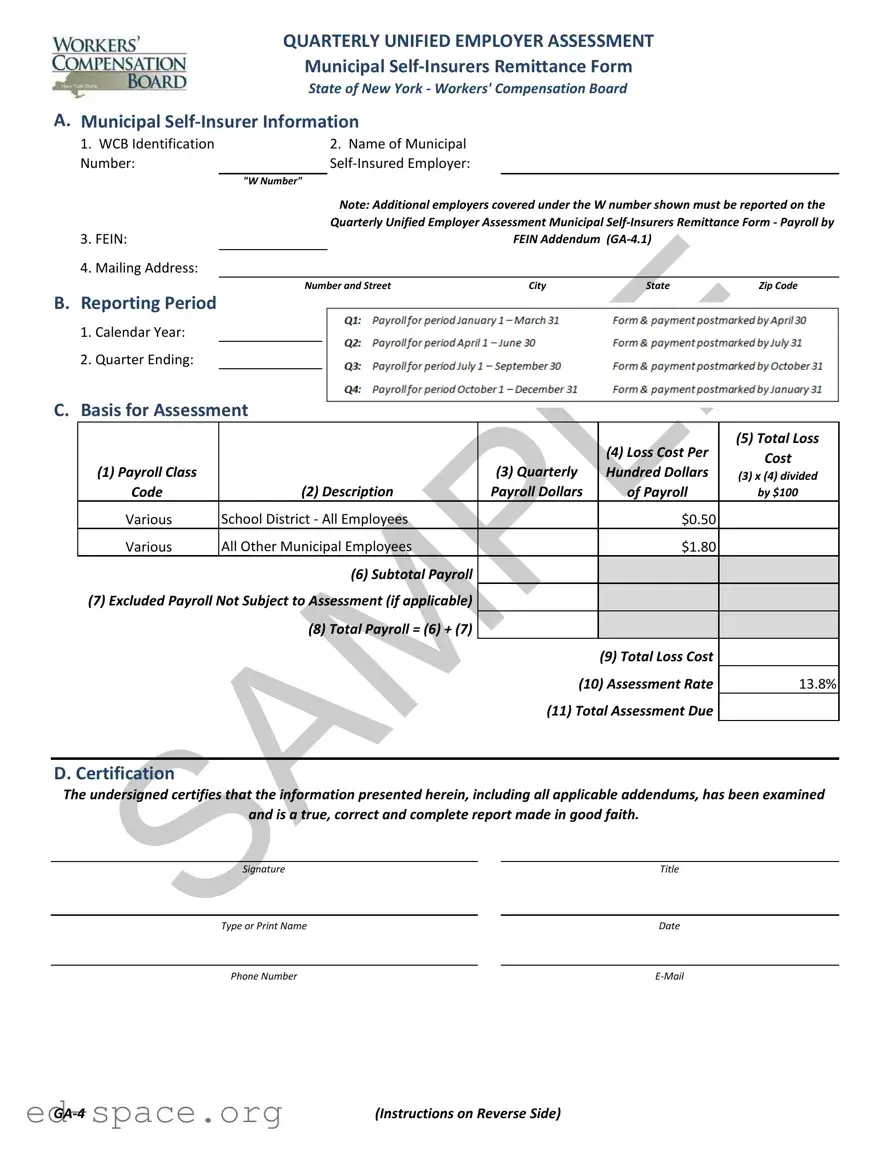

The GA-4 New York form, officially known as the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, plays a crucial role for municipal self-insured employers in New York. This form is required to be completed quarterly and submitted within thirty days after the end of each quarter. It collects essential information about the self-insured employer, including the WCB identification number, the legal name of the employer, and the Federal Employer Identification Number (FEIN). The form also outlines the reporting period and the basis for assessment, which includes payroll data and applicable loss costs. Employers must categorize their payroll into specific groups, such as school districts and other municipal employees, to determine the total assessment due. Additionally, if multiple employers are covered under the same W number, an addendum (GA-4.1) must be included to ensure accurate reporting. The form not only facilitates the assessment process but also ensures compliance with state regulations regarding workers' compensation self-insurance.

