When it comes to borrowing money in Georgia, a Promissory Note serves as a crucial document that outlines the terms of the loan agreement between a borrower and a lender. This legally binding form specifies the amount borrowed, the interest rate, and the repayment schedule, ensuring that both parties are clear on their obligations. It also includes important details such as the maturity date, which is when the loan must be fully repaid, and any penalties for late payments. Additionally, the Promissory Note may outline the rights of the lender in case of default, providing a safety net for the lender while offering transparency to the borrower. Understanding the nuances of this form is essential for anyone involved in a lending transaction in Georgia, as it not only protects the interests of both parties but also helps to foster trust and clarity in financial dealings.

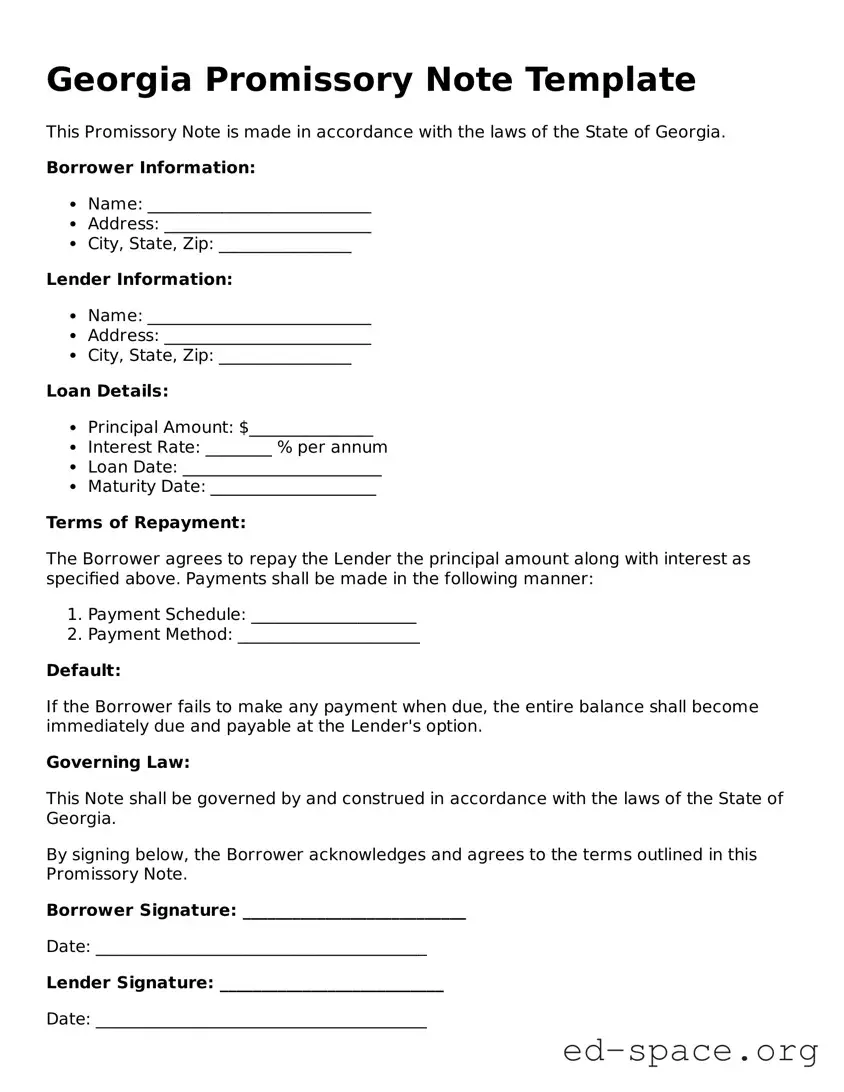

Georgia Promissory Note Template

This Promissory Note is made in accordance with the laws of the State of Georgia.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Lender the principal amount along with interest as specified above. Payments shall be made in the following manner:

Default:

If the Borrower fails to make any payment when due, the entire balance shall become immediately due and payable at the Lender's option.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Georgia.

By signing below, the Borrower acknowledges and agrees to the terms outlined in this Promissory Note.

Borrower Signature: ___________________________

Date: ________________________________________

Lender Signature: ___________________________

Date: ________________________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a future date. |

| Governing Law | The Georgia Promissory Note is governed by the Uniform Commercial Code (UCC) as adopted in Georgia. |

| Parties Involved | The document typically involves two parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The note may specify an interest rate, which can be fixed or variable, impacting the total repayment amount. |

| Payment Terms | Payment terms can include the due date, installment amounts, and any grace periods allowed for late payments. |

| Default Conditions | It outlines what constitutes a default, such as missed payments or bankruptcy, and the consequences of defaulting. |

| Secured vs. Unsecured | Promissory notes can be secured by collateral or unsecured, affecting the lender's recourse in case of default. |

| Transferability | Promissory notes in Georgia can often be transferred or assigned to another party, subject to certain conditions. |

| Signatures Required | For the note to be valid, it must be signed by the borrower, and often requires the lender's signature as well. |

| Legal Enforceability | A properly executed promissory note is legally enforceable in Georgia courts, providing recourse for the lender. |

After obtaining the Georgia Promissory Note form, you will need to provide specific information to complete it. This document outlines the terms of a loan agreement between a borrower and a lender. Once filled out, the form should be signed by both parties to make it legally binding.

What is a Georgia Promissory Note?

A Georgia Promissory Note is a legal document in which one party, the borrower, agrees to repay a specific amount of money to another party, the lender, under agreed-upon terms. This note outlines the principal amount, interest rate, repayment schedule, and any applicable fees. It serves as a formal acknowledgment of the debt and provides a clear framework for repayment, protecting both parties involved in the transaction.

What information is typically included in a Georgia Promissory Note?

Typically, a Georgia Promissory Note includes essential details such as the names and addresses of both the borrower and lender, the loan amount, the interest rate, and the repayment schedule. It may also specify the due date for payments, any late fees, and conditions for default. Additionally, the document often includes provisions regarding prepayment and any collateral securing the loan. These elements ensure clarity and prevent misunderstandings between the parties.

Is a Georgia Promissory Note legally binding?

Yes, a Georgia Promissory Note is a legally binding document, provided it meets certain requirements. For the note to be enforceable, it must be in writing, signed by the borrower, and include clear terms regarding the amount owed and repayment conditions. If these criteria are met, the lender can take legal action to recover the debt if the borrower defaults on the agreement. This binding nature underscores the importance of understanding the terms before signing.

Can a Georgia Promissory Note be modified after it is signed?

Yes, a Georgia Promissory Note can be modified after it is signed, but both parties must agree to the changes. Modifications should be documented in writing and signed by both the borrower and lender to ensure clarity and enforceability. This process may include changes to the repayment terms, interest rate, or any other conditions outlined in the original note. Clear communication and mutual consent are essential to avoid disputes in the future.

Incorrect Names: People often misspell their names or the names of the co-signers. Ensure that all names are accurate and match official identification.

Missing Dates: Failing to include the date when the note is signed can lead to confusion. Always write the date clearly.

Improper Amount: Some individuals write the loan amount incorrectly. Double-check the figures and ensure they match both in numbers and words.

Omitting Payment Terms: Not specifying how and when payments will be made is a common oversight. Clearly outline the payment schedule and method.

Neglecting Signatures: Some forget to sign the document. All parties involved must sign the note for it to be valid.

Ignoring State Laws: Each state has specific requirements for promissory notes. Failing to comply with Georgia’s regulations can invalidate the document.

When dealing with a Georgia Promissory Note, several other documents may be necessary to ensure clarity and legal protection for both parties involved. Here is a list of common forms and documents that often accompany a Promissory Note.

Understanding these documents can help both borrowers and lenders navigate the loan process more effectively. It is crucial to ensure that all necessary paperwork is completed accurately to avoid potential disputes in the future.

When filling out the Georgia Promissory Note form, it is important to follow certain guidelines to ensure accuracy and legality. Here are six things to keep in mind:

Understanding the Georgia Promissory Note form is essential for anyone entering into a loan agreement. However, several misconceptions can lead to confusion. Here are five common misconceptions and clarifications for each:

While notarization can add an extra layer of security, it is not a legal requirement for a promissory note in Georgia. A signed note can be enforceable without a notary's seal.

Many people believe that promissory notes are only necessary for significant amounts of money. In reality, they can be used for any loan amount, regardless of size.

There is no mandated format for a promissory note in Georgia. The essential elements include the amount, terms of repayment, and signatures of the parties involved. Flexibility exists in how these elements are presented.

Some believe that a signed promissory note is set in stone. In fact, the terms can be modified if both parties agree to the changes and document them properly.

While a promissory note is a type of contract, it is specifically focused on the promise to pay a debt. Other contracts may cover a broader range of agreements and obligations.

Being aware of these misconceptions can help you navigate the process of creating or signing a Georgia Promissory Note with greater confidence.

When dealing with the Georgia Promissory Note form, it is essential to understand its structure and requirements. Here are some key takeaways to keep in mind: