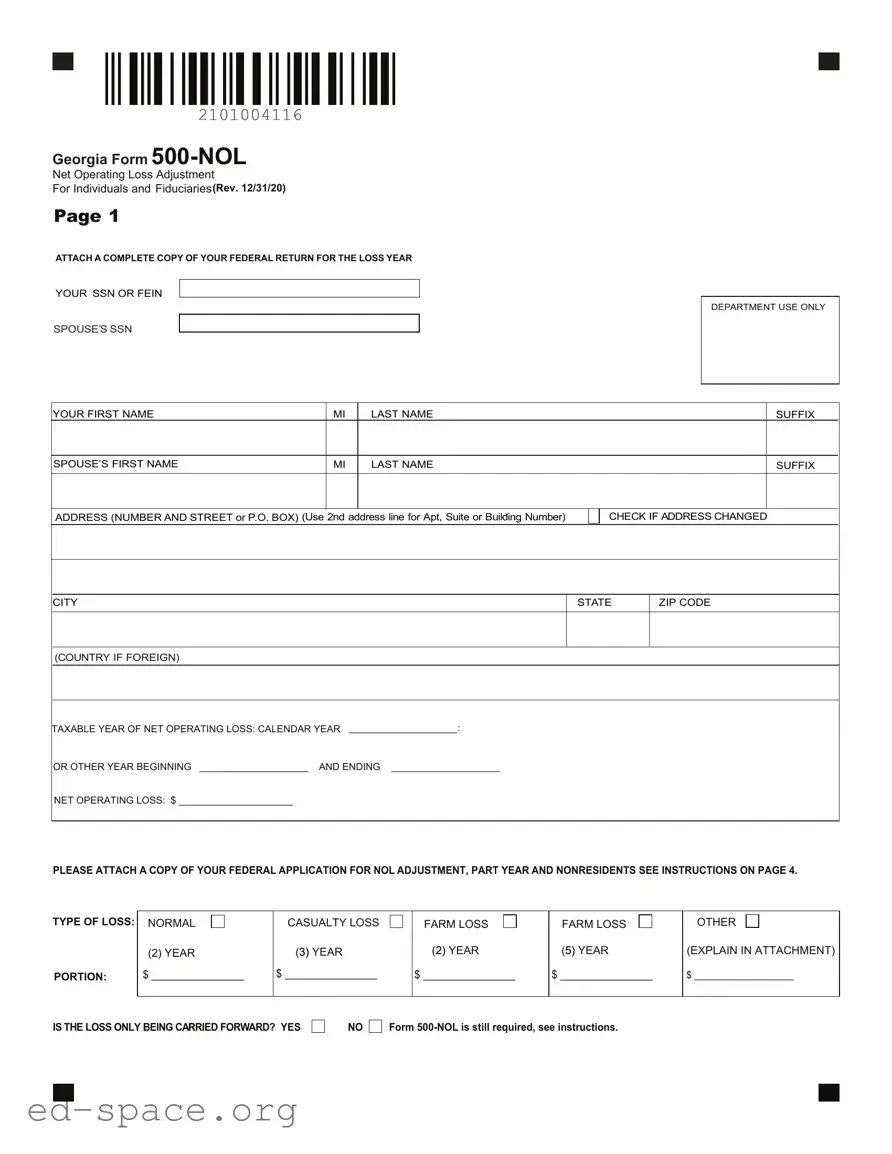

The Georgia Form 500-NOL is an essential document for individuals and fiduciaries who need to report a net operating loss (NOL) for tax purposes. This form allows taxpayers to adjust their income tax liability by carrying back or carrying forward losses incurred in previous tax years. It is crucial for those who have experienced financial setbacks, as it provides a means to offset taxable income and potentially receive tax refunds. The form requires detailed information, including the taxpayer's Social Security Number or Federal Employer Identification Number, the taxable year of the loss, and the specific amount of the net operating loss. Taxpayers must also indicate the type of loss—whether it is a normal loss, casualty loss, or farm loss—while ensuring that they attach a complete copy of their federal return for the loss year. Additionally, the form includes a section for calculating adjustments to federal adjusted gross income and determining Georgia adjusted gross income. Filing this form correctly is vital for establishing the NOL in the Department of Revenue's system, which can significantly impact future tax liabilities.

