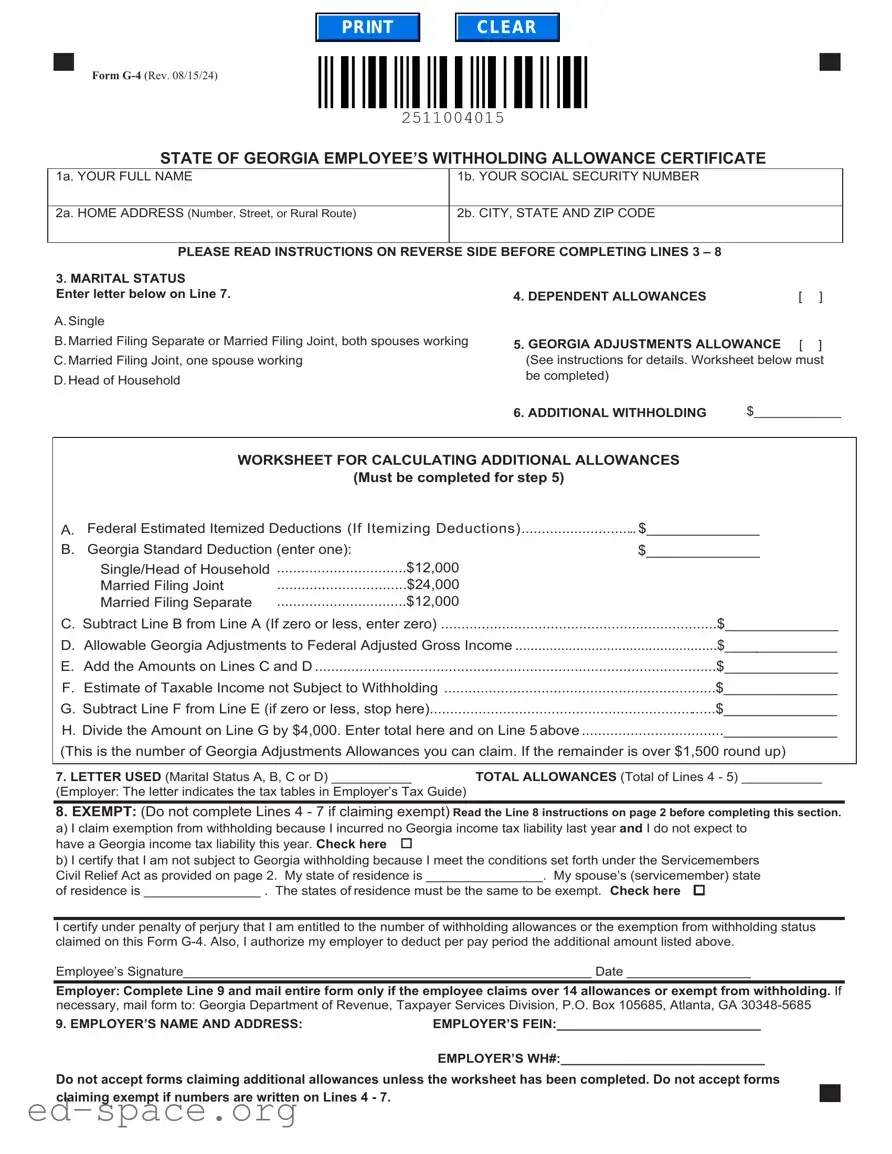

The G-4 Georgia form is an essential document for employees in Georgia, as it determines how much state income tax will be withheld from their paychecks. This form allows individuals to claim withholding allowances based on their marital status, dependents, and any additional allowances they may be eligible for. Employees must provide their full name, Social Security number, and home address at the top of the form. They will then indicate their marital status and the number of allowances they wish to claim. If applicable, they can also specify additional amounts to be withheld. The form includes a worksheet to help calculate additional allowances based on factors such as age, blindness, and allowable deductions. For those who qualify, there are options to claim exemption from withholding altogether. Completing the G-4 accurately is crucial, as failure to do so may result in the employer withholding tax as if the employee is single with zero allowances. Understanding the G-4 form can lead to more accurate tax withholding and potentially larger paychecks throughout the year.