QUARTERLY UNIFIED EMPLOYER ASSESSMENT

Municipal

State of New York - Workers' Compensation Board

A. Municipal

1. |

WCB Identification |

|

2. Name of Municipal |

|

|

|

Number: |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

"W Number" |

|

|

|

|

|

|

|

Note: Additional employers covered under the W number shown must be reported on the |

|||

|

|

|

Quarterly Unified Employer Assessment Municipal |

|||

3. |

FEIN: |

|

|

FEIN Addendum |

|

|

4. |

Mailing Address: |

|

|

|

|

|

|

|

|

|

|

||

|

|

Number and Street |

City |

State |

Zip Code |

|

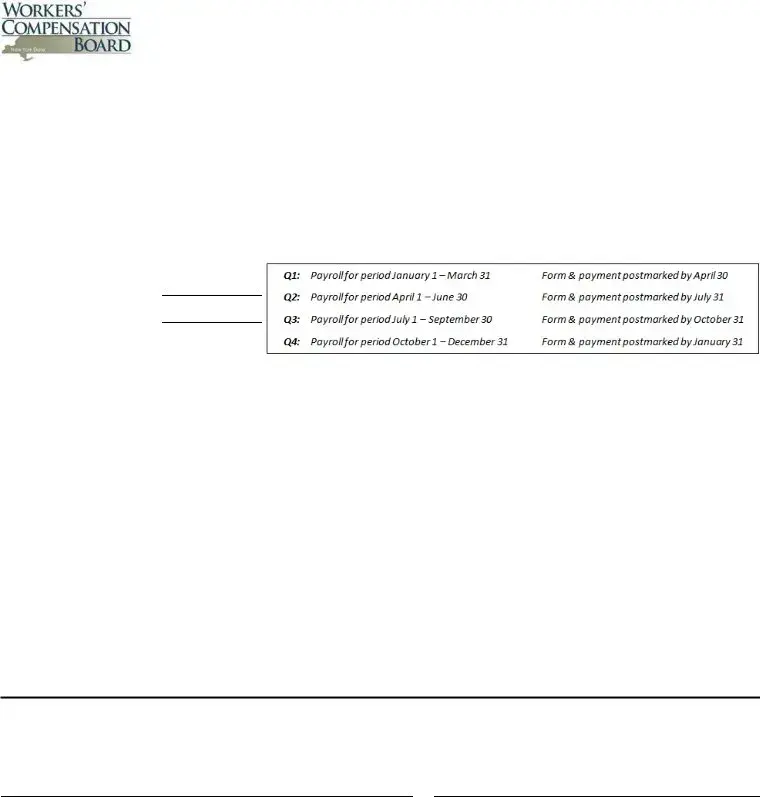

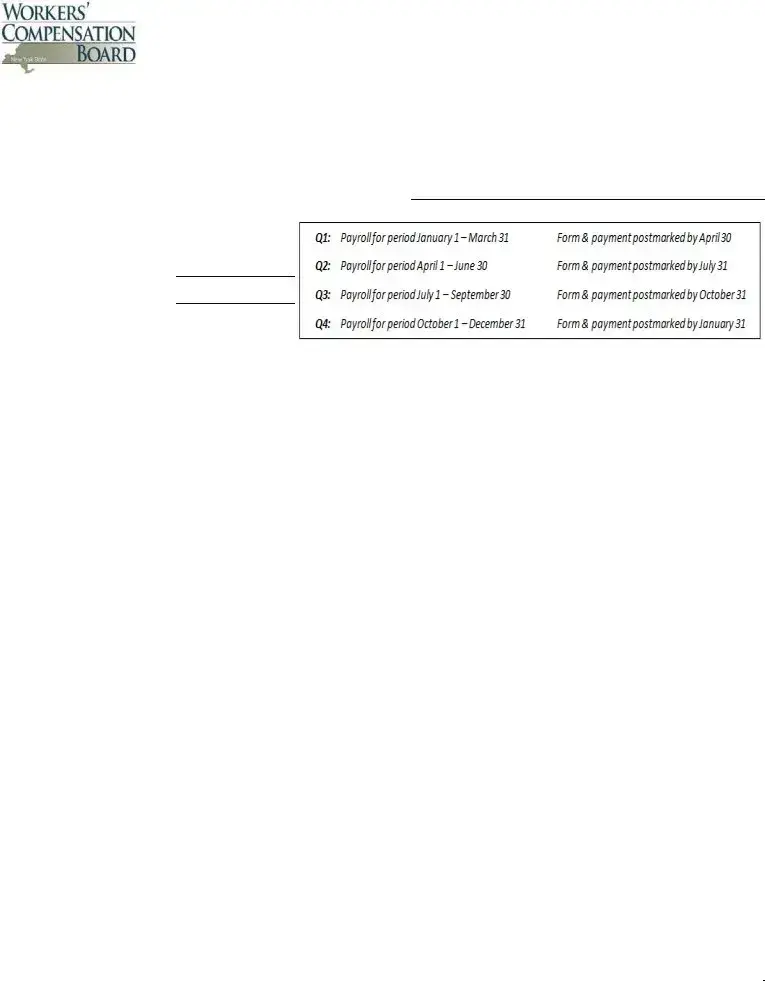

B.Reporting Period

1.Calendar Year:

2.Quarter Ending:

C.Basis for Assessment

|

|

|

|

(5) Total Loss |

|

|

|

(4) Loss Cost Per |

Cost |

|

|

(3) Quarterly |

|

|

(1) Payroll Class |

|

Hundred Dollars |

(3) x (4) divided |

|

Code |

(2) Description |

Payroll Dollars |

of Payroll |

by $100 |

Various |

School District - All Employees |

|

$0.50 |

|

Various |

All Other Municipal Employees |

|

$1.80 |

|

|

(6) Subtotal Payroll |

$0 |

|

|

(7) Excluded Payroll Not Subject to Assessment (if applicable) |

|

|

|

|

|

(8) Total Payroll = (6) + (7) |

$0 |

|

|

|

|

|

(9) Total Loss Cost |

|

|

|

(10) Assessment Rate |

13.8% |

|

|

|

(11) Total Assessment Due |

|

|

|

|

|

|

|

D. Certification

The undersigned certifies that the information presented herein, including all applicable addendums, has been examined

and is a true, correct and complete report made in good faith.

Signature |

|

Title |

|

|

|

Type or Print Name |

|

Date |

|

|

|

Phone Number |

|

(Instructions on Reverse Side) |

Instructions for Completing Quarterly Unified Employer Assessment

Municipal

General Instructions

1.The Quarterly Unified Employer Assessment Municipal

2.Additional municipal employers covered under the W number shown must be reported on the Quarterly Unified Employer Assessment Municipal Self- Insurers Remittance Form - Payroll by FEIN Addendum

3.Questions about the form or process should be directed to [email protected].

4.Checks are to be made payable to the Chair, NYS Workers' Compensation Board.

5.To ensure the proper application of payment please include W Number and applicable quarter on check.

6.This report and corresponding payment, along with applicable addendum, must be submitted quarterly by every municipal employer actively self- insured for workers' compensation. Employers that discontinued their

Submit completed form via

and mail check to address below

Or mail completed form and check to:

New York State Workers’ Compensation Board

328 State Street

Finance Unit, Room 331

Schenectady, NY

Municipal

1.The WCB Identification Number or "W Number" as assigned to the municipal

2.The Name of the Municipal

3.The FEIN, or Federal Employer Identification Number, must be reported for the municipal

4.The full mailing address of the municipal

Basis for Assessment

1.A blended rate for municipal payroll will be used and there is no need to breakout by class.

2.Payroll must be broken out between employers which are school districts and all other municipal employers.

3.Total quarterly payroll associated with either the school district and/or all other types of municipal

4.The loss cost per hundred dollars of payroll for municipal employers and school districts is set annually by the Chair. The rates are shown on the Quarterly Unified Employer Assessment Municipal

5.The total loss cost is determined by multiplying the payroll by the loss cost shown and dividing by $100.

6.Subtotal of payroll reported on the Quarterly Unified Employer Assessment Municipal

7.Excluded payroll not subject to assessment.

8.With limited exception, total payroll should agree with that reported on the Quarterly Combined Withholding, Wage Reporting and Unemployment

|

Insurance Return |

|

please provide reconciliation. No payroll caps are to be applied. |

9. |

Equal to the sum of all of the loss cost by payroll class shown. |

10. |

The assessment rate for the rating period established by the Chair pursuant to WCL Section 151. This can be found on the WCB's website |

|

www.wcb.ny.gov. |

11. |

The total assessment due is equal to the total loss cost multipled by the assessment rate. |

Certification

In accordance with WCL Section 151 the Chair may conduct periodic audits of any

QUARTERLY UNIFIED EMPLOYER ASSESSMENT

Municipal

Payroll by FEIN Addendum

State of New York - Workers' Compensation Board

A. Municipal

|

|

2. Name of |

1. WCB Identification |

|

Municipal Self- |

Number: |

|

Insured Employer: |

|

|

|

|

"W Number" |

|

B.Reporting Period

1.Calendar Year:

2.Quarter Ending:

C.Municipal Employers Covered Under the W Number Shown Above

|

|

|

(4) Excluded |

|

|

(3) Quarterly |

Payroll (if |

(1) FEIN |

(2) Municipal |

Payroll |

applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(5) Subtotal Payroll |

|

|

|

(6) Subtotal Excluded Payroll (if applicable) |

|

|

|

(7) Total Payroll = (5) + (6) |

|

$0 |

|

|

|

|

Instructions for Completing Quarterly Unified Employer Assessment

Municipal

Payroll by FEIN Addendum

General Instructions

1.The Quarterly Unified Employer Assessment Municipal

2.The Quarterly Unified Employer Assessment Municipal

3.The payroll by class code reported on the Quarterly Unified Employer Assessment Municipal

4.Questions about the form or process should be directed to [email protected].

5.This addendum, if applicable, must be sent quarterly with the Quarterly Unified Employer Assessment Municipal

Municipal

1.The WCB Identification Number or "W number" as assigned to the municipal

2.The Name of the Municipal

Municipal Employers Covered Under the W Number

1.The FEIN, or Federal Employer Identification Number, must be reported for the municipal

2.The municipal

3.Total quarterly payroll associated with the FEIN number.

4.Excluded payroll not subject to assessment.

5.Subtotal of payroll subject to assessment of the Quarterly Unified Employer Assessment Municipal

6.Subtotal of excluded payroll not subject to the assessment of the Quarterly Unified Employer Assessment Municipal

7.Total payroll and excluded payroll if applicable. With limited exception, total payroll should agree with that reported on the Quarterly Combined

Withholding, Wage Reporting and Unemployment Insurance Return

| Fact Name | Details |

|---|---|

| Form Purpose | The GA-4 form is used for the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance in New York State. |

| Submission Frequency | Every active municipal self-insured employer must complete and submit the form quarterly, within thirty days after the end of each quarter. |

| Governing Law | This form is governed by the New York Workers' Compensation Law, specifically WCL Section 151. |

| Required Information | Employers must provide their WCB Identification Number, name, FEIN, and mailing address on the form. |

| Assessment Rate | The assessment rate is set annually by the Chair of the Workers' Compensation Board and is currently 13.8%. |

| Payment Instructions | Payments should be made payable to the Chair, NYS Workers' Compensation Board, and can be submitted via mail or email along with the completed form. |

Completing the GA-4 form is an essential task for municipal self-insurers in New York. This form needs to be filled out accurately and submitted on time to ensure compliance with state regulations. Below are the steps to guide you through the process of filling out the GA-4 form.

After completing the form, ensure that you submit it along with any required payment within thirty days of the quarter's end. Remember to include your "W Number" on any checks made payable to the Chair, NYS Workers' Compensation Board. It is crucial to maintain accurate records and adhere to deadlines to avoid penalties or complications with your self-insured status.

What is the GA-4 New York form?

The GA-4 New York form, also known as the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, is a document that municipal self-insured employers in New York must complete each quarter. This form is essential for reporting payroll and calculating assessments related to workers' compensation. It ensures compliance with state regulations and helps maintain accurate records for self-insured employers.

Who is required to file the GA-4 form?

Every active municipal self-insured employer in New York must file the GA-4 form. This includes entities like school districts and other municipal employers that have been approved to self-insure for workers' compensation. If an employer has discontinued its self-insurance program, they are not required to submit this form.

What information do I need to complete the GA-4 form?

To complete the GA-4 form, you will need several key pieces of information. This includes your WCB Identification Number (or "W Number"), the full legal name of your municipal self-insured employer, your Federal Employer Identification Number (FEIN), and your mailing address. You will also need to report your total quarterly payroll and the basis for assessment, including loss costs and assessment rates.

When is the GA-4 form due?

The GA-4 form must be submitted within thirty days after the end of each quarter. Timely submission is crucial to avoid penalties and ensure compliance with state regulations. Mark your calendar to help you remember these deadlines!

What happens if I miss the GA-4 filing deadline?

If you fail to submit the GA-4 form by the deadline, you may face penalties. The Workers' Compensation Board may impose interest on any underpaid assessments, and repeated failures could lead to revocation of your self-insured status. It's important to stay on top of these deadlines to avoid complications.

How do I calculate the total assessment due on the GA-4 form?

The total assessment due is calculated by multiplying the total loss cost by the assessment rate. The assessment rate is established annually by the Chair of the Workers' Compensation Board. Make sure to refer to the form for the most current rates to ensure accurate calculations.

Can I report multiple employers on the GA-4 form?

Yes, if multiple employers are covered under the same W number, you must report them using the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form - Payroll by FEIN Addendum (GA-4.1). This addendum allows you to consolidate payroll information for all employers under your W number.

How do I submit the GA-4 form?

You can submit the completed GA-4 form via email to [email protected]. Additionally, you must mail a check made payable to the Chair, NYS Workers' Compensation Board, to the specified address. Ensure that your W number and applicable quarter are included on the check for proper processing.

What if I have questions about the GA-4 form?

If you have questions or need assistance with the GA-4 form, you can reach out directly to the Workers' Compensation Board at [email protected]. They are available to help clarify any uncertainties you may have regarding the form or the filing process.

What are the consequences of inaccurate reporting on the GA-4 form?

Inaccurate reporting can lead to significant consequences, including penalties and interest on underpaid assessments. If it is determined that you knowingly reported incorrect information, you could face additional penalties. Maintaining accurate records and reporting is essential to avoid these issues.

Incorrect WCB Identification Number: Many individuals mistakenly enter an incorrect or outdated WCB Identification Number, also known as the "W Number." This number is crucial for identifying the self-insured employer and ensuring accurate processing of the form.

Missing Full Legal Name: It is common for people to abbreviate or provide a different name than the full legal name of the municipal self-insured employer. This can lead to confusion and delays in processing.

Inaccurate FEIN Reporting: Failing to report the correct Federal Employer Identification Number (FEIN) is another frequent error. The FEIN must correspond to the municipal self-insurer, and any discrepancies can result in complications.

Improper Mailing Address: Some individuals neglect to provide the complete mailing address, including the street number, city, state, and zip code. This omission can hinder communication and affect the submission process.

Failure to Report Excluded Payroll: When applicable, individuals often forget to report excluded payroll not subject to assessment. This can lead to inaccuracies in the total payroll calculations.

Misunderstanding the Assessment Basis: There is a tendency to misunderstand how to calculate the total loss cost based on the payroll and the loss cost per hundred dollars. This misunderstanding can lead to incorrect total assessments.

Late Submission of the Form: Many fail to submit the form and payment within the required thirty days after the quarter ends. Late submissions can result in penalties and complications with self-insured status.

The GA-4 New York form, known as the Quarterly Unified Employer Assessment Municipal Self-Insurers Remittance Form, is a crucial document for municipal self-insured employers in New York. Along with this form, several other documents are often utilized to ensure compliance with reporting requirements and to provide comprehensive information about payroll and assessments. Below are five important forms and documents that are typically used in conjunction with the GA-4.

Utilizing these documents alongside the GA-4 form helps ensure that municipal self-insured employers remain compliant with New York's workers' compensation regulations. Understanding the purpose and function of each form can alleviate confusion and streamline the reporting process, ultimately supporting the financial health of municipal entities.

The GA-4 New York form is similar to several other documents that serve similar purposes in the realm of employer assessments and reporting. Here are six documents that share similarities with the GA-4 form:

When completing the GA-4 New York form, there are several important guidelines to follow. Adhering to these can help ensure accuracy and compliance.

Understanding the GA-4 New York form is crucial for municipal self-insured employers. However, several misconceptions can lead to confusion. Here are eight common misunderstandings:

Addressing these misconceptions can help ensure compliance and avoid unnecessary penalties. Understanding the requirements of the GA-4 form is essential for every municipal self-insured employer.

Here are key takeaways for completing and using the GA-4 New York form: