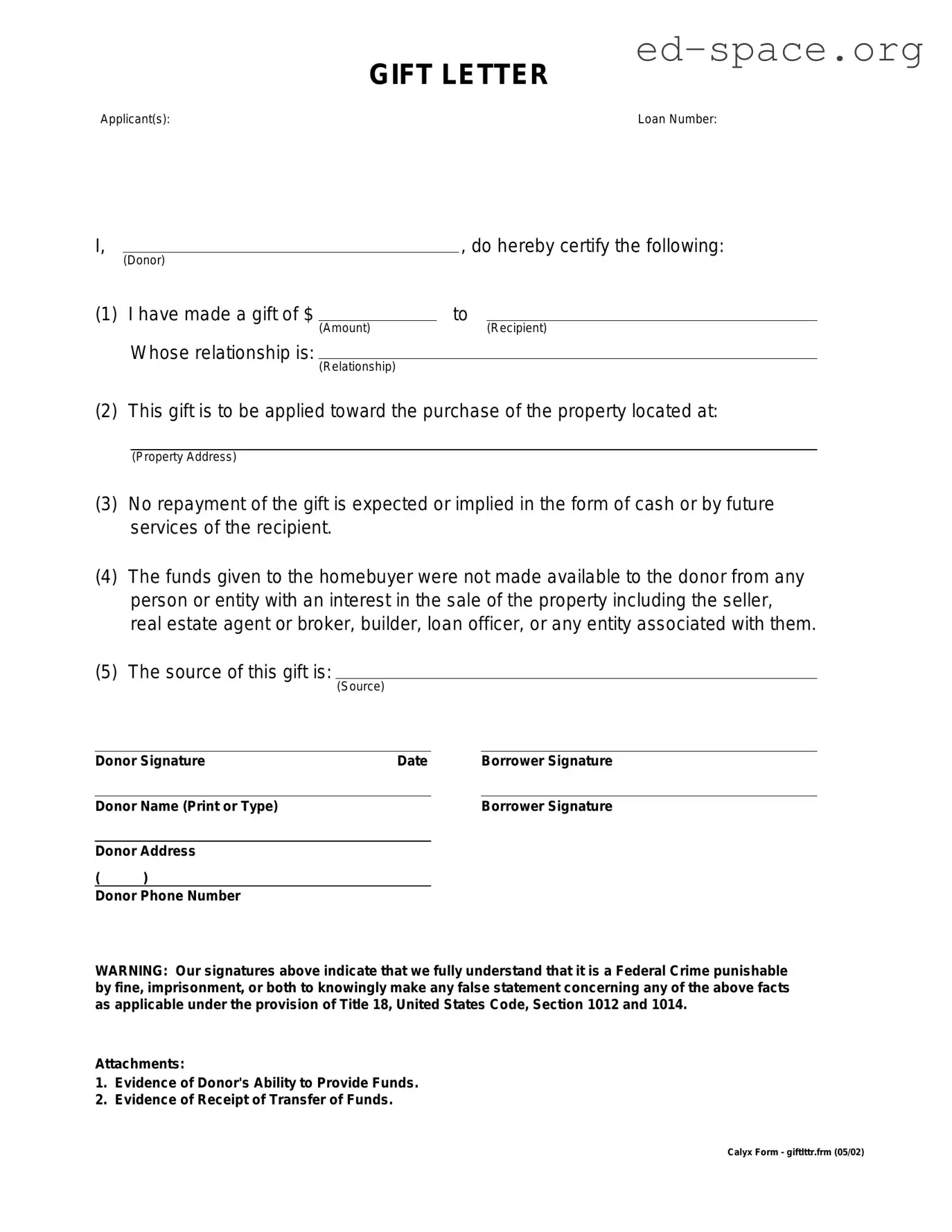

When individuals receive financial gifts to assist with significant purchases, such as real estate or a vehicle, a critical document comes into play: the Gift Letter form. This form is an essential tool that formally records the nature of the gift, ensuring that it is indeed a gift and not a loan that needs to be repaid. Through the Gift Letter, the gifter declares that the funds provided do not require repayment, clarifying the terms for both the recipient and any interested third parties, such as mortgage lenders or financial institutions. This distinction is vital for lenders to accurately assess the recipient's financial obligations when making approval decisions. The form typically includes important details like the donor's name and relationship to the recipient, the exact amount of the gift, as well as explicit statements about there being no expectation of repayment. By securely establishing the parameters of the financial gift, the form plays a pivotal role in smoothing the path towards major purchases, safeguarding the interests of all parties involved.

| Fact Name | Detail |

|---|---|

| Purpose | Confirms that a sum of money given is a gift, not a loan. |

| Contents | Typically includes the donor's name, recipient's name, relationship, gift amount, and a statement that no repayment is expected. |

| Use in Mortgage Applications | Often required by lenders to verify that down payment funds are gifts. |

| Tax Implications | May be referenced by the IRS to determine if gift tax applies. |

| State-Specific Variations | Some states may have specific requirements or forms. |

| Governing Law | Federal law and state laws, depending on tax implications and state requirements. |

| Signatory Requirements | Generally requires signatures from the donor and, in some cases, the recipient and/or witness. |

| Notarization | Not always required but recommended for added legal validity. |

| Common Misconceptions | Some people mistakenly believe a gift letter alone exempts them from any tax obligations. |

When preparing to complete a Gift Letter form, it's essential to understand that this document acts as an official way to show that a significant amount of money given to someone, often for the purchase of a home, is truly a gift and not a loan. This distinction is crucial because it affects the recipient's ability to qualify for a mortgage since loans need to be paid back, potentially impacting borrowing capabilities. By completing this form correctly and thoroughly, both the giver and the recipient can ensure that the financial transaction is transparent and meets legal and financial requirements.

After filling out the Gift Letter form, it should be submitted alongside the mortgage application of the recipient, or as requested by the financial institution or legal advisor. Ensuring the form is accurately completed and submitted promptly helps facilitate a smoother transaction and supports the recipient's financial journey, such as purchasing a home. Remember, it’s always recommended to keep a copy of the completed form for personal records and potential future reference.

What is a Gift Letter and why do I need one?

A Gift Letter is a document that clearly states money received from a friend or family member is a gift, meaning it does not need to be repaid. This letter is often required by lenders to confirm that the funds being used for a down payment on a home, or for any other major purchase, are not an additional loan that could impact the recipient's ability to honor their borrowing agreements.

Who needs to sign the Gift Letter?

The person giving the gift must sign the Gift Letter. This signature is a critical part of the document as it validates the gift's authenticity. Some lenders or legal entities may also require the recipient of the gift to sign the letter, acknowledging the gift and its terms.

Is there specific information that needs to be included in the Gift Letter?

Yes, certain details are essential for the Gift Letter to be considered valid. These include the donor's name and relationship to the recipient, the exact amount of the gift, the date the gift was or will be given, a statement that no repayment is expected or required, and the signatures of all parties involved. Some lenders may also require the letter to include the donor’s contact information and the recipient’s account details where the funds will be deposited.

Can a Gift Letter be handwritten or must it be typed?

While a handwritten Gift Letter may still be accepted by some lenders, a typed letter is generally preferred for clarity and legibility. The most important aspect is that the letter contains all of the required information and signatures. Always check with the lender or legal advisor to confirm their specific requirements.

Does a Gift Letter need to be notarized?

Not all gift letters need to be notarized. However, getting the letter notarized adds an extra layer of authenticity, as it confirms the identity of the signatories. Some lenders or legal situations may require a notarized letter, so it’s best to verify their requirements before proceeding.

Can a Gift Letter affect my taxes?

While the gift letter itself does not directly affect taxes, there are tax implications for large gifts. In the United States, there is an annual exclusion limit for gifts, beyond which the donor must file a gift tax return. The gift letter can serve as evidence that the transfer of funds was a gift if audited by tax authorities. The recipient typically does not have to pay income tax on the gift received.

How long is a Gift Letter valid?

A Gift Letter does not expire, but its relevance is generally limited to the specific transaction it was drafted for. Lenders will usually require the Gift Letter to be dated close to the transaction date to ensure the information is current and reflective of the funds being used for that specific purpose.

Are there legal consequences if it's found out the gift is actually a loan?

If it is discovered that the money was in fact a loan and not a gift, this could constitute fraud, especially if the misrepresented funds influenced a lender's decision to approve a loan or mortgage. This could lead to legal repercussions for both the giver and the receiver, including potential criminal charges for fraud or legal action by the lender to recover the loan based on actual financial standings.

Not providing the date of the gift. People often forget to mention the exact date when the gift was made. This is critical as it helps establish the timeline of the transaction.

Omitting the relationship between the giver and the recipient. A key component of the Gift Letter form is specifying the relationship (e.g., parent, friend) to underline that there’s no expectation of repayment.

Failing to state the exact amount of the gift. It's crucial to specify the amount in clear terms to avoid any ambiguity regarding the size of the gift.

Neglecting to declare that the gift is not a loan. The letter must clearly state that the money given is a gift without any obligation of repayment. Without this, there might be misunderstandings or legal complications regarding the nature of the funds.

Forgetting to include the recipient's full legal name. Sometimes, people casually write down nicknames or abbreviations. It’s important to use the recipient's full legal name for clarity and official purposes.

Not having the giver's signature on the form. A signature is required to authenticate the document, confirming that the giver indeed acknowledges the content of the Gift Letter.

Leaving out the giver’s address and contact information. It's essential to include the giver’s current address and contact details. This information might be required for any follow-up or verification process by the institution or party receiving the Gift Letter.

When people prepare a Gift Letter, they often make mistakes that can easily be avoided. Such errors can lead to delays or issues in the processing of the document. Paying attention to the details in the Gift Letter is important to ensure its acceptability by financial institutions or any other entities that require such documentation.

When preparing for major financial transactions, particularly those involving real estate, a Gift Letter form is often utilized to document that funds given from one party to another are indeed a gift and not a loan. This assurance can be crucial for lenders when determining a borrower's eligibility for financing. However, the Gift Letter form does not stand alone in the documentation process. Several other forms and documents usually accompany it to provide a comprehensive picture of financial standing and legitimacy.

In summary, while the Gift Letter form is a key document in transactions involving significant financial gifts, it is part of a network of documents that ensure transparency, legality, and the financial stability of the parties involved. Each document plays a vital role in ensuring that all aspects of the transaction are legitimate, clear, and fair to all parties involved.

A Promissory Note serves a similar purpose in that it details an agreement between two parties regarding the lending and repayment of money. Unlike the Gift Letter, which confirms that funds are given without expectation of repayment, a Promissory Note lays out the terms under which a loan must be repaid, including interest rates and repayment schedule.

The Affidavit of Support is often used in immigration processes to prove that a visa applicant has financial support in the United States, minimizing the risk that the applicant will rely on public benefits. Like the Gift Letter, this document attests to the provision of financial support, but it is legally enforceable and requires the sponsor to support the immigrant financially if necessary.

A Loan Agreement is a comprehensive document that outlines the terms and conditions of a loan between two parties. It includes information similar to that of a Promissory Note but is more detailed, often covering legal remedies and obligations in the event of default. The key difference from the Gift Letter is that it formalizes a loan, not a gift.

The Mortgage Down Payment Gift Letter is a specific type of Gift Letter that is directly related, used when an individual gifts money to a homebuyer to cover part of the down payment. It confirms the money is a gift and not a loan, ensuring lenders that the recipient is not under additional financial obligations.

An Earnest Money Deposit Receipt is used in real estate transactions to demonstrate the buyer's commitment to the purchase. It signifies that an initial deposit has been made towards the buying price. Although it serves a different purpose, it is similar to a Gift Letter in providing proof of financial transactions related to property purchases.

The Donation Receipt is given to donors by nonprofit organizations to acknowledge receipt of a gift. Like the Gift Letter, it can serve as documentation for financial transactions without expectations of repayment. However, it also serves as proof for the donor's tax-deductible contributions.

A Financial Support Letter is often required by educational institutions or consular officers to prove a student has sufficient funds for tuition and living expenses while studying abroad. It is similar to a Gift Letter as it documents the provision of financial support, but it emphasizes the sponsor’s commitment to covering specific expenses over time.

The Declaration of No Interest is a document that states one party holds no financial interest in the assets or transactions of another party. While it often pertains to business dealings and investments, it shares the core principle of a Gift Letter by declaring that funds are transferred without expectations of repayment or profit sharing.

When completing a Gift Letter form, it is essential to adhere to certain guidelines to ensure the process is conducted smoothly and effectively. A Gift Letter is a document that proves money received by someone is indeed a gift and not a loan that is expected to be repaid. Below are nine critical do's and don'ts to consider:

When navigating the waters of buying a home, financial gifts from family or friends can be a lifeline for many individuals. However, when it comes to formalizing these gifts through a Gift Letter form, there are several misconceptions that can confuse both donors and recipients. Understanding these misconceptions can help ensure that this generous support doesn't become a stumbling block in the home-buying process.

When it comes to using a Gift Letter form, it's important to understand its purpose and how to properly fill it out to ensure a smooth financial transaction. Below are four key takeaways to consider:

A Gift Letter form is a document that clearly states money given by a donor (such as a family member) to a recipient (usually the buyer in a real estate transaction) is indeed a gift and not a loan. This distinction is crucial because it means the recipient is not obligated to pay back the money.

The form should include specific details like the exact amount of the gift, the date the gift is made, and the relationship between the donor and the recipient. Including this information helps financial institutions verify the legitimacy of the gift, which is especially important when the recipient is using the gift towards a large purchase, like a home.

Both the donor and the recipient are required to sign the Gift Letter form. This formal acknowledgment by both parties is necessary for the document to be considered valid and binding. It's a straightforward step, but it's vital for the form's acceptance by lenders or banks.

Lastly, it is important to be honest and transparent when filling out the Gift Letter form. Attempting to disguise a loan as a gift can lead to potential legal and financial complications down the line. Lenders have processes in place to verify the information provided, so accuracy and honesty are paramount.

Ultimately, the Gift Letter form is a simple but powerful tool in confirming that a financial gift has been given. It plays a critical role in transaction processes, particularly in the home buying journey. By understanding and correctly using this document, donors and recipients can facilitate a transparent and efficient financial exchange.

Fed Benefits Dental - Ensure all sections of the form are filled out completely.

Oglala Sioux Tribe Enrollment - Parental history must include details for both the natural father and mother.

Ny Courts Eviction Forms - You cannot file a nonpayment case if the tenant has moved out permanently.