Georgia Form

Net Operating Loss Adjustment

For Individuals and Fiduciaries(Rev. 12/31/20)

PAGE 1

ATTACH A COMPLETE COPY OF YOUR FEDERAL RETURN FOR THE LOSS YEAR

YOUR SSN OR FEIN

SPOUSE’S SSN

DEPARTMENT USE ONLY

YOUR FIRST NAME |

|

MI |

|

LAST NAME |

|

|

|

|

SUFFIX |

|

|

|

|

|

|

|

|

|

|

SPOUSE’S FIRST NAME |

|

MI |

|

LAST NAME |

|

|

|

|

SUFFIX |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

ADDRESS (NUMBER AND STREET or P.O. BOX) (Use 2nd address line for Apt, Suite or Building Number) |

|

|

CHECK IF ADDRESS CHANGED |

||||||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

CITY |

|

|

|

|

STATE |

ZIP CODE |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(COUNTRY IF FOREIGN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAXABLE YEAR OF NET OPERATING LOSS: CALENDAR YEAR |

____________________: |

|

|

|

|

|

|||

OR OTHER YEAR BEGINNING ____________________ |

AND ENDING ____________________ |

|

|

|

|

|

|||

NET OPERATING LOSS: $ _____________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PLEASE ATTACH A COPY OF YOUR FEDERAL APPLICATION FOR NOL ADJUSTMENT, PART YEAR AND NONRESIDENTS SEE INSTRUCTIONS ON PAGE 4.

TYPE OF LOSS: |

NORMAL |

CASUALTY LOSS |

FARM LOSS |

FARM LOSS |

OTHER |

|

(2) YEAR |

(3)) YEAR |

(2)) YEAR |

(5)) YEAR |

(EXPLAIN IN ATTACHMENT) |

PORTION: |

$ ________________ |

$ ________________ |

$ ________________ |

$ ________________ |

$ ___________________ |

|

|

|

|

|

|

IS THE LOSS ONLY BEING CARRIED FORWARD? YES

NO |

Form |

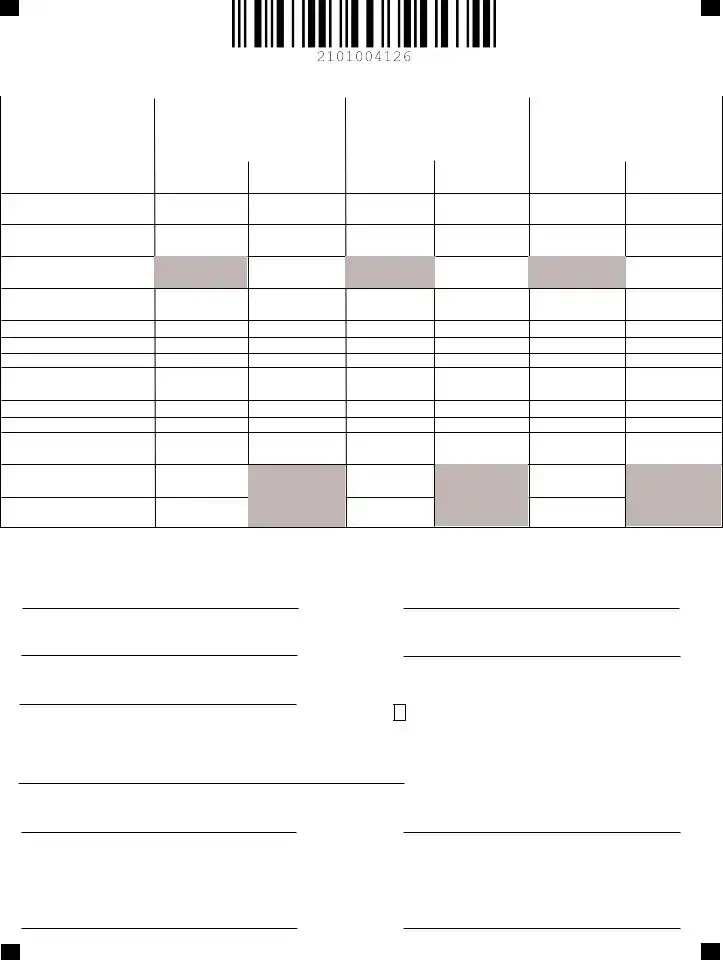

Georgia Form |

|

|

|

TAXPAYER’S FEIN |

||||

Net Operating Loss Adjustment |

|

|

|

|

|

|

|

|

For Individuals and Fiduciaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

PAGE 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

___________________ PRECEDING TAX |

___________________ PRECEDING TAX |

__________________ PRECEDING TAX |

||||

|

TAX YEAR: |

YEAR ENDED ______________________ |

YEAR ENDED ______________________ |

YEAR ENDED ______________________ |

||||

|

RESIDENCY STATUS |

|

|

|

|

|

|

|

|

FILING STATUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Return as filed or |

(b) Liability after |

(c) Return as filed or |

(d) Liability after |

(e) Return as filed or |

(f) Liability after application |

|

|

Computation of overpayments |

liability as last |

application of |

liability as last |

application of |

liability as last |

of |

|

|

|

determined |

determined |

determined |

||||

1.Federal adjusted gross income (exclude Federal NOL)

2.Georgia adjustments. See Page 5 of the instructions

3.Net operating loss. See Page 5 for 80% rule and other instructions

4.Georgia adjusted gross income Net total of Lines 1, 2 and 3.