CLEAR

Form

STATE OF GEORGIA EMPLOYEE’S WITHHOLDING ALLOWANCE CERTIFICATE

1a. YOUR FULL NAME |

1b. YOUR SOCIAL SECURITY NUMBER |

|

|

2a. HOME ADDRESS (Number, Street, or Rural Route) |

2b. CITY, STATE AND ZIP CODE |

PLEASE READ INSTRUCTIONS ON REVERSE SIDE BEFORE COMPLETING LINES 3 – 8

3. MARITAL STATUS

Enter letter below on Line 7.

A.Single

B.Married Filing Separate or Married Filing Joint, both spouses working

C.Married Filing Joint, one spouse working

D.Head of Household

4. DEPENDENT ALLOWANCES |

[ |

] |

5. GEORGIA ADJUSTMENTS ALLOWANCE [ |

] |

|

(See instructions for details. Worksheet below must |

||

be completed) |

|

|

6. ADDITIONAL WITHHOLDING |

$____________ |

|

WORKSHEET FOR CALCULATING ADDITIONAL ALLOWANCES

(Must be completed for step 5)

A. Federal Estimated Itemized Deductions (If Itemizing Deductions) |

$______________ |

|

B. Georgia Standard Deduction (enter................................one): |

$12,000 |

$______________ |

Single/Head of Household |

|

|

Married Filing Joint |

$24,000 |

|

Married Filing Separate |

$12,000 |

|

C. Subtract Line B from Line A (If zero or less, enter zero) |

$______________ |

D. Allowable Georgia Adjustments to Federal Adjusted Gross Income |

$______________ |

E. Add the Amounts on Lines C and D |

$______________ |

F. Estimate of Taxable Income not Subject to Withholding |

$______________ |

G. Subtract Line F from Line E (if zero or less, stop here) |

$______________ |

H. Divide the Amount on Line G by $4,000. Enter total here and on Line 5 above |

______________ |

(This is the number of Georgia Adjustments Allowances you can claim. If the remainder is over $1,500 round up)

7. LETTER USED (Marital Status A, B, C or D) ___________ |

TOTAL ALLOWANCES (Total of Lines 4 - 5) ___________ |

(Employer: The letter indicates the tax tables in Employer’s Tax Guide) |

|

8.EXEMPT: (Do not complete Lines 4 - 7 if claiming exempt) Read the Line 8 instructions on page 2 before completing this section. a) I claim exemption from withholding because I incurred no Georgia income tax liability last year and I do not expect to

have a Georgia income tax liability this year. Check here

b)I certify that I am not subject to Georgia withholding because I meet the conditions set forth under the Servicemembers Civil Relief Act as provided on page 2. My state of residence is ________________. My spouse’s (servicemember) state

of residence is ________________ . The states of residence must be the same to be exempt. Check here

I certify under penalty of perjury that I am entitled to the number of withholding allowances or the exemption from withholding status claimed on this Form

Employee’s Signature________________________________________________________ Date _________________

Employer: Complete Line 9 and mail entire form only if the employee claims over 14 allowances or exempt from withholding. If

necessary, mail form to: Georgia Department of Revenue, Taxpayer Services Division, P.O. Box 105685, Atlanta, GA

9. EMPLOYER’S NAME AND ADDRESS: |

EMPLOYER’S FEIN:____________________________ |

|

EMPLOYER’S WH#:____________________________ |

Do not accept forms claiming additional allowances unless the worksheet has been completed. Do not accept forms claiming exempt if numbers are written on Lines 4 - 7.

CLEAR

INSTRUCTIONS FOR COMPLETING FORM

Enter your full name, address and social security number in boxes 1a through 2b.

Line 3: Write the letter on Line 7 according to your marital status.

A.Single

B.Married Filing Separate or Married Filing Joint, both spouses working

C.Married Filing Joint, one spouse working

D.Head of Household

Line 4: Enter the number of dependent allowances you are entitled to claim. The term "dependent" shall have the same meaning as in the Internal Revenue Code of 1986; provided, however, that any unborn child with a detectable human heartbeat, as such terms are defined in Code Section

Line 5: Complete the worksheet on Form

Failure to complete and submit the worksheet will result in automatic denial on your claim.

Line 6: Enter a specific dollar amount that you authorize your employer to withhold in addition to the tax withheld based on your marital status and number of allowances.

Line 7: Enter the letter of your marital status from Line 3. Enter total of the numbers on Lines

a)Check the first box if you qualify to claim exempt from withholding. You can claim exempt if you filed a Georgia income tax return last year and the amount of Line 4 of Form 500EZ or Line 16 of Form 500 was zero, and you expect to file a Georgia tax return this year and will not have a tax liability. You cannot claim exempt if you did not file a Georgia income tax return for the previous tax year. Receiving a refund in the previous tax year does not qualify you to claim exempt.

EXAMPLES: Your employer withheld $500 of Georgia income tax from your wages. The amount on Line 4 of Form 500EZ (or Line 16 of Form 500) was $100. Your tax liability is the amount on Line 4 (or Line 16); therefore, you do not qualify to claim exempt.

Your employer withheld $500 of Georgia income tax from your wages. The amount on Line 4 of Form 500EZ (or Line 16 of Form 500) was $0 (zero). Your tax liability is the amount on Line 4 (or Line 16) and you filed a prior year income tax return; therefore you qualify to claim exempt.

b)Check the second box if you are not subject to Georgia withholding and meet the conditions set forth under the Servicemembers Civil Relief Act. Under the Act, a spouse of a servicemember may be exempt from Georgia income tax on income from services performed in Georgia if:

1.The servicemember is present in Georgia in compliance with military orders;

2.The spouse is in Georgia solely to be with the servicemember;

3.The servicemember maintains domicile in another state; and

4.The domicile of the spouse is the same as the domicile of the servicemember or the spouse of the servicemember has elected to use the same residence for purposes of taxation as the servicemember.

Additional information for employers regarding the Military Spouses Residency Relief Act:

1.On the

2.If the spouse of a servicemember is entitled to the protection of the Military Spouses Residency Relief Act in another state and files a withholding exemption form in such other state, the spouse is required to submit a Georgia Form

Worksheet for calculating additional allowances. Enter the information as requested by each line. For Line D, enter items such as Retirement Income Exclusion, U.S. Obligations, and other allowable deductions per Georgia Law, see the

Do not complete Lines

O.C.G.A. §

Employers are required to mail any Form

| Fact Name | Details |

|---|---|

| Form Purpose | The G-4 form is used in Georgia for employees to declare their withholding allowances, which affects the amount of state income tax withheld from their paychecks. |

| Governing Law | This form is governed by the Official Code of Georgia Annotated (O.C.G.A.) § 48-7-102, which mandates its completion for tax withholding purposes. |

| Marital Status Options | Employees can select from several marital statuses, including Single, Married Filing Joint, Married Filing Separate, and Head of Household, to determine their allowances. |

| Dependent Allowances | Line 4 of the form allows employees to claim allowances for dependents, which can further reduce their taxable income. |

| Additional Allowances | Employees may also claim additional allowances by completing a worksheet provided on the form, which helps calculate potential deductions. |

| Exemption Clauses | Employees may claim exemption from withholding if they had no Georgia income tax liability in the previous year and do not expect one for the current year. |

| Submission Requirements | Employers must mail the G-4 form to the Georgia Department of Revenue if an employee claims more than 14 allowances or is exempt from withholding. |

Completing the G-4 form is a necessary step for individuals working in Georgia to ensure that the correct amount of state income tax is withheld from their paychecks. Following the steps carefully will help in accurately reporting personal information and tax allowances.

After filling out the G-4 form, it is important to submit it to your employer. They will use this information to determine the correct withholding amounts from your pay. If you have any changes in your personal situation or tax status, you may need to update this form accordingly.

What is the purpose of the G-4 Georgia form?

The G-4 Georgia form is used by employees to declare their withholding allowances for state income tax. By completing this form, employees can adjust the amount of tax withheld from their paychecks based on their marital status, dependents, and other allowances. This helps ensure that the correct amount of state income tax is withheld throughout the year.

Who needs to fill out the G-4 form?

Any employee working in Georgia who wants to have state income tax withheld from their wages should complete the G-4 form. This includes new employees, those who experience changes in their personal situation, or anyone wishing to adjust their withholding allowances. It is essential to provide accurate information to avoid under- or over-withholding.

How do I determine the number of allowances to claim?

The number of allowances you can claim depends on your marital status and the number of dependents you have. The G-4 form provides specific instructions for each marital status category. For example, if you are single, you can enter either 0 or 1. If you are married and both spouses are working, you can also enter 0 or 1. You may need to complete the worksheet on the form to calculate additional allowances based on your specific financial situation.

What should I do if I want to claim exemption from withholding?

If you believe you qualify for exemption from withholding, you must check the appropriate box on Line 8 of the G-4 form. You can claim exemption if you had no Georgia income tax liability last year and do not expect to have one this year. If you are a spouse of a servicemember, you may also qualify under the Servicemembers Civil Relief Act. Make sure to read the instructions carefully before claiming exemption.

What happens if I do not submit a properly completed G-4 form?

If you fail to submit a properly completed G-4 form, your employer will withhold taxes as if you are single with zero allowances. This could lead to either too much or too little tax being withheld from your paycheck, which may affect your tax liability at the end of the year. It is crucial to ensure the form is filled out correctly and submitted on time.

Can I change my withholding allowances after submitting the G-4 form?

Yes, you can change your withholding allowances at any time by submitting a new G-4 form to your employer. This may be necessary if your personal or financial situation changes, such as getting married, having a child, or experiencing a change in income. Ensure that you complete the new form accurately to reflect your current situation.

What should employers do with the G-4 forms they receive?

Employers are required to review the G-4 forms for accuracy. They should honor the completed forms unless notified otherwise by the Georgia Department of Revenue. If an employee claims more than 14 allowances or claims exemption, the employer must mail the form to the Georgia Department of Revenue. Employers should keep the forms on file until a new form is submitted or until February 15 of the following year.

Missing Personal Information: Individuals often forget to fill in their full name, social security number, or address. This basic information is crucial for processing the form correctly.

Incorrect Marital Status: Selecting the wrong marital status can lead to inaccurate withholding allowances. It is essential to choose the option that reflects your current situation.

Neglecting Dependent Allowances: Some people overlook the section for dependent allowances. If you have dependents, not claiming them can result in higher tax withholding.

Skipping the Worksheet: Failing to complete the worksheet for additional allowances is a common mistake. Without this, any additional allowances claimed will be denied automatically.

Incorrect Additional Withholding Amount: Entering an incorrect dollar amount for additional withholding can lead to unexpected tax situations. Ensure that this amount is accurate and reflects your needs.

Claiming Exempt Incorrectly: Some individuals mistakenly claim exemption from withholding when they do not meet the criteria. Understanding the requirements is vital to avoid errors.

Not Signing the Form: A signature is required to validate the form. Forgetting to sign can delay processing and lead to complications with your employer.

When completing the G-4 Georgia form, several other forms and documents may be necessary to ensure accurate tax withholding and compliance with state regulations. Below is a list of commonly used documents that complement the G-4 form.

Understanding these documents can greatly assist in accurately completing the G-4 form and ensuring proper tax withholding. Always check for updates or changes to forms and guidelines to remain compliant with Georgia tax regulations.

When filling out the G-4 Georgia form, it's essential to follow specific guidelines to ensure accuracy and compliance. Below are six important dos and don'ts to keep in mind.

Here are some common misconceptions about the G-4 Georgia form, along with explanations to clarify them:

Filling out the G-4 form in Georgia is essential for managing your state income tax withholding. Here are some key takeaways to keep in mind:

Understanding these points can help ensure that your tax withholding aligns with your financial situation. Completing the G-4 form accurately is key to avoiding surprises during tax season.