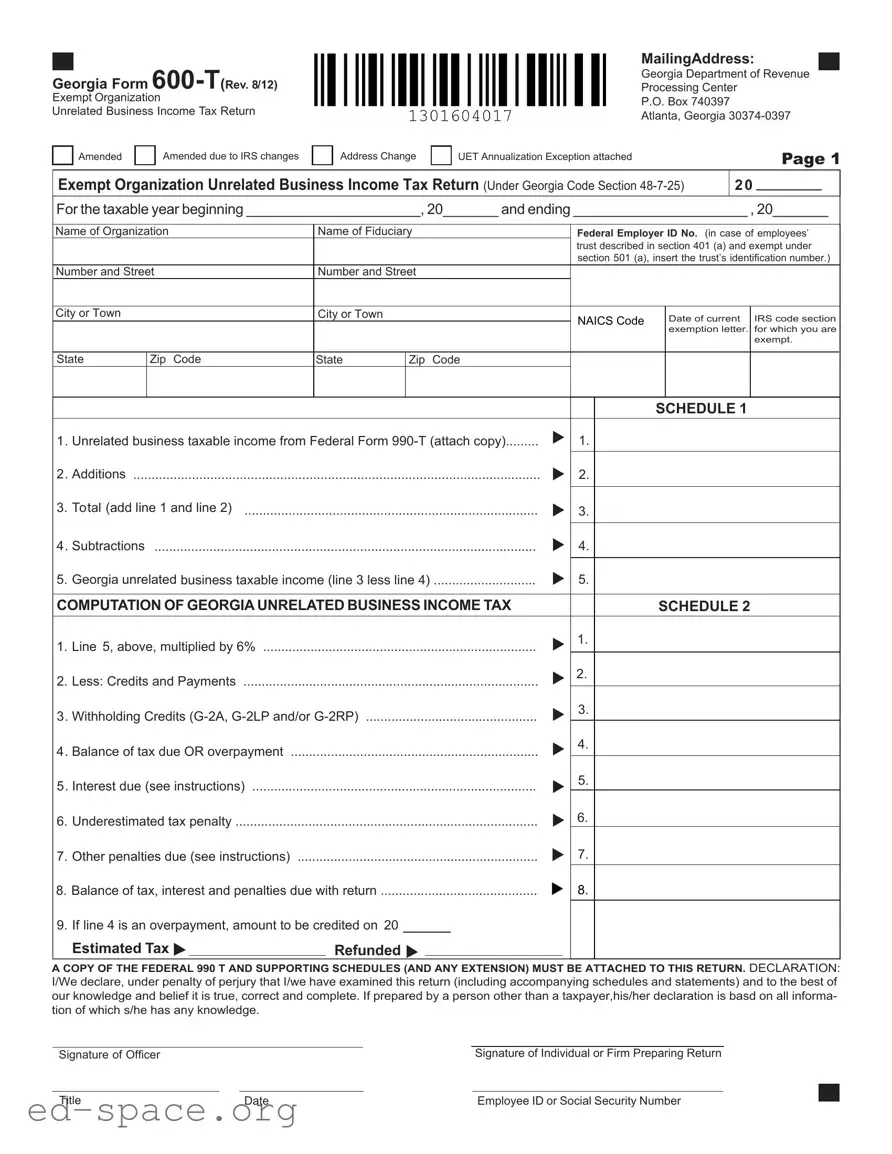

The Georgia Form 600-T serves as the Exempt Organization Unrelated Business Income Tax Return, specifically designed for organizations that generate unrelated business income from Georgia sources. This form is essential for any exempt organization required to file a federal Form 990-T. It captures vital information, including the organization’s name, address, and federal employer identification number. The form also requires the organization to report its unrelated business taxable income, detailing any additions and subtractions to arrive at the Georgia unrelated business taxable income. Tax rates for this income are set at 6%, and the form includes sections for calculating the total tax due, along with any applicable credits, penalties, and interest. Organizations must file the 600-T by the same deadline as the federal return, and it must be mailed to the Georgia Department of Revenue. Additionally, if an organization is granted an extension for its federal filing, it can attach a copy of that request to the Georgia return. Compliance with filing requirements, including attaching a copy of the federal Form 990-T, is crucial to avoid penalties and interest on unpaid taxes.

Georgia Form

Exempt Organization

Unrelated Business Income Tax Return

Amended |

|

Amended due to IRS changes |

|

|

|

Address Change

MailingAddress:

Georgia Department of Revenue

Processing Center

P.O. Box 740397

Atlanta, Georgia

UET Annualization Exception attached |

PAGE 1 |

|

Exempt Organization Unrelated Business Income Tax Return (Under Georgia Code Section

20

For the taxable year beginning ______________________, 20_______ and ending ______________________ , 20_______

Name of Organization |

Name of Fiduciary |

|

Federal Employer ID No. (in case of employees’ |

||||

|

|

|

|

|

trust described in section 401 (a) and exempt under |

||

|

|

|

|

|

section 501 (a), insert the trust’s identification number.) |

||

Number and Street |

Number and Street |

|

|

|

|

||

|

|

|

|

|

|

|

|

City or Town |

|

City or Town |

|

|

NAICS Code |

Date of current |

IRS code section |

|

|

|

|

|

|||

|

|

|

|

|

|

exemption letter. |

for which you are |

|

|

|

|

|

|

|

exempt. |

|

|

|

|

|

|

|

|

State |

Zip Code |

State |

Zip |

Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE 1 |

|

1. Unrelated business taxable income from Federal Form |

1. |

||||||||

2. Additions |

|

|

|

|

|

|

|||

|

|

|

|

2. |

|||||

3. |

Total (add line 1 and line 2) |

|

|

|

|

|

|

||

|

|

|

|

3. |

|||||

4. Subtractions |

|

|

|

|

|

|

|||

|

|

|

|

4. |

|||||

5. |

Georgia unrelated business taxable income (line 3 less line 4) |

|

|||||||

5. |

|||||||||

|

|

|

|

|

|

|

|||

COMPUTATION OF GEORGIAUNRELATED BUSINESS INCOME TAX |

SCHEDULE 2 |

||||||||

1. |

Line 5, above, multiplied by 6% |

|

|

|

|

|

1. |

||

|

|

|

|

|

|||||

2. |

Less: Credits and Payments |

|

|

|

|

|

2. |

||

|

|

|

|

|

|||||

3. Withholding Credits |

3. |

||||||||

4. |

|||||||||

4. Balance of tax due OR overpayment |

|

|

|

|

|

||||

|

|

|

|

|

|||||

|

|

|

|

|

5. |

||||

5. Interest due (see instructions) |

|

|

|

|

|

||||

|

|

|

|

|

|||||

|

|

|

|

|

6. |

||||

6. |

Underestimated tax penalty |

|

|

|

|

|

|||

7. |

Other penalties due (see instructions) |

|

|

|

|

7. |

|||

8. Balance of tax, interest and penalties due with return |

8. |

||||||||

9. |

If line 4 is an overpayment, amount to be credited on 20 |

|

|

|

|||||

|

|||||||||

|

Estimated Tax |

|

Refunded |

|

|

|

|||

A COPY OF THE FEDERAL 990 T AND SUPPORTING SCHEDULES (AND ANY EXTENSION) MUST BE ATTACHED TO THIS RETURN. DECLARATION: I/We declare, under penalty of perjury that I/we have examined this return (including accompanying schedules and statements) and to the best of our knowledge and belief it is true, correct and complete. If prepared by a person other than a taxpayer,his/her declaration is basd on all informa- tion of which s/he has any knowledge.

Signature of Officer |

|

Signature of Individual or Firm Preparing Return |

Title |

Date |

Employee ID or Social Security Number |

PAGE 2

INSTRUCTIONS FOR FORM

FILING REQUIREMENTS

Everyexemptorganization,whichis requiredto filea Form

or business income from Georgia sources, must file a

Georgia Form

WHENAND WHERE TO FILE

The return is due on or before the due date of the Federal Form

EXTENSION OF TIME

A reasonableextensionof time for filing may be granted by the Commissioner upon application on Form

TAX RATE

As provided by Georgia Code Section

ACCOUNTING METHOD

Taxable income must be computed using the method of accountingregularlyusedinkeepingtheorganization’sbooks and records. In all cases, the method adopted must clearly reflect taxable income.

PERIOD TO BE COVERED

The taxable period for Georgia purposes shall be the same as for Federal purposes.

ALLOCATION AND APPORTIONMENT OF INCOMEAND EXPENSES

For those organizations having unrelated business income for Georgia and in other states, the income and expenses relatedtoitsproductionshouldbeallocatedandapportioned to clearly reflect the Georgia unrelated business taxable income. Sufficient information should be attached to the Form

PENALTIESAND INTEREST

Penalties provided by the Georgia Code are: For delin- quent filing- 5% of tax not paid by the original due date for each month or part of month of delinquency. For delinquent payment- 1/2 of 1% due for each month or part month of delinquency. An extension of time for filing does not alter delinquent payment penalty. Delin- quent payment is not due if the return is being amended due to an IRS audit. For negligent underpayment- 5% of amount of

Underpayment of estimated tax (UET) Penalty. Attach Form 600 UET and enter the amount on line 6. Also if a penalty exception applies check the “UET Annualization Exception attached” box.

NOTE:Thecombinedtotalofthepenaltyfordelinquentfiling and penalty for delinquent payment cannot exceed 25% of the tax not paid by the original due date.

FEDERAL FORM

“Georgia Public Revenue Code Section

| Fact Name | Description |

|---|---|

| Governing Law | The Georgia Form 600-T is governed by Georgia Code Section 48-7-25, which pertains to the taxation of unrelated business income for exempt organizations. |

| Filing Requirement | Every exempt organization with unrelated business income from Georgia sources must file this form if required to file a Federal Form 990-T. |

| Due Date | The return is due on or before the due date of the Federal Form 990-T, as specified under the Internal Revenue Code. |

| Tax Rate | Unrelated business income is taxed at a rate of 6%, as outlined in Georgia Code Section 48-7-25(c). |

| Penalties for Delinquency | Penalties for late filing include a 5% charge of the unpaid tax for each month of delinquency, with a maximum of 25% of the total tax due. |

Filling out the Georgia Form 600-T is essential for exempt organizations with unrelated business income from Georgia sources. This form must be completed accurately and submitted by the due date to avoid penalties. Below are the steps to help you fill out the form correctly.

After completing the form, review it for accuracy. Ensure all necessary attachments are included. Mail the form to the Georgia Department of Revenue Processing Center by the due date to avoid penalties.

What is the Georgia Form 600-T and who needs to file it?

The Georgia Form 600-T is an Exempt Organization Unrelated Business Income Tax Return. It is required for any exempt organization that has unrelated business income from Georgia sources and must file a Federal Form 990-T. If your organization earns income from activities that are not related to its exempt purpose, you will need to file this form to report that income to the state of Georgia.

When is the Form 600-T due?

The Form 600-T is due on or before the due date of the Federal Form 990-T. This means you should check the federal filing deadline and ensure your Georgia return is submitted by the same date. To file, send the completed form to the Georgia Department of Revenue Processing Center at P.O. Box 740397, Atlanta, GA 30374-0397.

What are the penalties for late filing or payment?

Penalties for late filing include a 5% charge on the tax not paid by the original due date for each month or part of a month that the return is late. If you fail to pay the tax on time, there is an additional penalty of 0.5% for each month or part month of delinquency. Keep in mind that these penalties can accumulate, and interest will accrue at a rate of 12% per year from the due date until the tax is paid.

What documents must be attached to the Form 600-T?

When filing the Form 600-T, you must attach a copy of the Federal Form 990-T along with any supporting schedules and extensions. This documentation is essential for the Georgia Department of Revenue to verify your reported income and ensure compliance with state tax laws.

Incorrect Tax Year Dates: Failing to accurately fill in the beginning and ending dates for the taxable year can lead to significant errors in tax calculations.

Missing Federal Form 990-T: Not attaching a copy of the Federal Form 990-T and its supporting schedules can result in rejection of the return.

Errors in Income Calculation: Miscalculating unrelated business taxable income from Federal Form 990-T may lead to incorrect tax amounts.

Improperly Reporting Additions and Subtractions: Failing to accurately report additions and subtractions can distort the final tax calculation.

Incorrect Mailing Address: Sending the form to the wrong address can delay processing and lead to penalties.

Signature Issues: Not signing the form or having the wrong person sign can invalidate the return.

Ignoring Penalties and Interest: Not considering potential penalties and interest for late filing or payment can lead to unexpected financial burdens.

Failure to Apply for Extensions: Not applying for an extension when needed can result in late filing penalties.

The Georgia Form 600-T is an essential document for exempt organizations reporting unrelated business income. Alongside this form, several other documents are commonly required to ensure compliance with state and federal regulations. Below is a list of these documents, each serving a specific purpose in the tax reporting process.

These documents collectively facilitate the accurate reporting and compliance of tax obligations for exempt organizations in Georgia. Properly preparing and submitting each form helps avoid potential penalties and ensures that the organization maintains its tax-exempt status.

The Georgia Form 600-T is an important document for exempt organizations that have unrelated business income. It shares similarities with several other tax-related forms. Below is a list of eight documents that are comparable to the Georgia Form 600-T, along with explanations of how they are similar.

When filling out the Georgia Form 600 T, there are important practices to keep in mind. Here’s a list of things you should and shouldn’t do:

Understanding the Georgia Form 600 T can be challenging, especially with the various misconceptions that surround it. Here are seven common misunderstandings about this tax form:

This is incorrect. Form 600 T is specifically for exempt organizations that have unrelated business income. Even if an organization is tax-exempt, it must file this form if it earns income from activities not related to its exempt purpose.

Organizations must file Form 600 T regardless of whether they owe taxes. The form is necessary to report unrelated business income, even if that income results in no tax liability.

This is a common error. The filing deadline for Form 600 T aligns with that of the federal Form 990-T. Organizations should ensure they submit both forms by the same due date.

Even tax-exempt organizations face penalties for late filing. The Georgia Department of Revenue imposes a penalty for delinquent filing, which can accumulate over time.

It is essential to report all unrelated business income. Ignoring this income can lead to serious consequences, including fines and penalties.

This is misleading. A copy of the federal Form 990-T and any supporting schedules must accompany Form 600 T when it is submitted. This ensures that all reported income is verified and accurate.

While extensions can be granted, they must be applied for using Form IT-303 before the original due date. Organizations cannot assume they will receive an extension without taking the necessary steps.

By addressing these misconceptions, organizations can better navigate the complexities of filing the Georgia Form 600 T and ensure compliance with state tax regulations.

Filling out the Georgia Form 600-T requires careful attention to detail. Here are key takeaways to ensure compliance and accuracy:

Understanding these points can help streamline the filing process and minimize potential penalties.