5.Deductions. See Page 5 of the instructions.

6.Subtract Line 5 from Line 4

7.Exemptions. See Page 5 of instructions.

8.Taxable Income. Subtract Line 7 from Line 6.

9.Income Tax.

10.Credits. See Page 5 of the instructions.

11.Tax after credits. Subtract Line 10 from Line 9.

12.Enter Line 11 column (b) (d) (f), respectively.

13.Decrease in tax. Subtract Line 12 from Line 11.

Mailing Address: Georgia Department of Revenue Processing Center, PO Box 740318, Atlanta, GA.

Under penalty of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief it is true, correct and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Taxpayer’s Signature

Date

Taxpayer’s Phone Number

Taxpayer’s Spouse Signature

Date

Check the box to authorize the Georgia Department of Revenue to discuss the contents of this return with the named preparer.

By providing my

Taxpayer’s

Signature of Preparer Other Than Taxpayer |

Preparer’s Phone Number |

|

|

|

|

Name of Preparer Other Than Taxpayer |

Preparer’s FEIN |

|

Preparer’s Firm Name |

Preparer’s SSN/PTIN/SIDN |

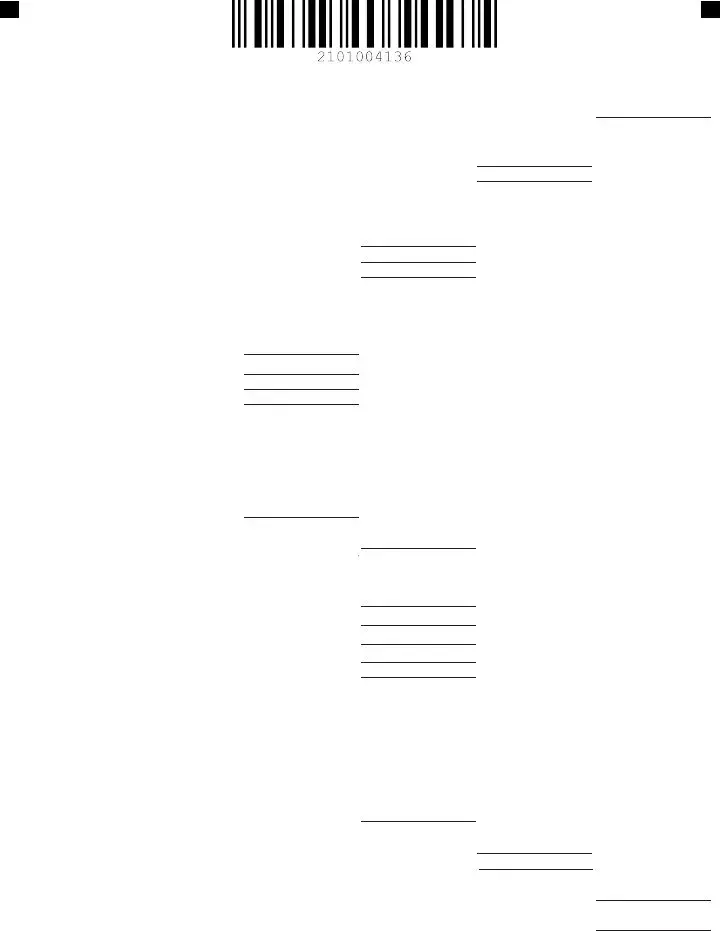

Georgia Form

COMPUTATION OF NET |

|

|

|

|

|

TAXPAYER’S FEIN |

|

|

||||

OPERATING LOSS - LOSS YEAR |

|

|

|

|

|

|

|

|

|

|

||

PAGE 3 |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

PART YEAR AND NONRESIDENTS, SEE INSTRUCTIONS ON PAGE 4 |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Adjusted gross income, Line 8, Page 2 of form 500 |

|

|

|

|

|

|

1. |

|

|

|

|

2. |

Line 9 adjustments |

.... |

................................ |

|

|

2. |

|

|

|

|||

|

. ..........................................................................................................3. Deductions (Applies to individuals only) |

|

|

|

|

|

|

|

|

|

|

|

|

|

. ........................a. Enter amount of your Standard or Itemized Deductions, Line 11c or Line 12 of form 500 |

3a. |

|

|

|

|

|||||

|

|

b. Personal exemption, Line 14c of form 500 |

|

|

|

|

3b. |

|

|

|

|

|

4. |

Total (Lines 3a and 3b) |

|

|

|

|

4. |

|

|

|

|

|

|

5. |

Taxable income. Total of Line 1 and Line 2 less Line 4 |

|

|

|

|

|

|

5. |

|

|

|

|

|

6. Exemptions claimed, Line 14c of form 500 |

|

|

|

|

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

7. |

................Nonbusiness capital losses before limitation. Enter as a positive number |

|

7. |

|

|

|

|

|

|

|||

8. |

Total nonbusiness capital gains (without regard to any I.R.C section 1202 exclusion) |

|

8. |

|

|

|

|

|

|

|||

9. |

If Line 7 is more than Line 8, enter the difference; otherwise, enter |

|

9. |

|

|

|

|

|

|

|||

10. |

If Line 8 is more than Line 7, enter the difference; otherwise, enter |

|

10. |

|

|

|

|

|

|

|||

|

11. Enter either your standard deduction or itemized deductions |

|

|

|

|

|

|

|

|

|||

|

|

less casualty, 2106 deductions, and state and local |

11. |

|

|

|

|

|

|

|

|

|

|

|

income taxes |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Contributions to |

|

|

|

|

|

|

|

|

|

|

|

12. |

|

|

|

|

|

|

|

|

|

|||

13. |

Alimony (paid) |

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

Forfeited interest/penalty on early withdrawal |

14. |

|

|

|

|

|

|

|

|

|

|

15. |

Contribution to an IRA |

15. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

16. |

Other (specify) |

16. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

17. |

Total nonbusiness deductions (Lines 11 through 16) |

|

|

|

17. |

|

|

|

|

|

|

|

18. |

Dividend income |

18. |

|

|

|

|

|

|

|

|

|

|

_______________________ |

|

|

|

|

|

|

|

|||||

19. |

Interest income |

19. |

|

|

|

|

|

|

|

|

|

|

_______________________ |

|

|

|

|

|

|

|

|||||

20. |

Alimony/pensions/annuities |

20. |

|

|

|

|

|

|

|

|

|

|

21. |

GA adjustment for retirement exclusion, U.S. interest, |

|

|

|

|

|

|

|

|

|

|

|

21. |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

22. |

Other (specify) |

22. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

23. |

Total nonbusiness income other than capital gains (Lines 18 through 22) |

|

23. |

|

|

|

|

|

|

|||

|

24. Add Lines 10 and 23 |

|

|

|

24. |

|

|

|

|

|

|

|

25. |

If Line 17 is more than Line 24, enter the difference; otherwise enter |

|

|

25. |

|

|

|

|

|

|||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|||||

26. |

If Line 24 is more than Line 17, enter the difference; otherwise enter |

|

|

|

|

|

|

|

|

|||

|

|

Do not enter more than Line 10 |

|

|

|

26. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

27. |

Total business capital losses before limitation. Enter as a positive number |

|

27. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||

28. |

Total business capital gains (without regard to I.R.C. section 1202 exclusion) |

|

28. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||

29. |

Add Lines 26 and 28 |

|

|

|

29. |

|

|

|

|

|

|

|

30. |

If Line 27 is more than Line 29, enter the difference; otherwise enter |

|

30. |

|

|

|

|

|

|

|||

31. |

Add Lines 9 and 30 |

|

|

|

31. |

|

|

|

|

|

|

|

|

32. Enter your net capital loss before the $3,000 federal limitation, if any. Enter as a |

|

|

|

|

|

|

|

|

|||

|

|

positive number. If you do not have this loss (and do not have an I.R.C. section |

|

|

|

|

|

|

|

|

||

|

|

1202 exclusion) skip Lines 32 through 37 and enter on Line 38 the amount from |

|

|

|

|

|

|

|

|

||

|

|

|

32. |

|

|

|

|

|

|

|||

|

|

Line 31 |

|

|

|

|

|

|

|

|

|

|

33. |

I.R.C. section 1202 exclusion (50% exclusion for gain from certain small business |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||

|

|

stock). Enter as a positive number |

|

|

|

|

33. |

|

|

|

|

|

34. |

Subtract Line 33 from Line 32. If zero or less enter |

|

|

|

34. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

35. Enter your net capital loss after the $3,000 Federal limitation. |

|

|

|

|

|

|

|

|

|||

|

|

Enter as a positive number |

|

|

|

35. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36. |

If Line 34 is more than Line 35, enter the difference; otherwise enter |

|

36. |

|

|

|

|

|

|

|||

37. |

........................................................If Line 35 is more than Line 34, enter the difference; otherwise enter |

|

37. |

|

|

|

|

|

||||

38. |

Subtract Line 36 from Line 31. If zero or less, enter |

|

|

|

|

38. |

|

|

|

|

|

|

|

39. Previous net operating loss claimed. Enter as a positive number |

|

39. |

|

|

|

|

|

||||

40. |

Add Lines 6, 25, 33, 37, 38, 39 |

|

|

|

|

|

|

40. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

41. Loss amount. Combine Lines 5 and 40. If the result is less than zero, enter it here. If the loss is being carried back to a part year or nonresident return, |

41. |

|

|

||||||||

|

|

see instructions on Page 4. If the result is zero or more, you do not have a normal net operating loss |

|

|

_______________________ |

|

|

|||||

42. |

IRC Section 461(1) loss eligible to be carried forward only (enter as negative) |

|

|

|

42. |

|

|

|

||||

|

43. |

Total Net Operating Loss. Combine Lines 41 (if Line 41 is a negative) and Line 42. |

Enter on Page 1 |

|

|

43. |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Georgia Form

PAGE 4

TAXPAYER’S FEIN

NET OPERATING LOSS CARRYOVER

Complete if applicable. See page 5 for instructions.

Complete one column before going

to the next column. Start with the earliest carryback year.

1.Net operating loss deduction .....

2.Taxable income before N.O.L. carryback .........................................

3.Net capital loss deduction. Enter as a positive number........................

4.I.R.C. section 1202 exclusion. Enter as a positive number..............

5.Adjustments to adjusted gross income ...........................................

6.Adjustments to itemized deductions

7.Exemptions ................................

8.Modified taxable income. Combine Lines 2 through 7. If zero or less, enter

9.Net operating loss carryover. Line

1 less Line 8. If zero or less, enter

___________________ PRECEDING TAX |

___________________ PRECEDING TAX |

__________________ PRECEDING TAX |

||||||||

YEAR ENDED ______________________ |

YEAR ENDED ______________________ |

YEAR ENDED ______________________ |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART YEAR AND NONRESIDENTS

Complete if applicable

Year_________ Use a separate schedule for all applicable years.

1.Georgia Adjusted Gross Income (exclude Federal NOL). See instructions below.....................................................

2.Georgia NOL. See instructions below............................

3.Adjusted AGI for NOL purposes...................................

4.Percentage. Line 3, column C divided by column A. See instructions below.....................................................

5.Itemized or standard deduction. See instructions below.

6.Personal exemptions.......................................................

7.Total deductions and exemptions; add Lines 5 & 6..........

8.Line 4 percentage times Line 7........................................

9.Adjusted taxable income, column C, Line 3 less Line 8, enter here and on taxable income Line 8 of Page 2.......

Column A |

Column B |

Column C |

|

Total |

Non Georgia |

Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part Year and Nonresident schedule instructions. (Use if carrying the loss to a part year or nonresident return regardless of whether the loss year is a part year or nonresident return.)

1.Lines 1 and 5, enter the amounts, after the adjustments that are required by I.R.C. Section 172 if any apply, for the year the loss is being carried to.

2.Line 2 column A and C, enter loss from Page 3, Line 41 or from Page 4, Line 9 of the net operating loss carryover schedule.

3.Line 4, if Georgia AGI is zero or negative, the percentage is zero. If the adjusted Federal AGI is zero or negative, the Line 4 percentage is considered to be 100%. This also applies if both adjusted Federal AGI and Georgia AGI are zero or negative. In this case, the taxpayer is entitled to the full exemp- tion amount and deductions.

Additional instructions for part year and nonresidents.

1.

2.

3.

500- NOL (Rev. 12/31/20)

General Instructions

A net operating loss carryback adjustment may be filed on this form by an individual or fiduciary taxpayer that desires a refund of taxes afforded by carryback of a net operating loss. This form must be filed no later than 3 years from the due date of the loss year income tax return, including any extensions which have been granted. Form 500X should not be used to carryback a NOL Form

Generally a net operating loss must be carried back (if applicable) and forward

in the procedural sequence of taxable |

periods provided by Section 172 |

of the Internal Revenue Code of 1986, |

as defined in Code Section |

the carryback period is 2 |

years (with special |

rules |

for farmers |

(5 |

||

years), |

casualty losses |

(3 years); specified |

liability |

loss (10 |

years), |

|

small |

business loss attributable to federally declared |

disasters |

(3 |

years); |

||

etc.) For losses incurred in taxable years ending after December 31, 2017, there is no carryback (with a 2 year carryback for farmers) and unlimited carryover. Also, Georgia does not follow the following federal provisions:

Special carryback rules enacted in 2009.

Special rules relating to Gulf Opportunity Zone public utility casualty losses, I.R.C. Section 1400N(j).

5 year carryback of NOLs attributable to Gulf Opportunity Zone losses, I.R.C. Section 1400N(k).

5 year carryback of NOLs incurred in the Kansas disaster area after May 3, 2007, I.R.C. Section 1400N(k).

5 year carryback of certain disaster losses, I.R.C. Sections 172(b)(1)(J) and 172(j).

The election to deduct public utility property losses attributable to May 4, 2007 Kansas storms and tornadoes in the fifth tax year before the year of the loss, I.R.C. Section 1400N(o).

For losses incurred in taxable years beginning on or after January 1, 2018, the net operating loss cannot offset more than 80% of Georgia taxable net income.

Within 90 days from the last day of the month in which this form is filed, the Commissioner of Revenue shall make a limited examination of the form and disallow without further action any form containing errors of computation not correctable within such

*Note: This form shall constitute a claim for credit or refund.

If the commissioner should determine that the amount credited or refunded by an application is in excess of the amount properly attributable to the carry- back with respect to which such amount was credited or refunded, the commissioner may assess the amount of the excess as a deficiency as if it were due to a mathematical error appearing on the face of the return.

What to attach:

1.Copy of Federal Application for Net Operating Loss.

2.Copy of Federal return for the loss year that includes pages 1 and 2, schedules 1, A, D, and E.

3.Copy of Federal returns for the carryback years that includes pages 1 and 2, Schedule 1 and Schedule A and any schedules that were recalculated in carry- back year.

4.Copy of Georgia returns for the carryback or carryforward years

5.Copy of Georgia form 500 for the lossyear.

Be sure to attach all required forms listed above and complete all lines of the Form

The carryback period may be foregone and the NOL carried forward. Election: A taxpayer is bound by the Federal election to forego the carryback period. A copy of this election should be attached to the Georgia return. If there is a Georgia NOL but no Federal NOL, the taxpayer may make an election “for Georgia purposes only” under the same rules and restrictions as the Federal election. The Form

Example: A taxpayer has a large Net Operating Loss in 1998 (both Federal and Georgia). With his timely filed Federal return, he includes a statement that he elects to forgo the carryback period. He must therefore carry his Georgia (as well as his Federal) NOL forward without first carrying it back. Any portion not absorbed after 20 years is lost.

Page 2 Instructions

Columns a, c, and e.

Enter the amounts from your original return or as previously adjusted by you or the Department of Revenue.

Columns b, d, and f.

Lines 1 and 5, enter the amounts after adjustments that are required by I.R.C. Section 172, if any. Line 1 should not be reduced by the Federal or Georgia NOL.

Lines 2 and 7, enter the amounts from your original return or as previously adjusted by you or the Department of Revenue.

Line 3. For the earliest carryback year, in column (b) enter the NOL from page 3, line

41.In column (d) and (f) if applicable, enter the amount from line 9 of the Net Operating Loss Carryover schedule on page 4. For example, a taxpayer has a oss from 2013 which has a two year carryback period. The loss from page 3 line 41 s listed on line 3 in column (b) for 2011. Not all of the loss is utilized. The taxpayer makes the adjustments as required for 2011 in the Net Operating Loss Carryover schedule on page 4 and lists the amount from line 9 (if it is a positive amount) on ine 3 in column (d) for 2012.

Line 10, the credit for taxes paid to other states should be recomputed based on the new Georgia AGI and deductions. Other credits that are based on liability should be adjusted accordingly. Any credits that are not allowed and that are eligible for carry- forward can be carried forward. Do not enter more than Line 9.

Page 3 Instructions

A Georgia Net Operating Loss (NOL) must be computed separately from any Federal NOL. It is possible to have a Federal NOL, but not a Georgia NOL.

Line 21. In computing a Georgia NOL only Georgia amounts can be used. Interest on U.S. savings bonds should be entered as a negative number on this line. Non- Georgia municipal interest should be entered as a positive number on this line. The nonbusiness portion of the retirement exclusion should be entered as a negative number on this line. This should be computed as follows. The total nonbusiness income (as it is defined for NOL purposes) that is included in the retirement exclusion should be divided by the total income that is included in the retirement exclusion. This percentage should then be multiplied by the retirement exclusion. For example, if the taxpayer has $8,000 in wages and $20,000 in interest income, the taxpayer would divide $20,000 by $28,000 and then multiply this by the retirement exclusion amount. When computing the percentage, the following guidelines should be followed:

1.If the total nonbusiness income that is included in the retirement exclusion is zero or less than zero, the percentage is zero. This would apply even if the total income that is included in the retirement exclusion is zero or less than zero.

2.If the total nonbusiness income that is included in the retirement exclusion is greater than zero and exceeds the total income that is included in the retirement exclusion, the percentage is 100%. This would apply even if the total income that is included in the retirement exclusion is zero or less than zero.

Additionally, in situations where two people file married filing joint, a separate computation should be made to determine each taxpayer’s portion of the retirement exclusion that is related to nonbusiness income.

Line 42. Georgia follows the I.RC. Section 461(l) loss limitation. However, before the I.RC. Section 461(l) loss limitation is applied, the business should compute the business income and deductions pursuant to the I.R.C. as defined for Georgia purposes (with the I.R.C. section 168(k) disallowance, etc.). Then the 461(l) provisions should be applied. The 461(l) loss that is disallowed and is eligible to be carried forward should be entered on line 42. This amount must be included when the 500- NOL is filed to establish the NOL on the Department’s systems so the NOL will be available when subsequent year returns are filed.

Page 4 Instructions

Net Operating Loss Carryover

1.A Georgia Net Operating Loss (NOL) carryover must be computed separately from any Federal NOL carryover. It is possible to have a Federal NOL carryover but not a Georgia NOL carryover.

2.Line 3, enter as a positive number the adjustment as required by I.R.C. Section 172, if it applies.

3.Line 4, enter as a positive number the gain excluded under I.R.C. section 1202 on the sale or exchange of qualified small business stock, if it applies.

4.Lines 5 and 6, enter the adjustments that are required by I.R.C. Section 172, if any.

5.Line 9, if the 80% limitation applied to the year the loss was carried to,

an additional adjustment must be made before entering the loss on either the carryover year on page 2 or the carryover year after the loss year. After computing the amount on line 9, add the difference between the taxable income before NOL carryback on line 2 and the NOL actually used considering the 80% limitation. For example, the taxpayer has a 2019 NOL of 200,000. Their taxable income in 2020 is 100,000 (they used 80,000 of the NOL after considering the

80% rule) and that $100,000 is entered on line 2 of the schedule at the top of page 4. For simplicity sake assume the only adjustment that is required on the top of page 4 are exemptions of 7,400 and that is entered on line 7.

Therefore |

the modified taxable |

income on line 8 |

is 107,400. Subtracting |

|

the 107,400 from the 200,000 results in 92,600 being entered on line 9. |

The |

|||

difference |

of the 100,000 line |

2 amount and the |

80,000 is 20,000. |

This |

would be added to the 92,600 and therefore 112,600 is available to be carried to 2021.

500- NOL (Rev. 12/31/20)

Please note that the amount from line 9 of the year directly preceding the loss year is the amount (if any) that can be carried to the year after the loss year (carryover year). The same adjustments from this schedule must be made to each year in the carryover period to determine the amount that is available to be carried to the next carryover year. For example, a taxpayer has a loss from 2013 which has a two year carryback period. The loss is

carried back to 2011 and |

2012 |

on |

page 2 but not all of the |

loss |

is |

|||||||||

utilized. |

The taxpayer makes |

the |

adjustments as |

required |

|

to |

2011 |

|||||||

and 2012 |

in |

the |

Net Operating |

Loss Carryover |

schedule |

at |

the |

top |

||||||

of page 4. |

After computing the |

amount for 2012 |

there |

is |

a |

positive |

||||||||

amount |

on |

line 9 |

of |

the 2012 |

column. This amount |

can |

be carried |

|||||||

to 2014 and the amount used in |

2014 should |

be listed on the 2014 |

||||||||||||

return not on Form |

is |

utilized |

|

in 2014, |

||||||||||

the taxpayer should make the same adjustments |

to |

2014 |

as |

|

are |

|||||||||

listed |

in |

the |

Net |

Operating |

Loss Carryover |

schedule |

|

on |

page |

|||||

4to determine if any loss is available to be carried to 2015. A schedule showing this should be attached to the 2014 return and should not be listed on the Form

If the loss was carried to a part year or nonresident return, on line 2 of the carryover schedule enter the amount from line 14 schedule 3 of Form 500 for the year it was carried to. For lines 3, 4, and 5, enter amount if related to Georgia Income. For lines 6 and 7, multiply the amount by the ratio on line 9, schedule 3 of Form 500 for the year the loss was carried to.

Part Year and Nonresident Instructions. See instructions on page 4.

| Fact Name | Description |

|---|---|

| Form Purpose | The Georgia Form 500-NOL is used by individuals and fiduciaries to adjust net operating losses for state tax purposes. |

| Filing Deadline | This form must be filed no later than three years from the due date of the loss year income tax return, including any extensions. |

| Governing Law | The form is governed by Section 172 of the Internal Revenue Code and Georgia Code Section 48-1-2. |

| Attachment Requirements | Taxpayers must attach a complete copy of their federal return for the loss year along with other specified documents. |

Filling out the Georgia Form 500-NOL can seem daunting, but following a clear step-by-step process makes it manageable. This form is essential for individuals and fiduciaries who have experienced a net operating loss and wish to adjust their tax filings accordingly. To ensure accuracy, gather all necessary documents before starting.

After submitting the form, be prepared to wait for a response from the Georgia Department of Revenue. They may take up to 90 days to review your application and issue any refunds or credits based on your net operating loss claim. Keep a copy of your submission for your records.

What is the Georgia Form 500-NOL?

The Georgia Form 500-NOL is used by individuals and fiduciaries to report a net operating loss (NOL) adjustment. This form allows taxpayers to claim a refund of taxes by carrying back a net operating loss to prior tax years or carrying it forward to offset future income. It is essential to file this form within three years from the due date of the loss year’s income tax return, including any extensions.

Who should file the Georgia Form 500-NOL?

Any individual or fiduciary who has experienced a net operating loss and wishes to adjust their tax liability should file this form. This includes taxpayers who have losses from normal business operations, casualty losses, or farm losses. If you are unsure whether you qualify, it is advisable to consult a tax professional.

What information do I need to complete the form?

To complete the Georgia Form 500-NOL, you will need your Social Security Number (SSN) or Federal Employer Identification Number (FEIN), details about your net operating loss, and a complete copy of your federal tax return for the loss year. Additionally, you should provide any relevant schedules and forms that support your claim, including copies of your federal returns for the carryback years.

What happens if I only want to carry the loss forward?

If you decide to carry the loss forward without carrying it back, you still need to file the Georgia Form 500-NOL by the due date of the loss year return. This is necessary to establish the NOL in the Department’s system. Make sure to complete all applicable lines on the form to avoid any issues with your application.

Are there specific instructions for part-year residents and nonresidents?

Yes, part-year residents and nonresidents must follow specific instructions when filling out the form. You should complete the designated sections that apply to your residency status and ensure that you calculate your Georgia adjusted gross income correctly. If you are carrying a loss to a part-year or nonresident return, additional calculations will be necessary to determine the appropriate amounts.

What should I attach to the form when I file it?

When submitting the Georgia Form 500-NOL, you need to attach several documents. These include a copy of your federal application for the net operating loss, your federal return for the loss year, and any federal returns for the carryback years. Additionally, include copies of your Georgia returns for the carryback or carryforward years and the Georgia Form 500 for the loss year. Ensure all required forms are attached to avoid disallowance of your application.

What if I have both a federal and a Georgia NOL?

If you have both a federal and a Georgia NOL, it is important to remember that they are computed separately. You may have a federal NOL but not a Georgia NOL. When filing your Form 500-NOL, be sure to follow Georgia-specific rules and adjustments, as they can differ from federal guidelines. This ensures that your claim is accurate and compliant with state regulations.

Incomplete Federal Return Attachment: Many individuals forget to attach a complete copy of their federal return for the loss year. This omission can lead to delays or disallowance of the NOL claim.

Incorrect Tax Year Selection: Some taxpayers mistakenly select the wrong taxable year for the net operating loss. Ensure that the year corresponds accurately with the loss incurred.

Failure to Specify Type of Loss: It’s essential to correctly identify the type of loss—normal, casualty, or farm loss. Failing to do so can result in processing issues.

Neglecting to Check Residency Status: Taxpayers often overlook the residency status section. This is crucial, especially for part-year residents or nonresidents, as it affects the calculations.

Errors in Calculating the NOL Amount: Many individuals miscalculate the net operating loss amount. Double-check all figures to ensure accuracy before submission.

When dealing with the Georgia Form 500-NOL, several other forms and documents are often required to ensure a complete and accurate submission. Each of these documents serves a specific purpose in the process of claiming a net operating loss and may help facilitate the review and approval of your claim. Below is a list of commonly used forms alongside the Georgia 500-NOL.

Submitting these forms alongside the Georgia Form 500-NOL helps to create a clear picture of your financial situation. Ensure that all required documentation is complete and accurate to facilitate the processing of your claim. This can make a significant difference in receiving the benefits you are entitled to during difficult financial times.

The Georgia Form 500-NOL is a specific document used for reporting net operating losses. It has similarities to several other forms that serve related purposes in tax reporting. Below is a list of documents that share characteristics with the Georgia Form 500-NOL:

Each of these forms serves a specific purpose but shares commonalities with the Georgia Form 500-NOL in terms of reporting income, losses, and adjustments. Understanding these similarities can help in navigating tax reporting requirements effectively.

When filling out the Georgia Form 500-NOL, it’s important to follow specific guidelines to ensure your application is processed smoothly. Here’s a list of things you should and shouldn’t do:

By following these guidelines, you can help ensure that your Form 500-NOL is completed correctly, which may expedite the processing of your application.

Here are ten common misconceptions about the Georgia Form 500-NOL, along with clarifications:

This form is applicable to both individuals and fiduciaries who have incurred a net operating loss.

A complete copy of your federal return for the loss year must be attached to the 500-NOL form.

Generally, the carryback period is limited to two years, with specific exceptions for certain types of losses.

It is possible to have a Georgia NOL even if there is no federal NOL, but you must compute it separately.

The 500-NOL form is required even if you are only carrying the loss forward to establish it in the Department’s system.

For losses incurred in years after December 31, 2017, the NOL can only offset up to 80% of Georgia taxable net income.

The 500-NOL is specifically for claiming a net operating loss adjustment, not for amending prior returns.

A refund is not guaranteed; it depends on the calculations and whether the loss can be applied to previous tax liabilities.

It is crucial to follow the specific instructions provided for calculating Georgia NOL, as they differ from federal guidelines.

The 500-NOL form must be filed no later than three years from the due date of the loss year income tax return.

Understanding the Georgia Form 500-NOL is crucial for individuals and fiduciaries seeking to adjust their net operating loss (NOL) for tax purposes. Here are key takeaways regarding the completion and use of this form: